Is Taxing Wealth Possible? Practical? Desirable? Yes, if we’re smart about it

This column originally appeared in the Milken Institute Review at https://www.milkenreview.org/articles/is-taxing-wealth-possible-practical-desirable.

Key takeaways

- Taxing wealth is consistent with America’s progressive tax tradition—and may in fact be necessary to restore it, given strong evidence that the tax system turns regressive at the very top.

- The main source of this regressivity is the combination of indefinite deferral on unrealized capital gains and the stepped-up basis rule at death, allowing many of the wealthiest Americans to never pay any tax on a large portion of their fortunes.

- With the national debt near 100 percent of GDP and inequality fueling social unrest, slow growth, and democratic backsliding, the status quo is not sustainable. Tax reform that reaches the unrealized capital gains of the ultra-wealthy is an indispensable part of the solution.

- Policymakers have several practical options for achieving this policy aim, from a net-worth or mark-to-market tax to taxing unrealized capital gains at death to tightening business tax rules.

- What this means for growth: Inequality is a drag on economic growth, so more effectively taxing wealth at the top—and spending the proceeds on high-return public investment and deficit reduction—will boost broadly shared prosperity.

Overview

While the American economy has outperformed much of the industrialized world in recent years, there are good reasons to be deeply concerned about its long-term prospects. It is dogged by high debt, high inequality and (by historical standards) slow growth – related problems that vex policymakers and economists alike. One fix, which promises to address all three simultaneously, is gaining political traction: a wealth tax on the super-rich.

Is this merely a Hail Mary pass, a reflection of frustrations that have been building across the new millennium that is no more than a diversion in our bitterly divided political arena? Or is it our last, best chance to ensure the U.S. tax system is effective, efficient and fair? As debates about wealth taxes heat up – notably in bellwether California, where such a tax measure may be placed before voters in November – how can citizens separate fact from fiction?

I argue that, despite the preponderance of rhetoric to the contrary, taxing wealth is consistent with the U.S. tradition of progressive taxation – and, in fact, is needed to patch an increasingly porous income tax system. Targeting taxes on the super-rich’s fast-growing accumulation of wealth, which today is largely in the form of unrealized capital gains, could go a long way toward improving the nation’s fiscal position, tempering inequality, spurring more broad-based economic growth and helping to offset the drift toward government by and for the rich.

Debt As Far As The Eye Can See

The federal government’s annual deficit is roughly 6 percent of gross domestic product, and the national debt is nearly 100 percent of GDP – both near historic highs even though we currently face no major war, recession or pandemic. With interest rates climbing in recent years, interest payments on the debt are now cannibalizing a record one-sixth of the federal budget.

Though a fiscal crisis does not seem imminent – the dollar’s unique role in the global economy provides a lot of insulation – the risk of such a crisis is nevertheless increasing as there is no sign of the deficit trend reversing. Indeed, even if the Trump tariffs are allowed to stand by the courts, that roughly $175-billion tax increase on consumers would barely dent the $1.8-trillion budget deficit.

Conservatives argue that huge deficits even when the economy is operating near full throttle constitute a spending problem, not a revenue shortfall. While every analyst, conservative or liberal, has favorite targets for stricter spending discipline, the “spending problem” rhetoric belies hard, cold facts.

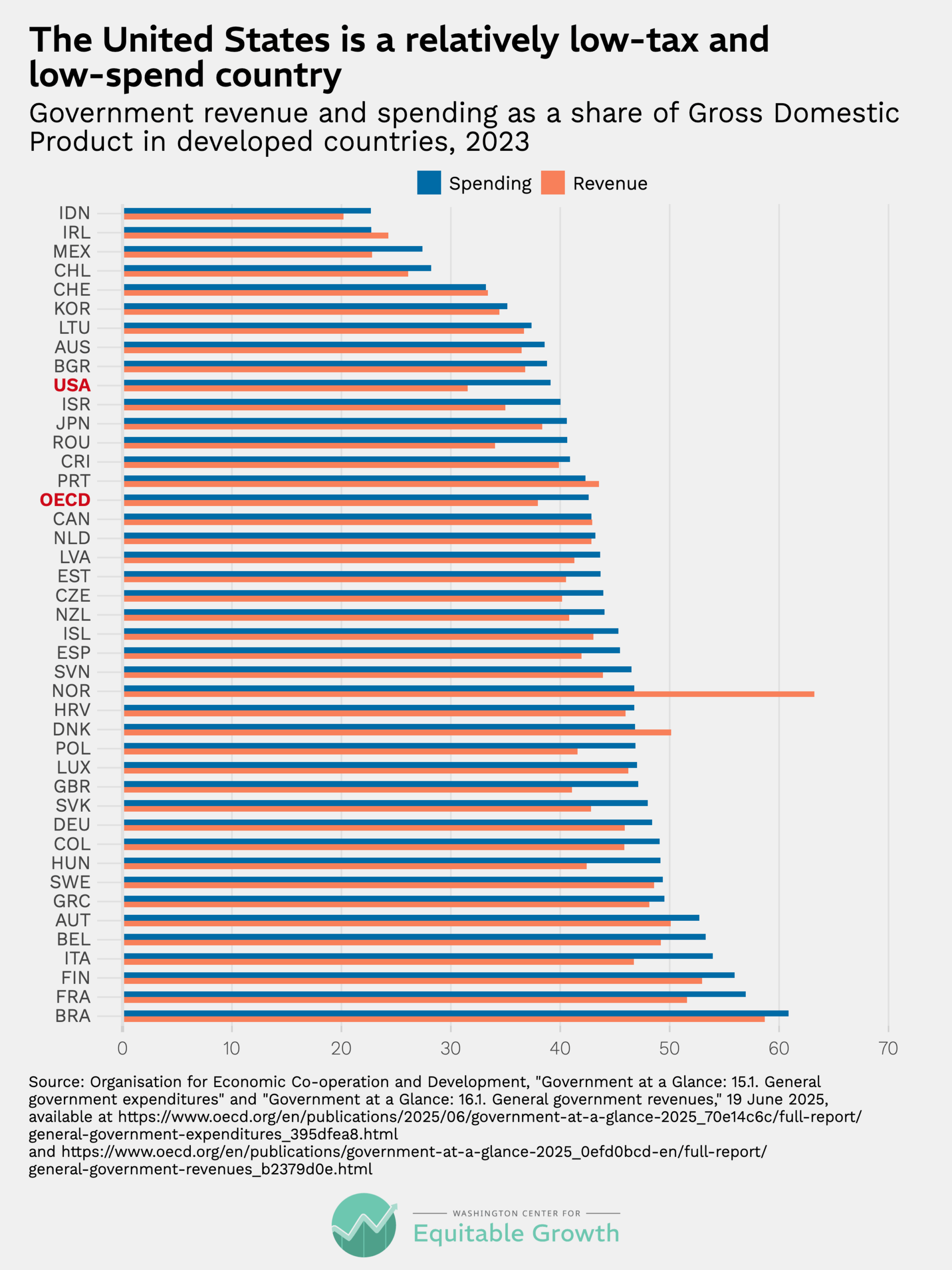

Government accounts for relatively little spending as a percentage of GDP by comparison to other affluent nations – and notably less than should be spent in scientific research, education and infrastructure if the U.S. is to remain a global leader and sustain productivity growth along with the economic capacity to deliver quality-of-life improvements. (See Figure 1.)

