Introduction

The U.S. economy has undergone a structural transformation in recent decades. Large firms have shifted from doing many activities in-house to buying goods and services from a complex web of other companies. These outside suppliers make components and provide services in areas such as logistics, cleaning, and information technology.

Deregulation, market failures, and corporate policies have led to the rise of supply chains comprised of small, weak firms that innovate less and pay less. These problems in supply chains threaten U.S. competitiveness by undermining innovation, and also contribute to the erosion of U.S. workers’ standard of living.

Download FileSupply Chains Report

Read the full PDF in your browser

A different kind of outsourcing is possible. Instead of suppliers and contingent workers engaged in a race to the bottom, supply chains could be comprised of skilled specialists who collaborate with each other on innovative products and services. This paper suggests policies to promote supply chain structures that stimulate equitable growth—that is, policies that both promote innovation and also ensure that the gains from innovation are broadly shared.

While decisions about how to structure supply chains matter greatly for working Americans, this topic rarely takes a front seat in discussions of polices to address inequality. This paper aims to remedy this oversight. In order to stimulate equitable growth, policymakers must understand how the economic pie is created—not just how it is divided. Because of the size and importance of supply chains to the U.S. economy, their structure and governance are key determinants of the viability of “good jobs strategies.” Moreover, the way the economic pie is created affects the way it is divided.

We first describe important characteristics of supply chains in the United States. While there are important differences based on industry and lead firm strategy, in general U.S. supply chains are responsible for a significant part of product costs, consist of interconnected networks of independent firms, are largely domestic, and are increasingly made up of small firms.

We then analyze the impact of outsourcing strategies, and find that the current structure and governance of supply chains have had largely negative consequences for innovation and job quality. Next, we examine the market failures and other failures that have led to this state of affairs, and present examples of how more collaborative governance of supply chains and the eco-systems in which they exist leads to better outcomes.

We close the paper with a discussion of ways that supply chain public policies and private business practices can be improved. Key recommendations to improve job quality and boost innovation include:

- Encourage collaborative relationships between lead firms and suppliers

- Nurture productive eco-systems of firms, universities, communities, and unions

- Promote the formation of supply chains in industries that advance national goals

- Promote good jobs and high-road strategies

- Discourage low-road production strategies

- More fairly share the benefits and risks of contingent work

These kinds of public policies and business practices would help to turn the outsourcing of jobs from a weakness into a strength. They would improve the productivity of firms across supply chains, boost innovation, and raise workers’ wages. Taken together, supply chain reforms are vital to enhancing U.S. competitiveness in the global economy, and a key pathway toward equitable growth.

The role of supply chains in the U.S. economy

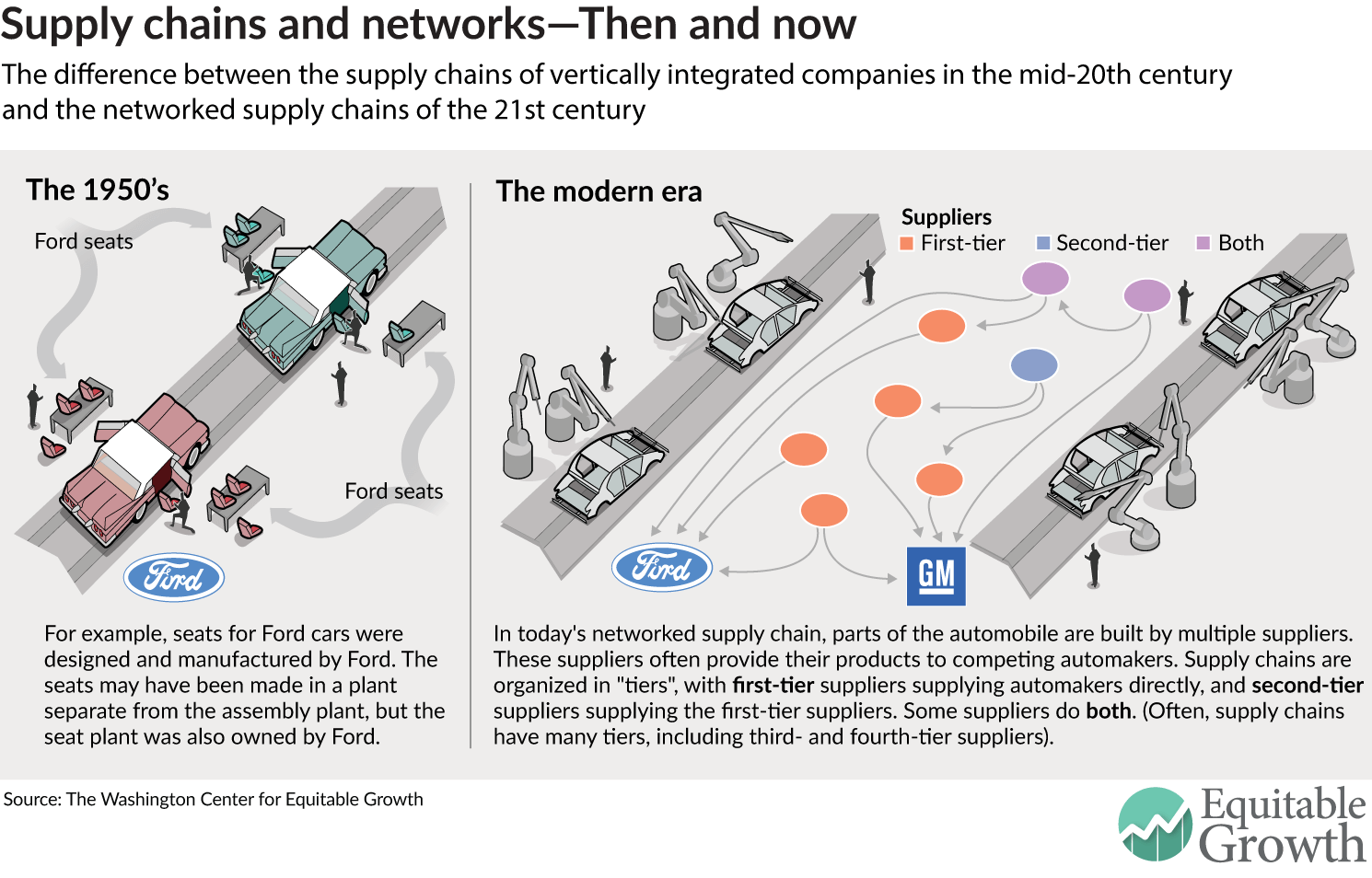

A supply chain links companies—often in multiple industries and multiple locations—to design, produce components, assemble, and distribute a final product such as a car or a computer.1 For much of the 20th century, a significant part of the U.S. economy was characterized by supply chains that were vertically integrated.2 An extreme example is Henry Ford’s production model, in which most parts of the supply chain were located close together and owned by Ford. In the 1920s, ’30s, and ’40s, Ford Motor Company’s River Rouge production complex included offices for product design, furnaces for making iron and steel, electric power generation, plants for making tires, stamped parts, engines, transmissions, radiators, tool and die, and assembly. Ford also owned the natural resources needed to produce automobiles: forests, iron mines and limestone quarries, coal-rich land, and a rubber plantation.3

In contrast, industries such as furniture-making that continued to use production processes with low fixed costs never had much vertical integration.4 Beginning in the 1970s and 1980s, large firms in many industries began to sell off assets and outsource work. This process of outsourcing has given rise to a complex and international web of customer-supplier relationships.5 Now the lead firm typically designs and directs production by multiple tiers of suppliers in many locations but does not own most of these suppliers.6 (See Box.)

Workers and supply chains: outsourcing, offshoring, and contingent work

Discussion of corporate organization suffers from ambiguous definitions of key terms. In this paper, we follow Annette Bernhardt and her co-authors at the University of California-Berkeley’s Center for Labor Research and Education in using the term outsourced to refer to the case where an organization contracts with another organization to provide goods and services, such as production of components or janitorial services.7 By offshored we mean that that work is performed outside the United States. This offshored work may be performed by employees of a lead firm, such as employees of General Electric Company in China, or it may be outsourced to workers at financially independent suppliers.

Supply chains are often dominated by lead firms that direct the companies in the supply chain. Usually these firms are very large, and usually they are customers of other firms in the supply chain, as in the GE example above. Sometimes the lead firm is barely bigger than its suppliers. And in some cases, as with agricultural inputs, large supplier firms such as Monsanto Company or Caterpillar Inc. play a key role in structuring the market faced by their customers (farmers in this case).

Modern supply chains have many layers, or tiers. A lead firm’s direct suppliers are called first-tier suppliers; suppliers to those companies are called second-tier suppliers, and so on. Supply chains may contain the following types of workers:

- Regular employees of a lead firm

- Subcontractors, who may work at a customer firm’s site (such as employees of ManpowerGroup Inc. who assemble parts at a Nissan Motor Co Ltd factory) or at another site, such as employees of an auto supplier that has its own factory that sends parts to Nissan

- Individuals classified (correctly or not) as independent contractors who work for companies in supply chains rather than directly for consumers

Some of the above workers may be contingent, meaning they have only a temporary employment contract. This contract may be with a temporary help agency, such as Manpower, or directly with the firm whose site they work at (direct-hire temporaries). Others may be full-time regular workers, even if they work for a subcontractor or supplier to a lead firm.

These outsourced supply chains, sometimes called Global Value Chains, or GVCs, differ from vertical integration in that the lead firm does not own supplier facilities. The lead firm benefits from this arrangement by gaining access to products made by suppliers with experience making similar products for multiple customers, and by not being responsible for subsidiaries’ fixed costs.

These supply chains also typically differ from economists’ model of perfect competition, in which transactions between firms are at arm’s length and the only information crossing firm boundaries pertains to prices. In the upper tiers of value chains at least, suppliers usually make specialized products for the lead firm and exchange information regarding designs, production processes, and future plans. Suppliers also may have a role in designing the products they provide. The lead firm often exercises detailed control over the operations of suppliers, specifying quality-control procedures and inventory practices. Lead firms find companies in these supply chains advantageous over perfectly competitive markets in that they are able to quickly obtain components tailored to their needs. The complementary disadvantage is that firms are often unable to change suppliers easily.

