Moving from Federal Pandemic Unemployment Compensation to a job losers’ stimulus program amid the coronavirus recession

Overview

The coronavirus recession is shattering businesses and dramatically increasing unemployment, which hit 14.7 percent in April 2020, the highest level since 1948.1 So far, the federal government has delivered a one-time cash stimulus to most households and increased the amount of unemployment benefits for workers who have lost their jobs through no fault of their own through a program called Federal Pandemic Unemployment Compensation. But individuals and households affected by the coronavirus pandemic and ensuing recession will continue to need support even after it is safe for businesses to reopen. The federal government should therefore consider allowing people who have lost their jobs to keep their expanded unemployment benefits when they go back to work for as long as they could have collected these benefits by staying unemployed.

My proposed policy, the job losers’ stimulus program, is a cash stimulus for workers who have lost their jobs regardless of whether they remain unemployed or find new employment. Compared to only providing higher unemployment benefits to the unemployed, the job losers’ stimulus program boasts the twin benefits of providing greater support to workers who have been most affected by pandemic-related job losses while also modestly increasing overall employment. The exact size of the impact of this new stimulus program is difficult to predict, but a simple policy simulation shows that it could increase the amount of stimulus by 34 percent and allow an additional 6 percent of workers to exit unemployment and return to work within 4 months of losing their jobs.

The job losers’ stimulus program would strengthen the fiscal stimulus at a critical time for economic recovery and would create jobs and raise Gross Domestic Product by increasing consumer demand.2 This is especially important as consumer demand is low during the pandemic, which already led to price decreases as of April 2020.3 Such price decreases can lead to a deflationary spiral in which businesses are cash-strapped and must lay off workers, leading to even lower consumer demand and further price decreases down the road. Beyond these macroeconomic effects, the job losers’ stimulus program also directly benefits job losers and their families: The literature shows that an unconditional cash transfer has many positive effects, in particular on children’s education and health outcomes.4

Download FileMoving from Federal Pandemic Unemployment Compensation to a job losers’ stimulus program amid the coronavirus recession

The job losers’ stimulus program would also have positive effects on the U.S. labor market, allowing workers to return to work when the economy can safely reopen without losing precious income. Typically, Unemployment Insurance benefits do not replace all of a worker’s lost income, but the federal move to expand benefits by $600 per week during the pandemic as part of the Coronavirus Aid, Relief, and Economic Security, or CARES, Act means that some workers are receiving more in unemployment benefits than they earned while employed. Instead of taking away these important benefits from workers when the economic recovery is fragile, the job losers’ stimulus program would allow them to keep these benefits as they start working again and make more money overall than if they stayed unemployed.

Unemployment Insurance benefits are a powerful fiscal stimulus during times of low consumer demand

An increase in federal government spending during a recession can increase GDP by more than the value of that spending—in some cases, almost doubling the amount of the original stimulus. This multiplier effect occurs when consumer demand is low. In April of this year, for example, the price of clothing decreased by 4.7 percent because there was not enough demand.5 When it is safe to reopen, a cash stimulus can increase consumers’ demand for clothing and create jobs in the clothing retail industry. These extra jobs then lead to more people having higher incomes and spending on more clothes, as well as other goods and services, multiplying the impact of the original cash stimulus.

The multiplier effect for Unemployment Insurance is at least 1.7, meaning that a $100 increase in government spending leads to $70 additional GDP in the private sector.6 This 1.7 multiplier effect is based on the effect of fiscal stimulus during the Great Recession of 2007–2009. The expansion of Unemployment Insurance during the Great Recession had an even greater impact—about 1.9, which means that every $100 spent on Unemployment Insurance led to $90 additional GDP value.7

The job losers’ stimulus program would build on this success by giving additional cash to formerly unemployed workers after they find a new job or otherwise return to work. In doing so, the job losers’ stimulus increases the size of the stimulus at a time when it can have the greatest impact, and the effect of each additional dollar can be calculated using the fiscal multiplier.

