…For one thing, some of the opposition to the TPP comes from people who support free trade, and who worry that the treaty’s intellectual property provisions amount to a restriction of trade. As Krugman points out, Mankiw ignores this. Mankiw’s second problem is that this same old case has failed again and again to persuade the general public. Yes, economists overwhelmingly favor the idea of free trade. But the public remains stubbornly skeptical. Is this because they are just not smart enough to get the Econ-101-David-Ricardo thing even after hearing it a hundred times? Or is it because people are irrational and biased?

In his article, Mankiw lists three biases that he blames for people’s refusal to accept the free-trade argument. These are ‘anti-foreign bias,’ ‘anti-market bias,’ and ‘make-work bias.’ Essentially, Mankiw is telling you that you don’t believe the simple truth because deep down within you lurks a xenophobic socialist. Call me crazy, but I don’t think this is a beneficial, constructive way for economists to engage with the public. Maybe the public is neither xenophobic nor socialist. Maybe people are perfectly smart and rational enough to understand the David Ricardo idea, and also smart enough to understand something else that economists have known for 200 years — international trade doesn’t necessarily benefit everyone within a country. That’s right — trade creates winners and losers. Econ 101 says that the winners outnumber the losers in dollar terms, but not necessarily in people terms — if the richest 1 percent of Americans gain $1 billion from a trade agreement and the other 99 percent lose $900 million, then Ricardo’s theory says the country benefited overall. That outcome is perfectly consistent with Econ 101.

Most pro-free-trade economists, if you confront them with this fact, will say that this problem can be solved if we use redistributive taxes to compensate the losers. This ignores that we often don’t know who the winners and losers are from any particular trade deal — this is why you can’t buy insurance against the possibility of losing your job to a trade agreement. This also ignores that the tax system wasn’t set up to carry out this compensation. And on top of that, many pro-free-trade economists, Mankiw included, are almost always opposed to tax increases. In other words, Mankiw is giving the public a pro-trade argument that, even on its own merits, might be bogus. Econ 101 says that it’s possible that free trade might hurt the majority of Americans, and yet Mankiw doesn’t seem to think the public needs to hear that fact.

Like I said, I am in favor of the TPP. And, like most economists, I think free trade has, on balance, been a big net positive for most Americans over the past century, relative to any alternative we might have pursued. But I think the American people are intelligent and grown-up enough to hear the basic case against free trade, as well as the case in favor. Yes, Mankiw is smarter than most of us. That doesn’t mean we’re dummies.

Things to Read at Nighttime on May 3, 2015

Must- and Should-Reads:

- : When science fiction authors are no longer grounded in reality

- (2012): How an Astounding New Right-Wing Lie About the Economy Was Born

- : Wonks Abandon an Economic Dream

- : The Economics of Ferguson: Emerson Electric, Municipal Fines, Discriminatory Policing

Might Like to Be Aware of:

- : “I recall hearing… that sometime after Ethan of Athos, Jim Baen told Lois she could write anything she wanted EXCEPT a sequel to ‘San Francisco Planet’…”

- : “By the midpoint of the year, I was a staggering, raging wreck, filled with madness and raw cunning. I was a complete convert to the Law of the Jungle. Jim Baen had showed me that only ruthless sociopaths could expect to prosper in the world…”

- : One Week with the Apple Watch

Things to Read at Nighttime on May 1, 2015

Must- and Should-Reads:

- : “Pennsylvania Gov. Tom Wolf (D) on Friday outlined a contingency plan for his state in case the Supreme Court guts ObamaCare. Wolf’s plan calls for Pennsylvania to set up its own insurance marketplace if the court rules against the Obama administration in the case King v. Burwell. The case could revoke subsidies that help 7.5 million people afford healthcare coverage…”

- (D-MO): “I don’t think that coming after working people is how you build an economy”

- : Elizabeth Warren is Not Impressed with Your Diamond-Encrusted Ring

- Today’s Must-Must-Read: : There Is a Name for This

- : Altruistic punishment in humans

- : What Detroit can teach us all

- Must-Read: : This Is Not A Trade Agreement

- : “This morning the markets are shocked thanks to a year-over-year gain in US salaries and wages of 2.6%. The ten-year Treasury yield is now up almost 10% over the last four days….”

- : Is Cosmopolitan Communitarianism still Possible? Was it ever?

