Time for the Fed to look beyond 2 percent target inflation?

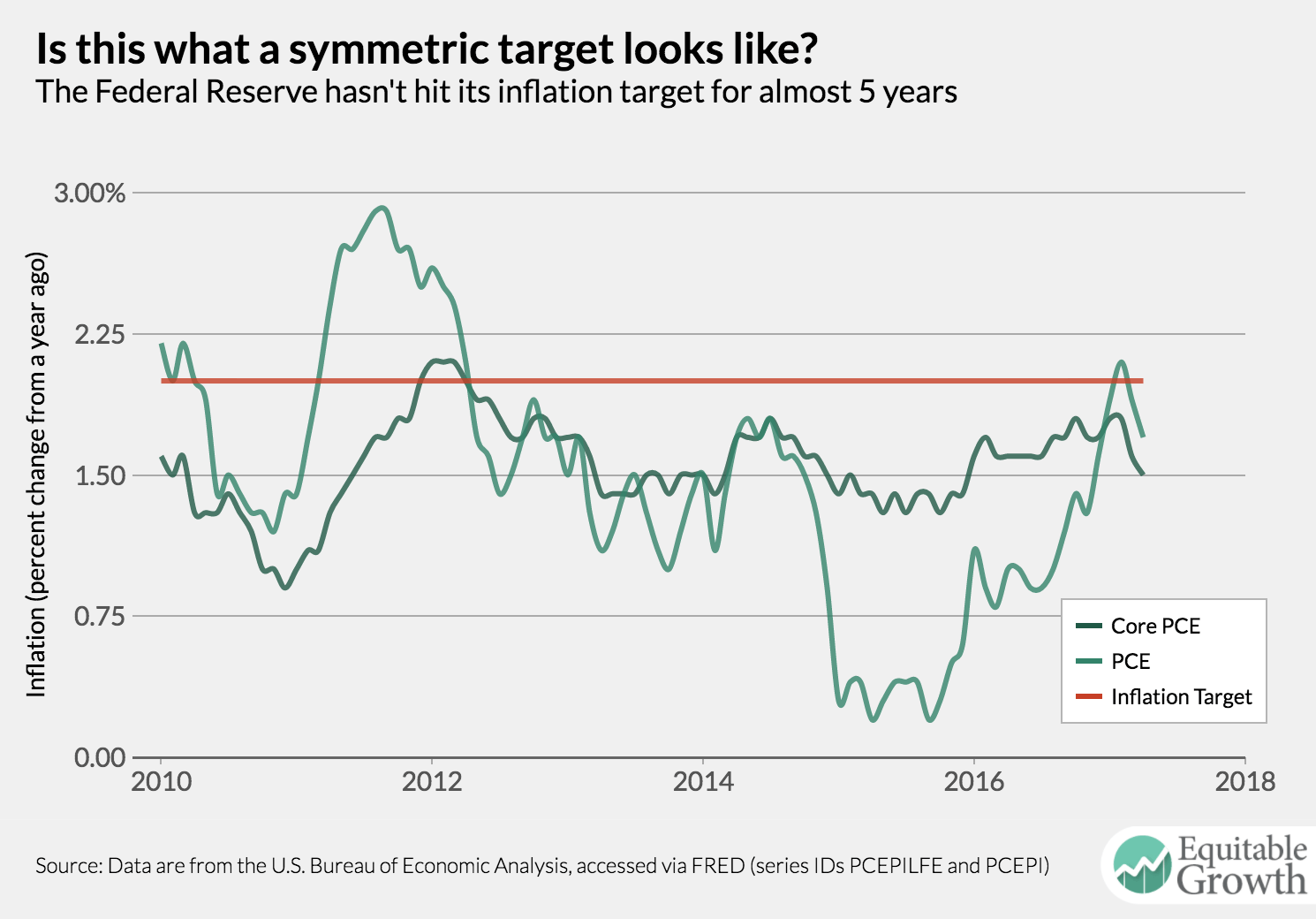

If insanity is repeating the same thing over and over again and expecting new results, then perhaps it’s insane to expect the Federal Reserve to wait for inflation to hit the U.S. central bank’s inflation target of 2 percent before tightening monetary policy. With no serious sign that inflation is accelerating, the Fed seems ready to hike interest rates. Only once in almost five years has inflation cracked that level—set by the Federal Open Market Committee, or FOMC—for a single month. (see Figure 1)

Figure 1

For most of the past half decade, inflation measured by the Personal Consumption Expenditure price index—both the headline figure and the core inflation rate that strips out volatile food and energy prices—has been below target. Chair Janet Yellen and the rest of the FOMC have noted that they consider the target to be “symmetric,” meaning that missing that target both above and below 2 percent is treated the same. Yet given that the central bankers seem ready to announce an increase in interest rates when their meeting concludes tomorrow, they don’t seem that comfortable with inflation even getting close to 2 percent.

Maybe it’s time for the Fed to rethink its inflation target. Maintaining stable inflation is half of the Federal Reserve’s dual mandate—the other being full employment—and one would hope that this sort of track record on inflation would spark a rethink of the inflation target. In fact, it might, at least in part. Last week, a group of economists, including Equitable Growth’s Heather Boushey, sent a letter to the Fed’s Board of Governors asking them to reconsider the current 2 percent target.

The idea that a stable and credible inflation target must be 2 percent is an accident of history, a figure “plucked out of the air” in New Zealand more than a quarter century ago and which has since been adopted by other high-income countries, including the United States. Inflation this low may have been a positive development in the past, but it presents problems now. With nominal interest rates so low, a 2 percent inflation target limits how low inflation-adjusted, short-term interest rates can go.

Josh Bivens of the Economic Policy Institute argues persuasively that a higher inflation target would make monetary policy more effective the next time interest rates need to be slashed to cope with the next U.S. economic downturn. A higher inflation rate could also boost growth by redistributing money toward net debtor households, many of which would be more likely to spend that money. Given that one of the most cited costs of higher inflation—price distortion—might not be that large, the case for higher inflation seems quite strong.

But perhaps the rethink should go beyond just a higher level of inflation. A higher inflation target would be beneficial, but monetary policy in the United States might still have a “ceiling” problem, not a “target” problem. The Fed might go from undershooting 2 percent to undershooting 4 percent should it lift its inflation target. To avoid this possibility, the FOMC could target not the pace of price increases—inflation—but the price level.

Under such a regimen, if inflation undershot 2 percent for a period of time, then monetary policymakers would need to balance it out with a temporary overshoot of inflation. Targeting inflation more flexibly may also help central bankers deal with the problems of the “zero-lower bound.” And if central bankers want to go even further, they could consider targeting something entirely new: the level of nominal gross domestic product.

Frustration with the current monetary policy response to sub-2 percent inflation could lead to complaints that the current rules aren’t being followed or to requests for new ones. The 2 percent inflation target might have been the right target at a certain point in time, but it looks like its time has passed. The conversation to have is how much policymakers want to shake things up.