Figure 1

This is why attempts at severely curtailing federal services – such as Elon Musk’s predictably disastrous Department of Government Efficiency – inevitably bump against the reality that the U.S. government is already relatively lean. In fact, an underreported fiscal fact is that the reforms in the Affordable Care Act did help to “bend” the health care cost “curve” down (remember that crisis of the early 2000s?), saving the government trillions of dollars.

Slow and Unequal Growth

Optimists hold out hope that the U.S. can grow out of chronic budget deficits. While it’s true that faster economic growth could improve the fiscal outlook by shrinking the debt-to-GDP ratio, both generating more tax revenue without higher tax rates and reducing the demand for safety-net services like unemployment insurance and food stamps, there is little reason to believe that – even with an AI-fueled productivity boom – the U.S. is poised to consistently grow at the 3-plus-percent rate required to begin to close the budget gap, especially if immigration continues to fall.

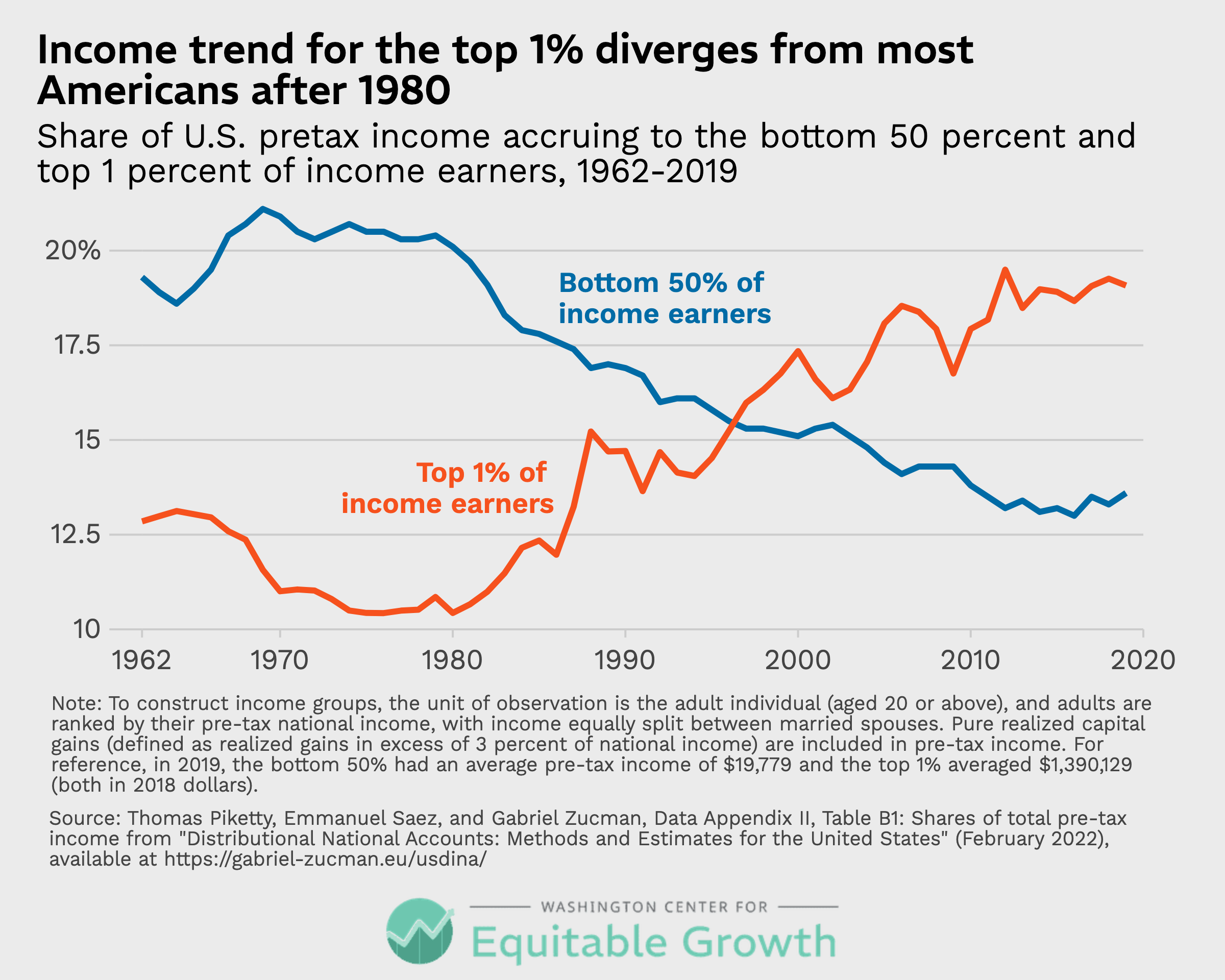

The societal picture gets gloomier when one also considers the unequal nature of recent economic growth. While the most recent data suggest a possible plateauing of inequality, the general trend toward winner-take-all in recent decades has been unmistakable. (See Figure 2.)

Figure 2

Inequality is not just a moral stain on the country that threatens political stability, it contributes to our precarious economic position. Some research suggests that economies with high levels of inequality can’t grow rapidly. As Heather Boushey, a member of the Biden Council of Economic Advisors, has argued, this is likely a result of the way inequality obstructs opportunity by lowering investment in human capital and beefing up unproductive rent-seeking as the rich seek to cement their privileges.

Similarly, Thomas Piketty has noted that with returns to capital growing faster than those to labor, value extraction is rewarded over value creation, undermining incentives for work and innovation. It’s no coincidence that the S&P 500 has grown 400 percent in real terms over the past 20 years, while real wages grew by 12 percent. It seems likely that the continued development of artificial intelligence, which may well increase economy-wide productivity, will only exacerbate this capital-labor divide.