Firms have two main reasons for outsourcing that are partly in conflict with each other. One is to gain access to specialized knowledge in an area outside the firm’s core competence. An outside supplier typically has multiple customers. Each customer benefits from this state of affairs, due to reduced fixed costs and increased access to suppliers’ experience making similar products for other customers. In contrast, lead firms have reduced incentive to invest in upgrading the supplier’s capabilities if that supplier may also use those capabilities to serve a competitor. A firm’s success depends upon a robust networks of suppliers, but no one firm is responsible for keeping these networks healthy.

Another reason firms outsource is to find input providers that have relatively low bargaining power, so that most profits remain in the hands of the lead company’s shareholders and top executives. Lead firms benefit from the existence of many interchangeable suppliers and workers who are forced to compete against each other to provide the lowest cost. In this cut-throat environment, however, relationships are expected to be short. Parties therefore do not invest in collaboration, and relationships remain arm’s length.

Both reasons for outsourcing have become more compelling in recent decades. An explosion of new materials, technologies, and computing techniques has made it more attractive for lead firms to collaborate with suppliers that specialize in these diverse areas. In the 1960s, for example, a car was largely made of one material (steel) and electronics were confined to the radio. Today, a car contains many materials (including multiple kinds of steel, plastics, and magnesium), several computers, and many electronic sensors. Automakers can learn from suppliers that sell to their rivals and also to other industries, leading to a convergence between Detroit and Silicon Valley.

Deregulation has made interchangeable suppliers even more attractive, as we discuss below. This second reason for outsourcing has often determined the structure of U.S. supply chains in recent decades. Lead firms’ desire to maintain bargaining power has led to supply chains characterized by a “race to the bottom” instead of a more collaborative structure produced by a quest for specialized knowledge. (See Figure 1.)

Figure 1

Characteristics of U.S. manufacturing supply chains

While there are important differences by sector and by lead firm strategy, in general supply chains are responsible for a significant part of manufacturing costs, are largely domestic, consist of interconnected networks of independent firms, and are increasingly made up of small firms. Below we describe each of these features in turn.

Supply chains are responsible for the lion’s share of firms’ costs

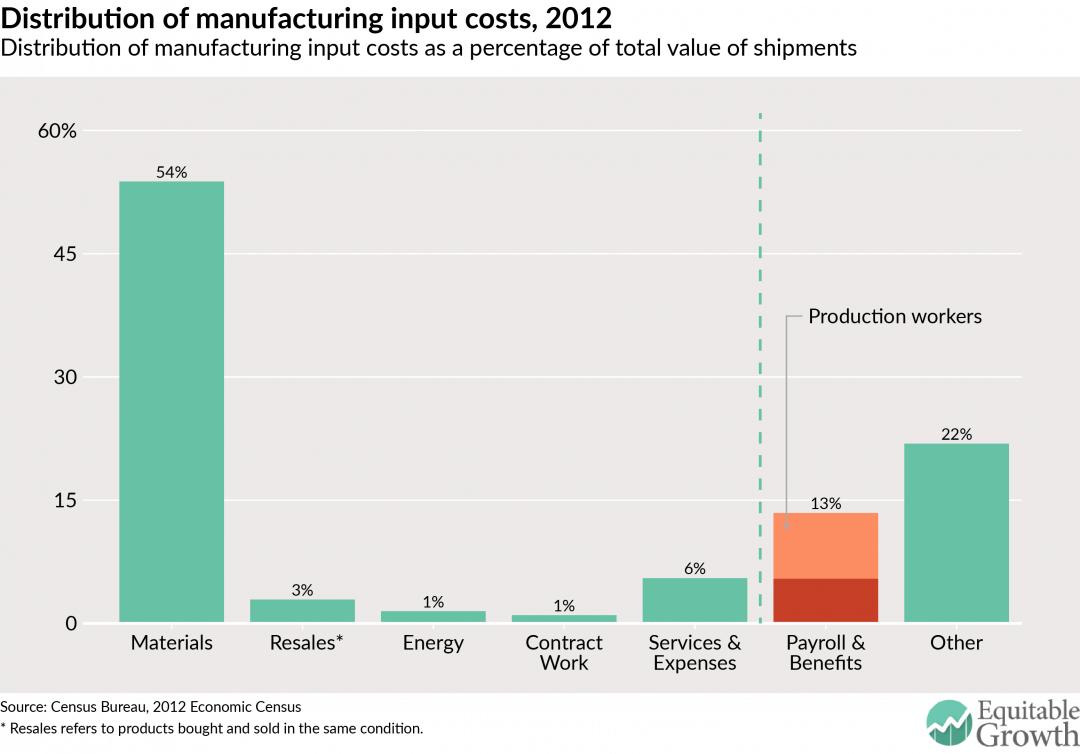

As of 2012, supply chain inputs accounted for 65 percent of the total value of finished goods, or “shipments,” in U.S. manufacturing. For the economy as a whole (including services) the average U.S.-located multinational firm buys intermediate inputs that comprise about 75 percent of the value of their output. A domestically owned firm buys intermediate inputs equal to about 50 percent of output value.8 (See Figure 2.)

Figure 2

Total labor costs in manufacturing are less than 13 percent, and the percentage of costs due to in-house production workers—about which much ink is spilled—is even lower, at 8 percent.9 Of course, suppliers have labor costs as well, so much of the total cost of production is due to labor in the supply chain. Yet, there is much room for efficiency gains in improving the interfaces among firms in the supply chain. Suppliers and customers, for example, can pool their knowledge of production processes and market demand to reduce manufacturing costs by redesigning or eliminating process steps. They also can reduce inventory by improved scheduling. These methods often yield far greater savings than does trying to cut costs by asking workers to do the same tasks, only faster and cheaper.10

Supply chains are largely domestic

In 2008, Apple Inc.’s production of the iPod offered an example of a global value chain in which the company designed in the United States but did not manufacture domestically. The iPod’s parts came from the United States, Japan (the hard disk drive was from Toshiba Corp), South Korea (Samsung Electronics Co., Ltd. manufactured the memory components), and China (small parts came from anonymous companies). Taiwanese companies with factories in mainland China oversaw assembly.11 The iPod is no longer produced, but Apple’s iPhone—and many other electronic devices—are produced in a similar way.

Though well-known, the iPod’s highly-offshored supply chain is not in fact typical of most manufacturing. Proximity advantages and historical relationships create a supplier landscape in which lead firms are more likely to outsource production to other firms in their own country. Thus, the world is not especially “flat” in the sense popularized by the author and New York Times columnist Thomas Friedman.12

This is true of the United States, where most supplier-customer relationships still involve two U.S. firms. In 2010, Universtiy of California-Berkeley economist Clair Brown and her co-authors found that 48 percent of full-time employees in the U.S. economy (including manufacturing, service sector, and nonprofit workers) worked at firms that outsourced work domestically, whereas only 23 percent of American employees worked at firms that sourced internationally.13 Only about 10 percent of intermediate inputs are imported for a typical U.S. firm.14

Figure 3

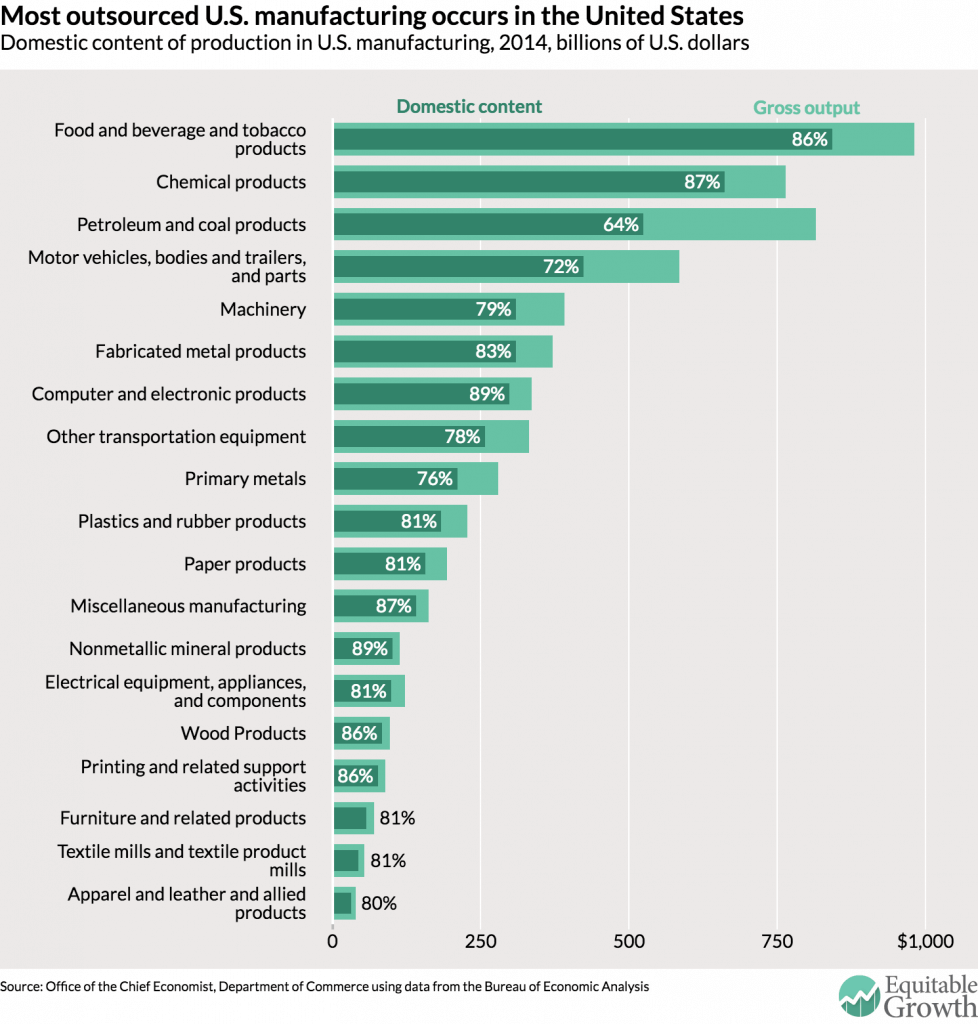

In U.S. manufacturing in 2012, imported content was about 21 percent of the value of output for a typical firm.15 That is, of the $5.6 trillion of goods U.S. manufacturing firms sold in 2012, $4.4 trillion, or 79 percent, was “Made in the U.S.A.” Figure 3 shows the percentage of domestic sourcing by sector for products that are manufactured domestically.

