This is not the rate hike you’re looking for

Unless they’re setting up a twist ending worthy of M. Night Shyamalan, the Federal Open Market Committee will end seven years of zero-interest-rate policy later today at its last meeting of 2015.

The arguments for raising interest rates are varied, but ultimately all lacking, as Larry Summers argues. One of the underlying assumptions of the potential rate hike is that the economic recovery is strong enough that it’ll continue apace as short-term interest rates creep up from zero. But the recovery has actually shown some signs of deceleration in 2015. While a 0.25-percentage-point increase in the federal funds rate seems unlikely to totally derail the recovery, it might be prudent to make sure the nation’s economy is on a positive trajectory before raising rates.

A simple look at the U.S. labor market shows that job creation has slowed down this year. So far in 2015, the U.S. economy has added an average of 210,000 jobs a month. Compared to the average of 253,000 net jobs per month during the first 11 months of 2014, the level of job growth has taken a clear turn down this year.

According to some analysts, however, that might not be a terrible thing. It could be that job growth slows down as slack in the labor market is whittled away. With fewer unemployed or underemployed workers, the economy would have less room to run and job growth would naturally slow. And with the U.S. unemployment rate at 5 percent, this argument that proximity to full employment means slower employment growth might have some glint of truth to it.

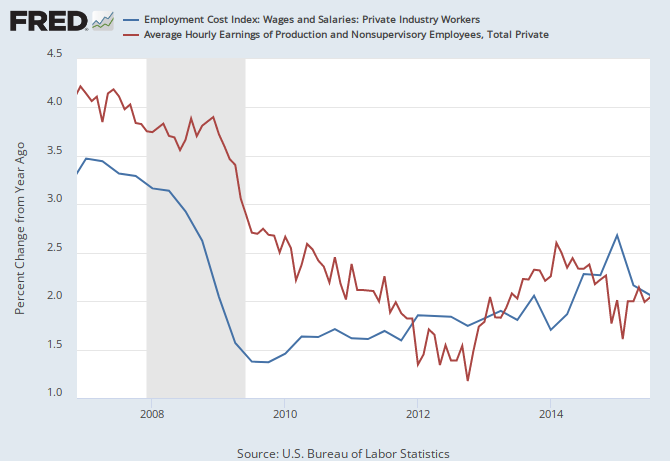

But while 5 percent unemployment is near some estimates of a sustainable unemployment rate, other signals aren’t showing a particularly tight labor market. For starters, sustained, accelerating wage growth—the best sign of a tightening labor market—hasn’t shown up yet. Yes, there has been an uptick in one measure of wage growth—the year-on-year growth in average hourly earnings for all private employees—over the last couple of months. But that increase has only been from 2.0 percent to 2.3 percent, well below a reasonable wage target of 3.5 percent to 4 percent. Other measures still show wage growth hovering around 2 percent.

{kind=link}

So when should we expect healthy wage growth in the United States? The unemployment rate is often used as the measure of labor market tightness to predict wage growth, but we might want to use something else. In the past, Equitable Growth has pointed to the employment-to-population ratio for prime-age workers (those 25 to 54 years old) as a good predictor of future wage growth. Specifically, since 1990, wage growth of at least 3.5 percent only occurred after the prime-age EPOP reached 79 percent. With the prime-age EPOP currently sitting at just 77.4 percent, there’s a ways to go until the economy hits that threshold. Given the slow growth in the rate over the last 12 months, it’ll take more than three years to get to 79 percent. If the prime-age EPOP had continued to grow at its 2014 rate during 2015, however, the economy would be on pace to hit that target in little over a year.

To be clear, the small step the Fed will likely take today won’t immediately stall economic growth in the United States. But the step toward higher interest rates will result in fewer workers employed than otherwise and slower wage growth. This choice is one to not fully use the potential resources of the U.S. economy—and we will all be worse off for that decision.