Unusually warm weather over much of the United States helped boost employment growth in December as the U.S. economy added 292,000 jobs, according to the Bureau of Labor Statistics. Wages also rose by 2.5 percent compared to a year ago while the unemployment rate stayed the same at 5.0 percent.

Although wages seemed as though they might be beginning to accelerate significantly in recent months, revisions to prior data suggest more modest growth. Both the year-over-year change and the change over the past three months place U.S. annual wage growth at 2.5 percent, well below healthy wage growth targets of 3.5 to 4.0 percent. Because wages were actually flat or falling this month compared to last month, this anomaly may be reversed in future revisions to show somewhat higher wage growth.

Widely spread across different industries, employment growth in December also appeared to respond in part to the unexpected warm temperatures. The Northeast, Midwest, and South all saw exceptionally warm weather last month, with 29 states experiencing their warmest average temperature on record. Partly as a result, the construction industry gained 45,000 jobs and restaurants grew by 36,900 workers. Reported employment for these sectors may be depressed in subsequent months if the good weather simply pulled forward hiring plans. Retail, however, only added 4,300 jobs—perhaps more hurt by the warm winter weather, which depresses sales as customers avoid purchasing winter apparel. The manufacturing sector also only grew by 8,000 jobs last month, negatively affected by the relatively strong dollar, which makes U.S. exports more expensive.

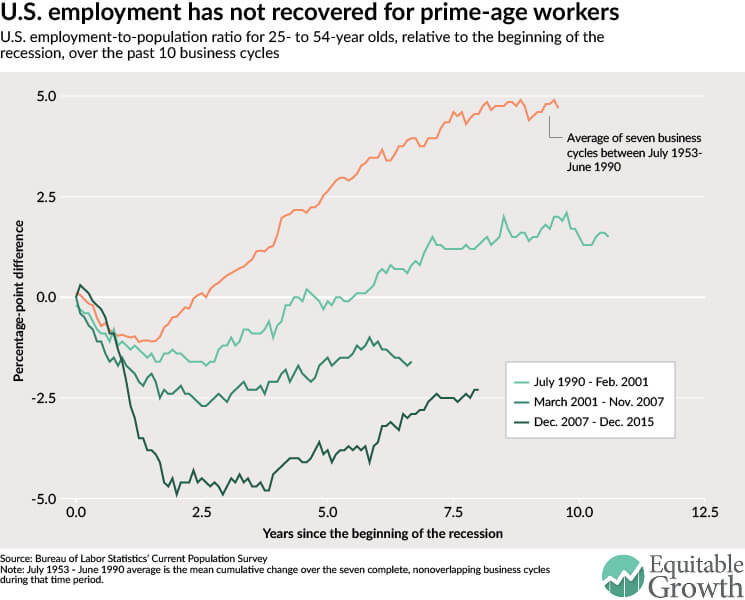

Recent job gains have had a small positive impact on the prime-age workforce, or those between 25 and 54 years old. The employed share of the nation’s prime-age population is now at 77.4 percent, unchanged from last month and up only about 0.3 percentage points compared to a year ago. Compared to other business cycles, the labor market recovery for prime-age workers has been particularly weak. At the historical pace of recovery in all but the past two business cycles, prime-age employment would have recovered by now to its pre-recession levels. Today’s prime-age employment rate, however, is about 2.3 percentage points below its value of 79.7 percent just before the official onset of the Great Recession of 2007–2009. (See Figure 1.)

Figure 1

The past two years have been the only years since 2005 when the U.S. economy’s monthly job growth exceeded 200,000 jobs on average, but employment growth was somewhat slower in 2015 compared to 2014. After nearly hitting the 200,000-a-month mark in 2013, employment growth accelerated in 2014 to add nearly 260,000 jobs each month. During 2015, however, the monthly pace of job creation slowed to about 221,000. The slowdown is apparent even when we focus on the most recent quarter and include the strong job gains of October and December. The average monthly employment growth over the quarter was about 284,000, yet over the last three months of 2014, gains averaged about 324,000.

The Federal Reserve’s recent interest rate hike will additionally dampen employment growth and make it more difficult for workers to secure economically meaningful wage gains, but these effects will likely occur with a significant lag. In the near term, next month’s employment report will reflect some of the initial impact of state and city minimum wage changes that occurred in January. Fourteen states and several cities and localities raised their minimum wages around the first of this month. Consequently, we should expect to see some stronger-than-usual wage growth in the leisure and hospitality sector, and also possibly in retail establishments, since these two industries intensively employ low-wage workers.

Photo of “Now Hiring” sign by Tess Aquarium, flickr, cc

{kind=link}