Increasing Unemployment Insurance has little effect on overall employment levels during a deep recession

In a booming economy, when there are jobs to be had, increasing unemployment benefits can moderately increase the length of time workers remain unemployed. Overall, the literature shows that a 10 percent increase in benefits increases unemployment duration by 5 percent. This 0.5 elasticity is the average in the U.S. literature.8

Yet increasing unemployment benefits generally produces less of an effect on unemployment duration during a recession. The literature on Unemployment Insurance shows both theoretically and empirically that the impact of Unemployment Insurance on employment levels in a recession is smaller than in a boom.9 For instance, while more generous Unemployment Insurance can reduce job applications, this may not increase unemployment much if jobs are in short supply to begin with.10 A randomized controlled trial shows that increasing job search intensity in a depressed labor market has little effect on overall unemployment because job seekers engage in a rat race, where they are stealing jobs away from each other.11

But how small is the elasticity of unemployment with respect to unemployment benefits during the current recession? It is almost certainly smaller than the average elasticity estimated in the U.S. literature of about 0.5. Using data from the Great Recession, I have shown that the effects of Unemployment Insurance on aggregate unemployment are 40 percent smaller than the micro effects on individual behavior.12 If we apply this reduction to the 0.5 elasticity from the literature, we obtain an elasticity of 0.3.13

Because the coronavirus recession is particularly deep, the elasticity could be even less than 0.3—potentially close to zero. Indeed, a careful quasi-experimental identification strategy finds no statistically significant effect of benefit extensions on aggregate unemployment during the Great Recession.14

The job losers’ stimulus program would help newly employed workers while allowing those still unemployed to search for the right job

When Unemployment Insurance does increase the duration of unemployment, it does so for two main reasons. The first (and most commonly discussed) reason is what economists call “moral hazard,” where workers are less likely to return to work because doing so will make them lose their unemployment benefits. The other reason, called the “liquidity effect,” is that unemployment benefits give unemployed workers enough money to live on so that they can afford to wait for a reasonable job, instead of being so desperate that they must take the first job opportunity they find to avoid severe financial hardship. Research by Harvard University economist Raj Chetty shows that the effect of Unemployment Insurance on employment is about 60 percent due to the liquidity effect.15

Because the job losers’ stimulus program would ensure that workers continue to receive unemployment benefits after returning to work, it only has a liquidity effect. In other words, it removes any potential disincentive to return to work, neutralizing the moral hazard concern, but continues to support job searchers who are looking for an appropriate match.

What does this mean for the potential impact of the job losers’ stimulus? We know that the elasticity due to liquidity effects is only 60 percent of the overall elasticity of unemployment with respect to unemployment benefits. If the elasticity is 0.5 to begin with, then the liquidity effect elasticity is only 0.3, calculated as 0.50.6=0.3. If the elasticity is already only 0.3, as I argued is more realistic in this recession, then the liquidity effect elasticity is just 0.18, calculated as 0.30.6=0.18. Therefore, the effect of moving from the extra Unemployment Insurance benefit to the equivalent job losers’ stimulus removes the moral hazard effect and only maintains a liquidity effect, thereby lowering the elasticity from 0.3 to 0.18.

Putting it all together: Simulated policy impact

We can predict the likely impact of the job losers’ stimulus by calculating a simulation of the program if it were hypothetically implemented. To begin, we assume that the reference policy is to give a $600 weekly additional benefit to the insured unemployed only, and for up to 4 months starting at the beginning of the unemployment spell. The 4-month period was chosen because the Federal Pandemic Unemployment Compensation, or FPUC, program created by the CARES Act ends on July 31, 2020, which is 4 months after the act was passed.

To simulate the impact of the proposed job losers’ stimulus program, I examine the difference it makes relative to the reference policy I just described. The reference policy is different from the actual FPUC program because the reference policy is not limited in time; for my purposes, I will assume that a worker who loses his or her job in May can collect Federal Pandemic Unemployment Compensation for 4 months until September 2020 instead of having the benefit cut in July. In contrast, I assume that the job losers’ stimulus program allows all covered unemployed workers to receive $600 a week for 4 months, whether they remain unemployed or not.

