Taxing the rich: The effect of tax reform and the COVID-19 pandemic on tax flight among U.S. millionaires

Taxing the rich is one of the central policy debates in this time of rising inequality. Elite taxation can change the distribution of income in society, support equitable growth, and finance public goods and services that improve the quality of life for everyone. None of these goals are well served, however, if taxes lead to high levels of tax flight among U.S. millionaires. Progressive taxation, especially at the state level, ultimately depends on the embeddedness of the tax base. In other words, are the rich “mobile millionaires,” readily drawn to places with lower tax rates? Or are they “embedded elites,” who are reluctant to migrate away from places where they have been highly successful?

Supply-side economics has long argued that taxes on the rich cause avoidance behavior and reduce the incentive to work, invest, and innovate. Amid the growing red state/blue state rivalry in the United States, tax incentives for migration have become a new focus of debate. Why would rich people continue to live in New York, New Jersey, or California when they could save large sums in taxes by moving to places such as Florida, Texas, or Nevada? Of course, taxes also fund public goods that the rich consume—not even the richest city dweller can get to work without public infrastructure—but top earners have greater ability to opt out of many public services such as schools and social services. From this view, the rich seem motivated and mobile—sensitive to taxation and readily capable of exit.

Yet there are myriad social dimensions that rich households face when migrating to avoid taxes. Top earners are often the “working rich,” with many roots in the places where they built their careers. Others are business owners with complex ties between customers, suppliers, and workers that are not easily relocated. Top earners are often married, have school-aged children, and have lived in their state for many years—social factors that tie people to places. These ties represent place-specific social capital, a form of embeddedness that makes migration costly.

Our new working paper, “Taxing the Rich: How Incentives and Embeddedness Shape Millionaire Tax Flight,” examines the joint effect of incentives and embeddedness on the mobility of the rich in the United States. Drawing on administrative tax data from IRS tax returns of top income earners, we study two large-scale “natural experiments,” which are contrasting real-life situations that social scientists investigate to determine cause-and-effect relationships. The first is the federal Tax Cuts and Jobs Act of 2017, which changed tax incentives to favor low-tax states. The second is the COVID-19 pandemic, which began in early 2020 in the United States and which deeply disrupted people’s socioeconomic attachments to places.

The 2017 federal tax bill championed by then-President Donald Trump cut the top income tax rate but also raised taxes on some top earners by capping a deduction used most heavily in so-called blue states: the state and local tax deduction. This made the tax reform highly polarizing, actually raising taxes on millionaires in many blue states, such as New York and California, while cutting taxes in red states, such as Florida and Texas. Many predicted dramatic migration flows of top earners from high-tax to low-tax states. President Trump himself soon moved his permanent residence from New York to Florida.

To study the 2017 tax reform, we used administrative data from IRS tax returns, drawing on more than 12 million observations. We employed so-called difference-in-differences models, which compare the changes in outcomes over time between a population affected by the tax cuts and the pandemic (the treatment group) and a population not affected (the comparison group). Tax-induced migration can occur along two different margins: the decision of whether to move at all and, conditional on moving, what destination to select. We examine each margin in detail.