Overall, however, only 53 percent of U.S. domestic demand for manufactured goods is made in the United States. To understand the difference, consider again the electronics supply chain discussed above. When “computer and electronics products” are made in the United States, their domestic content is 89 percent as Figure 3 illustrates. That is, U.S. manufacturing supply chains are not particularly “hollowed out,” even in electronics. But most computer and electronics products are not made in the United States. Seventy-two percent of total domestic demand for such products is met by imports, including imports of products such as iPhones.16 Globally, the picture is similar. For a typical global value chain, the foreign value-added share was only 34 percent in 2008, up from 28 percent in 1995.17

Supply chains are often interconnected

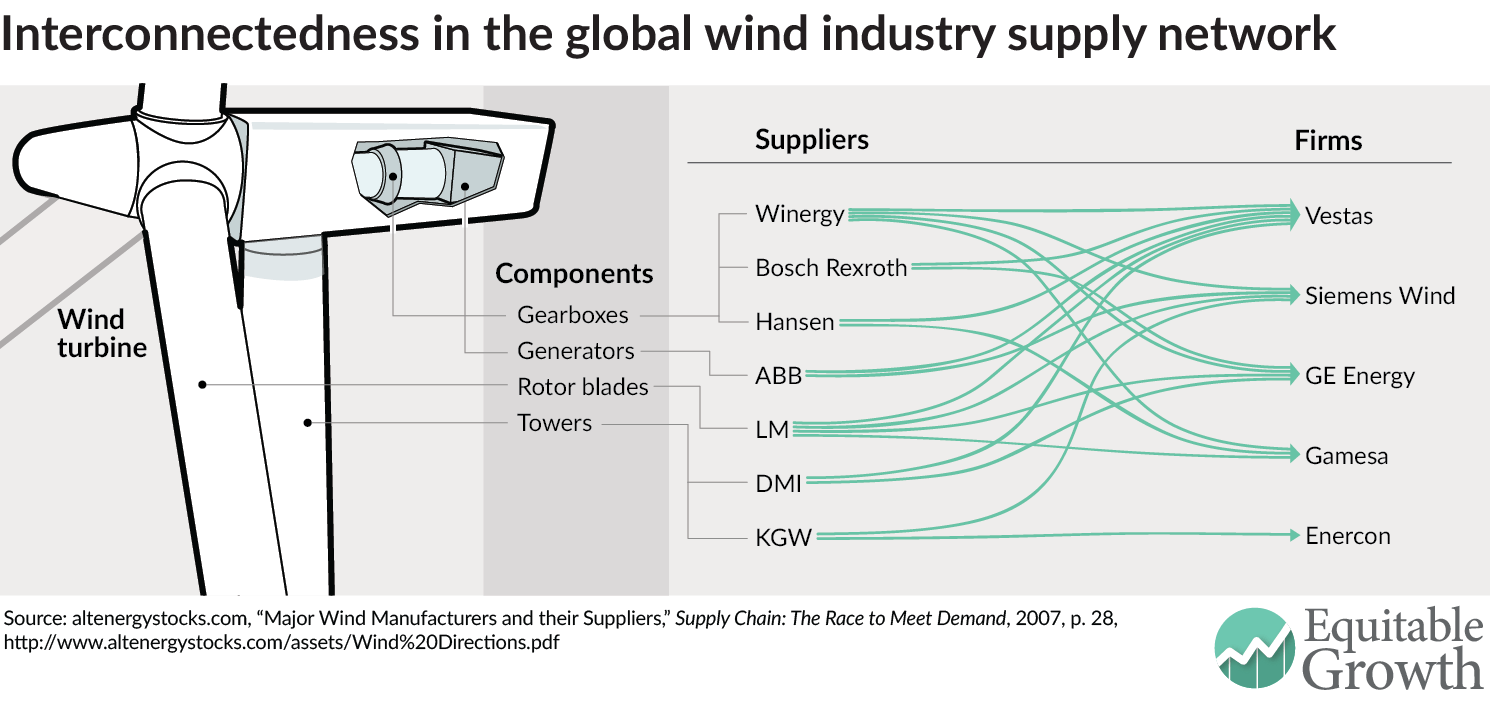

The iPod case highlights a key result of vertical disintegration: Large corporations now often share, rather than own, the production networks upon which they rely. For example, a 2007 study of wind turbine supply chains found that Winergy, a unit of Siemens AG, supplied gearboxes and LM Wind Power A/S supplied rotor blades to four of five lead firms.18 (See Figure 4.)

Figure 4

Interconnectedness can lead to vulnerability if it is hard for firms to switch suppliers, as occurred during the 2009 automobile industry crisis sparked by the Great Recession. Alan Mulally, president and chief executive of Ford Motor Co., found himself in the unusual position of asking the U.S. Congress to bail out two key rivals—General Motors Co. and Chrysler19—because of the harm their bankruptcies would have inflicted on the supply chain that Ford shared with them. Ford benefited from not having to make duplicative investments in suppliers, but suffered a risk of contagion. If Chrysler or General Motors had gone out of business, critical suppliers for all of Detroit’s Big Three automakers would likely have shut their doors as well, causing Ford to shut down “within days—if not hours” due to lack of parts.20

In other cases, supply chains experience a lot of churn, particularly among third- and fourth-tier firms. In the garment industry, for example, competition is so intense that small firms frequently go bankrupt or are shut down for violation of labor laws. Owners of the defunct firms often re-open quickly under a new name and in a slightly different location. This churn makes it difficult for retailers to adopt potentially more profitable “quick-response” strategies that reduce suppliers’ lead time but would require collective investment in training and capital.21

Governance of supply chains varies widely by industry and by lead firm

Supply chain structures vary with industry characteristics, such as the complexity of information that traverses organizational boundaries, the importance of tacit knowledge that is best conveyed through interpersonal interaction, and the technological capabilities required to supply a certain industry.22 But these industry characteristics are not exogenously given. In fact, lead-firm strategy often drives industry structure. As the automotive example below demonstrates, there is significant variation in supplier-customer relationships within the same industry,23 and lead-firm strategy may have a powerful effect on supplier capability.24

A key determinant of what choice the lead firm makes is the amount of market power it has over its final customers. For most of the 20th century, General Motors had a great deal of market power in the United States, giving the firm an incentive to protect the resulting profits from being shared with its suppliers. Retaining bargaining power requires maintaining a credible threat to exit, meaning that the lead firm often offers only short-term contracts, and neither supplier nor purchaser invests much in relationship-specific knowledge or equipment.

Maintaining power in this way, however, comes at a cost to efficiency.25 The automaker retained power by unbundling tasks—for example by separating design and production, and dividing components into smaller subcomponents. Dividing work in this way reduced barriers to entry, which created competitive markets for individual tasks and allowed lead firms to protect their final-product market rents from being shared with suppliers. Such strategies were common in U.S. manufacturing in the mid 20th century.

Over time, this separation between tasks may weaken productive eco-systems and diminish national competitiveness. Particularly damaging is the separation of innovation and production—when the lead firm no longer knows how to make a part, it also loses potential opportunities for innovation.26 In contrast, the Japanese automaker Toyota established longer-term, information-rich relations with suppliers, gaining insight about the root causes of quality problems. Toyota helped to transform its suppliers in Japan from small workshops into world-class producers through extensive technical assistance.27

In some cases, lead firms choose suppliers located nearby. Sometimes, co-locational decisions are strategic, intended to increase productivity, prevent intellectual property leakage, or create shared knowledge. In other cases, firms shift work to low-wage areas. In these cases, outsourcing decisions are often evaluated based on broad strategic principles rather than in-depth analysis of each choice. For instance, many U.S. automotive manufacturers shifted production—both their own and their suppliers’—to southern states such as Alabama and South Carolina during the 1990s and early 2000s. Managers at these firms describe a two-step process. First, corporate executives made a strategic decision to shift work south. Then, middle managers and sourcing professionals evaluated future sourcing decisions in the context of the previous companywide directive.

These outsourcing decisions to relocate everything to one location are based on the idea that a geographic strategy can create strategic unity, save time, create consistency of managerial thought across subsequent waves of management, and maybe lead to cluster-based advantages down the road. Many firms also pursue this strategy to avoid creating a supply chain that spans too many regions, since operating in multiple regions spread over great distances can be difficult.

Other lead firms attempt to make sourcing decisions on a case-by-case basis, and are comfortable with a greater level of complexity. IBM Corp. provides an example of a large, global firm with such complex supply chains that it depends upon third-party and even fourth-party logistics firms, or 4PLs, to oversee them.28 4PLs coordinate sourcing decisions among multiple third-party logistics coordinators. In effect, IBM has outsourced much of its sourcing decision-making apparatus. Given its strong desire to focus on core competencies such as data analytics and cloud computing, the company deems this a worthwhile trade-off. The fact that its employees and customers live on six continents may contribute to the firm’s embrace of a supplier network that spans 100 countries.

Lead firms often lack information about the lower tiers of their supply chain

Some lead firms have a general sense of their immediate suppliers, but not those suppliers’ suppliers.29 Others have a much deeper understanding of their whole supply chains. Despite extensive academic work on the value of information sharing and strong supplier-customer relationships, these views are not embraced throughout U.S. manufacturing.30 Large customers often find it difficult to maintain accurate information on lower tier suppliers. This is especially true in low-trust relationships, where customer firms frequently switch suppliers, and direct suppliers may not wish to reveal the names of their suppliers further down the chain.

Similarly, the amount of information that small firms maintain about downstream value chains varies. For instance, a chemical treatment firm and a metal stamping firm interviewed in 2010 reported that their business models depend upon high numbers of one-off batches. Maintaining detailed knowledge of their customers, who these firm’s managers rarely meet in person, is viewed as neither critical nor practical.

