This is a weekly post we publish on Fridays with links to articles that touch on economic inequality and growth. The first section is a round-up of what Equitable Growth published this week and the second is the work we’re highlighting from elsewhere. We won’t be the first to share these articles, but we hope by taking a look back at the whole week, we can put them in context.

Equitable Growth round-up

Building off a piece from last week, Nick Bunker takes a second look at a new research on income inequality in the United States, which explores some reasons for why one-year income inequality has increased while lifetime income inequality has not changed too much.

Equitable Growth released two new working papers, one of which takes a look at the consequences that bad credit reports have on credit and the labor market, while the other discusses some of the contradictions present in a well-known critique of Keynesian economics.

Researchers and policymakers generally agree that the benefits of early childhood education make it a worthwhile investment in the United States. But there is much less agreement on how to build high-quality programs and sustain the cognitive gains made in preschool. Kavya Vaghul explains that another important consideration that is often missing from the conversation is preschool classroom diversity.

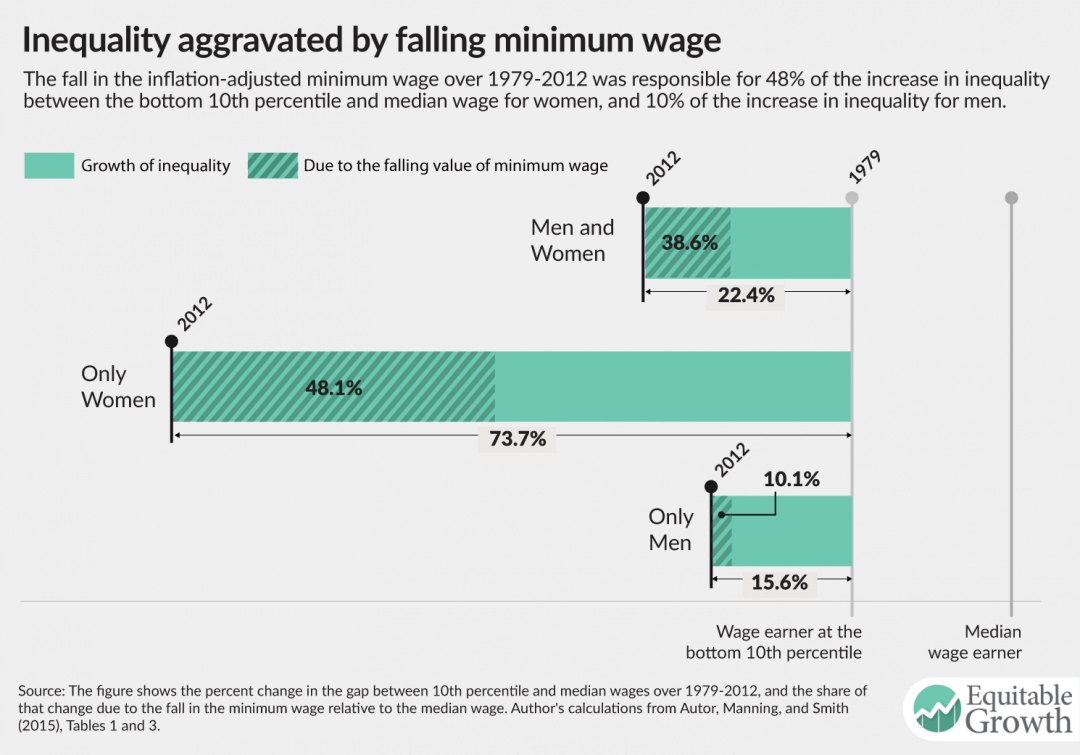

A new issue brief dives into the importance of raising the minimum wage to spur far-reaching economic growth in the United States, surveying the work of several academics in Equitable Growth’s network of scholars. Together, the work helps elucidate whether and how the minimum wage affects family incomes and job opportunities and offers ideas for how to structure future minimum wage policies.

“After Piketty: The Agenda for Economics and Inequality,” a new book published by Harvard University Press, was released this week, featuring several essays reflecting on what gaps still remain to be researched following economist Thomas Piketty’s best-seller “Capital in the Twenty-First Century.” See an excerpt from one of the essays by Suresh Naidu here.

What were the economic ramifications of opening up the United States to more trade with China in 2000? According to new research, one consequence may have been fuel added to the housing bubble as increased competition from Chinese imports weakened the labor market. Nick Bunker further explores the connection.

Links from around the web

Through a series of interviews, Matthew Desmond tackles the relationship between homeownership and inequality in the United States, highlighting how the benefits of home mortgage interest and other real estate tax deductions overwhelmingly accrue to the upper-middle class and the wealthy. [new york times]

Speaking of housing, it may be surprising that the quality of subsidized or assisted housing conditions are pretty equal for children of different races. The problem, however, as Gene Demby points out, is that the location of subsidized housing significantly varies for black and white children, which ultimately influences their life outcomes. [npr]

The “robot apocalypse,” the idea that technologies and automation could increasingly push out workers, is not in fact coming, argues Greg Ip. It may actually be that many low-productivity sectors need to start adopting them to improve the productivity and living standards of workers. [the wall street journal]

Leila Morsy highlights new research on the connection between parents’ incarceration and their child’s cognitive and behavior outcomes, suggesting that mass incarceration may be intrinsically linked to education policy. [the american prospect]

With Mother’s Day around the corner, Valerie Wilson analyzes the Current Population Survey to show the unique role that African American mothers play in the economic well-being of their families. Black moms work more hours and are much more likely to work. [epi]

Friday figure

Featured in “The importance of raising the minimum wage to boost broad-based U.S. economic growth” and originally from “How raising the minimum wage ripples through the workforce”