I start with the unemployment survival rate that would prevail in the absence of any extra $600 weekly FPUC benefit. This allows policymakers to know, after each month of unemployment, what percent of originally unemployed people are still unemployed. To predict how the extra $600 a week for the unemployed affects unemployment duration, I apply the elasticity of unemployment with respect to unemployment benefits to the survival function for each of the first 4 months of unemployment. For simplicity, I assume that from the fifth month on, the unemployment survival function converges back to what it would have been without the Federal Pandemic Unemployment Compensation benefit.

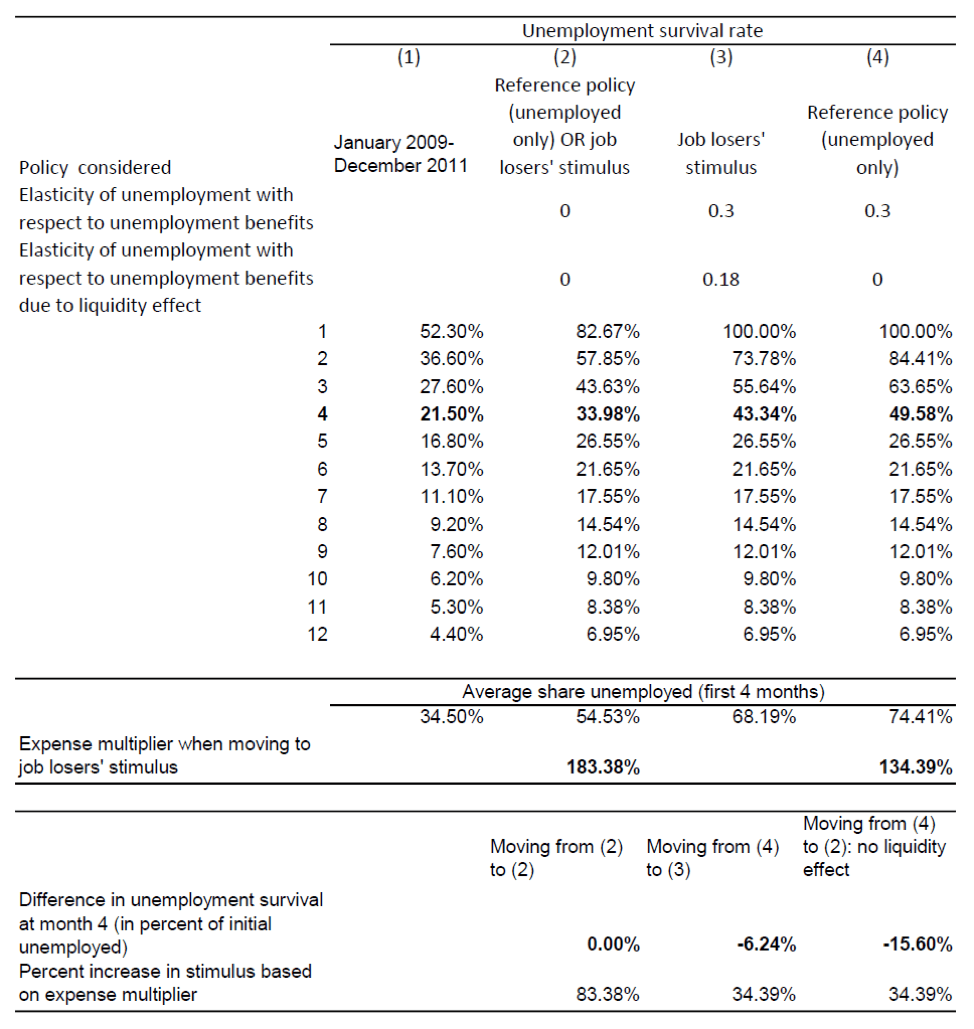

Next, I examine how moving from the reference policy to the job losers’ stimulus program affects the amount of stimulus and unemployment. To figure out the extra amount of stimulus, I use the elasticity-adjusted survival function calculated in the prior step. (See the Table in the Appendix.) Taking the average over the first 4 months shows the share, out of the initial job losers, who are still unemployed and receive the job losers’ stimulus benefits over the first 4 months of the spell. One minus this average gives us the share of those who are no longer unemployed and receive benefits—this is the size of the extra stimulus because the benefits are expanded to those who are no longer unemployed.