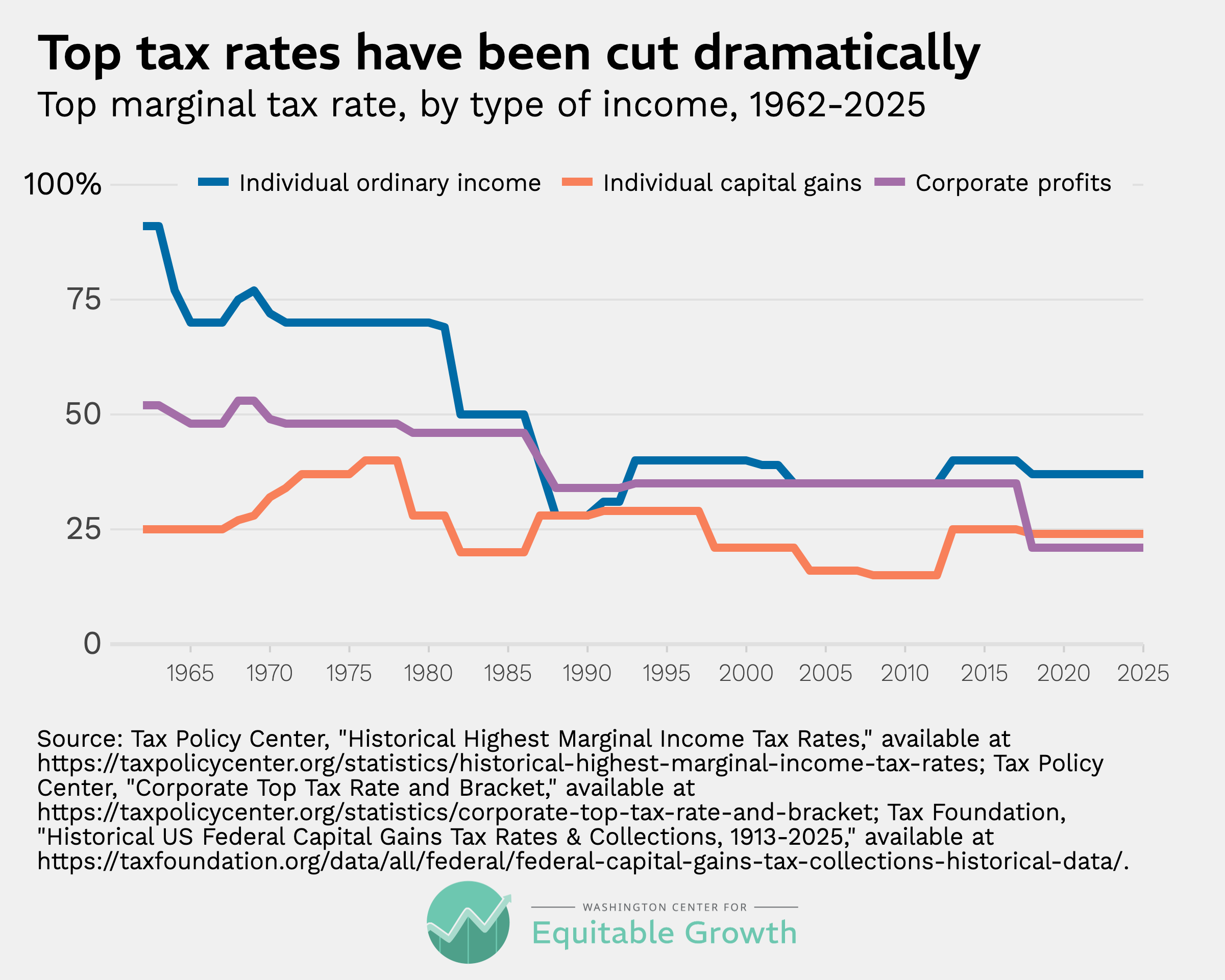

Taxes As Both Cause and Effect

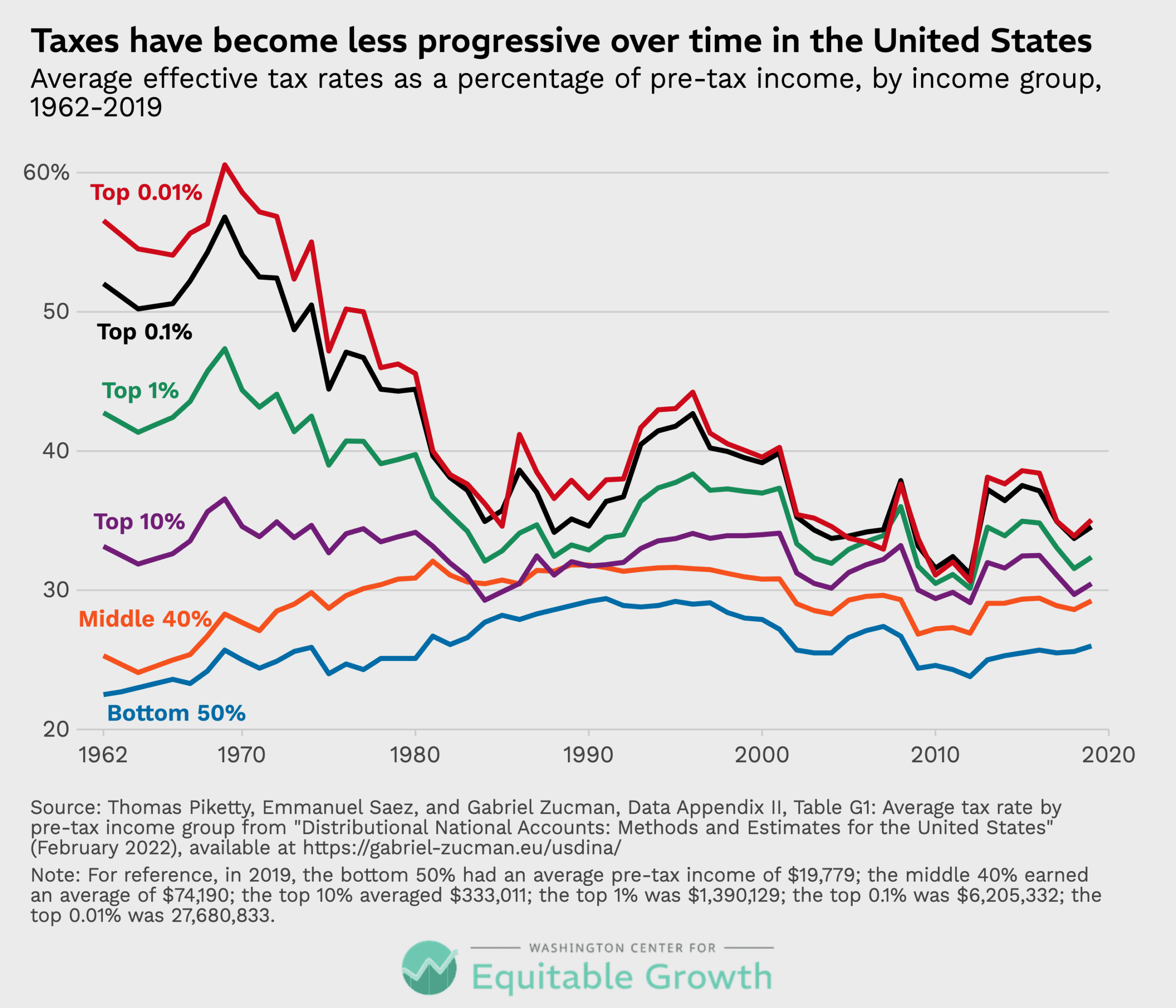

The rise of inequality over the past few decades also helps explain some of the hollowing out of the tax system. As more income is earned by those at the top – often capital income earned through highly complex business structures – taxes became more easily gamed and less progressive. (See Figure 3.)

