Do product innovations affect economic inequality? In a new working paper published today, I find that shifts in income distribution in the United States lead to product innovations that target high-income households, which increases purchasing-power inequality. Such product innovations have both a direct effect on purchasing power across income groups because they target specific groups, as well as an indirect effect through competition with products already in the marketplace.

In short, wealthier households are more likely to spend on product categories where product innovations are more common and where competition is increasing, while low- and middle-income households are more likely to purchase products that face less competitive pricing pressures in the marketplace. For economic policymakers, this dynamic has important implications for the price indexation of government programs that provide support for low- and middle-income families.

New Working Paper

The unequal gains from product innovations: Evidence from the US retail sector

Here’s the new fact

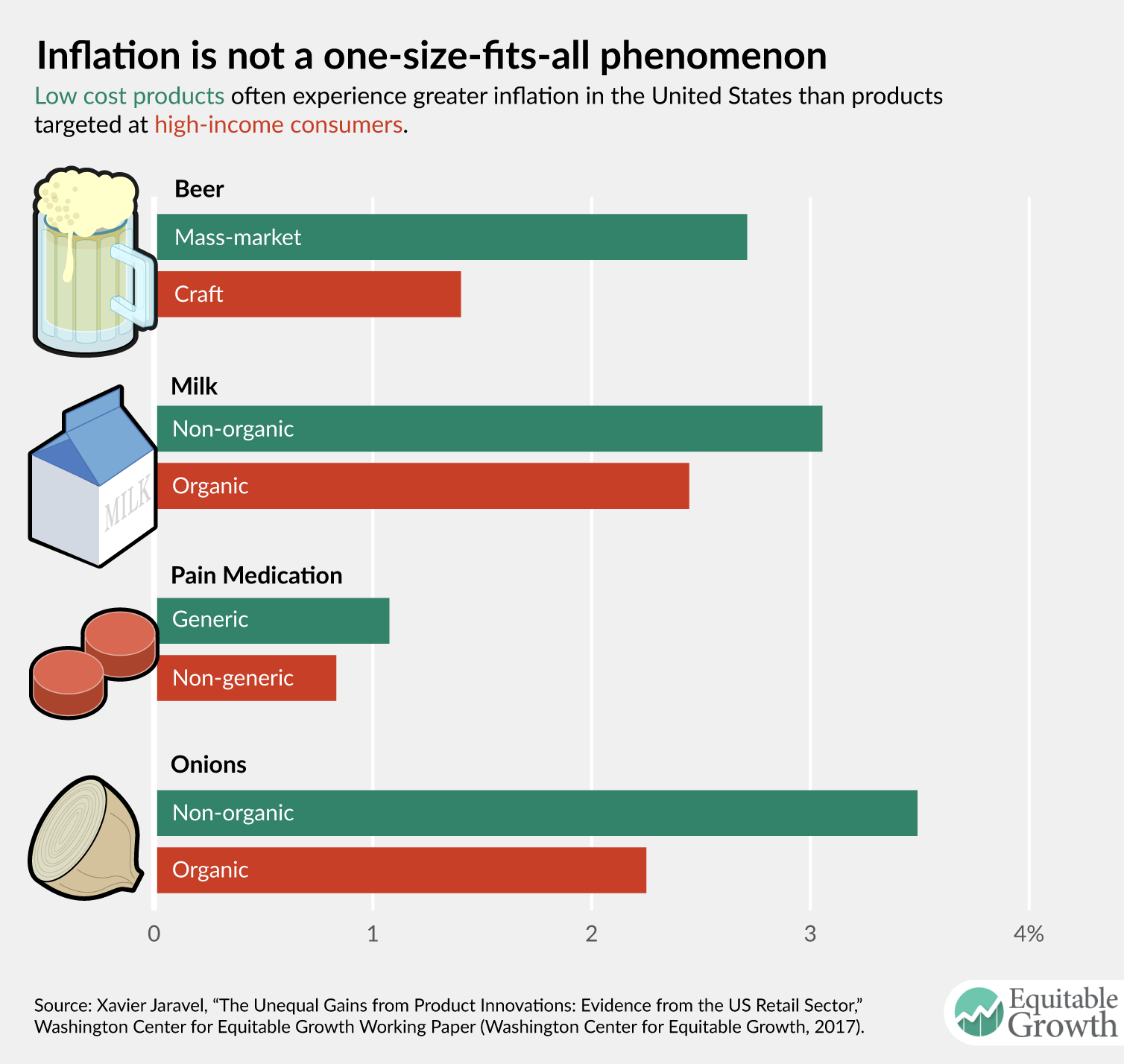

In the first part of my analysis, I measure how the introduction of new products and price changes on existing products affect economic inequality in a setting where very detailed data are available. I examine scanner data recorded at cash registers in the U.S. retail sector between 2004 and 2015—covering broad product categories, including food, alcohol, beauty and health, general merchandise, and household supplies, all of which account for 15 percent of household expenditures. I find that product categories predominantly consumed by high-income households—such as organic food, craft beer, and branded drugs—feature higher levels of product innovations (measured by entry of new products) and lower levels of inflation (measured using price changes on already existing products).

The accompanying infographic charts how this dynamic plays out in the marketplace for four everyday consumer products. (See Figure 1.)

Figure 1

Taking into account the 3 million products in the database, these price effects are large. In the U.S. retail sector, annual inflation was 0.65 percentage points lower for households earning more than $100,000 per year, relative to households making less than $30,000 per year. The current methodology used by statistical agencies, including the U.S. Department of Labor’s Bureau of Labor Statistics, cannot capture this difference, which arises primarily because income groups differ in their spending patterns along the quality ladder within detailed item categories. (BLS currently collects data measuring income-group-specific spending patterns across broad item categories, leading to aggregation bias.)

Explaining the new fact

In the second part of my analysis, I find that the patterns of product innovations and inflation inequality in the U.S. retail sector resulted from the response of firms to so-called market-size effects. Specifically:

