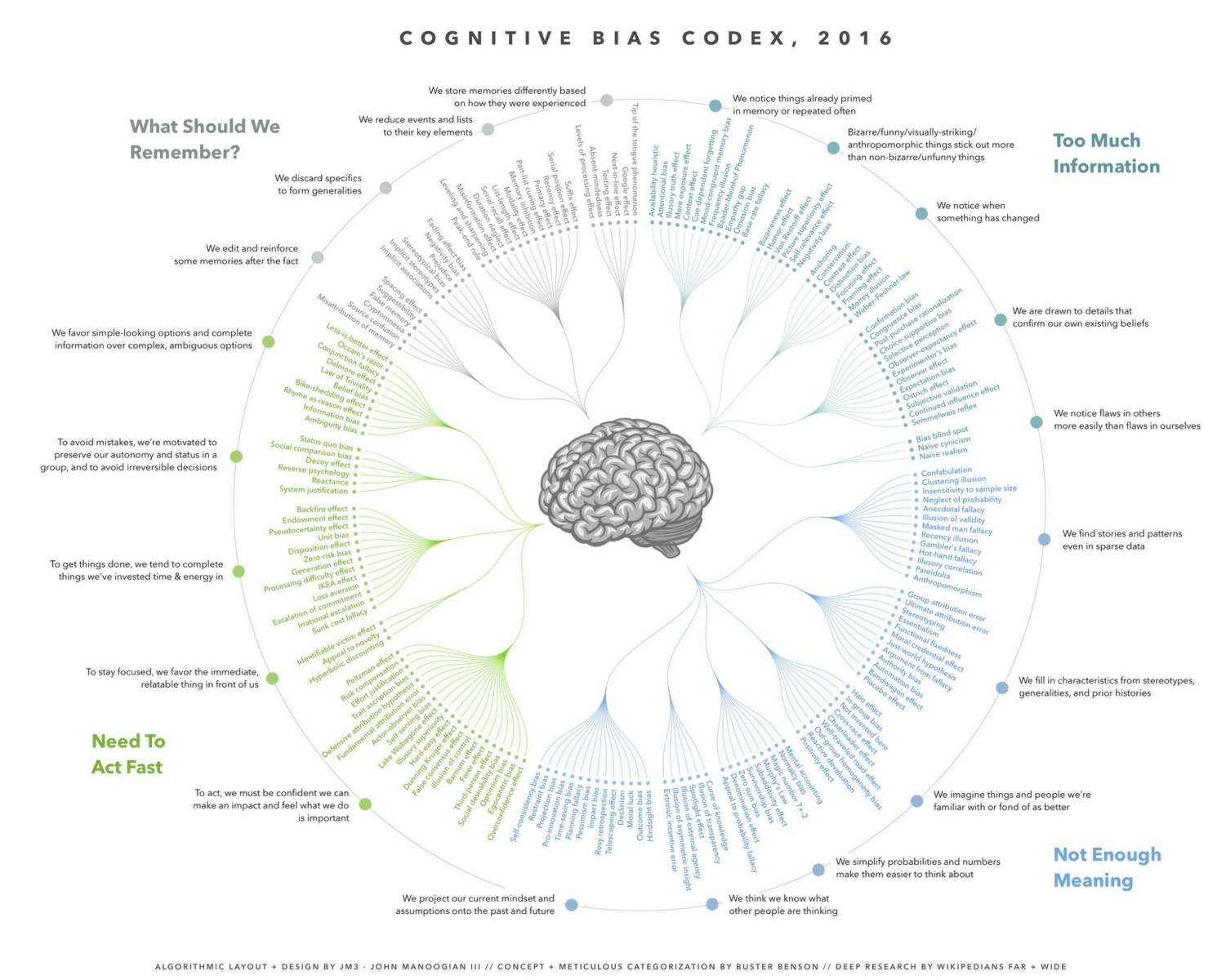

Musings on “Just Deserts” and the Opening of Plato’s Republic:

Greg Mankiw Defending the 1% proposes what he calls the “just deserts” theory of social justice:

What you have gained and hold by playing by the economic rules is yours: social justice consists in not cheating or injuring people, and not being cheated or injured in turn.

This is an old theory: we see it first in the western intellectual tradition nearly 2400 years ago, in the opening of the dialogue that is Plato’s Republic. It is advanced by Kephalos…

The other participants in Plato’s dialogue, led by Sokrates, conclude relatively quickly that Kephalos’s argument–taken up by his son Polymarkhos–is unphilosophical, and thus unworthy of consideration by those who want to gain a deep and true understanding of the subject. For the rest of the dialogue, Kephalos’s position–that justice consists of getting one’s just deserts: not injuring or cheating people, and not being injured or cheated–is abandoned. The live positions are, instead,

- That “justice” does not really exist: it is merely a rhetorical weapon with which the strong control the weak.

-

That justice consists of the right arrangement of human society, because a rightly arranged human society is an instrumental virtue that produces many many benefits.