U.S. manufacturing supply chains are increasingly made up of small firms

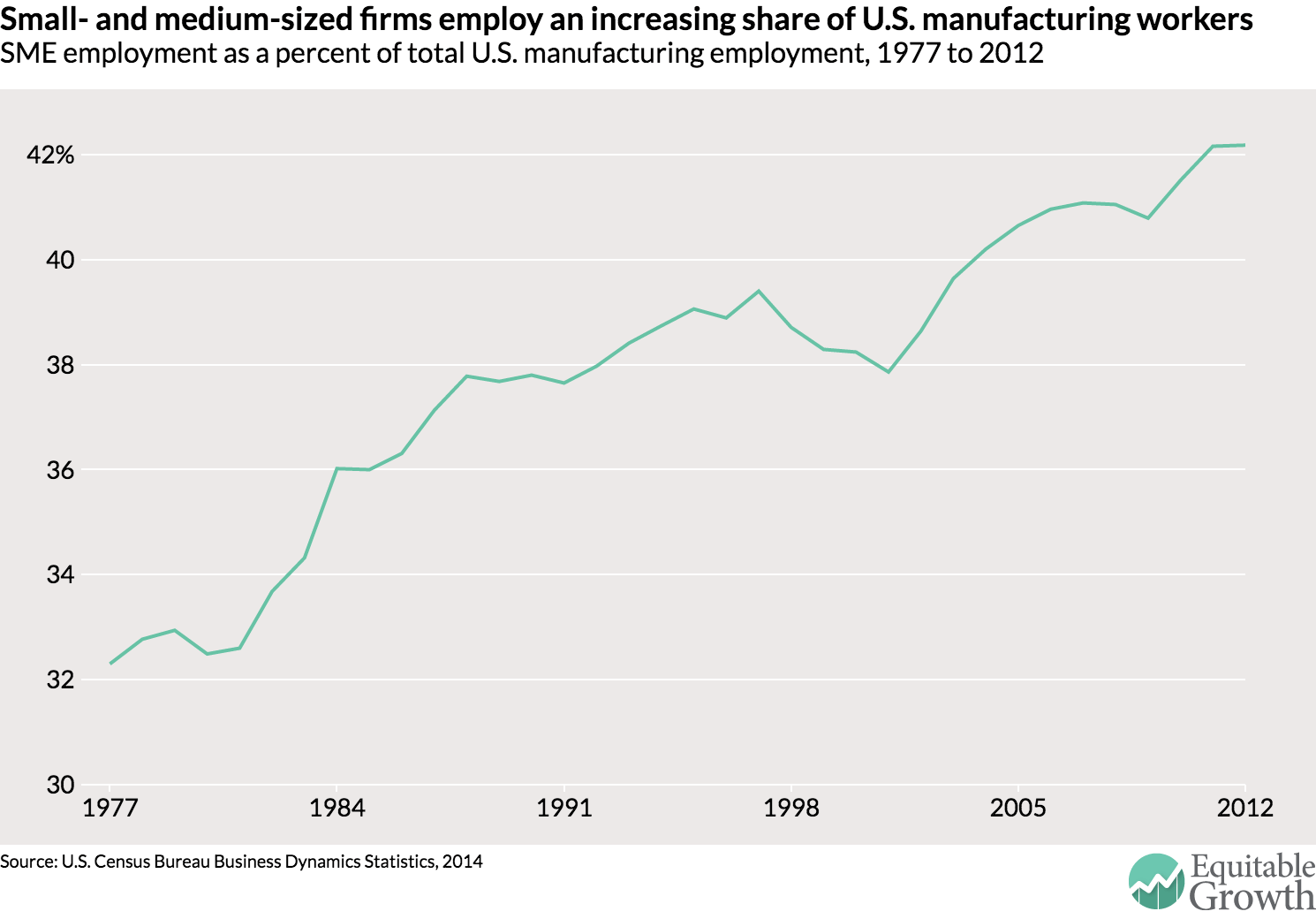

In 1980, small- and mid-sized enterprises, or SMEs, defined as businesses with direct employment of fewer than 500 people, accounted for 32.5 percent of U.S. manufacturing employment. By 2012, this figure had grown to over 42 percent. SMEs have played an outsized role in the recovery of the U.S. manufacturing sector. Since 2010, more than 50 percent of manufacturing employment growth has taken place at small manufacturing firms.31 (See Figure 5.)

Figure 5

Innovation and wage challenges due to the U.S. supply chain structure

In the first section of this report, we showed that despite differences by industry and region, U.S. supply chains represent almost two-thirds of manufacturing costs. They are largely domestic, consist of interconnected networks of independent firms, are governed in diverse ways, and are increasingly made up of small firms.

In this section, we consider the impact of these features on the performance of supply chains as measured by innovation and wages.32 Next, we present suggestive evidence that collaborative supply chains and vibrant eco-systems result in better outcomes for many lead firms and for the U.S. economy overall. Yet, we also find that U.S. small firms, on average, struggle both to innovate and to provide high-quality jobs—a state of affairs that is not inevitable but rather is a result of market and policy failures both within and between firms.

Macroeconomic impacts of supply chain structure

While the structure of supply chains has important impacts on innovation and job quality, it also has important (and little-studied) impacts on macroeconomic outcomes. To the extent that “the linkage structure in the economy is dominated by a small number of hubs supplying inputs to many different firms or sectors,” a hiccup in one hub may have impacts that spread across the globe, as was the case with the global disruption caused by the Fukushima tsunami.33

The potential for disruption is even greater if firms lack knowledge of which firms make up their supply chains. This lack of visibility is particularly acute in supply chains with many tiers, and has proven quite costly when supply chains are disrupted. Forty percent of the world’s automotive microcontrollers, for example, were made in a single plant in Japan—a plant that was severely damaged in the 2011 tsunami.34 Many automakers (including U.S.-based firms) were surprised to find that this plant was deep in their supply chains, and global vehicle production was disrupted for weeks.35

In contrast, other linkage structures could lead to more risk-pooling, which provides increased stability. Case in point: The growing use of outsourced services—legal, advertising, janitorial, temporary help—may mean that a supplier is less susceptible to shocks to their various clients: When one client’s business is down, another client’s business may be up.36

Implications of supply chain structure for innovation

Because innovation is concentrated in manufacturing—indeed, two-thirds of private-sector research and development is performed in manufacturing—this section looks at supply chains in manufacturing only. Data is not readily available for innovation in other sectors, in part because so much of it takes place in manufacturing.

Economists often divide innovation into three phases.

The first phase is invention, in which the product or process is created for the first time. Spending on research and development is a key indicator of inventiveness. Small- and mid-sized firms are only about 15 percent as likely as large firms to conduct R&D. While SMEs employ 42 percent of the U.S. manufacturing workforce, they conduct only 33 percent of manufacturing R&D.37

Commercialization is the second phase of the innovation process. This involves taking a new process or prototype product out of the lab and figuring out how to manufacture and sell it economically in large-scale production. Small firms often struggle with this step because they lack the financial and marketing advantages enjoyed by large firms. Compared to large firms, small firms lack retained earnings and have more difficulty gaining access to external finance because they also lack collateral. Large firms also tend to have formal processes for launching and marketing new innovations. These processes involve professionals from diverse backgrounds such as finance, design, and marketing. In small firms, the same individuals responsible for daily production and sales often must grapple with these commercialization challenges as well.

The third phase of innovation is adoption of a new product or process after it has been developed and commercialized by others and shown to be commercially viable. Small firms struggle in this stage as well. Overall, small firms are only 60 percent as productive in manufacturing as large firms due to difficulty in financing and learning about new technology that would increase productivity.38 In addition, small firm productivity growth is hampered by failure to adopt proven managerial techniques. Fewer than half of small auto suppliers, for example, have adopted quality circles (in which production employees gather regularly to troubleshoot quality concerns) and only two-thirds of them self report that they consistently perform preventative maintenance.39 Again, an expertise gap contributes to this productivity gap. Large firms have the money and human resources programs to hire experienced and well-educated managers, engineers, and consultants. By comparison, a quarter of small automotive firms employ no engineers.40

A skeptic may ask why large lead firms cannot innovate enough to support their entire production network. But problems such as reducing the vibration of a wind turbine cannot be solved in advance or from afar. Solving problems such as these require both hands-on analysis of each part of the production process and holistic problem-solving: A machine composed of many parts that exert strong forces on each other cannot simply be divided into one problem for the gearbox manufacturer to solve, one for the rotor manufacturer to solve, and another for the assembly team to solve. Limiting innovation only to lead firms also deprives the supply chain of insights that come from being very close to a particular type of production or use.

Long-term supplier-customer relationships built upon trust and collaboration best facilitate de-bugging of new products and processes. Lack of such relationships accounts for many of the problems U.S. industries face in moving new technologies from lab to market.41 When production and innovation are separated by geographic and firm boundaries, and firms don’t know even the identity of suppliers in other tiers, it is difficult for them to adopt techniques such as value analysis/value engineering, or VAVE, in which firms in a supply chain jointly analyze the value of each process step. As a result, VAVE has not been widely adopted in the United States despite strong evidence of its effectiveness. A 2011 survey of U.S. auto suppliers found that less than one-third had adopted the technique.42

In short, network problems are everyone’s problems. Some of the most important problems associated with outsourcing take place at the network level, compromising the health of broader supply networks. Put more optimistically, policy that helps address these network problems can create economy-wide benefits that are captured by more than just one firm. We discuss proposals to do that in the final section of this report.

Implications of supply chain structure for job quality

Workers are employed in supply chains in a variety of ways. (See side bar “Workers and supply chains: outsourcing, offshoring, and contingent work”. Instead of being hired directly by lead firms as regular employees, workers may be hired by temporary help agencies. This “contingent work” has become increasingly important to the U.S. economy. The share of contingent work at firms with more than 1,000 employees grew from 12 percent in 2009 to 18 percent in 2014.43 These arrangements allow firms to quickly adapt to volatile work volumes by increasing and reducing labor as needed. Workers bear the brunt of this uncertainty in income, though some employees appreciate the greater flexibility of temp work.

Alternatively, workers may be hired as regular workers at supplier firms. In other cases, workers are hired to work at in-house subcontractor firms, often with the status of regular employees. In still other cases, they are hired as independent contractors.