- Must-Read: : The role of consumption in economic inequality

- Must-Read: : Money, Banking and Financial Markets:

- : Kansas shows us what could happen if Republicans win in 2016 – The Washington Post

At Equitable Growth—The Equitablog

- Needed: New Economic Frameworks for a Disappointing New Normal

- Over at Project Syndicate: An Even More Dismal Science

- Let Me Strongly Agree with Ben Bernanke on the Wall Street Journal Editorial Page: It Is and Has Long Been a Clown Show

- Let Me Strongly Dissent from Ben Bernanke’s Claim That the Critical Objective of Recovery Viewed in the Proper Metrics Is Being Met

- : What does weak U.S. economic growth in first quarter mean for the current recovery?

- : The merits and limits of “college for the masses”

- : Weekend reading

Might Like to Be Aware of:

- (2006): After Neoconservatism

- : “I was curious as Apple products have been more than just up market gadgets to me… my access to the many things… those of us with deafblindness particularly struggle with…. I am severely deaf and have only a very small tunnel of vision in my right eye…. I decided to order the Apple Watch Sport 42mm (the bigger face size) with white strap so I’d not lose it quite so easily…. The default settings I have on my iPhone are set to large text and I was pleased to be able to have this on my Apple Watch. I also use Zoom large text set to the largest. The new setting ‘Prominent Haptic’ is perhaps my favourite in accessibility… definitely awesome for me as a deafblind person. So far for me the most useful App on the Apple Watch is Maps–on my iPhone I can plan my journey from one destination to another, for me it will be on foot with Unis my guidedog. This is where Haptics really come into its own–I can be directed without hearing or sight, but by a series of taps via the watch…. I am now very happy to own an Apple Watch and look forward to making it work well for me.”

- : Civicist

Needed: New Economic Frameworks for a Disappointing New Normal

When I was taught economics lo more than a generation ago now, I was taught that there were six major and significant political-economic market and governance failures that called for action:

- failures of the distribution of income to accord with utility and desert, which called for social insurance–and we had about the right amount of that.

- failures of the market in the area of public goods, which called for government spending on physical, organizational, and social infrastructure–and we had about the right amount of that.

- failures of the demand for money to remain stable over time, which called for aggressive monetary policy to stabilize the path of total spending around its trend–and we needed to better at that.

- failures of voters to understand that low interest rate policies were ultimately counterproductive and created costly inflation, which called for independent and conservative hard-money technocratic central banks.

- voter myopia about spending and taxes, which called for pressure and institutions to make the public sphere of discussion fear deficits–and we were moving toward that.

- failures of the financial markets to actually mobilize society’s risk-bearing capacity and so make the hurdle rate for corporate investment as low as it should be, which we could do little about save trying to open up finance and teach people the benefits of diversification–and, I was taught, the equity return premium was on the decline, and would be the time I was middle-aged no longer be a first-order economic failure.

All this was in the context of the age of Social Democracy–in which we could expect fast productivity growth, a relatively egalitarian income distribution, and in which the principal socio-economic problems were those of moving toward socioeconomic inclusion for more than just well-educated white guys and keeping populist policy mistakes from disrupting the mechanism via monetary inflation or excessive government debt burdens.

This entire structure is now in ruins. Our social-democratic income distribution has been upending in an appalling manner by the Second Gilded Age. Our government, here in the U.S. at least, has been starved of proper funding for infrastructure of all kinds since the election of Ronald Reagan. Our confidence in our institutions’ ability to manage aggregate demand properly is in shreds–and for the good reason of demonstrated incompetence and large-scale failure. Our political system now has a bias toward austerity and idle potential workers rather than toward expansion and inflation. Our political system now has a bias away from desirable borrow-and-invest. And the equity return premium is back to immediate post-Great Depression levels–and we also have an enormous and costly hypertrophy of the financial sector that is, as best as we can tell, delivering no social value in exchange for its extra size.

We badly need a new framework for thinking about policy-relevant macroeconomics given that our new normal is as different from the late-1970s as that era’s normal was different from the 1920s, and as that era’s normal was different from the 1870s.

But I do not have one to offer.