Once the increase in stimulus is known, its effect on the economy can be calculated using the fiscal multiplier discussed above.

What about the effect of the job losers’ stimulus program on unemployment? The job losers’ stimulus only has a liquidity effect and no moral hazard effect. Therefore, it’s important to compare the unemployment survival rate in the first 4 months for the reference policy, which includes both a moral hazard and a liquidity effect, to the unemployment survival rate for the job losers’ stimulus, which includes only a liquidity effect. Because the liquidity elasticity is smaller than the overall elasticity, unemployment necessarily decreases with the job losers’ stimulus, and more people return to work.

Empirically, not all workers exiting unemployment return to work. Some people will leave the labor force entirely. But as these exits usually occur later on in the unemployment spell, policymakers can reasonably assume that all those who exit unemployment in the first 4 months do so because they are returning to work.

To implement this calculation, I first take the unemployment survival function during the Great Recession. Using the Current Population Survey gives me the survival function for unemployment spells for Unemployment Insurance-eligible workers in January 2009 to December 201116; I reproduce these numbers in column 1 of Table 1 in the Appendix. During that period, the unemployment rate was, on average, 9.3 percent, using the data from the St. Louis Federal Reserve.17 In April 2020, the unemployment rate was 14.7 percent, and this is before any effects of the extra $600 weekly benefit could have reasonably increased unemployment duration. I, therefore, inflate the unemployment survival rate by an amount proportional to the ratio of the unemployment rates between the two periods.18 I reproduce the inflated unemployment survival rate in column 2 in the upper panel of Table 1 in the Appendix. I then take this survival function to be the unemployment survival function in the absence of $600 a week extra unemployment benefits, or if the elasticity of unemployment with respect to benefit levels is zero.