Sometimes workers who should be counted as employees are misclassified as independent contractors, thus allowing firms to avoid paying employee benefits. In order to hire someone as an independent contractor instead of an employee, the individual must satisfy stringent legal tests, such as having multiple customers and having autonomy in determining work methods. Yet some companies have taken advantage of gray areas in these definitions to shift the risk of layoffs when demand goes down (and sometimes safety risk in dangerous workplaces) to individual workers, while maintaining detailed control over their activities. In a high-profile case settled in 2015, FedEx Corp. was found to have misclassified drivers as independent contractors.44 The resolution involved creating a $228 million fund to compensate drivers for the benefits that would have been due to them had they been correctly classified as employees.

Relatively little research has been done of the impacts on employees of these trends. Several studies have compared the fortunes of workers at lead firms and outsourced workers doing similar tasks. The general finding is that the process of outsourcing typically creates undesirable outcomes for workers in areas such as wages, benefits, job security, and safety.45 In the United States, economists at the University of Massachusetts-Amherst and the University of Maryland found that when janitors and guards are not employed by the owner of the establishment they work in, their wages and access to health benefits fall significantly.46 A German study examining the impact of moving cleaning, security, and logistics outside of a firm found that, after a decade, wages for the outsourced work were 10 percent to 15 percent lower than wages for similar work that was not outsourced.47

Employment outcomes are particularly bad for part-time or temporary workers. A 2015 Government Accountability Office study found these contingent workers were at greater risk of workplace injury, and earned 10.5 percent less per hour and 47.9 percent less per year than non-contingent workers.48

Three main reasons explain these negative effects of outsourcing on job quality.

First, outsourcing of work often reduces “rent-sharing,” or suppliers’ access to profits earned by the lead firm. Organizational structures tend to minimize wage differentials within firms, due both to norms of fairness and to a desire to promote cooperation within an organization.49 Thus, janitors that work for a large company earn more than janitors performing similar work for a small company.50 This form of outsourcing often increases occupational segregation, meaning that the earnings of workers in lower-wage occupations are not pulled up by having higher-wage colleagues.

Research finds that most of the recent increase in wage inequality has taken place between establishments, consistent with a story of increased occupational segregation.51 Workers at large firms not only benefit from higher wages in the short run, but also gain access to better career paths in the long run. Large firms have diverse job functions, many levels of management, and formal training or mentoring programs, which means employees at large firms have more opportunities to gain both skills and responsibility and to increase their economic value over time.

Second, the recent outsourcing wave has taken place in the context of deregulation of labor, product, and financial markets. One example of the impact of this political context is that under U.S. labor law it is difficult to establish unions at new worksites or with new employers. Thus, a mature firm will find it very difficult to de-certify an in-house union but it can gain access to a non-unionized workforce by simply contracting work to an outside firm. (We provide further examples below.)

Third, in part because of the bargaining power-based strategies incentivized by deregulation, outsourcing has been associated with an increased role for small businesses, which generally pay less. This “size premium” among firms has been well documented in academic literature for more than a century, and persists across national boundaries and different industries.52 There are several reasons for this size premium. As discussed above, small firms in the United States experience lower productivity and innovation, meaning they cannot afford to pay the same wages that large firms offer. Even if productivity is similar as measured in units of output per hour, smaller firms are more easily replaced as subcontractors, which means they have less bargaining power than larger firms.

Finally, owners of small firms are better able to personally supervise workers than are owners of large firms. Large firms often find it preferable to use an “efficiency wage” strategy of paying above-market compensation so that workers will work hard even without being closely supervised, out of satisfaction with the high wage or fear of losing a good job.53

But the outcomes of outsourcing are not always negative. The types of outsourcing that have been most studied (moving work from regular workers at lead firms to employees at temp agencies or at subcontractors) are the types of work most likely to suffer from the occupational segregation, de-unionization, and size premium effects discussed above. Other kinds of outsourcing may have less negative effects, but have been studied less. The effects of occupational segregation, for example, might work in reverse to increase wages for white-collar workers—say, in information technology jobs or in payroll processing—whose work is outsourced from low-wage firms.54 In addition, when work is outsourced to a supplier with market power, workers may be able to bargain for a share of the resulting profits. We discuss suggestive evidence on this point below, as well as policies that promote better job quality in supply chains.

The recent rise in outsourcing is in large part a response to a particular environment, one characterized by the deregulation of financial, product, and labor markets. This deregulation, combined with the rise of the view that corporations exist to maximize shareholder value led to increased interest in maximizing return on assets by reducing assets, in part by dismantling managerial hierarchies. Financial deregulation and the rise of incentive compensation for top management gave these managers enormous incentives to slice and dice corporate structures.55 Relaxed antitrust enforcement allowed lead firms to increase their product market power,56 while erosion of government-provided worker protections made it increasingly attractive for lead firms to seek to escape the rent-sharing imperatives of their internal labor markets by outsourcing to suppliers they attempted to keep relatively interchangeable.57 Given this context, it is not surprising that firms promoted outsourcing strategies that would maximize their bargaining power rather than their knowledge.

Yet we also see some hopeful signs. While decades of outsourcing have dismantled vertically integrated structures that offered some power to workers, the restructuring that has followed may create new potential sources of power. Much production now relies on “just-in-time” supply strategies (carrying very little inventory, and relies on relatively few warehousing and logistics providers).58

The recent decision by the National Labor Relations Board in the Browning-Ferris case will help reduce “race to the bottom” outsourcing. Browning-Ferris Industries Inc. employed temps who had voted to join the same Teamsters local union as the company’s regular workers. The NLRB held that Browning-Ferris was a joint employer (with the temp agency) of the temporary workers, because the company played an important role in determining the conditions of work. (Browning-Ferris controlled the speed of conveyor belts, and had the right to discharge any agency worker.) Before this decision, the company controlled the conditions of work, but wasn’t considered the temps’ employer. Therefore it had no legal obligation to bargain with them. And if temps engaged in concerted activity then the company could discharge them simply by requesting replacements from the staffing agency. As a result of the decision (if it withstands court challenge), temps can now organize, and both the temp agency and the contracting employer would have to sit at the bargaining table.59

Market and network failures in supply chains

In the previous section, we showed that the central tendency of U.S. supply chains was to suppress innovation and make jobs worse. Below we address the question of why this situation persists and explore some cases of innovative supply chains with good jobs.

Supply chain governance suffers from three forms of market failure:

- Free-rider problems between firms. When a lead firm makes investments in upgrading its suppliers—by providing technical assistance to suppliers, training supplier workers, or helping them invest in new equipment—some of this improved capability will often spill over to benefit a supplier’s other customers, including the lead firm’s rivals. Lead firms thus have less incentive to invest in their suppliers than would be socially beneficial.60

- Siloes within firms. Internal conflicts between departments within a firm can lead to a focus on finding suppliers offering low prices rather than those providing high quality and innovation. An easy way for firms to evaluate their purchasing departments, for example, is by evaluating the extent to which they reduce the price per unit they buy. In this case, a purchasing agent can be rewarded for choosing a supplier whose costs were $1,000 less than a rival supplier—even if that supplier’s skimping on quality control causes the shutdown of a line that costs the operations department $100,000. It may seem unlikely that sophisticated companies would fall prey to such problems, but often the cause and effect are not so clear cut. Quality and innovation are harder to measure than prices, and their benefits often accrue to departments other than purchasing.61

- Profit protection. Outsourcing of work often reduces workers’ access to profits earned by the lead firm. As discussed above, there are pressures to minimize wage differentials within firms, due to both norms of fairness and to a desire to promote cooperation within an organization. Firms with a high degree of market power have lots of profits to protect, which they often do by adopting policies that make their suppliers interchangeable, even at a cost to efficiency.62

The result of these market failures has been an emphasis in the United States on arm’s length rather than collaborative governance of supply chains. The result is a hollowing out of productive eco-systems as firms divested in-house divisions and maintained incentives for their purchasing departments that privilege supplier firms that could win competitive bidding wars. These “winners” tended to be small firms, with low expenditures on overhead costs covering such things as salaries for managers and engineers and worker training. In extreme cases, such as garment production or janitorial services, competition has been so fierce that firms compete in part by violating laws on safety, minimum wages, overtime, and disposal of toxic waste. In this era of lax regulation, these firms have seldom been caught. When they have been, they sometimes were able to file for bankruptcy and re-open under another name.63

While addressing market failures is important, recent research on manufacturing supply chains suggests that it is not sufficient. Networks may fail as well.64 They may simply fall apart or they may stagnate due to the absence of new blood.65 Perhaps because these types of network failure do not fit into conventional economic theories of market failure, public policy has been slow to address them.66 Doing so goes beyond simply providing tax breaks for individual firms. Instead, government can play an important role in enhancing the health and vitality of relationships within existing networks. Policy can reduce uncertainty, risk, and incompetence within knowledge networks, enabling them to be more productive. A century ago, the federal government played this role in agriculture by funding land grant universities, which led not only to the creation of knowledge but also created durable networks of researchers and practitioners through which such knowledge could quickly spread.67

Policies for innovative supply chains with good jobs

Outsourcing has its advantages, principally in making possible a potentially efficient division of labor in which specialist firms can achieve economies of scale and diffuse best practices by serving a variety of customers. Yet lead firms’ zealous embrace of the non-collaborative version of this strategy has resulted in significant weaknesses in innovation and job quality in the United States.

Just as the rise of outsourcing strategies was not inevitable, neither is the continuation of the problems described above. Creating solutions to these challenges will help to address some of the root causes of wage inequality and productivity stagnation in U.S. manufacturing and service industries.

Such policies could improve the performance of small- and medium-sized firms, which already have significant advantages over their larger brethren in nimbleness and strong community ties. Supportive financial institutions, non-profit research organizations, and unions could help them perform better even on the metrics of innovation and job quality. Germany’s Mittelstand (medium-sized firms) are the backbone of the German manufacturing sector due to the help they get from community banks, applied research institutes, and unions.68 In the United States, the unionized construction sector has developed structures that create good jobs and fast diffusion of new techniques, even though the industry remains characterized by small firms and work that is often short-term and intermittent. Building trades unions work with signatory employers to provide apprenticeships, continuing education programs, and portable benefits.