Olivier Blanchard has thoughts:

…I had implicitly assumed that this new normal would be very much like the old normal, one of decent growth and positive equilibrium interest rates. The assumption was challenged…. Ken Rogoff argued that what we were in the adjustment phase of the ‘debt supercycle’…. Larry Summers argued… more was going on… a chronic excess of saving over investment [with] keeping the economy at potential may well require very low or even negative real interest rates…. I am closer to Summers… than to Rogoff. What the new normal will be matters a lot for policy design….

[Has] financial regulation… successfully reduced financial risk. There was agreement on ‘reduced,’ not so on ‘successfully.’… The discussion became granular…. Should monetary policy go back to its old ways?… Ben Bernanke’s answer was largely yes. Once economies were out of the zero lower bound, most of the programs introduced during the crisis should be put back on the shelf, ready to be used only if there was another sufficiently adverse shock…. Issue was taken on by others, in particular Ricardo Caballero…. If the central banks are in a unique position to be able to supply safe assets shouldn’t they do it? I see this discussion as having just started, raising deep issues about the private demand for safe assets, and the potential role of central bank in this context….

Judging the central bank on how it fulfills its mandate, rather than requiring it to follow a simple rule, [Bernanke] argued, is the way to proceed. I agree…. Tucker however argued for the use of macro prudential tools to deal with ‘exuberance,’ not necessarily for fine tuning in more normal times. Rubin remarked that we were not very good at telling when times were exuberant…. Lars Svensson argued that a simple cost-benefit analysis suggests that monetary policy is a very poor instrument to deal with financial risk….

The traditional objection to using fiscal policy as a macroeconomic policy tool was that recessions did not last long, and by the time discretionary fiscal measures were implemented, it was typically too late. Martin Feldstein made the point that some recessions, in particular those associated with financial crises, are long enough that discretionary policy can and should be used…. Despite questions by the chair of the session, Vitor Gaspar, on potential improvements in the design of automatic stabilizers (based on the very interesting chapter 2 of the April 2015 Fiscal Monitor), the issue did not register, and I am still struck by the lack of action on this front….What struck me most in the discussion of capital flows was the recognition that they have complex effects…. This… has one clear implication, namely that hands-off policies are not the solution. I see this as one area where the rethinking has been striking, say compared to ten years ago…. There was no agreement on capital controls…. Ricardo Caballero touched upon the demand for safe assets by emerging market countries, and argued for a better provision of international liquidity by the IMF and by central banks….

Not all the questions I had raised in my pre-conference blog were taken up, and few were settled. Still, to go back to the title of the conference, Rethinking Macro Policy III: Progress or Confusion?, my answer is definitely: Both. Progress is undeniable. Confusion is unavoidable…

Must-Read: Micah Sifry: Civicist

Over at Grasping Reality: Live from Crow’s Coffee: 435 Magazine

Live from Crow’s Coffee: 435 Magazine. I was reading 435 Magazine (offices at 11775 W. 112th Street, Suite 200, Overland Park, KS 66210, ten miles away from here) on the airplane on my way back from California to Kansas City. I found myself getting scared.

The scary thing is that Los Angeles is not that very much larger then Kansas City. And yet it has about nine times the population. READ MOAR

Today’s Must-Must-Read: Steve Randy Waldman: The Baltimore Riots as Altruistic Punishment

…Look it up. Altruistic punishment is a ‘puzzle’ to the sort of economist who thinks of homo economicus maximizing her utility, and a no-brainer to the [evolutionary] game theorist who understands humans could never have survived if we actually were the kind of creature who succumbed to every prisoners’ dilemma. Altruistic punishment is behavior that imposes costs on third parties with no benefit to the punisher, often even at great cost to the punisher. To the idiot economist, it is a lose/lose situation, such a puzzle. For the record, I’m a fan of the phenomenon. Does that mean I’m a fan of these riots, that I condone the burning of my own hometown? Fuck you and your tendentious entrapment games and Manichean choices, your my-team ‘ridiculing’ of people you can claim support destruction. Altruistic punishment is essential to human affairs but it is hard. It is mixed, it is complicated, it is shades of gray…

…Unlike other creatures, people frequently cooperate with genetically unrelated strangers, often in large groups, with people they will never meet again, and when reputation gains are small or absent. These patterns of cooperation cannot be explained by the nepotistic motives associated with the evolutionary theory of kin selection and the selfish motives associated with signalling theory or the theory of reciprocal altruism. Here we show experimentally that the altruistic punishment of defectors is a key motive for the explanation of cooperation. Altruistic punishment means that individuals punish, although the punishment is costly for them and yields no material gain. We show that cooperation flourishes if altruistic punishment is possible, and breaks down if it is ruled out. The evidence indicates that negative emotions towards defectors are the proximate mechanism behind altruistic punishment. These results suggest that future study of the evolution of human cooperation should include a strong focus on explaining altruistic punishment.

