New research finds capital gains are highly concentrated and hardly taxed, underscoring widespread U.S. inequality

For two decades, booming stock, housing, and private business markets have driven large capital gains in the United States. Real capital gains, which are the inflation-adjusted appreciation of a financial or physical asset, have averaged 20 percent of national income over the past two decades, compared to 5 percent prior to 1980. In 2021 alone, according to calculations using IRS and financial accounts data, capital gains totaled almost $6 trillion—a whopping 39.2 percent of national income.

Clearly, capital gains are becoming increasingly relevant to many U.S. households’ bottom lines. But who is actually receiving this money? And how does it affect already-widespread inequality in the United States? Our new working paper, which was funded in part by the Washington Center for Equitable Growth, seeks to answer these questions.

Capital gains are different than other forms of income for two reasons. First, they are extraordinarily concentrated, mostly flowing to the top income percentiles. And second, they are difficult to measure, which is partly why most studies of inequality do not include capital gains as part of their income series.

Using internal IRS tax return data, under a data-use agreement with the IRS under the Joint Statistical Research Program, our paper studies the distribution of capital gains in the United States and their contribution to both income inequality and tax progressivity. Using IRS data offers many advantages—the data are comprehensive, spanning the entire income distribution and wealth distribution in the United States.

At the same time, however, only realized sales of assets are reported on tax forms since the United States only taxes capital gains upon realization—though not all realized sales are taxed (for example, taxes are deferred on the return to assets held in retirement accounts, and the first $250,000 of a gain from the sale of a primary home is exempted entirely). This means a large portion of total appreciation, or the sum of unrealized and realized capital gains, is unreported in these data.

Specifically, between 1954 and 2021, $116 trillion in total capital gains were accrued, but less than 20 percent of that was reported on tax forms and subject to taxation. We cannot say with certainty whether the remaining 80 percent of gains will ever be taxed in the future (e.g., if they are sold in taxable accounts at any point after 2021). But much of these assets will likely escape taxation, thanks to avoidance strategies such as the so-called stepped-up basis rule that allows tax-free bequeaths of unsold stock to heirs. Due to these strategies, using taxed capital gains is therefore a poor proxy for total capital gains.

To overcome this limitation of realized gains, we utilize a three-step approach to more accurately estimate total capital gains: We link individuals to their portfolio holdings to ensure accurate valuation; capitalize income to estimate their wealth; and estimate capital appreciation by multiplying wealth by price appreciation in asset-class-specific returns—specifically, in public equities, private equities, owner-occupied housing, tenant-occupied housing, and pension assets.

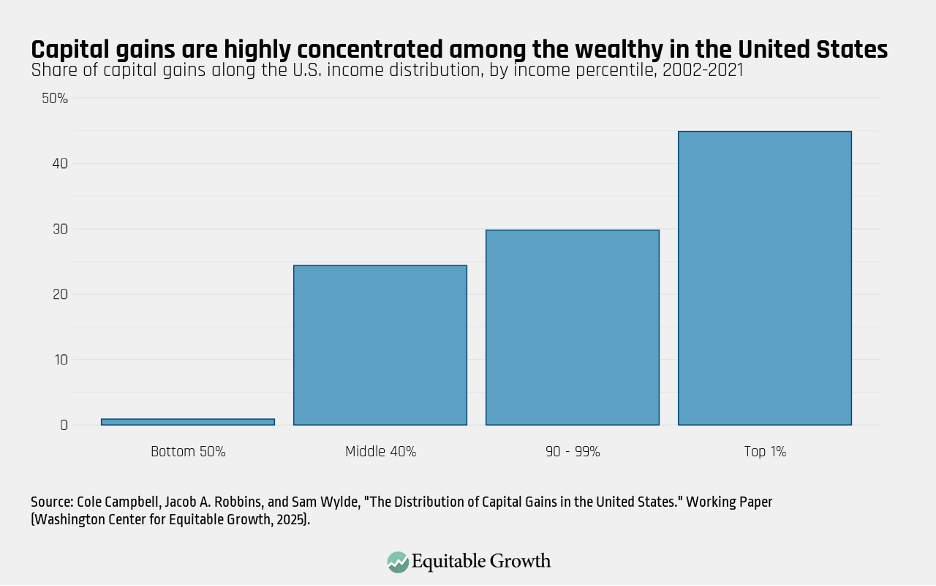

Upon doing so, we find that capital gains are both large and highly concentrated. Indeed, they are the most concentrated form of income in the United States. Overall, the top 1 percent of the income distribution received 45.3 percent of capital gains from 2002 to 2021, and the top 10 percent received three-quarters of capital gains (75.7 percent). (See Figure 1.)

Figure 1

In fact, capital gains are so concentrated that they have a substantial impact on levels of inequality when included in calculations of income distribution in the United States. Our results show that the top 1 percent’s share of total U.S. income increases from 18 percent without capital gains to 21 percent with gains included. The top 10 percent of individuals receive 45 percent of income without gains, compared to almost 48 percent with capital gains included.

Accounting for capital gains also makes the U.S. tax system less progressive. Overall, as indicated above, only a small proportion of capital gains are taxed. We find this results in an effective tax rate on real capital gains of 5.2 percent—significantly below the statutory rate of between 15 percent and 20 percent depending on income level.

Because capital gains are concentrated in the top 10 percent of the income distribution, the average tax rate on income is lower for higher-income groups when capital gains are included, leading to an all-in tax rate that is essentially flat across the income distribution. We find that the middle 40 percent of the income distribution pays an average rate of 27.3 percent, the 90th to 99th percentile pays 27 percent, and the top 1 percent pays 26.8 percent. Further, we find that the top 0.01 percent pays 25.5 percent.

Lastly, we find that returns on capital gains exhibit marked differences across income levels. Richer individuals, for example, tend to have higher returns on real estate. This is because they tend to live in “superstar” cities, which have flourished over the past two decades. The private business wealth of the rich also sells for a premium because these businesses are large and more liquid, increasing their value, and they tend to be in industries, such as manufacturing, that investors prefer. This heterogeneity makes a material difference in measures of overall income and wealth inequality.

Our new working paper highlights the distributive impacts of capital gains, which almost entirely benefit the top 10 percent, and the current disparate treatment of capital gains income, which has a low effective tax rate. These findings are directly relevant to tax policy—particularly the debate around capital gains taxation, in which potential revenue gains are often pitted against the administrability of a more comprehensive capital tax system, such as a mark-to-market tax on unrealized gains, or what is sometimes called a Billionaires Income Tax, as well as possible effects on entrepreneurship.

Our paper suggests that the wealthy have long shielded capital gains from taxation and that raising substantial revenue from a capital gains tax would require closing certain loopholes in the tax code. As tax policy debates occur throughout 2025 in the U.S. Congress, policymakers interested in raising revenue, reducing income inequality, and making the tax code more progressive should keep these implications in mind.

Did you find this content informative and engaging?

Get updates and stay in tune with U.S. economic inequality and growth!