Policies to address these issues should be rooted in the understanding that outsourcing will almost always have both desirable and undesirable consequences. When done well, though, less powerful actors such as workers and small firms can capture at least some of the positive effects. Six key policies could contribute to more equitable economic growth:

- Encourage collaborative relationships between lead firms and suppliers

- Nurture productive eco-systems of firms, universities, communities, and unions

- Promote formation of supply chains in industries that advance national goals

- Promote good jobs and high-road strategies

- Discourage low-road production strategies

- More fairly share the benefits and risks of contingent work

Let’s examine each of these policy recommendations in turn.

Encourage collaborative relationships between customers and suppliers

Government support for economic growth has long focused on the diffusion of physical technologies, yet the diffusion of operational insights may be just as valuable. The White House Supply Chain Innovation Initiative summarized the evidence, showing that lead firms that adopt collaborative supply chain practices are more likely to increase innovation, to the benefit of a variety of stakeholders.69 The White House report highlighted three such practices:

- Lead firms should offer suppliers assurance that they will receive a fair return on investments they make in new technologies and in upgrading their capabilities. In order to become partners in innovation, suppliers need to develop better capabilities in product and process design, and upgrade equipment. Trust is a necessary precursor to mutually beneficial investment because both parties need to know the relationship will last long enough to justify the investments.

- Lead firms should promote information-sharing and make changes in their own operations as a result of supplier suggestions. A key insight from the Toyota Production System is that firms and workers who are close to production have access to information not easily available to those at the top of the chain.70 Firms that establish mechanisms to learn from their suppliers (such as value analysis) can significantly improve cost and quality.

- Lead firms should use a “total cost of ownership”approach when making purchasing decisions. They should consider impacts of sourcing decisions on quality and innovation as well as price per unit purchased.71 Interviews suggest that many firms, some of them quite large, rely upon back-of-the-envelope calculations to make important sourcing decisions. These firms are likely to ignore costs of non-collaborative outsourcing, such as poor quality, hidden inventory costs, and less reliable delivery—costs that often accrue to departments other than those making sourcing decisions.

The benefits associated with awarding contracts based on these three collaborative supply chain practices create value and reliability for firms, as compared to the arm’s length, low-price-per-unit approach to outsourcing. Forming long-term, collaborative relationships with highly competent suppliers may be in a firm’s best overall interests, yet purchasing departments are not always incentivized to consider these benefits. Employees looking to improve their department’s performance as measured by a narrow set of cost variables may have little way of viewing the larger picture. Supply chain practices need to be designed to help managers overcome these problems of information siloes and misaligned incentives within firms.

Public officials can promote adoption of these business practices by using the bully pulpit, and convening companies in supply chains to discuss common problems. Government purchasers could build on their (nascent) efforts to consider total cost of ownership rather than the lowest bidder on a per-unit basis.

Nurture productive eco-systems of firms, universities, communities, and unions

One reason for the struggles that small- and medium-sized U.S. firms face is that they are “home alone” with few institutions to help with innovation, training and finance.72 For reasons of both equity and efficiency, these firms should not depend solely on their customers for strategic support.

Policies that nurture small firms, local universities, their communities, unions, and community banks could help the firms leverage their advantages over their larger brethren in nimbleness and strong community ties. As mentioned above, such supportive infrastructure enables Germany’s Mittelstand to exist as the backbone of the German manufacturing sector. In the United States, the unionized construction sector has developed structures that create good jobs and fast diffusion of new techniques, even though the industry remains characterized by small firms and work that is often intermittent. Building trades unions work with signatory employers to provide apprenticeships, continuing education programs, and portable benefits.

Federal technology assets should be better deployed as well, continuing the work begun by the Obama White House Supply Chain Innovation Initiative. National labs can be encouraged to work with small as well as large firms, for example, and the Manufacturing Extension Partnership can expand its efforts to work with entire supply chains (rather than firms one by one) to identify sources of inefficiency. A century ago, the federal government played this role in agriculture by funding land grant universities, which led not only to the creation of knowledge but also created durable networks of researchers and practitioners through which such knowledge could quickly spread.73

Government budgets would be more effectively spent on building these eco-systems rather than used for “tax expenditures” or tax breaks for individual firms. The United States spends more than $60 billion on such tax breaks every year, with little if any net impact.74 In fact, the federal government could discourage the use of such incentives at the state and local level by making them taxable at the federal level.

Promote formation of supply chains in industries that advance national goals

The free-rider problems discussed above are likely to be particularly acute in developing collaborative supply chains for new products, such as improved solar panels or wind turbines. These industries face additional market failures leading to underinvestment in addressing climate change. The Obama Administration’s “Clean Energy Manufacturing Initiative” helps to move new technologies out of the laboratory and into production. It would be useful to explicitly address the incentive and information issues in supply chains for producing and installing these products. The next administration could convene firms throughout the supply chain to engage in value analysis to improve product designs, to uncover hidden pockets of inventory, and to adopt total cost of ownership techniques.

Promote good jobs and high-road strategies

Much research documents the ways that firms can utilize “high-road” policies or “good jobs” strategies to tap the knowledge of all their workers to create innovative products and processes. High-road firms remain in business while paying higher wages than their competitors because their highly skilled workers help these firms achieve high rates of innovation, quality, and the ability to respond quickly to unexpected situations. Shop-floor workers can play an important role by participating in continuous improvement activities. These activities increase the return to having skilled and motivated workers, who are most effective if they are paid above-average wages. The resulting high productivity allows these firms to pay high wages while still making fair profits.

A robust body of literature shows the feasibility of these good-jobs strategies.75 Most research in this area looks only at practices adopted within firms and does not consider the impact of supply chain governance. Yet some evidence suggests that collaborative supply chain governance also can play an important role in providing stability and ongoing demand for problem-solving,

One very narrow industry, automotive stamping, provides an example. Automotive stampers—firms classified by the U.S. Census in in its North American Industry Classification System codes, specifically NAICS 332116 and 336370—use stamping presses to produce automotive parts from sheet metal. Like most industries, this industry is characterized by wide dispersion in productivity. Firms in in the 90th percentile on productivity are more than twice as productive as the median firm. These high-productivity firms pay almost one-third more than median-productivity firms to workers in the same occupation, such as press operators, not including more generous benefits.

These higher wages and higher productivity are associated with continuous-improvement practices inside the plant, such as preventive maintenance on equipment and quality circles. Key to sustaining these internal practices is collaborative supply chain governance: These types of firms are more likely to say their key customer is trustworthy, and to participate in the design of the product they produce.76 Public policies to promote high-road strategies include training for workers in problem-solving and other skills and technical assistance for managers to re-organize production to take advantage of the new skills.77

Discourage low-road production strategies

Even in these collaborative scenarios, however, wages are often less than in the old vertically integrated model. Members of the United Automobile Workers union employed in stamping plants owned by the Big Three Detroit automakers typically earned more than even the stamping plant workers in the 90th percentile plants mentioned in the collaborative supply chain example above. Outsourced supply chains are not the only cause of this decline in bargaining power. The corrosion of labor union power and the re-organization of workplace relationships enables the increasing prevalence of outsourcing, and the increase in outsourcing in turn has further decreased workers’ bargaining power.

Thus, as important as it is to “pave the high road,” it is also important to “block the low road.”78 The Department of Labor has begun to take advantage of modern supply chains’ emphasis on “just-in-time” delivery, recognizing that reduced inventories make regulators’ threat to shut down suppliers for violation of wage and hour laws a more potent threat.79 New policies could combine such sticks with some carrots. The federal government could offer technical assistance, for example, to help small garment manufacturers move away from the existing low-road model in which ill-trained workers typically do one simple operation to a garment, and then pass it on to the next worker. Instead, they could adopt a more agile production recipe, one that involves more broadly trained and higher-paid workers collaborating in teams—a high-road model sustained by greater productivity and reduced lead times.

Government should implement collaborative supply chain practices within its own purchasing, building on the Obama Executive Order that makes it harder for supply chains with recent violations of labor laws to sell to the government. In 2010, the Government Accountability Office found that almost two-thirds of the 50 largest wage-and-hour violations and almost 40 percent of the 50 largest workplace health-and-safety penalties issued between fiscal years 2005 and 2009 went to companies that went on to receive new government contracts.80

More fairly share the benefits and risks of contingent work

Today, lead firms and their suppliers reap the benefit of paying workers only when needed, while the risks of being left without earnings are borne by workers. Several proposals could improve the balance here: encouraging work-sharing in downturns (which would make hiring regular workers less costly), continuing to improve the portability of benefits across firms, and promoting schedule stability.81

Conclusion: Retooling supply chains for equitable growth

Over the past several decades, U.S. firms have outsourced their supply chains in a way designed to protect their short-term profits, rather than to build knowledge through collaborative supply chains. The rise of such supply chains, including the increased use of contingent workers, threatens U.S. economic competitiveness by undermining innovation, and erodes U.S. workers’ economic security. The rise over the past few decades of supply chains with small, weak firms leads to an increased presence of firms that innovate less and pay less.

It is unlikely and undesirable that the United States would return to the often bureaucratic and stifling vertically integrated supply chains of the mid-20th century. We can do better. This paper outlined government and corporate policies to promote both more innovation and better job quality in supply chains. In particular, more collaborative supply chains and better-supported local eco-systems could significantly improve both the rate of innovation and the viability of “good jobs strategies.”

References

altenergystocks.com, “Supply Chain: The Race to Meet Demand,” wind directions, January/February 2007, p. 28. http://www.altenergystocks.com/assets/Wind%20Directions.pdf

End Notes

1. Rashmi Banga, “Measuring Value in Global Value Chains,” Working Paper, (New Dehli: Centre for WTO Studies, May 2013), http://wtocentre.iift.ac.in/workingpaper/ Measuring%20Value%20in%20Global%20Value%20Chains%20CWS%20WP%20Final.pdf.

2. Alfred Chandler, The Visible Hand, (Cambridge: Harvard University Press, 1978).

3. Executive Office of the President and the U.S. Department of Commerce, “Supply Chain Innovation: Strengthening America’s Small Manufacturers,” (Washington, D.C., March 2015). https://www.whitehouse.gov/sites/default/files/docs/supply_chain_innovation_report.pdf.