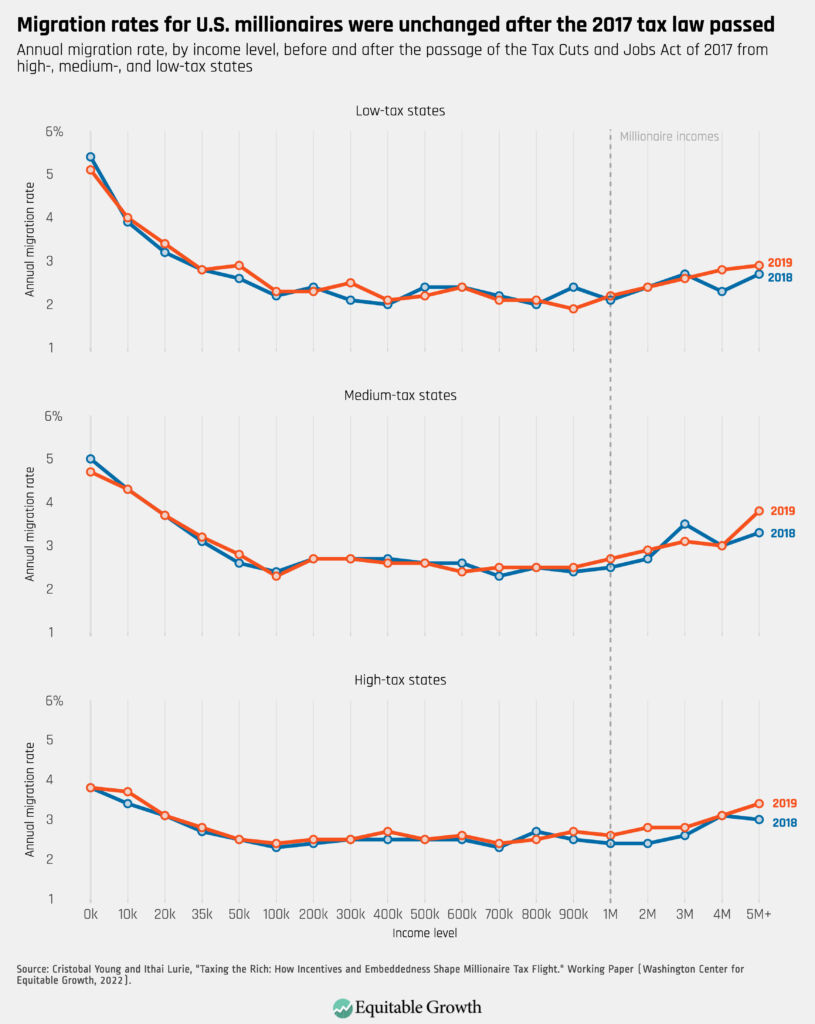

In a typical year, a small number of millionaires circulate between states: Roughly 2.7 percent of the millionaire population moves across state lines, exchanging one state for another. How much did the 2017 tax reform influence this migration? In our working paper, we examined migration rates for every income group, starting from those with the lowest incomes to those making $5 million a year or more. We also examined migration rates for those living in low-tax states, who were incentivized to stay, and high-tax states, who were incentivized to move. Migration patterns before and after the tax reform law passed were essentially identical. (See Figure 1.)

Figure 1

In a 2018 opinion piece published in The Wall Street Journal, “So Long, California. Sayonara, New York,” economists Arthur Laffer and Stephen Moore predicted that “based on the historical relationship between tax rates and migration patterns, both California and New York will lose on net about 800,000 residents over the next three years—roughly twice the number that left from 2014-16.” Then-New York Gov. Andrew Cuomo (D) likewise feared that his state’s millionaires would flee to a better tax environment. Yet our estimate of this migration, as shown in Figure 1, is zero.

Indeed, millionaires generally have low rates of migration—lower than that of the poor—because they are rooted in place by socioeconomic ties, such as employment, marriage, children at home, and business ownership. There is a subset of millionaires with high migration rates and who fit the image of the mobile millionaire. They are relatively young, unmarried, childless, and earn their money from capital rather than work. We term these individuals the “anomic elite,” who are unencumbered by place-based attachments. They move more frequently but are a small minority of the millionaire population.

After the decision to move, a second element of tax migration is the choice of destinations that movers select. To analyze this, we focus only on those millionaires who actually move. Among movers, did lower-tax states become more attractive after federal tax reform?

It is perhaps surprisingly common to see millionaires move into states that charge them higher tax rates. Basketball star LeBron James, for example, made a series of moves from Florida (no income tax) to Ohio (5 percent top rate) to California (13 percent top rate). Many millionaire moves are also between states that have roughly the same tax rate. There are many idiosyncratic and personal reasons why millionaires move, and most migrations do not come with a net tax advantage. Nevertheless, there is a systematic pattern in which low-tax states are favored as migration destinations. The effect is modest, but millionaire migration tends to flow from high-tax to low-tax states.