Figure 3

Some of this is the consequence of the tax code not keeping up with the times. For example, the cap on Social Security payroll taxes excluded just 10 percent of top wages in 1977. But because of faster salary growth at the top in recent decades, the cap now misses 17 percent of the highest salaries, costing the Social Security Trust Fund trillions of dollars.

Or consider capital gains, which are taxed at a favored rate. Because of the explosive growth in the stock market (and the corporate trend toward retaining earnings rather than paying dividends), these capital gains have become a much more important stream of income for the richest Americans. Realized capital gains – that is income realized when assets are sold – are notoriously volatile since they depend in large part on stock market performance. But they have nonetheless been inexorably climbing as a portion of income from an average of 2.58 percent of GDP between 1963 and 1983 to 4.35 percent over the past 20 years.

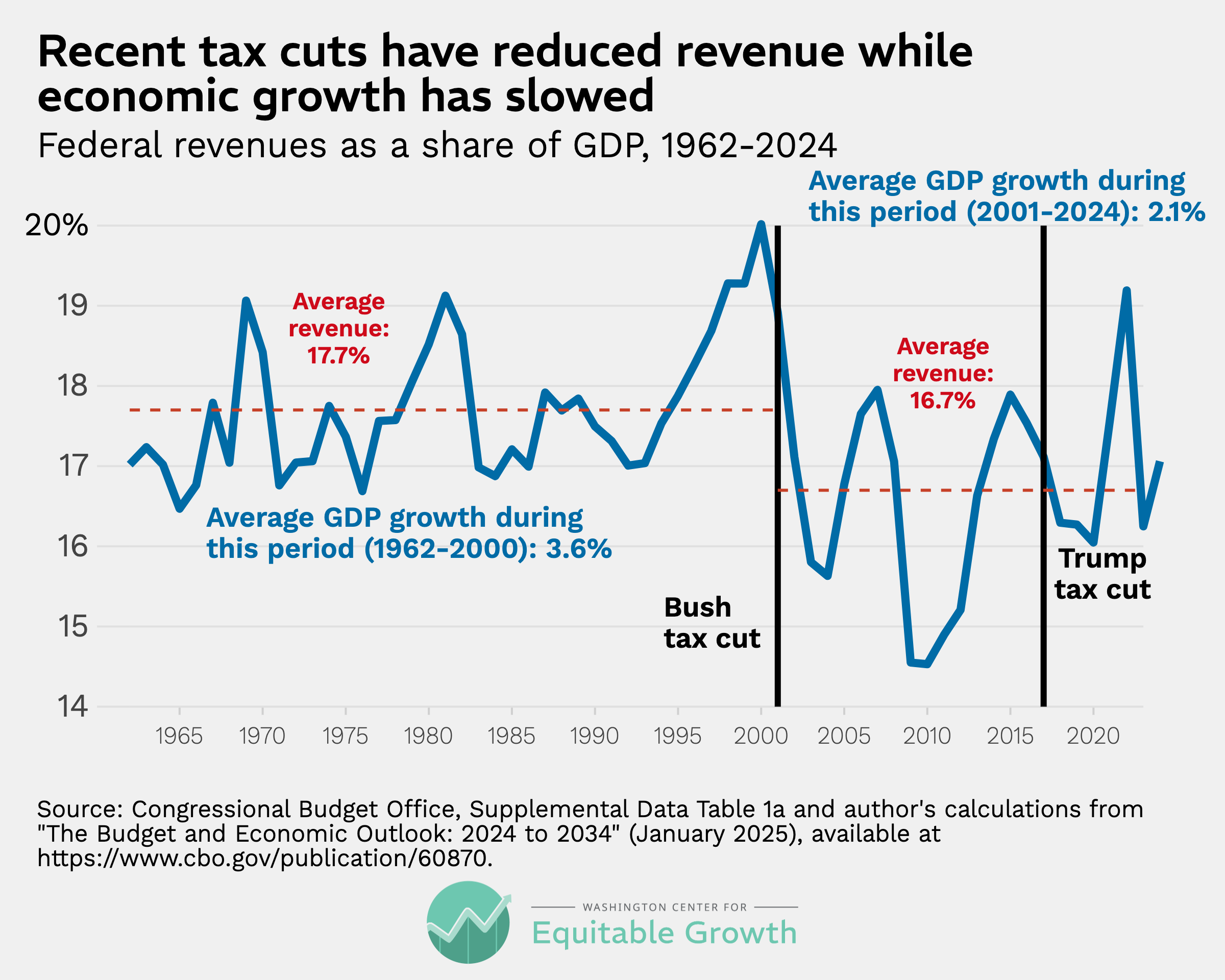

Some of the changing nature of the tax system was the result of proactive policy choices by a political class that was captured by claims from investors that, in spite of mountains of evidence to the contrary, lower taxes increase broad-based growth. (See Figure 4.)

Figure 4

The apotheosis of this approach came last year, when Republicans in Congress passed a deeply regressive measure that will cut revenues by $5 trillion and add $3.4 trillion to the national debt over the next decade. One trillion dollars of that will go just to the top 1 percent of earners (who in 2027 will make more than $526,000). But this was certainly not the first time in recent memory that tax cuts favored the rich.

