- Larry Summers: The Best Books on Globalization: “[The Economic Consequences of the Peace][] by John Maynard Keynes…

- Timothy Burke: Fighting for the Ancien Regime: “We were… part of the system…

- Ezra Klein: Trump’s weak closing argument on health care — and why it matters: “President Trump’s closing argument was weak…

- David Anderson: The Individual Market Under AHCA V2: “What [could] the individual insurance market could look like under the AHCA as rumored to be as of 0030, March 23, 2017[?]…

- Alan de Bromhead et al.: When Britain turned inward: “[To what] extent… [was] trade policy… responsible…

- Caitlin MacNeal: Mulvaney: If Your State Doesn’t Mandate Maternity Care, Change Your State: “Budget Director Mick Mulvaney… brushed off concerns about… repeal[ing] the Essential Health Benefits requirement….

- Ray Dalio et al.: Populism: The Phenomenon: “This report is an examination of populism, the phenomenon…

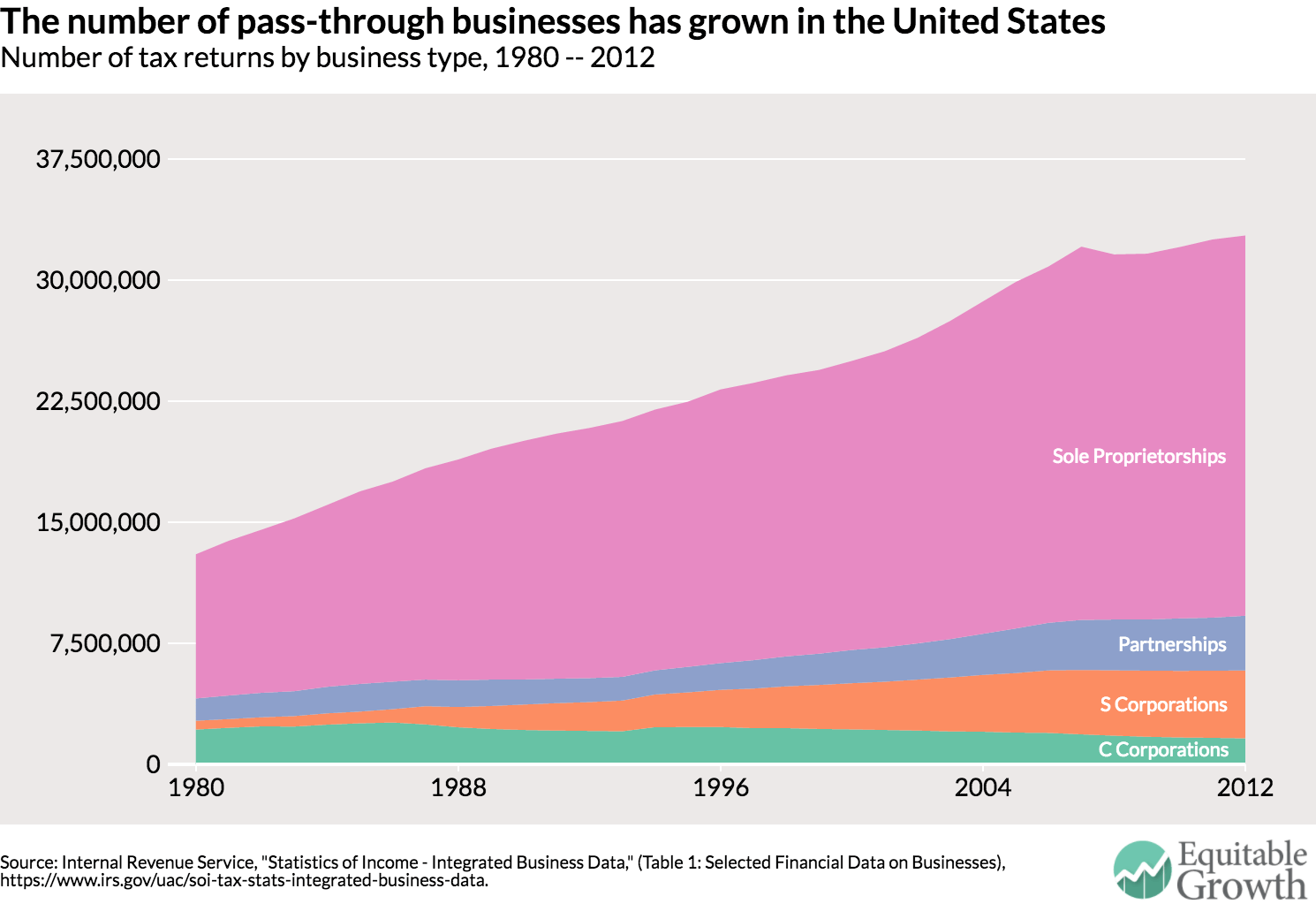

Interesting Reads:

- Ryan Avent: The Productivity Paradox

- Paul Krugman: Robot Geometry

- Heather Boushey, J. Bradford DeLong, Marshall Steinbaum: After Piketty: The Agenda for Economics and Inequality

- Jason Furman: Trump promised 4 percent growth. Here’s why we’d be very lucky to hit 3

- Mike Konczal: Why Banking Leverage Requirements Are Not Enough

- Nouriel Roubini: Markets overestimating Donald Trump policy positives

- Pranab Bardhan: State and Development: The Need for a Reappraisal of Current Literature

- Martin Wolf: There is more than one explanation for the fall in sterling

- Notes: What Does President Donald Trump Mean for the US Economy?

- Sequel of the Return of Rise of the Robots Again

- FIRST DRAFT: Review for “Nature” of “A Culture of Growth”, by Joel Mokyr

- Are There Benefits from Free Trade?: DeLong FAQ

- Will Somebody Please Tell Me Why the Federal Reserve Has Embarked on a Tightening Cycle Again?:

- AP: No House vote on GOP health care bill today: “Canceling Thursday’s vote would amount to a significant political setback for Trump and House Speaker Paul Ryan…

- Jonathan Chait: Mitch McConnell’s Trumpcare Plan Is to Lose Fast: “Mitch McConnell has laid out a wildly aggressive time frame…