The uneasiness over the “fade-out” effect of early childhood education programs in the United States certainly isn’t, well, fading out. There’s an ever-growing body of evidence that demonstrates the substantial individual, familial, and social benefits from investments in high-quality early childhood education programs, yet naysayers continue to argue that the academic gains of attending preschool dissipate in primary school, making it an ineffective policy strategy. These naysayers, unfortunately, focus only on a small subset of the medium-term effects of early education programs while ignoring both the full range of their effects and their long-run impacts.

Over the past few months, the early education pessimists have been egged on by a recent study from Mark Lipsey, Dale Farran, and Kerry Hofer of Vanderbilt University. Using a randomized control trial, the three researchers appraise the academic and behavioral outcomes—through literacy, language, and math assessments and teacher-rating instruments—of students who attended Tennessee’s Voluntary Prekindergarten program. Upon entry into kindergarten, the prekindergarten participants scored significantly higher on cognitive test scores than did the non-participants. The researchers, however, chart that after entry into kindergarten, the academic achievement gap between students who had attended the prekindergarten program and those who hadn’t begins to narrow. By third grade, children who had attended the Voluntary Prekindergarten program had test scores that were similar to those of their non-attending counterparts.

In short, the study, like some others before it, documents a fade-out in the “cognitive skills” thought to be developed by a preschool education.

But there are several problems in using the third grade outcomes of the Tennessee Voluntary Prekindergarten program to disparage investment in high-quality early education. First of all, the Tennessee program is not what most researchers define as “high quality.” This is important to note because the cognitive effects are larger and the fade-out effects are less pronounced in high-quality programs. As a consequence, the achievement gaps between participants and non-participants in high-quality programs may diminish, but they do not disappear.

Many scholars also note that the so-called fade-out of academic achievement should be more accurately described as a convergence between the cognitive achievement of preschool-goers and their peers as non-attendees catch up, not as a “fading” away of benefits. But, regardless of how you frame it, there’s something troubling about measuring the effectiveness of preschool as a policy lever through just the cognitive aptitude of third graders: Test scores simply don’t paint the whole picture.

Instead, the appeal of implementing high-quality prekindergarten programs lies in their long-term benefits, largely generated by the interaction of both “cognitive” and “non-cognitive” skills. Non-cognitive skills are the non-technical habits or skills, such as emotional intelligence, character, and grit, all of which play an important role in the life-long success of an individual. According to research by Melissa Tooley and Laura Bornfreund of the New America foundation, a high-quality prekindergarten environment and education can teach or nurture these traits early on.

Over time, well-developed cognitive and non-cognitive skills often help determine how successful a student will be later on in life. More specifically, longitudinal studies on programs such as the Chicago Child-Parent Center have found that attending a high-quality early childhood education interventions can:

- Reduce grade retention rates

- Reduce a student’s reliance on special education services

- Increase a student’s odds of completing high school

- Improve college attendance post-high school

- Decrease a child’s exposure to abuse and neglect and, subsequently, welfare services

- Decrease the potential for juvenile or adult arrest

- Reduce the incidence of major depressive disorder

- Decrease adult smoking rates

- Increase a student’s earnings later in life

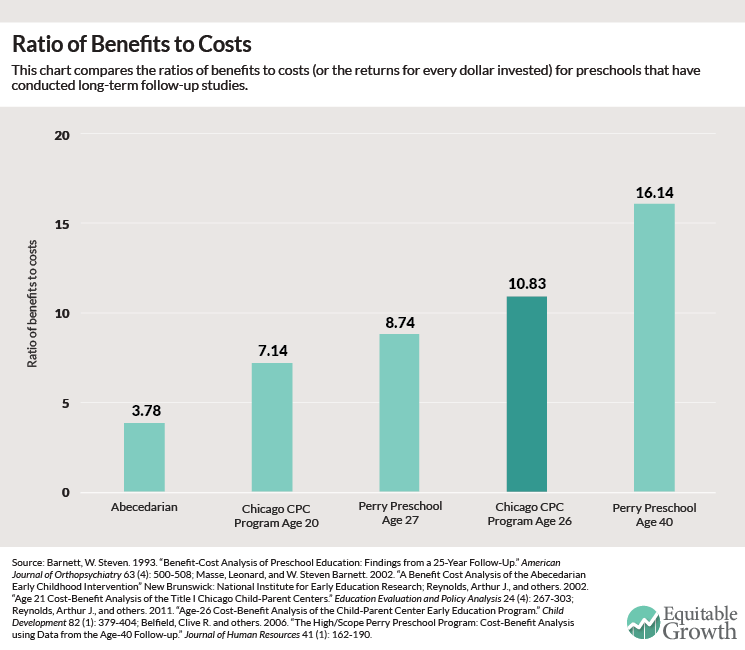

These benefits are by no means comprehensive, but they are demonstrative of the types of measures that can appropriately characterize the effectiveness of preschool programs. Instead of “fading,” many of these benefits persist and even “accentuate” over time. The benefit-cost ratio, for example, has been growing over time in the cases of the Chicago Child-Parent Center program and another famous longitudinal study involving the Perry Preschool program. In fact, because these outcomes are quantifiable, we can analyze the benefits and costs of preschool program investments.

In a report released last year by the Washington Center for Equitable Growth, researchers found that if the United States were to invest in a public, voluntary, high-quality universal prekindergarten program for 3- and 4-year-olds modeled on the Chicago Child-Parent Center (studied by Arthur Reynolds and colleagues) in 2016, the program would break even in eight years, and by 2050, it would return $8.90 for every dollar invested in it. That amounts to approximately $270.3 billion in net benefits in 2050, split among savings to government, increased compensation for students and their guardians, and individual savings due to less crime and better health. In other words, as a policy tool for improving socioeconomic outcomes, a high-quality universal prekindergarten program could more than pay for itself in the long-run.

Academics and policymakers need to be more mindful about how they measure the success of high-quality prekindergarten programs and then study their policy efficacy. The partial fade-out of cognitive skills alone cannot be an indicator of whether preschool is effective. But, at the same time, policymakers cannot disqualify concerns about the achievement gap diminishing in spite of substantial initial cognitive gains due to preschool programs’ high quality. The fade-out of cognitive achievement may be highlighting an important mismatch in our educational system—the quality of early childhood education may be high, yet the quality of primary school remains important in sustaining the gains.

{kind=link}