-

That justice consists of the right arrangement of human society, a good and worthwhile thing both because of the other benefits it produces and a thing very much worth having in itself.

Ever since Plato, moral philosophers have followed his lead–or, rather, the lead of the characters in his dialogue–in this dismissal of “justice is neither cheating nor being cheated”. But, as Obama CEA Chair Jason Furman pointed out to me, that cannot be completely right. First, justice as what Mankiw calls “just deserts” has enormous psychological resonance for human beings. To the extent that moral philosophy exists to account for an help us understand the morality we human beings do have, dismissing a very large chunk of our moral intuitions as wrong simpliciter is not very helpful. Second, given that human beings have a strong tropism toward Kephalos’s “just deserts” position–that justice consists of not injuring or cheating people, and not being injured or cheated–anyone who tries to set out what a rightly arranged society is without taking account of this strong human psychological tropism will almost surely fail.

My tentative ideas on this are unfinished, and probably wrong.

But I would suggest that we might be thinking about the fact that humans are, at a very deep and basic level, gift-exchange animals. We create and reinforce our social bonds by establishing patterns of “owing” other people and by “being owed”. We want to enter into reciprocal gift-exchange relationships. We create and reinforce social bonds by giving each other presents. We like to give. We like to receive. We like neither to feel like cheaters nor to feel cheated. We like, instead, to feel embedded in networks of mutual reciprocal obligation. We don’t like being too much on the downside of the gift exchange: to have received much more than we have given in return makes us feel very small. We don’t like being too much on the upside of the gift exchange either: to give and give and give and never receive makes us feel like suckers.

We want to be neither cheaters nor saps. It is, psychologically, very hard for most of us to feel like we are being takers: that we are consuming more than we are contributing, and are in some way dependent on and recipients of the charity of others. It is also, psychologically, very hard for most of us to feel like we are being saps: that others are laughing at us as they toil not yet consume what we have produced.

And on top of this evopsych propensity to be gift-exchange animals–what Adam Smith called our “natural propensity to truck, barter, and exchange”–we have built our complex economic division of labor. We construct property and market exchange–what Adam Smith called our natural propensity “to truck, barter, and exchange” to set and regulate expectations of what the fair, non-cheater non-sap terms of gift-exchange over time are.

But we face a problem: How do we enter into a gift-exchange relationship with somebody we will never see again? And we have a solution: a cash-on-the-barrelhead exchange. We devise money as a substitute for the trust that in this transaction one is indeed in a gift-exchange relationship, rather than a sap being taken by a grifter.

And on top of this we have constructed a largely-peaceful global 7.4B-strong highly-productive societal division of labor, built on:

- assigning things to owners—who thus have both the responsibility for stewardship and the incentive to be good stewards…

- on very large-scale webs of win-win exchange…

- mediated and regulated by market prices…

There are enormous benefits to arranging things this way. As soon as we enter into a gift-exchange relationship with someone or something we will see again–perhaps often–it will automatically shade over into the friend zone. This is just who we are. And as soon as we think about entering into a gift-exchange relationship with someone, we think better of them. Thus a large and extended division of labor mediated by the market version of gift-exchange is a ver powerful creator of social harmony. This is what the wise Albert Hirschman called the doux commerce thesis.

Now it is certainly true that economists do not talk about this once. For example, in Books I and II of his Wealth of Nations, Adam Smith definitely does write as if self-interest mediated by exchange is at the foundation of the social order. But Adam Smith the moral philosopher (as opposed to Adam Smith the proto-economist attempting to disrupt the 18th century discipline of “political oeconomy”) does not believe that. And it is not true. People as economists conceive them are not “Hobbesians” focusing on their narrow personal self-interest, but rather “Lockeians”: believers in live-and-let live, respecting others and their spheres of autonomy and eager to enter into reciprocal gift-exchange relationships—both one-offs mediated by cash alone and longer-run ones as well. In an economist’s imagination, people do not enter a butcher’s shop only when armed cap-a-pie and only with armed guards, fearing that the butcher will not sell him meat for money but will, rather, knock him unconscious, take his money, slaughter him, smoke him, and sell him as long pig. Rather, there is a presumed underlying order of property and ownership that is largely self-enforcing, that requires only a “night watchman” to keep it stable and secure.

This extended pattern of independence is a very valuable piece of our societal capital.

Thus, given these psychological and institutional facts-on-the-ground, in my view any rightly arranged society has to successfully do all of:

- setting up a framework for the production of stuff…

- setting up a framework for the distribution of stuff…

- creating a very dense reciprocal network of interdependencies to create and reinforce our belief that we are all one society…

- and doing so in such a way that:

- people do not see themselves, are not seen as, and are not saps–people who are systematically and persistently taken advantage of by others in their societal and market gift-exchange relationships.

- people do not see themselves, are not seen as, and are not moochers–people who systematically persistently take advantage of others in their societal and market gift-exchange relationships.

Achieving these results is complicated and difficult, for reasons related to [the water-diamonds paradox][]. But I am now far afield, and need to get back to my main topic…

Cf., also:

{kind=link}