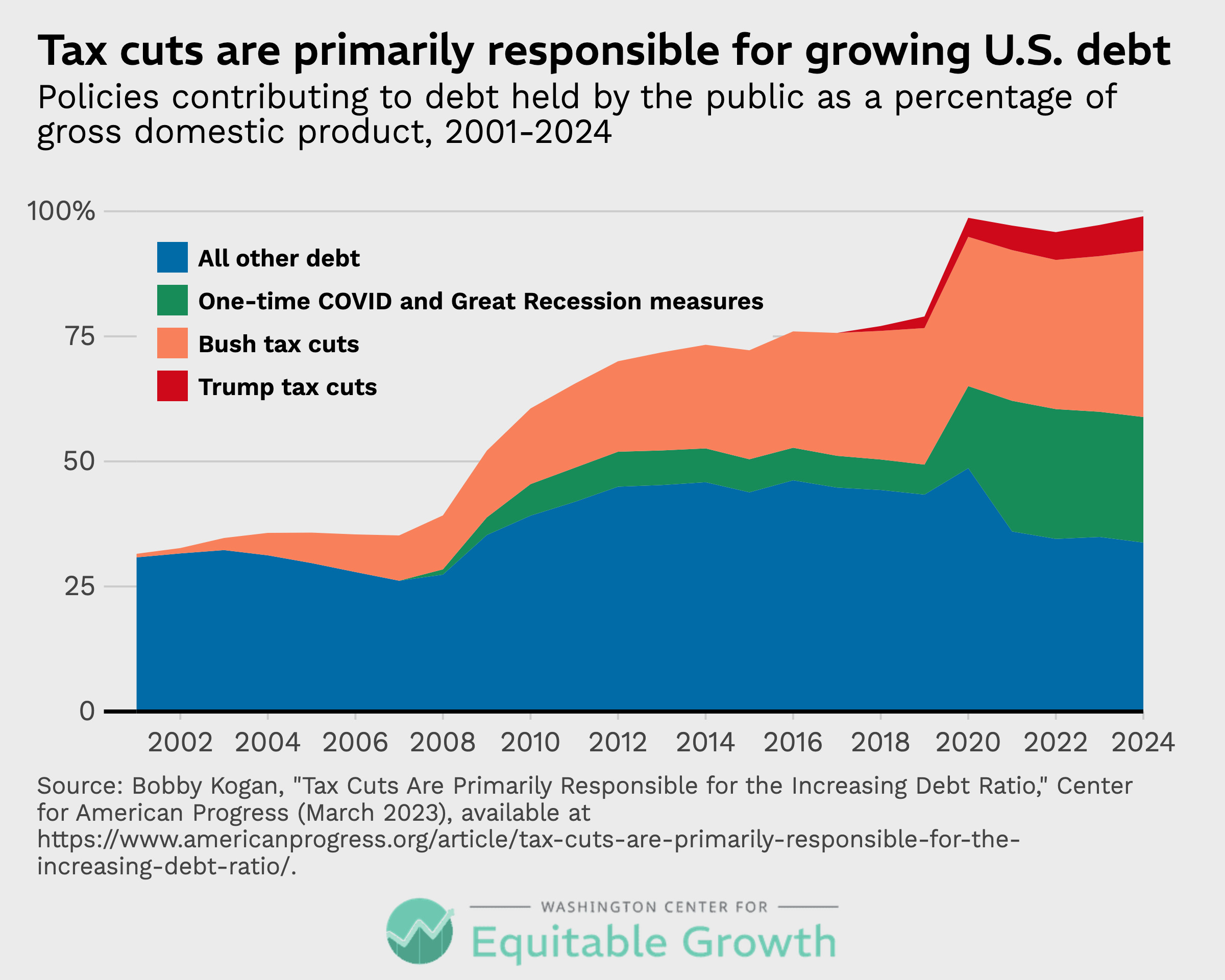

Regressive tax cuts also passed in 2001, 2003 and 2017, which retrospective analysis shows are the main cause of the current debt trajectory. (See Figure 5.) This analysis prompted Senator Elizabeth Warren to dub the nation’s fiscal affairs a “tax doom loop.”

Figure 5

The New Robber Barons

Not only did the tax cuts blow a hole in the budget and fail to lead to faster growth, they also empowered a new upper crust.

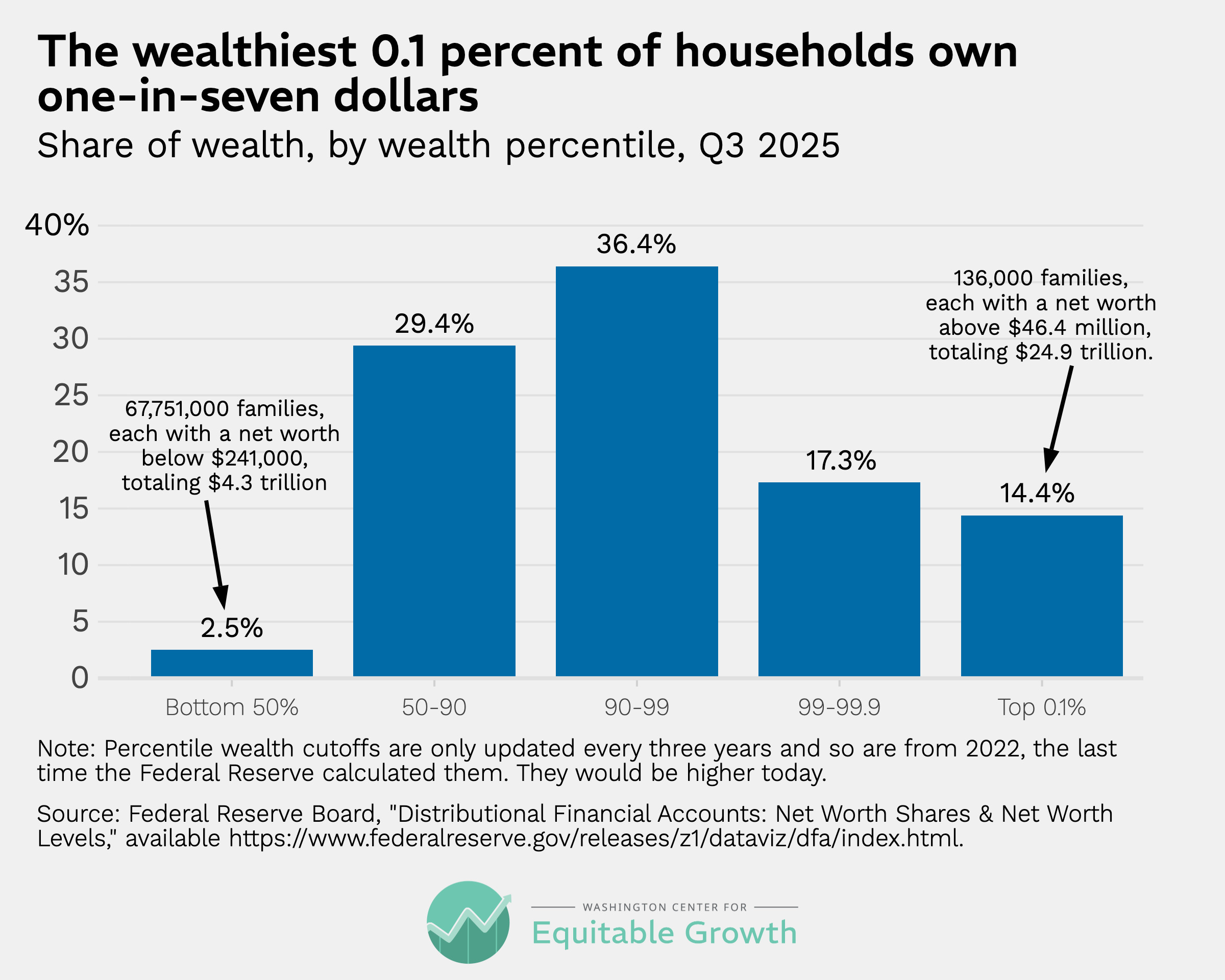

Today, the top 0.1 percent – the richest 136,000 U.S. households with an average net worth of more than $46 million – own roughly one-seventh of the nation’s wealth. (See Figure 6.) About 1,000 of these Americans are billionaires, who as of January 2026 collectively owned $8.2 trillion in wealth, up from $6.7 trillion just a year prior largely thanks to the soaring stock market.