Nature 415, 137-140 (10 January 2002) | doi:10.1038/415137a; Received 5 October 2001; Accepted 5 November 2001

University of Zürich, Institute for Empirical Research in Economics, Blümlisalpstrasse 10, CH-8006 Zürich, Switzerland. University of St Gallen, FEW-HSG, Varnbüelstrasse 14, CH-9000 St Gallen, Switzerland. Correspondence and requests for materials should be addressed to E.F. (e-mail: efehr@iew.unizh.ch).

Weekend reading

This is a weekly post we publish on Fridays with links to articles we think anyone interested in equitable growth should be reading. We won’t be the first to share these articles, but we hope by taking a look back at the whole week we can put them in context.

Links

Dietz Vollrath points out that our system for categorizing industries and measuring their contribution to economic growth are wildly out of date. [growth economics]

Ryan Decker follows up and adds that the primary way economists think about productivity—total factor productivity—is based on thinking about a world full of manufacturing firms. [updated priors]

Eduardo Porter argues that economic inequality is having severe social consequences in the United States. [nyt]

Jordan Weissman sticks to his prediction from a few years ago: Millennials will be more frugal than previous generations. [slate]

Ufuk Akcigit, Salome Baslandze, and Stefanie Stantcheva write up their research on the effects of top tax rates on superstar inventors in the United States and Europe. [voxeu]

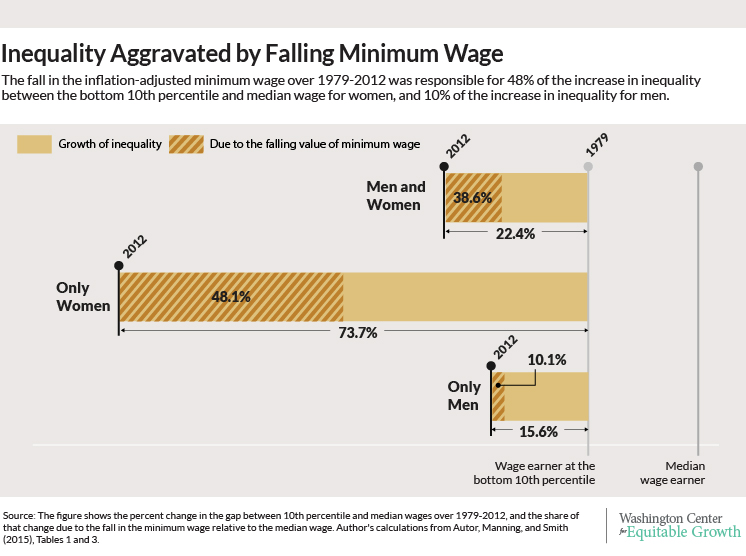

Friday figure

Figure from “How raising the minimum wage ripples through the workforce,” by Ben Zipperer

Over at Project Syndicate: An Even More Dismal Science

Over at Project Syndicate: For the past twenty-five years those of my elders whom I regard as the barons of policy-relevant academic macroeconomics–at least the reality-based and sane barons–have been asking themselves fundamental questions. The first question was whether the business-cycle pattern of the post-World War II generation of full employment, a bias toward moderate inflation, and rapid growth had in fact come to an end. The second question was how best to think about the business cycle after the end of the post-WWII era’s “Thirty Glorious Years.” READ MOAR

First out of gate, in 1991, was Larry Summers, with his “How Should Long-Term Monetary Policy Be Determined?” Summers was not certain that the economic policy régime and economic reality had changed. Thus his first goal was to stengthen the technocratic independence of the central bank. “Institutions should do the work of rules”. And attention should be devoted to “strengthening the[ir] independence”. While politicians should and could set goals, technocrats could carry them out better than politicians micromanaging or politicians prescribing rules that would inevitably fail in unexpected circumstances. That would guard against a repetition of the inflationary disturbances of the 1970s. His second goal, however, was to convince the technocrats he hoped to see running central banks that a 2-3%/year inflation rate should be the goal. He did “not see evidence that [inflation] instability results at [such a] low rate.” He saw “forgo[ing] that opportunity under a zero inflation rate” of achieving the right real interest rate if the “real rate of interest should be negative… at certain times” as very expensive. And the expense was amplified by three considerations: The first was that the presence of money illusion and downward nominal rigidities in labor and debt contracts. The second was that the productivity slowdown made wage growth more likely to bump up against zero. And the third was that the combination of the productivity slowdown and the demographic transition made interest rate more likely to bump up against zero.

