Must-Read: Five Revisions of Its Model That the Fed Should Make or Test: And I do not think that the Fed is handling the process of revising its thinking properly.

I say that the Fed should, right now, be rethinking its estimates of:

- the long-run real natural rate of interest,

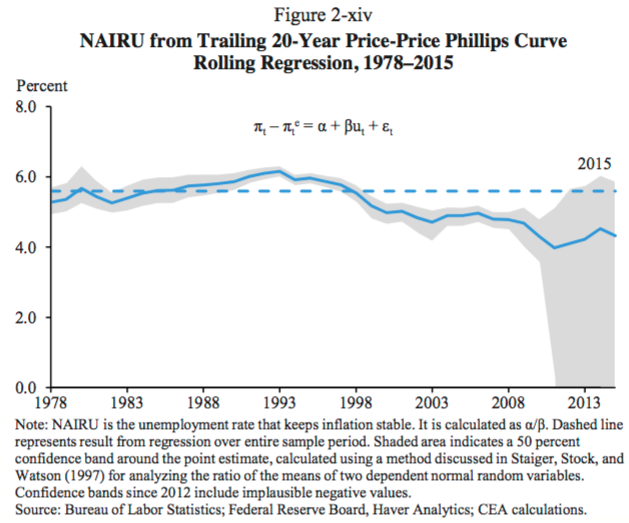

- the natural rate of unemployment,

- the slope of the Phillips Curve, and

- the gearing between recent past deviations of inflation from its target and expectations of future inflation.

Ryan Avent says that the Fed is rethinking (1) and (2), but also rethinking a (5): its estimate of long-run potential output growth. I don’t think there is evidence to rethink (5). I think that the consilience of a low pressure economy and apparent sluggish potential output growth is just too large for people to be satisfied rejecting it as a mere coincidence. Ryan agrees with me, and asks why the Federal Reserve seems to want to jump to conclusions about (5) rather than testing it. I agree. But I also want to ask: why isn’t the Fed rethinking its views on (3) and (4) as well? There is powerful evidence that they are different from the implicit model Fed policy has been running off of for the past decade as well:

Ryan Avent: Absence of Evidence: The Fed Rethinking One Thing too Many:

OFFICIALS at the Federal Reserve, a few of them anyway, seem to be rethinking their views of the economy in some dramatic ways….

Ben Bernanke suggests… top policy-makers still have confidence in their mental model of the economy; they have just been tweaking a few of the parameters… long-run… GDP growth… unemployment… and their benchmark interest rate…. The latter two [what I call (1) and (2)]—a lower unemployment rate and a lower long-run interest rate—clearly imply that rates will rise more slowly to a lower overall level. The projection of a lower potential growth rate [what I call (5)], however… suggests, for instance, that the American economy is running closer to its “speed limit”… push[ing]… toward a more hawkish stance…. These three revisions are not created equal…. [(1) and (2)] are clearly justified…. [(5)] is different, however. Available evidence is consistent with a world in which long-run potential growth has fallen… but… also… with an economy… growing slowly because of too little demand… in which both strong employment growth and low productivity growth are side effects of the low level of wages.

The only way to resolve the question in a satisfying way is to test it: to push the economy beyond the estimated potential growth rate and see if inflation rises…. Bernanke argues that Fed officials are willing to be a little patient with the economy, to see whether running it a little hot brings more workers into the labour force and encourages productivity-enhancing investments. It certainly seems clear to me that overshooting is the right way for the Fed to err….

But I am less confident than Mr Bernanke in the Fed’s openness to overshooting. It did not exactly intend to run the unemployment rate experiment that demonstrated how run its previous projections had been…. Now, the Fed looks all too willing to revise down its GDP growth projections without ever really testing them…. There is far too little radicalism at the Fed. It risks making permanent a low-growth state of affairs which is largely a consequence of its own excessive caution.

I would say may be rather than is. But one thing we agree on is that it is definitely the Fed’s responsibility to find out. And on its current policy trajectory it will find out only by accident–only if the economy turns out to be stronger than the Fed currently projects.

{kind=link}