- The demand for products consumed by high-income households increased because of growth and rising income inequality.

- In response, firms introduced more new products catering to such households.

- As a result, already existing products in these market segments lowered their price due to increased competitive pressure.

To establish empirically the causal effect of increasing demand on firms’ product innovations, I study the effect of changes in demand resulting from shifts in the national income and age distributions over time. I find that increasing demand in a market segment leads to the introduction of more new products and lower inflation for already existing products due to increasing competitive pressure. For instance, in the case of craft beer, new varieties of craft beer are constantly being introduced, and this increase in competition keeps inflation low for existing varieties of craft beer, while competition is more stable and inflation is higher for more longstanding products in the market such as mass-produced beer.

Implications

The results of the analysis suggest that two trends are at work in the U.S. economy today. First, economic inequality has increased faster than is commonly thought because of the dynamics of product innovations and inflation. And second, rising income inequality has an amplification effect because when high-income households get richer, firms strategically introduce more new products catering to these consumers, which increases inequality further.

One limitation of the analysis is that it primarily covers the U.S. retail sector only from 2004 to 2015. Yet I find a similar trend of lower inflation for higher-income households when considering the full consumption basket of U.S. households going back to 1953 using data from the Consumer Price Index and the Consumer Expenditure Survey.

Moreover, the results from the U.S. retail sector have direct implications for the indexation of various government safety-net programs that are currently indexed to the food Consumer Price Index such as the U.S. Department of Agriculture’s Supplemental Nutrition Assistance Program (also known as food stamps). Based on the sample of goods examined in my research, I find that indexation of the benefits on the food Consumer Price Index implies an increase in nominal food stamp benefits of 24.8 percent between 2004 and 2015. In contrast, indexation of the benefits on the relevant food price index for households eligible for supplemental nutrition assistance would imply a much higher increase of 35.5 percent because these households effectively face a higher food inflation rate.

—Xavier Jaravel is a post-doctoral fellow in economics at Stanford University.

Download File

031417-jaravel-product-innovation

Read the full PDF in your browser