In our database on cross-border migration flows, the elasticity of the millionaire population with respect to the top tax rate is 0.14. For the average state, if top tax rates rise by 1 percent, this causes roughly 13 more out-migrations and 12 fewer in-migrations, from a base population of more than 9,000 millionaires—amounting to a population loss among millionaires of one-third of 1 percent.

We also see that when the tax reform changed the relative tax rates between states, low-tax states increased their share of millionaire destinations while high-tax states lost shares. For California, the Tax Cuts and Jobs Act produced a loss of roughly 380 millionaires from a base population of 81,000, or 0.5 percent of the millionaire population. Similarly, we calculate that Texas gained 140 millionaires due to the 2017 tax law, a 0.4 percent increase on its base population of 39,000 millionaires.

In summary, the tax reform did not cause greater numbers of millionaires to migrate. But for those already moving anyway, tax reform played a role in where they moved. In other words, taxes do not affect the decision to move, but, conditional on moving, they do influence the choice of destination—making low-tax states incrementally more attractive.

Given this level of tax migration, how should state governments respond? Do some states have tax rates on the rich that are too high? Would states be better off if they cut taxes? To address this question, we incorporate our estimates of millionaire tax migration into a model of optimal tax rates, which calculates the tax rate on top earners that maximizes revenue. We find that the revenue-maximizing tax rate on the rich, combining federal, state, and local income tax rates, is 66 percent. This is much higher than current tax rates in any state. This means that if states cut taxes in an effort to attract millionaires, the revenue losses would far exceed the gains.

For further insight into the role of embeddedness in tax migration, we examine the impact of the COVID-19 pandemic. Arriving shortly on the heels of major tax reform, the pandemic disrupted almost every socioeconomic factor that ties people to places. Offices and schools closed their doors and moved online. Urban amenities were shuttered. And face-to-face contact became a public health problem. Many homes and apartments felt too small for shelter-in-place orders. The pandemic was an occasion to rethink the geography of work and life, especially for top earners, who could work remotely from anywhere. We test whether this disruption to embeddedness ushered in a new wave of millionaire migration away from high-tax places.

The timing of the tax return data offers a unique way to understand the effects of the COVID-19 pandemic on tax migration. There are two kinds of IRS records that show taxpayer residency: W2 forms that report earnings and other information and 1040 tax returns that households file. These forms are sent to the IRS at different times, offering a before-after analysis of the onset of the pandemic.