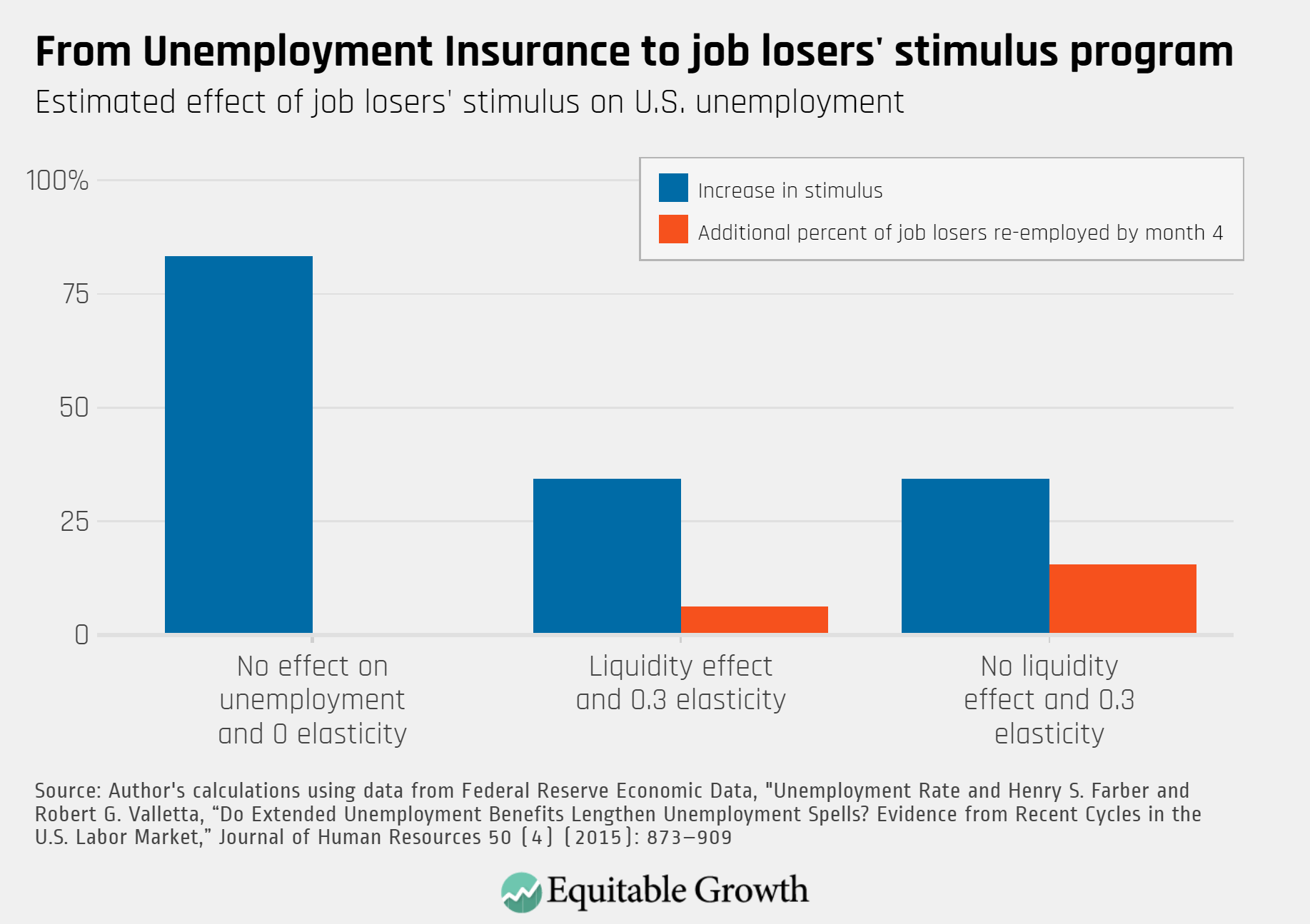

The exact size of the impact of the job losers’ stimulus is difficult to predict, but the relative size of each of these benefits follows a highly predictable pattern. If the effect of the job losers’ stimulus on unemployment is smaller, then the stimulus effect is larger, and vice versa. (See Figure 1.)

Figure 1

Let’s look at the effect of the job losers’ stimulus through how it would affect a worker with the median annual wage of $40,000, according to Consumer Population Survey data for 2019. This median worker receives $393 in weekly unemployment benefits in a typical state such as Pennsylvania. Adding the $600 Federal Pandemic Unemployment Compensation benefit is an increase of 153 percent.

I then calculate the proportional increase in cash stimulus and the extra share of the initially unemployed who exit unemployment and return to work using the procedure outlined above. I consider three scenarios, summarized in Figure 1. The underlying full calculations are in Table 1 in the Appendix. Specifically:

- In the first scenario, the benefit increase has no effect on unemployment. In this case, the unemployment survival rate does not change (it stays as it is in column 2 in Table 1 in the Appendix), and the stimulus effect is maximum, with an 83 percent increase in the stimulus due to those job losers finding jobs within 4 months also receiving benefits.

- In the second scenario, the elasticity of unemployment duration with respect to benefit extensions is 0.3, and there is a liquidity effect: 60 percent of the elasticity is due to a liquidity effect, so the effective elasticity is 0.18, calculated as 0.3*0.6=0.18. In this case, the stimulus effect is lower, with a 34.39 percent increase in the stimulus. In contrast, now there is an effect on unemployment—an additional 6.24 percent of the initial job losers return to work within 4 months. (See the survival rate in month 4 in column 4 versus column 3 of Table 1 in the Appendix.)

- In the third scenario, the elasticity of unemployment duration with respect to benefit extensions is 0.3, and there is no liquidity effect—in other words, the whole of the elasticity is explained by moral hazard. In this case, the job losers’ stimulus—which removes moral hazard effects—has no effect at all, not even a liquidity effect, on unemployment duration. Therefore, the job losers’ stimulus now decreases unemployment more than in the second scenario—an additional 15.6 percent of job losers return to employment within 4 months. (See the survival rate in month 4 in column 4 versus column 2 of Table 1 in the Appendix.) The stimulus effect is the same as in scenario 2 above, a 34.39 percent increase in stimulus, because the stimulus effect only depends on the overall elasticity, not the liquidity effect.

Therefore, comparing column 2 and column 4 in Table 1 in the Appendix demonstrates that the higher the unemployment survival function is (meaning that unemployment duration is longer), the smaller the stimulus effect is because there are fewer people who are no longer unemployed and will also receive the benefits. For the same reason, a higher elasticity leads to a lower stimulus effect because a higher elasticity increases the unemployment survival rate, and so there are fewer re-employed people who can benefit.