Figure 6

Today’s billionaire class stands out even when compared to the richest people from the first Gilded Age. John D. Rockefeller was worth roughly $900 million in 1913 (or $30 billion in today’s dollars), equivalent to 2.3 percent of GDP. That made him the richest American of all time. Until now: Elon Musk’s fortune today (around $800 billion) is roughly 2.8 percent of GDP

Taxing Wealth

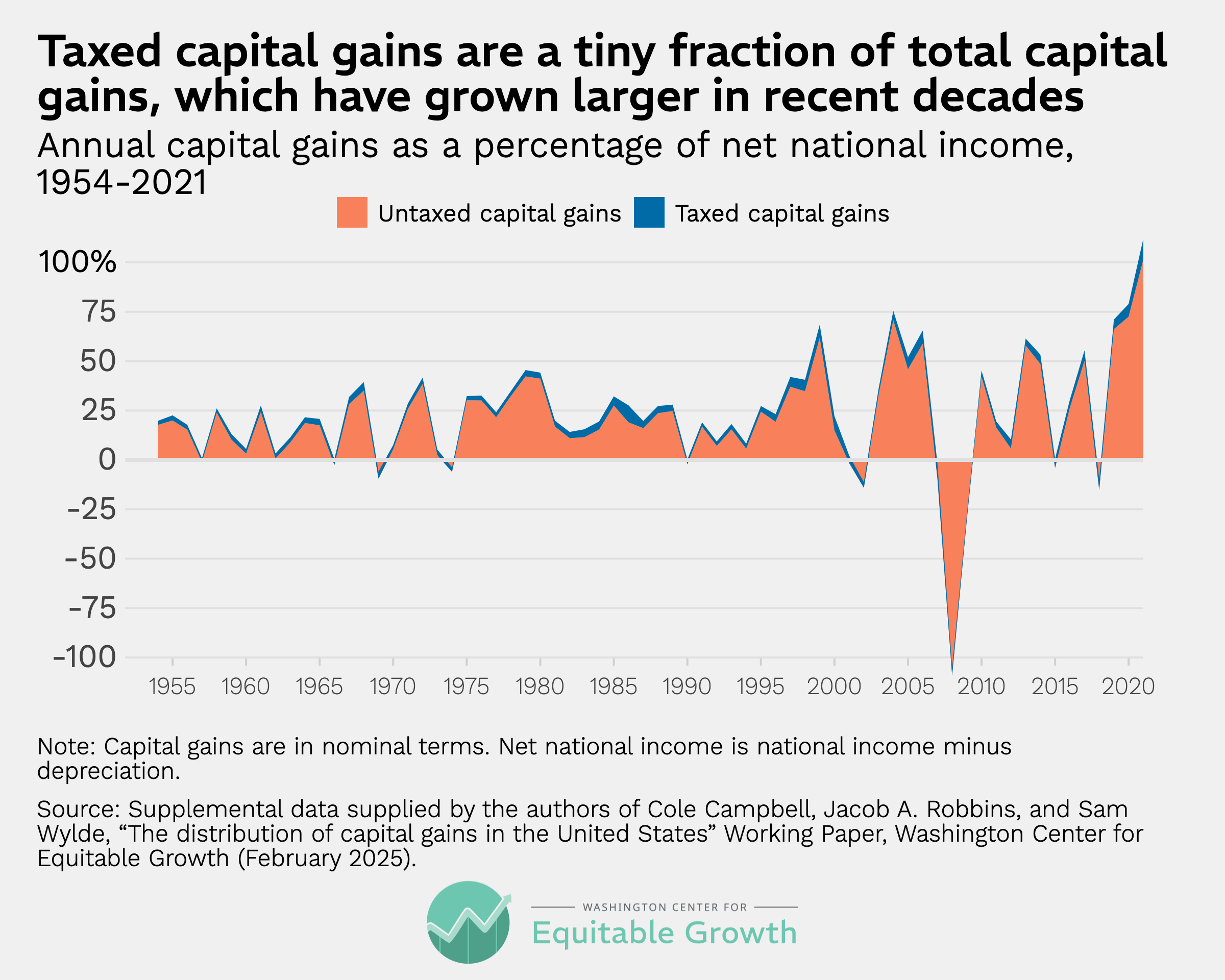

It’s not just the size and growth of these fortunes that are unique, but also how the wealth is treated by the tax system. While most Americans pay tax as they earn their income (with money automatically deducted from paychecks), the extremely wealthy largely choose when (or even if) they pay income tax. That’s because a considerable portion of their income is in the form of appreciation of real estate, stocks and other financial assets, and those gains are not taxed until the asset is sold (or “realized,” in tax parlance). (See Figure 7.) Even when they are taxed, long-term capital gains as well as dividends paid to asset owners enjoy a lower tax rate than that paid on labor income. For those at the top, the difference is between 23.8 percent on gains and 40.8 percent on income.

Figure 7

When this policy of indefinite deferral is combined with what’s known as “stepped-up basis,” a tax rule that wipes away tax liability on unrealized gains at death, the result is that many of the richest Americans will never pay any tax on much of their wealth. When the wealthy find it inconvenient to wait for death to turn their unrealized gains into cash, they can still save on taxes by borrowing using their assets as collateral – a strategy dubbed “buy-borrow-die.”