4. Chandler, The Visible Hand

5. These relationships are typically referred to as supply chains, production networks, or global value chains, or GVCs. Timothy Sturgeon defines value chains and supply chains as necessarily vertical processes, reserving the term production network to describe processes that are both vertical and horizontal. See Timothy J. Sturgeon, “How Do We Define Value Chains and Production Networks?” Massachusetts Institute of Technology and Bellagio Value Chains Workshop (Cambridge, MA: Massachusetts Institute of Technology) , October 2000. https://www.ids.ac.uk/ids/global/pdfs/vcdefine.pdf.

6. Marcel P. Timmer, Abdul Azeez Erumban, Bart Los, Robert Stehrer, Gaaitzen J. de Vries, “Slicing Up Global Value Chains,” Journal of Economic Perspectives 28, No. 2 (2014), https://www.aeaweb.org/articles?id=10.1257/jep.28.2.99. See also Richard Baldwin and Javier Lopez-Gonzalez, “Supply Chain Trade: A Portrait of Global Patterns and Several Testable Hypotheses,” NBER Working Paper No. 18957, April 2013, http://www.nber.org/papers/w18957

7.

Annette Bernhardt, Rosemary Batt, Susan Houseman, and Eileen Appelbaum, “Domestic Outsourcing in the U.S.: A Research Agenda to Assess Trends and Effects on Job Quality,” IRLE Working Paper No. 102-16, (Berkeley: Industrial for Research on Labor and Employment, February 2016), http://irle.berkeley.edu/workingpapers/102-16.pdf.

8.

James Fetzer and Erich H. Strassner, “Identifying Heterogeneity in the Production Components of Globally Engaged Business Enterprises in the United States,” Bureau of Economic Analysis, (Washington, DC: U.S. Department of Commerce, 2015), https://bea.gov/about/pdf/acm/2015/november/identifying-heterogeneity-fetzer-strassner.pdf.

9. Ryan Noonan, “Supply Chains Take on Larger Role in Manufacturing,” Economics & Statistics Administration, (Washington, DC: U.S. Department of Commerce, August 2015), http://www.esa.doc.gov/economic-briefings/supply-chains-take-larger-role-manufacturing.

10. Susan Helper and Rebecca Henderson, “Management Practices, Relational Contracts, and the Decline of General Motors.” Journal of Economic Perspectives 28, no.1 (2014): 49-72, https://www.aeaweb.org/articles?id=10.1257/jep.28.1.49.

11. Jason Dedrick, Kenneth L. Kraemer, and Greg Linden, “Who Profits from Innovation in Global Value Chains? A Study of the iPod and notebook PCs,” (Irvine, CA: Alfred P. Sloan Foundation Industry Studies Annual Conference, 2008), http://web.mit.edu/is08/pdf/Dedrick_Kraemer_Linden.pdf.

12. Thomas. L. Friedman, The World Is Flat: A Brief History of the Twenty-first Century, (New York: Farrar, Straus and Giroux, 2005).

13. Clair Brown, Timothy Sturgeon, and Connor Cole, “The 2010 National Organizations Survey: Examining the Relationships Between Job Quality and the Domestic and International Sourcing of Business Functions by United States Organizations,” IRLE Working Paper No. 156-13, (Berkeley, CA: Institute for Research on Labor and Employment, 2013), http://escholarship.org/uc/item/1sp77818.

14. James Fetzer, and Erich H. Strassner. “Identifying Heterogeneity in the Production Components of Globally Engaged Business Enterprises in the United States.” Bureau of Economic Analysis, (Washington, DC: U.S. Department of Commerce, Washington, DC, 2015), https://bea.gov/about/pdf/acm/2015/november/identifying-heterogeneity-fetzer-strassner.pdf.

15. Jessica R. Nicholson and Ryan Noonan, “What is Made in America?” Economics and Statistics Administration, (Washington, DC: U.S. Department of Commerce, 2014). http://www.esa.doc.gov/sites/default/files/whatismadeinamerica_0.pdf.

16. Nicholson and Noonan, “What is Made in America?”.

17. Timmer et. al, “Slicing Up Global Value Chains.”

18. altenergystocks.com, “Supply Chain: The Race to Meet Demand,” Wind Directions, January/February 2007, p. 28. http://www.altenergystocks.com/assets/Wind%20Directions.pdf.

19. Chrysler is now part of Fiat Chrysler Automobiles NV.

20. Alan R. Mulally, Testimony before the Senate Banking Committee, (Washington, DC: Senate Banking Committee, November 18, 2008), http://www.banking.senate.gov/public/_cache/files/dc9ae2d6-85df-4620-8f82-13926da9e3fb/33A699FF535D59925B69836A6E068FD0.mulallytestimony.pdf. Another issue was that many auto suppliers were barely scraping by even before the recession, due to the extractive focus of many of their customers’ purchasing strategies, as discussed below.

21. David Weil, The Fissured Workplace, (Cambridge, MA: Harvard University Press, 2014).

22. Gary Gereffi, John Humphrey and Timothy Sturgeon, “The governance of global value chains,” Review of International Political Economy 12, no. 1 (2005): 78–104, http://www.fao.org/fileadmin/user_upload/fisheries/docs/GVC_Governance.pdf. See also Susan Helper and Timothy Krueger, “Promoting win/win development of global value chains,” prepared for EWC-NSF Workshop on Mega-Regionalism: New Challenges for Trade and Innovation, (Honolulu, HI: East West Center, 2015), http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2745483.

23. Neil Coe and Henry Yeung, “Toward a Dynamic Theory of Global Production Networks,” Economic Geography 9, no. 1( 2015): 29-58, http://www.readcube.com/articles/10.1111/ecge.12063.

24. In more general (and academic) language, industry characteristics (such as information complexity) and the nature of supplier/customer governance are jointly determined. See Susan Helper and David I. Levine, “Long-Term Supplier Relations and Product-Market Structure,” Journal of Law, Economics, & Organization 8, No. 3 (1992): 561-581, https://www.researchgate.net/profile/David_Levine6/publication/5214362_Long-Term_Supplier_Relations_and_Product-Market_Structure/links/0912f5106eeeba3036000000.pdf?inViewer=0&pdfJsDownload=0&origin=publication_detail.

25. Helper and Levine, “Long-Term Supplier Relations and Product-Market Structure.”

26. Gary P. Pisano and Willy C. Shih, “Restoring American Competitiveness,” Harvard Business Review, 2009. https://hbr.org/2009/07/restoring-american-competitiveness/ar/1. See also Suzanne Berger, Making in America: From Innovation to Market, (Cambridge, MA: MIT Press, 2013).

27. Toshihiro Nishiguchi, Strategic Industrial Sourcing: The Japanese Advantage, (Oxford University Press, 1994). See also Michael Smitka, Competitive Ties: Subcontracting in the Japanese Automotive Industry, (New York: Columbia University Press, 1991). Problems in maintaining these deep levels of knowledge flow as the company has grown, with new suppliers in dozens of countries, help account for many of Toyota’s recent quality troubles. See John MacDuffie and Takahiro Fujimoto, “Why Dinosaurs Will Keep Ruling the Auto Industry,” Harvard Business Review, 2010. https://hbr.org/2010/06/why-dinosaurs-will-keep-ruling-the-auto-industry.

28. Gerry Susman, “Selecting and Evaluating Environmentally Responsible Suppliers of Hazardous, Nonhazardous Special Waste and Product-End-Of-Life Management Services.” Prepared for The Second Smeal Sustainability Case Competition, (State College, PA: Pennsylvinia State University, 2015), http://www.smeal.psu.edu/sustainability/documents/ibm-case-pdf.

29. Susan Helper with Kyoung Won Park, Jennifer Kuan, Timothy Krueger, Alex Warofka, Joy Zhu, William Eisenmenger, and Brian Peshek, “The U.S. Auto Supply Chain at a Crossroads: Implications of an Industry in Transformation,” (Washington, DC: U.S. Department of Labor, 2011), http://drivingworkforcechange.org/reports/supplychain.pdf.

30. Susan Helper and Rebecca Henderson, “Management Practices, Relational Contracts, and the Decline of General Motors,” Journal of Economic Perspectives 28, no. 1 (2014): 49-72, https://www.aeaweb.org/articles?id=10.1257/jep.28.1.49.

31. Executive Office of the President and the U.S. Department of Commerce, “Supply Chain Innovation: Strengthening America’s Small Manufacturers.”

32. In contrast, much of the literature in this area focuses narrowly on the prevalence of outsourcing, and does not examine how supply chance governance may shape the consequences of outsourcing when it occurs.

33. Vasco M. Carvalho, “From Micro to Macro via Production Networks,” Journal of Economic Perspectives 28, no. 4 (2014): 23-48, https://www.repository.cam.ac.uk/bitstream/handle/1810/246199/ Carvalho%202014%20Journal%20of%20Economic%20Perspectives.pdf?sequence=3.

34. Microcontrollors are used for engine monitoring and control, transmission control, airbag and other safety device control, in-vehicle networking, and infotainment connectivity.

35. Bill Canis, “The Motor Vehicle Supply Chain: Effects of the Japanese Earthquake and Tsunami,” (Washington, DC: Congressional Research Service, 2011), https://www.fas.org/sgp/crs/misc/R41831.pdf.

36.

Erica Groshen, “Sources of Intra-Industry Wage Dispersion: How Much Do Employers Matter?” The Quarterly Journal of Economics 106, no. 3 (1991): 869-884,

https://www.jstor.org/stable/2937931?seq=1#page_scan_tab_contents.

37. Executive Office of the President and the U.S. Department of Commerce, “Supply Chain Innovation: Strengthening America’s Small Manufacturers.”

38. Ibid.

39. Susan Helper, Kyoung Won Park, Jennifer Kuan, Timothy Krueger, Alex Warofka, Joy Zhu, William Eisenmenger, and Brian Peshek, “The U.S. Auto Supply Chain at a Crossroads: Implications of an Industry in Transformation,” (Washington, DC: U.S. Department of Labor, 2011), http://drivingworkforcechange.org/reports/supplychain.pdf.