Let’s take scenario 2 as an example to see how we can calculate the dollar amount for the stimulus effect and the number of job losers who return to work within 4 months based on our estimates. In scenario 2, the stimulus increases by 34.39 percent. The Congressional Budget Office currently projects that the extra $600 a week will cost $176 billion.19 If I take this number as the baseline, then the increase in stimulus is $61.42 billion.20 With a fiscal multiplier of 1.9, this would create an additional $55.28 billion in economic activity.21 At the same time, an additional 6.24 percent of the insured unemployed now find a job within 4 months.

Given that there were 18.9 million insured unemployed on April 18, and most of those entered unemployment in April, then an estimated 1.18 million job losers would return to work within 4 months due to the job losers’ stimulus.22

Conclusion

Overall, then, moving from the Federal Pandemic Unemployment Compensation to the job losers’ stimulus program would provide more income to workers who lost their jobs during the coronavirus recession. It would strengthen the much-needed stimulus to the economy while also allowing more unemployed workers to return to work when it is safe to do so.

—Ioana Marinescu is an assistant professor of economics at the University of Pennsylvania.

Appendix

Table 1

Notes: In the upper panel, the unemployment survival rate in column 1 is from (Farber and Valletta 2015), Table 3. In column 2, the survival rate is multiplied by 14.7/9.3 to account for the fact that the unemployment rate was 14.7% in April 2020 vs. 9.3% in January 2009-January 2011. In column 3, the survival rate from column 2 for months 1-4 is multiplied by the elasticity 0.18 and by 153%, which is the increase in weekly benefit levels; in month 1, the survival rate is slightly above 100%, so I truncate it to 100%. In column 4, the survival rate from column 2 for months 1-4 is multiplied by the elasticity 0.3 and by 153%, which is the increase in weekly benefit levels; in month 1, the survival rate is slightly above 100%, so I truncate it to 100%.

In the middle panel, the average share unemployed in the first 4 months is the simple average of the survival rate in months 1-4. The expense multiplier when moving to job losers’ stimulus is the inverse of the average survival rate in months 1/4.

In the bottom panel, we can calculate the effect of moving from unemployment benefits to job losers’ stimulus under different assumptions as described by column headings. The 34.39% in column 3 is not a mistake but represents the fact that moving to job losers’ stimulus allows job seekers who would have been reemployed under unemployment insurance (in col. 4) to also receive the job losers’ benefit.

End Notes

1. “Unemployment Rate,” available at https://fred.stlouisfed.org/series/UNRATE (last accessed June 4, 2020).

2. Gabriel Chodorow-Reich, “Geographic Cross-Sectional Fiscal Spending Multipliers: What Have We Learned?” American Economic Journal: Economic Policy 11 (2) (2019): 1–34, available at https://www.aeaweb.org/articles?id=10.1257/pol.20160465; Marco Di Maggio and Amir Kermani,“The Importance of Unemployment Insurance as an Automatic Stabilizer.” Working Paper no. 22625 (National Bureau of Economic Research 2016).

3. U.S. Bureau of Labor Statistics, “Consumer Price Index Summary – April 2020” (2020), available at https://www.bls.gov/news.release/cpi.nr0.htm.

4. Ioana Marinescu, “No Strings Attached: The Behavioral Effects of U.S. Unconditional Cash Transfer Programs.” Working Paper no. 24337 (National Bureau of Economic Research, 2018).

5. U.S. Bureau of Labor Statistics, “Consumer Price Index Summary – April 2020.”

6. Chodorow-Reich, “Geographic Cross-Sectional Fiscal Spending Multipliers: What Have We Learned?”

7. Maggio and Kermani, “The Importance of Unemployment Insurance as an Automatic Stabilizer.”

8. Johannes F. Schmieder and Till von Wachter, “The Effects of Unemployment Insurance Benefits: New Evidence and Interpretation,” Annual Review of Economics 8 (1) (2016): 547–81, available at http://www.econ.ucla.edu/tvwachter/papers/annualreview_UI_wp_2016_08_15.pdf.

