The Trump administration (I won’t say “Donald Trump”, because I am not convinced that Donald Trump knows what the Congressional Budget Office is) wants people to take on the CBO’s projections that real GDP growth is likely to average a hair less than 2 percent per year.

And professional Republicans John Cogan of Stanford, Glenn Hubbard of Columbia, John Taylor of Stanford, and Kevin Warsh of Stanford deliver.

Michael Strain provides them with a warning—which they do not and will not heed:

Michael Strain: Stop Bashing the CBO, Republicans: “A word to the wise from a fellow conservative: Expert analysis isn’t your problem; bad legislation is… https://www.bloomberg.com/view/articles/2017-08-01/stop-bashing-the-cbo-republicans

…The nonpartisan agency… was the subject of a bizarre attack ad by the White House last month. Mick Mulvaney, President Donald Trump’s budget director, has publicly questioned whether “the day of the CBO” has “come and gone.” Former House speaker Newt Gingrich recently advocated: “Abolish CBO. It is totally destructive. It is totally dishonest.” Last week, members of the House Freedom Caucus authored amendments that would cut the CBO’s funding in half and eliminate the division responsible for producing cost estimates of legislation…. The GOP is unwise to delegitimize the CBO even out of pure political self-interest. The agency frequently produces analysis that Democrats could live without…. Republicans are in power now, but they won’t be forever…

And Michael offers advice on how to criticize the CBO:

I often find myself thinking a particular CBO analysis is a little off base, that I would have used different assumptions, or done the analysis differently. There is often significant uncertainty in analysis as ambitious as that frequently produced by the CBO. And it would be good for the CBO to be more transparent about its analysis and with its models…

In short: Present a better analysis than the CBO does! And argue your case!

This is advice which Cogan, Hubbard, Taylor, and Warsh do not follow.

As best as I can see, their critique of CBO is not what I would recognize as an analysis of CBO’s growth estimates, or, indeed, any other sort of quantitative and reality-based growth-accounting exercise. It is, rather, a few stray sentences like:

The data are not supportive of the popular contention that the United States is in the midst of a long-term decline in productivity growth…

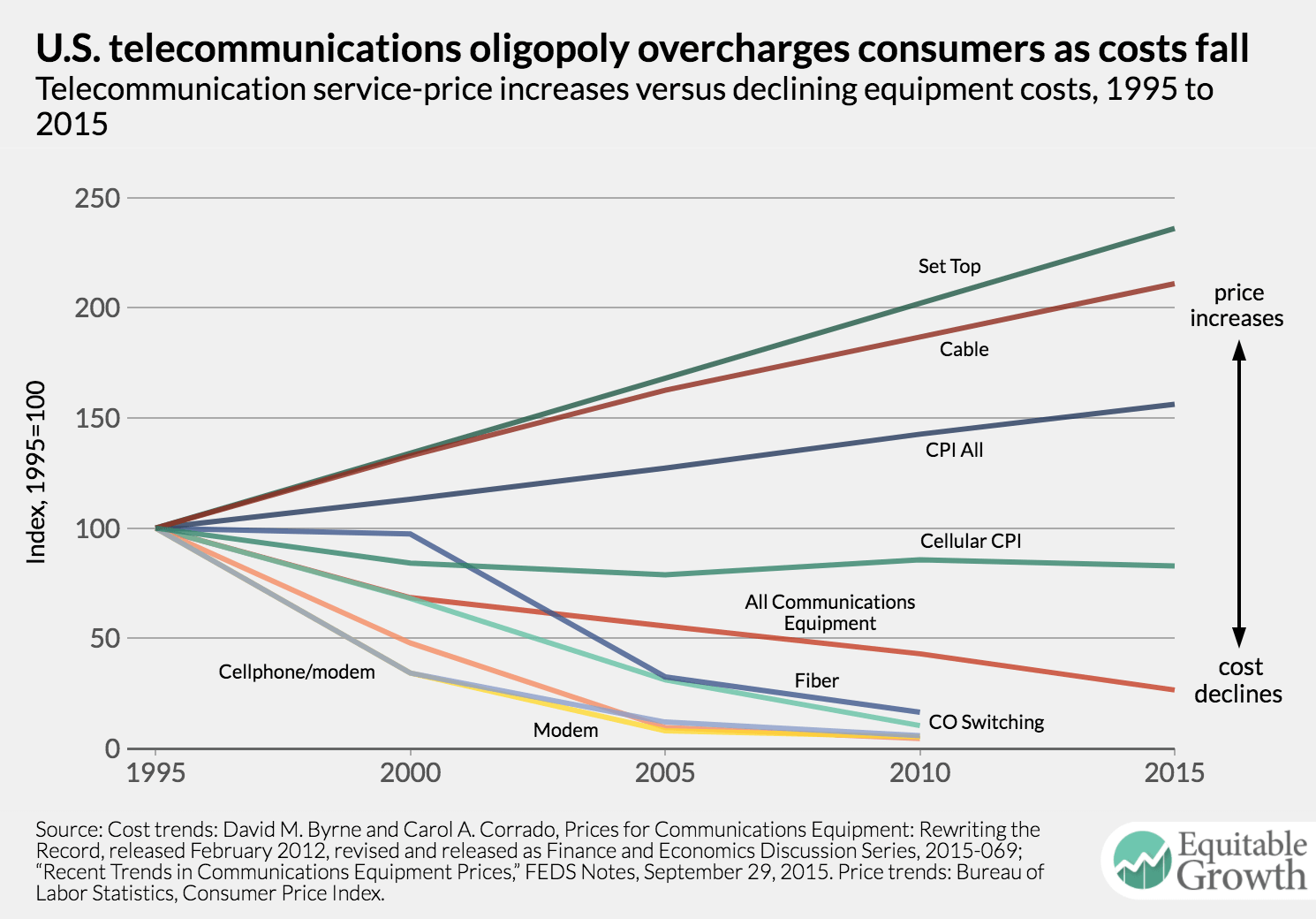

supported by a fake graph—the one on the left, when they should be plotting something much more like the one on the right:

Drawing random arrows to try to fool naive readers into thinking that statistical trends are things that they are not is not something that should be done by anybody I would call an economist.