Second was Paul Krugman in 1998, with his book The Return of Depression Economics2 and his paper “It’s Baaack: Japan’s Slump and the Return of the Liquidity Trap.3 Krugman argued powerfully that central banks had succeeded in anchored inflation and inflation expectations to a low level. Thus, he believed, the global economy–or at least the North Atlantic economy–had returned to an earlier pattern. The pattern was the pre-World War II pattern of “depression economics”. And in it shortages of aggregate demand, risks of deflation, financial crises, and liquidity traps would become important and perhaps dominant features.

Summers believed that technocratic central banks under loose political reins could guard against both the inflationary dysfunctions of the 1970s and the depression-prone dysfunctions of the pre-WWII era. Krugman believed that hope was vain, and that the régime of depression economics had returned. And at the third point of the triangle was Ken Rogoff. Ever since his 1998 Brookings Institution comment on Paul Krugman he has found himself “not quite buy the view that short- and medium-term full-employment real interest rates… are negative. And even if they are… the right policy is probably to raise the real interest rate through expansionary fiscal policy… free[ing] monetary policy from its supposed liquidity trap.” He has viewed what Krugman sees as a long-term vulnerability to “depression economics” as, rather, the temporary consequences of failures to properly regulate and curb debt accumulation. It is such debt accumulation cycles which cause the problems by inevitably ending in a great deal of underwater loans in and economy. And then they can and must be cured only by painful deleveraging accompanied by heterodox government-enforced debt writedowns.

And the other barons–Joe Stiglitz, Ben Bernanke, Marty Feldstein, and many others–have not so much staked out their own positions as remain in some Schroedingerian superposition. Sometimes they argue as if we still lived in the 1953-1986 world in which central bankers like William McChesney Martin, Arthur Burns, and Paul Volcker operated. Sometimes they sound like Krugman, Summers, or Rogoff.

So what can we say about this debate, which has now been ongoing for twenty-five years?

Most importantly, we can say that the answer to the first question–whether the business-cycle pattern of the first post-World War II generation has come to an end–is: “yes, definitely.” The models and approaches developed to understand the small size of the post-WWII generation’s cycle and its bias toward moderate inflation are worse than useless for today. Second, Summers has more-or-less abandoned his 1991 belief that central banks can and will and perhaps even should interpret “price stability” flexibly enough to keep the return of depression economics away. In his view, with which I concur, more of the risk-bearing and long-term investment-planning and investing role in society needs to be taken over by governments. And we strongly believe that at least those governments with exorbitant privilege that issue the world’s reserve currencies can take on this role without any substantial chance of so-loading future taxpayers with inordinate debt burdens. Rogoff, by contrast, continues to hold to the rather Minskyite position that has underpinned his thinking since at least 1998: that successful macroeconomic performance requires regulating finance and curbing debt accumulation in the boom.

The triangle of positions has thus collapsed to a line. Perhaps central banks could have managed to attain the technocratic utopia of macroeconomic business-cycle management Summers hoped for back in 1991. But they have failed to do. And few if any seem to have good ideas as to what institutional changes could provide them with both the will and the power to a accomplish that mission.

And the line reflects different positions not so much on the situation but on whether macroeconomic management can provide a cure. Summers and Krugman now both believe that more expansionary fiscal policies could accomplish a great deal of good. Rogoff still believes that attempting to cure an overhang of bad underwater private debt via issuing mountains of government debt currently judged safe is too dangerous–for when the private debt was issued it too was regarded as safe.

It is a far cry from the optimism of the Great Moderation era.

Must-Read: Adair Turner; Money, Banking and Financial Markets

…to a very significant extent as having one primary objective – low and stable inflation (with some countries in addition including a broad employment mandate) – and one policy tool, the policy interest rate. I think that this definition involving a very small set of objectives and one policy tool was fundamentally mistaken…