9. Camille Landais, Pascal Michaillat, and Emmanuel Saez, “A Macroeconomic Approach to Optimal Unemployment Insurance: Theory,” American Economic Journal: Economic Policy 10 (2) (2018): 182–216, available at https://www.aeaweb.org/articles?id=10.1257/pol.20150088; Johannes F. Schmieder, Till von Wachter, and Stefan Bender, “The Effects of Extended Unemployment Insurance Over the Business Cycle: Evidence from Regression Discontinuity Estimates Over 20 Years,” The Quarterly Journal of Economics 127 (2) (2012): 701–52, available at https://academic.oup.com/qje/article-abstract/127/2/701/1825004; Kory Kroft and Matthew J. Notowidigdo, “Should Unemployment Insurance Vary with the Unemployment Rate? Theory and Evidence,” The Review of Economic Studies 83 (3) (2016): 1092–1124, available at https://academic.oup.com/restud/article-abstract/83/3/1092/2461292; Ioana Marinescu, “The General Equilibrium Impacts of Unemployment Insurance: Evidence from a Large Online Job Board,” Journal of Public Economics 150 (2017): 14–29, available at https://www.nber.org/papers/w22447#:~:text=Using%20data%20from%20the%20large,jobs%2C%20a%20general%20equilibrium%20effect; Camille Landais, Pascal Michaillat, and Emmanuel Saez, “A Macroeconomic Approach to Optimal Unemployment Insurance: Applications,” American Economic Journal: Economic Policy 10 (2) (2018): 182–216, available at https://www.aeaweb.org/articles?id=10.1257/pol.20160462.

10. Marinescu, “The General Equilibrium Impacts of Unemployment Insurance: Evidence from a Large Online Job Board”; Ioana Marinescu, Ioana Elena, and Daphné Skandalis, “Unemployment Insurance and Job Search Behavior.” SSRN Scholarly Paper ID 3303367 (Social Science Research Network, 2019), available at https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3303367#:~:text=Unemployment%20insurance%20(UI)%20helps%20workers,behavior%20due%20to%20moral%20hazard.&text=We%20show%20that%2C%20in%20the,their%20target%20wage%20by%203.5%25.

11. Bruno Crépon and others, “Do Labor Market Policies Have Displacement Effects? Evidence from a Clustered Randomized Experiment,” The Quarterly Journal of Economics 128 (2) (2013): 531–80, available at https://www.nber.org/papers/w18597.

12. Marinescu, “The General Equilibrium Impacts of Unemployment Insurance: Evidence from a Large Online Job Board.”

13. Calculated as 0.5*0.6=0.3.

14. Gabriel Chodorow-Reich, John Coglianese, and Loukas Karabarbounis, “The Macro Effects of Unemployment Benefit Extensions: A Measurement Error Approach,” The Quarterly Journal of Economics 134 (1) (2019): 227–79, available at https://academic.oup.com/qje/article-abstract/134/1/227/5076383?redirectedFrom=fulltext.

15. Raj Chetty, “Moral Hazard versus Liquidity and Optimal Unemployment Insurance,” Journal of Political Economy 116 (2) (2018): 173–234, available at https://dash.harvard.edu/bitstream/handle/1/9751256/Chetty_MoralHazard.pdf.

16. Henry S. Farber and Robert G. Valletta, “Do Extended Unemployment Benefits Lengthen Unemployment Spells? Evidence from Recent Cycles in the U.S. Labor Market,” Journal of Human Resources 50 (4) (2015): 873–909, table 3, available at http://jhr.uwpress.org/content/50/4/873.short.

17. “Unemployment Rate,” available at https://fred.stlouisfed.org/series/UNRATE (last accessed June 4, 2020).

18. Farber and Valletta, “Do Extended Unemployment Benefits Lengthen Unemployment Spells? Evidence from Recent Cycles in the U.S. Labor Market.”

19. CARES Act, Public Law 116-136, 116th Cong. (March 27, 2020), available at https://www.cbo.gov/publication/56334.

20. Calculated as 176*34.9%.

21. Maggio and Kermani, “The Importance of Unemployment Insurance as an Automatic Stabilizer.”

22. Calculated as 6.24%*18.9 million.