40. Jenny Kuan and Susan Helper, “What Goes on Under the Hood? How Engineers Innovate in the Automotive Supply Chain,” NBER Working Paper No. 22552, (Cambridge, MA: August 2016), http://www.nber.org/papers/w22552.

41. For more detailed discussion on this challenge, please see Susan Helper, Timothy Krueger, and Howard Wial, “Why Does Manufacturing Matter? Which Manufacturing Matters?” (Washington, DC: Brookings Institution, 2012), http://www.brookings.edu/research/papers/2012/02/22-manufacturing-helper-krueger-wial

42. Kuan and Helper, “What Goes on Under the Hood? How Engineers Innovate in the Automotive Supply Chain.”

43. Maria Wood, “No Longer Just a ‘Temp’: The Rise of the Contingent Worker.” SkilledUp, March 2015, http://www.skilledup.com/insights/longer-just-temp-rise-contingent-worker

44. Robert Wood, “FedEx Settles Independent Contractor Mislabeling Case for $228 Million,” Forbes, June 16, 2015, http://www.forbes.com/sites/robertwood/2015/06/16/fedex-settles-driver-mislabeling-case-for-228-million/#6da0bdd15f5a

45. Bernhardt, Annette, Rosemary Batt, Susan Houseman, and Eileen Appelbaum. “Domestic Outsourcing in the U.S.: A Research Agenda to Assess Trends and Effects on Job Quality”. IRLE Working Paper No. 102-16, February 2016. http://irle.berkeley.edu/workingpapers/102-16.pdf

46. Dube, Arindrajit and Ethan Kaplan. “Does Outsourcing Reduce Wages in the Low-Wage Service Occupations? Evidence from Janitors and Guards.” Industrial and Labor Relations Review, Vol. 63, No. 2, 287-306, 2010. http://www.irle.berkeley.edu/workingpapers/171-08.pdf.

47. Deborah Goldschmidt and Johannes Schmieder, “The Rise of Domestic Outsourcing and the Evolution of the German Wage Structure,” (Kalamazoo, MI: Upjohn Institute for Employment Research, 2015), http://research.upjohn.org/cgi/viewcontent.cgi?article=1262&context=up_workingpapers. Note that in some cases, firms outsource high-wage occupations, such as lawyers and consultants. Little research has been done on the effect of unbundling on the quality of these jobs.

48. U.S. Government Accountability Office, “Contingent Workforce: Size, Characteristics, Earnings, and Benefits,” GAO-15-168R, (Washington, DC: Government Accountability Office, Apr 20, 2015), http://www.gao.gov/assets/670/669766.pdf.

49. Gerald Davis and J. Adam Cobb, “Corporations and Economic Inequality around the World: The Paradox of Hierarchy,” Research in Organizational Behavior, No. 30 (2010): 35-53, http://webuser.bus.umich.edu/gfdavis/Papers/Davis_Cobb_3-31.pdf.

50. Erica Groshen, Discussion of “Understanding declining fluidity in the U.S. labor market,” (Washington, DC: Brookings Papers on Economic Activity), March 3, 2016, http://www.brookings.edu/about/projects/bpea/papers/2016/molloy-et-al-declining-fluidity.

51. Erling Barth, Alex Bryson, James C. Davis, and Richard Freeman, “It’s Where You Work: Increases in Earnings Dispersion across Establishments and Individuals in the U.S.” NBER Working Paper No. 20447, (Cambridge, MA: National Bureau of Economic Research, 2014). http://ftp.iza.org/dp8437.pdf; Elizabeth W. Handwerker and James R. Spletzer, “The Role of Establishments and the Concentration of Occupations in Wage Inequality,” IZA Discussion Paper No. 9294, (Bonn, Germany: German Institute for the Study of Labor, 2015), http://ftp.iza.org/dp9294.pdf; Jae Song, David J. Price, Fatih Guvenen, Nicholas Bloom, and Till von Wachter, “Firming Up Inequality,” NBER Working Paper No. 21199, (Cambridge, MA: National Bureau of Economic Analysis), http://www.nber.org/papers/w21199.

52. William E. Evan and David A. Macpherson, “Is Bigger Still Better? The Decline of the Wage Premiums at Large Firms,” Southern Economic Journal 78, no. 4 (2012): 1181-1201.

53. Charles Brown, “Firms’ Choice of Method of Pay,” Industrial Labor Relations Review 43, no.3 (1990): 165S-182S; Brown Charles and James Medoff, “The Employer Size-Wage Effect,” The Journal of Political Economy 97, no. 5 (1989): 1027-1059.

54. In this case, there would still be an association among outsourcing, occupational segregation and inequality; however, the wages of the outsourced workers would rise (in contrast to the case of low-wage occupations like janitors discussed above).

55. William Lazonick, Sustainable Prosperity in the New Economy? Business Organization and High-Tech Employment in the United States, (Kalamazoo, MI: Upjohn Institute for Employment, 2009); Susan Helper and Mari Sako, “Management innovation in supply chain: appreciating Chandler in the twenty-first century,” Industrial and Corporate Change 19, no. 2 (2010): 399-429, http://icc.oxfordjournals.org/content/19/2/399.short; Eileen Appelbaum, Rosemary Batt, Annette Bernhardt, Susan Houseman, “Domestic Outsourcing in the U.S.: A Research Agenda to Assess Trends and Effects on Job Quality,” Prepared for The Future of Work Symposium, (Washington, DC: U.S. Department of Labor, 2015), http://cepr.net/images/stories/reports/working-paper-domestic-outsourcing-2016-03.pdf; Annette Bernhardt, Rosemary Batt, Susan Houseman, and Eileen Appelbaum, “Domestic Outsourcing in the U.S.: A Research Agenda to Assess Trends and Effects on Job Quality,” Working Paper No. 102-16, (Berkeley. CA: Institute for Research on Labor and Employment, 2016), http://irle.berkeley.edu/workingpapers/102-16.pdf.

56. The Economist, “Too much of a good thing,” March 26, 2016, http://www.economist.com/news/briefing/21695385-profits-are-too-high-america-needs-giant-dose-competition-too-much-good-thing.

57. Note that this explanation does not rely on the rise of the internet. “Whilst we agree that ICT speeds up communication and reduces monitoring costs, these advantages may be exploited within firms as much as between firms. Thus, what tips the scale from vertical integration to disintegration is not ICT per se, but the use of ICT to pursue the changed managerial goals derived from deregulation.” See Helper and Sako, “Management innovation in supply chain: appreciating Chandler in the twenty-first century.”

58. Chris Brooks, “Interview, Part 2: Labor’s New Sources of Leverage,” Labor Notes, August 12, 2016, http://www.labornotes.org/MoodyInterview.

59. Harris Freeman and George Gonos, “Temp Organizing Gets Big Boost from NLRB,” Labor Notes, August 23, 2016, http://www.labornotes.org/2016/08/temp-organizing-gets-big-boost-nlrb.

60. Josh Whitford, The New Old Economy: Networks, Institutions, and the Organizational Transformation of American Manufacturing. (Oxford, United Kingdom: Oxford University Press, 2006), Susan Helper and Janet Kiehl, “Developing supplier capabilities: Market and non-market approaches.” Industry and Innovation 11, no. 1-2 (2004): 89-107.

61. Whitford, The New Old Economy: Networks, Institutions, and the Organizational Transformation of American Manufacturing; Susan Helper and Rebecca Henderson, “Management Practices, Relational Contracts, and the Decline of General Motors,” Journal of Economic Perspectives 28, No. 1 (2014): 49-72.

62. A medium amount of market power can however promote efficient collaboration in supply chains; if the lead firm has no economic profits, it may be unable to make commitments that promote long-term, mutually profitable relationships. Helper and Levine, “Long-Term Supplier Relations and Product-Market Structure.”

63. David Weil, The Fissured Workplace.

64. Andrew Schrank and Josh Whitford, “The Anatomy of Network Failure,” Sociological Theory, 29, no. 3(2011): 151-177, http://www.columbia.edu/~jw2212/Writing/Main/02-ANF-ST.pdf.

65. Brock Yates, The Decline and Fall of the American Automobile Industry, (New York: Empire Books, 1983); Gerno Grabher, On the weakness of strong ties: The ambivalent role of inter-firm relations in the decline and reorganization of the Ruhr, (Berlin: Wissenschaftszentrum Berlin für Sozialforschung, 1990).

66. Fred Block, Matthew Keller, Andrew Schrank, and Josh Whitford, “A Strategy to Foster Advanced Manufacturing Networks in the United States,” Scholars Strategy Network Working Paper, (2012), http://www.scholarsstrategynetwork.org/sites/default/ files/ssn_strategy_brief_block_keller_schrank_whitford_on_advanced_manufacturing.pdf.

67. Ibid.

68. Susan Helper, Timothy Krueger, and Howard Wial, “Why Does Manufacturing Matter? Which Manufacturing Matters?,” (Washington, DC: Brookings Institution, 2012), http://www.brookings.edu/research/papers/2012/02/22-manufacturing-helper-krueger-wial; Suzanne Berger, How We Compete: What Companies Around the World Are Doing to Make it in Today’s Global Economy, (New York: Currency, 2005).

69. Executive Office of the President and the U.S. Department of Commerce, “Supply Chain Innovation: Strengthening America’s Small Manufacturers.”

70. In contrast, Taylorist theories of management hold that “brain work” (such as process design) and “hand work” (such as production) should be done by different people, with little payoff to feedback between the groups (Helper and Henderson, 2014); Paul S. Adler and Bryan Borys, “Two types of bureaucracy: Enabling and coercive,” Administrative Science Quarterly, 41, no. 1 (1996): 61-89.

71. U.S. Department of Commerce, “Assess Costs Everywhere”. Tool for assessing sourcing costs. http://acetool.commerce.gov

72. Berger, Making in America: From Innovation to Market. See also Robert D. Ezell and Stephen J. Atkinson, “International Benchmarking of Countries’ Policies and Programs Supporting SME Manufacturers,” (Washington, DC: The Information Technology & Innovation Foundation, September 2011), http://www.itif.org/files/2011-sme-manufacturing-tech-programs.pdf, and Helper et al., “Why Does Manufacturing Matter? Which Manufacturing Matters?”.