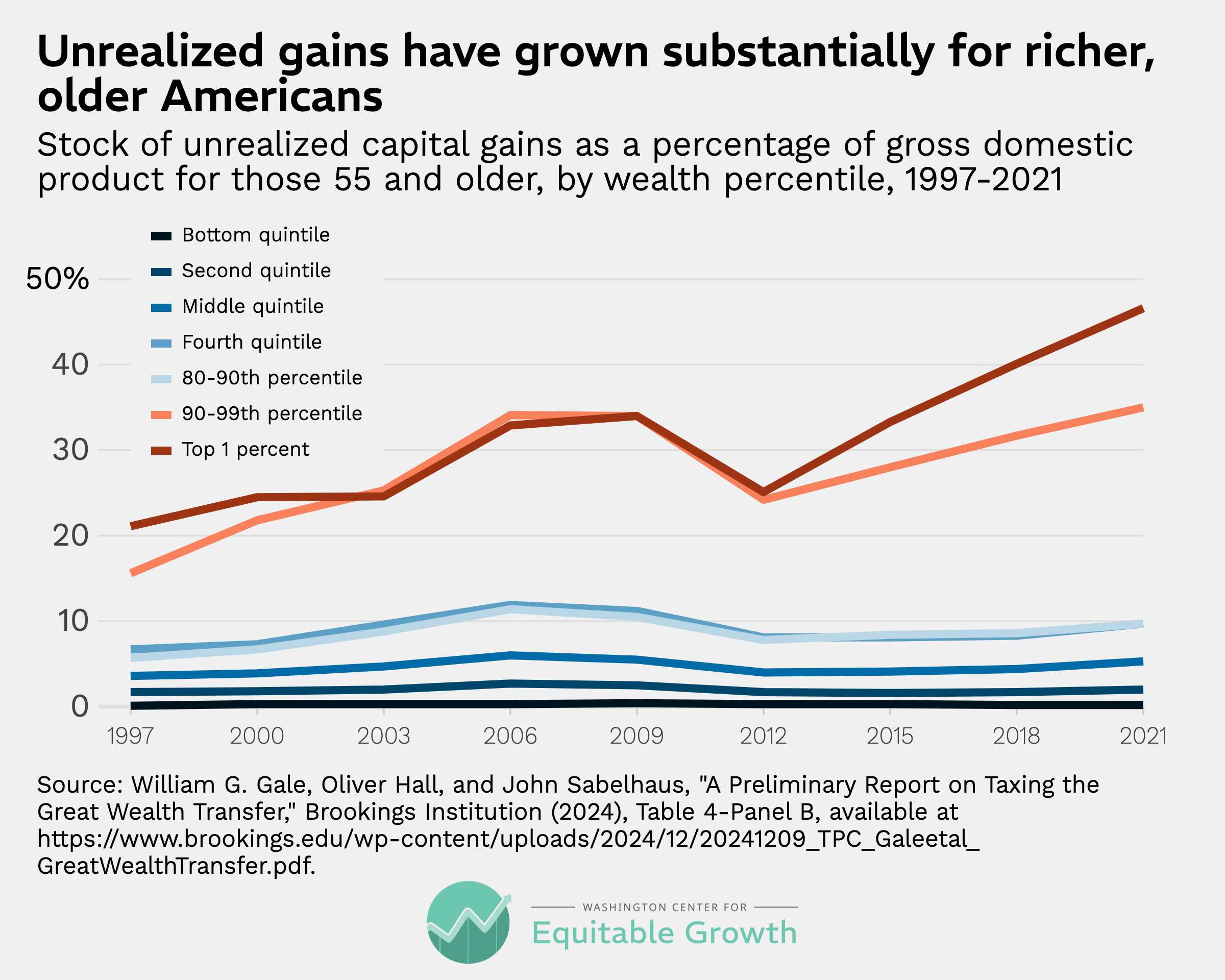

Though stepped-up basis sounds like a technical issue, it stands at the center of the roiling debate around wealth taxes. That’s because unrealized gains make up a large chunk of the total net worth of all Americans today – it was estimated at 27 percent in 2019 and is probably much higher today since the S&P 500 has more than doubled since then. For those in the top 1 percent of wealth holders, the figure was 41 percent. Moreover, roughly half of the unrealized gains held by those in the top 1 percent are concentrated in the top 0.1 percent – and these holdings have been increasing rapidly. As a result, this group pays tax on roughly half of their actual “economic” income (i.e., the increase in their net worth) each year.

Some of this wealth will be taxed eventually – but not much. According to a conservative estimate by the Brookings Institution, of the $36 trillion in unrealized gains held in 2021, $11 trillion are held by those in the top 1 percent who are also over the age of 54, implying that most of this wealth will be bequeathed on a stepped up basis. (See Figure 8.) In generations past, the estate tax would have captured some of these unrealized gains before they were transferred to heirs. But the estate tax has been weakened by Congress and is now easily avoided by creating a spiderweb of trusts, among other (legal) tactics.

Figure 8

It was also historically the case that business taxes would have indirectly captured more of the income accruing to the richest Americans. Most economists believe that the burden of the profits tax on standard, limited liability C corporations is largely borne by stockholders. But the top corporate tax rate has been continuously cut and today is just 21 percent. (See Figure 9.) After all the corporate deductions are taken into account, the effective tax rate on corporate profits is considerably lower.

Figure 9

In any event, many rich Americans organize their business holdings in what are called pass-through entities, meaning these firms’ profits are reported directly on their owners’ personal income tax forms. This introduces a host of tax avoidance opportunities outside the scope of this article. But no one disputes that much of the income generated by these closely held companies does not show up on tax returns. (It also allows the richest Americans to take political cover as “small business owners,” since most bona fide small businesses also organize themselves in this way.)

When all income, including unrealized gains and business profits, and all the tax cuts and tax avoidance schemes mentioned above are taken together (but not factoring in outright tax evasion), the overall picture at the top end of the wealth spectrum is much less progressive than is generally assumed. Indeed, there is strong (albeit disputed) evidence that the U.S. tax system turns regressive at the extreme top, with the richest 400 families paying less (24 percent) than average middle-class families (30 percent). This result has been corroborated by other researchers who estimate a 25.5 percent tax rate for the top 0.01 percent of earners.

What Can Be Done?

Early in the 20th century, the country faced a similar combined threat from a growing need for public investment and sky-high inequality. In that case, the advent of the personal income tax ushered in decades of strong tax revenues, equitable economic growth, and a relatively stable political order in which Americans could be confident that the rich were paying their fair share of taxes.

Today, policymakers need to similarly rethink the tax system to address the threats we face from low revenue, high inequality, uneven growth and social unrest expressed as right-wing populism. While any plausible tax on billionaires’ unrealized gains would not be enough to eliminate the debt and inequality chasms, part of any reform aimed at rebalancing tax burdens and reestablishing trust in the system must target tax preferences (aka loopholes) that in substantial part explain the accumulation of wealth in so few hands.

There are a number of novel – and practical – ways to do this discussed below, but any initiative that fails to tax unrealized gains should be dismissed as a nonstarter in the debate. Even serious conservative commentators recognize this. For example, the center-right Arnold Ventures philanthropy group included an excise tax on borrowing against unrealized gains in their tax reform prescription last year. And Republican former-Senator Mitt Romney has come out in favor of closing the stepped-up basis loophole. For that matter, even Donald Trump once proposed a large, one-time wealth tax on the rich.

In my view, opponents of any of the approaches below, which are admittedly imperfect, should be required to offer up their preferred alternative, given the untenable status quo.

A Net Worth Tax

The most straightforward way to tax wealth is a wealth (or “net-worth”) tax. As with all taxes, the two key design considerations are how to calculate what is taxed (the tax “base”) and what percentage of that base will satisfy the revenue target (the tax rate). Most states already have a wealth tax in the form of property taxes. But while those target residential and commercial land and buildings, most current wealth tax proposals would exempt primary residence and retirement accounts – the two main sources of middle-class wealth.

Instead, most wealth tax proposals focus on the key sources of wealth for the superrich, namely stock holdings in public and private businesses. One challenge is valuing certain assets that have not historically been reported to the IRS or for which there is no liquid market to determine price (e.g., artwork and closely held businesses). Exempting too many of these categories could create a perverse incentive for taxpayers to over-invest in these now tax-preferred asset classes.

The most compelling justification for a wealth tax is that it could quickly raise a lot of revenue from the richest of the rich. Even a one-time wealth tax at the state level, such as the one that might get on the ballot in California later this year, would raise upwards of $100 billion. A federal wealth tax of 1 percent on fortunes above $50 million and 2 percent on net worth above $100 million – somewhat similar in design to those proposed by Senators Bernie Sanders and Elizabeth Warren – would raise roughly $3 trillion over 10 years, though projections heavily depend on assumptions about breadth of the tax base, compliance and enforcement.