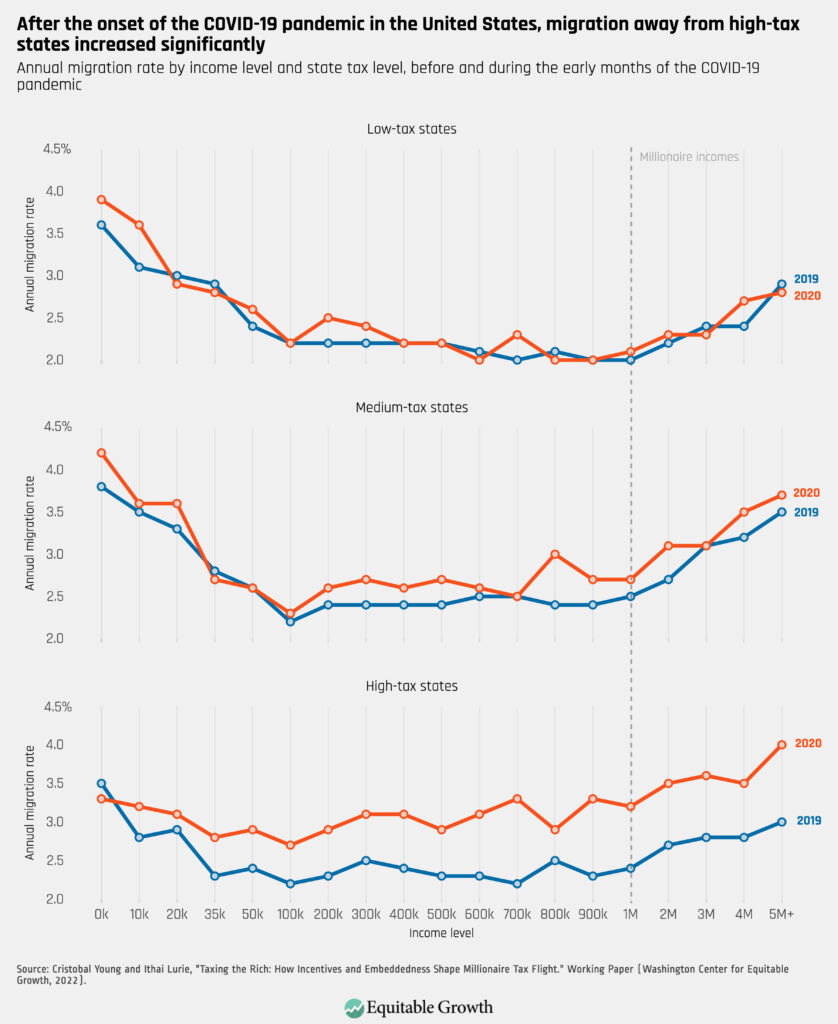

In 2020, W2 forms were sent about 6 weeks before the United States declared COVID-19 a national emergency on March 13, 2020. The deadline for filing 1040 returns, in contrast, was delayed until mid-July of that year, and with no-penalty extensions, most millionaires actually filed their returns in August. This means that migration measured by the W2 forms captures mobility occurring entirely before the pandemic, while migration using the 1040 returns includes moves during the early months of the pandemic. We find a clear rise in migration out of high-tax states, especially among higher-income earners, a very modest pandemic migration effect among middle-tax states, and no change in migration rates among low-tax states during the pandemic. (See Figure 2.)

Figure 2

In short, the pandemic upended many people’s ties to places, providing new opportunities to decouple from where they live and from where they work, especially for high-income earners who were able to work from home. We find that once pandemic restrictions arrived, households began questioning the value of living in expensive, high-tax states. In this sense, diminished embeddedness raised the tax-flight cost of taxing the rich.

Conclusion

Taxes on the rich at the state and local level are not costless, but places have considerable fiscal capacity to set their own policies. Tax flight is a product of both incentives and embeddedness, and elite embeddedness dampens financial incentives for migration. When economic action is embedded in ongoing social relations that shape and constrain market behavior, embeddedness gives a layer of insulation from market incentives and pressures.

In the language of economics, greater embeddedness leads to smaller elasticities. When social ties are strong, fiscal and financial incentives have a smaller playing field and less influence on individual behavior. To counteract millionaire migration, states could cut taxes on the rich, attempting to lure back missing millionaires, but we estimate that cutting state and local taxes on the rich leads to severe revenue losses. Thus, while the 2017 tax cuts indeed benefited red states at the expense of blue states, progressive taxes still generate large revenues for blue state expenditure programs. Embeddedness allows states to experiment with new fiscal policies without risking elite exodus or a deep loss of their tax base.

Nevertheless, a challenge for places with progressive taxes is that embeddedness is weakened due to COVID-19, while tax migration incentives have grown due to the 2017 tax law. There was no state fiscal crisis in high-tax states, but the continuing pandemic and its effects on embeddedness raise important questions. Are work-from-home policies here to stay, or will elite offices return to something of their pre-pandemic concentrations in major cities? Will remote technologies make place-specific social capital less important in the future?

Further research is needed to answer these and other questions to shed valuable light on the future of high-tax, high-amenity places in the United States and on the enduring importance of embeddedness among the wealthy.