So what is to be done about this degradation of public discourse? Commenters at Bloomberg have ideas and observations:

Mark Buchanan: Economists Are Cheating Their Profession: “Ideology remains a problem… https://www.bloomberg.com/view/articles/2017-08-01/economists-are-cheating-their-profession

…“Economic theory and historical experience,” it boldly asserts, “indicate economic policies are the primary cause of both the productivity slowdown and the poorly performing labor market.” This willfully misrepresents current thinking. Economists hold diverse views on the roots of the recent malaise, and remain divided and uncertain about the fundamental causes of growth…. When professional economists write as experts and claim theory as a basis for their views, they also have a duty to present that theory—and other economists’ thoughts about it—honestly. Their failure to do so is “unprofessional,” as University of California at Berkeley economist Brad DeLong rightly put it….

What, if anything, [will] the profession… do about it[?] Does it have standards? If so, can it enforce them?… How can the profession combat such capture? [Luigi] Zingales has suggested public shaming, following the example of media efforts such as the film “Inside Job”…. Shaming seems appropriate. After all, public trust is a resource from which all economists benefit. If they want to preserve it, they should draw guidance from Nobel Prize winner Elinor Ostrom. She showed that successful management of such resources typically requires an effective means to maintain group standards and values—for example, by punishing and deterring self-serving behavior…

Noah Smith: Supply-Siders Still Push What Doesn’t Work: “Few critics have focused on what I see as the weakest part of Cogan et al.’s essay… https://www.bloomberg.com/view/articles/2017-08-01/supply-siders-still-push-what-doesn-t-work

…the claim that lower taxes, deregulation and reduced government spending can boost growth significantly. Tax cuts have generally proven to be a big bust…. The most glaring example is Kansas Governor Sam Brownback….

On deregulation, I’m much more sympathetic to the supply-sider concerns. Some regulations are probably hurting economic dynamism by protecting incumbent industries, while others would fail a cost-benefit test. But other regulations probably help the economy…. It’s no easy job to tell the good regulations from the bad. The Trump administration has promised to tackle this thorny problem, but given its record of general ineffectiveness, there’s no reason to assume, as Cogan et al. do, that it will make wise choices….

As for fiscal austerity, there is no reason to think that any further gains can be made there…. Basic economic theory says that low deficits boost growth by lowering long-term interest rates — but with rates already near record lows, there isn’t much scope for improvement in this regard…

Justin Fox: Yes, Financial Crises Do Bring Hangovers: “I was struck by the second paragraph of the piece, written by John F. Cogan, Glenn Hubbard, John B. Taylor and Kevin Warsh… https://www.bloomberg.com/view/articles/2017-07-20/yes-financial-crises-do-bring-hangovers

…The view that periods of weak economic growth tend to follow major financial crises rests heavily on the work of Harvard economists Carmen Reinhart and Kenneth Rogoff…. After I wrote a column in March that relied heavily on Reinhart and Rogoff’s research, the abovementioned John B. Taylor responded thusly:

Old hangover theory of weak recovery http://bloom.bg/2nxEJSI @foxjust was demolished by Bordo http://on.wsj.com/2mT5cHa others. Problem=policy

Hmm, I thought when I saw that. There were financial crises of 1973 and 1981? Yes, there were a couple of prominent bank failures in the U.S. in the wake of the 1973-74 and 1981-82 recessions (Franklin National Bank in 1974 and Continental Illinois in 1984), but they certainly didn’t cause those recessions. The 1990 recession did occur in the midst of the long-running U.S. savings and loan crisis, but a) it was followed by a really weak recovery and b) that crisis, however painful, was still nowhere near as dire as the global shock of 2008.

When I looked at… Bordo and… Haubrich… my puzzlement did not abate…. Nobody in the 1890s thought the aftereffects of 1893 were modest and brief. The recovery that followed the recession that started in 1929… was indeed quite impressive, but it didn’t start until 1933…. That’s why they call it the Great Depression, people!

In sum, I find Reinhart-Rogoff much more convincing than Bordo-Haubrich. This doesn’t mean that economic hangovers following financial crises are inevitable…. But… Bordo came nowhere near “demolishing” the hangover theory…

Cogan, Hubbard, Taylor, and Warsh is not a contribution to the economic literature either on growth-accounting trends or on the effects of financial crises, it is not a summary and survey of either of the two literatures, and it is not a better analysis of what the future economic growth baseline should be than CBO has provided. So what do these professors and fellows from Stanford and Columbia think they are doing, if not providing ammunition for what Michael Strain has correctly identified as an extraordinarily dubious enterprise? And why are they doing it?

Key takeaways

Key takeaways