One particular challenge with state-level wealth taxes is that they could lead their rich targets to move to lower-tax states. But evidence on the “fleeing millionaire” phenomenon is actually fairly weak. Though a few big names may leave a state upon the imposition of a wealth tax, there are ways to design effective exit taxes, the net revenue will still be positive and there could even be some positive spillovers from losing residents who are most responsible for bidding up prices in local real estate markets. That said, the raceto- the-bottom, jurisdiction-shopping problem is a reason a federal wealth tax would be superior to a state one.

The larger problem with wealth taxes has been the questionable ability of jurisdictions to efficiently enforce a tax that the wealthy would surely try to game – for example, by moving assets offshore or undervaluing privately held businesses. But some European countries, such as Spain and Switzerland, have overcome these challenges, designing effective and durable wealth taxes.

In terms of real economic behavior – rather than just tax-motivated accounting – there is little reason to think the rich wouldn’t still invest the vast bulk of their fortunes as productively as they know how (you can only consume so much). In fact, a tax could lead to greater efficiency rather than less. The rich would no longer face the perverse incentive to hold assets until death, eliminating what economists call the “lock-in effect.”

At the federal level, the problem is less economical and more political in nature: the Supreme Court, in its current composition, seems likely to impose an imaginary realization restriction on Congress’s taxing power in order to block the implementation of a wealth tax (or any tax on unrealized gains), should one be passed.

Comprehensive Tax on Capital Income

Another way to tax wealth is to tax the annual (realized and unrealized) proceeds from that wealth – sometimes referred to as a “mark-to-market,” “accrual,” “billionaire” or “billionaires income” tax. This is more in keeping with the income tax tradition in the U.S. in which gains are calculated in relation to cost “basis,” which is usually the purchase price. But a wealth tax could be designed to achieve an identical result economically: a 1-percent tax on an American with $100 million in end-of-year net assets (producing $1 million in tax) is the same as a 10-percent tax on that same taxpayer’s annual capital income if their portfolio grows by 11 percent (going from $90 million to $100 million over the course of the year). Of course, a recurring wealth tax that hits even in years in which the taxpayer’s investments lose money would likely raise more money than an annual capital income tax, especially if the capital income tax regime gives taxpayers credit for losses.

Some economic models find that a wealth tax is more efficient than a tax on capital income. That’s because it hits lower performing asset portfolios harder than higher performing ones, thus putting more money in the hands of the most productive investors and disempowering the rentiers who are not making best use of their capital.

While a tax on unrealized gains faces many of the same administrative and judicial hurdles as a wealth tax, there is more room for clever workarounds. For example, Brian Galle of UC Berkeley Law has proposed a way to tax deferred gains that only requires payment of the tax at realization (which would include death) but incentivizes taxpayers to pay earlier. To ensure taxpayers who fail to prepay can’t continue to benefit from indefinite deferral, an extra fee on the buildup of the asset is levied upon realization. This kind of voluntary prepayment approach should both bring in short-term revenue and pass constitutional muster.

A more traditional mark-to-market tax, though perhaps doomed in the courts, could be designed to raise considerable revenue. For example, charging ordinary income tax rates on deferred gain from taxpayers with more than $16.5 million in gross assets would bring in $3 trillion over 10 years.

Transfer Taxes at Death

A simpler but less lucrative approach would be to tax unrealized capital gains at the transfer of these assets at death rather than during the life of the taxpayer. The modern estate tax was created in 1916 to do just that. But this tax on wealth has been decimated by conservatives over the past few decades, with now only 0.14 percent of those dying owing tax.

Taxing unrealized gains at death through an estate tax, inheritance tax or some other mechanism – while also tightening rules around trusts and charitable giving, two of the most popular ways the rich avoid the estate tax today – would bring the U.S. into closer alignment with other countries. For example, Canada does not have an estate tax, but it does tax unrealized gains at death – a policy that a recent analysis found was effective because it reduced the incentive to hold assets indefinitely. One recent proposal in the U.S. calls for taxing unrealized gains at higher rates at death than in life to reinforce this anti-lock-in effect.

According to the Congressional Budget Office, a tax on accrued capital gains at death in the U.S. would raise $536 billion over 10 years. This number is considerably lower than the wealth tax estimates above partially because the revenues materialize more slowly (i.e., the government needs to wait for taxpayers to die).

That raises an ancillary political problem: the rich would have ample time to lobby Congress to reverse or water down the tax. A policy that replaces stepped-up basis with carry-over basis, meaning heirs would eventually have to pay tax on the appreciation that occurred during the life of the decedent but would not have to pay at the transfer at death, would face an even harsher version of this problem (and it is estimated to only raise $197 billion over 10 years).

That said, Norway replaced stepped-up basis with carry-over basis in 2006 and still managed to raise considerable revenue as Norwegians realized – and paid taxes on – gains they otherwise would have deferred. (Norway also has a wealth tax, and there is evidence that this combination of policies can actually enhance efficiency.)

Enhanced Tax on Business Profits

Finally, given the aforementioned importance of business income for the richest Americans, policymakers could ensure more fulsome taxation of business entities, avoiding some of the thorny questions that arise when taxing shareholders in their individual capacity. As mentioned above, so-called subchapter C corporations, which include all public firms, already face a 21 percent entity-level tax, which ensures that some tax is paid on corporate profits even if shareholders escape capital gains taxes. Very few companies actually pay the full 21 percent rate given many deductions, offshoring opportunities and other goodies embedded in the code – but that is a fixable problem.

A more substantial complication is that a large and growing segment of business income is taxed via what are called passthrough firms, meaning the owners pay tax on their business income on their individual returns. These business structures – often limited liability companies organized as partnerships for tax purposes – allow for various tax avoidance schemes that, among other things, convert ordinary business income into capital gains. Many of the richest Americans have ownership interests in these privately held businesses, and so instituting an entity-level tax by, for example, requiring pass-throughs above a certain size to pay taxes as C corporations would capture some otherwise avoided tax. This more unified business tax structure would also improve economy-wide efficiency by leveling the playing field between firms and eliminating tax arbitrage opportunities.

An outdated version of this proposal was projected to raise $300 billion over 10 years, but that figure would be higher in today’s dollars and the policy could be combined with other tax increases on large businesses. So while not as glitzy or targeted as a wealth tax, fixing the nation’s business income tax system could raise considerable revenue while closing a key tax loophole currently exploited by the rich.

Sooner Rather Than Later

The societal problems created by concentrated wealth, an eroding tax base and lagging economic growth are not going away; reckonings are coming, both in fiscal and political terms. We already see that in high interest rates and populism. The traditional income tax has not been up to the challenge, and so policymakers must think creatively about how to reach the unrealized capital gains that have become such an important part of the wealthy’s fortunes. There are a number of good options for policymakers to choose from that avoid the obvious pitfalls. The question is whether we have the will to act.

Did you find this content informative and engaging?

Get updates and stay in tune with U.S. economic inequality and growth!

Stay updated on our latest research