…once the global financial crisis is finally over? Will it resume the pre-crisis consensus, or will it be forced to contend with a post-crisis ‘new normal’? Have we made progress in addressing these issues, or does confusion remain?… Prominent figures—including Ben Bernanke, Lawrence Summers, and Paul Volcker—offer… essays that address topics that range from the measurement of systemic risk to foreign exchange intervention. The chapters address whether we have entered a ‘new normal’ of low growth, negative real rates, and deflationary pressures, with contributors taking opposing views; whether new financial regulation has stemmed systemic risk; the effectiveness of macro prudential tools; monetary policy, the choice of inflation targets, and the responsibilities of central banks; fiscal policy, stimulus, and debt stabilization; the volatility of capital flows; and the international monetary and financial system, including the role of international policy coordination…. Is there progress or confusion?… Both. Many lessons have been learned; but, as the chapters of the book reveal, there is no clear agreement on several key issues.

Must-Read: July 20, 1994: Alan Greenspan reintroduces Knut Wicksell’s 1898 Geldzins und Güterpreise, and so shifts America’s macroeconomic discussion from the quantity of money to the natural (or equilibrium, or neutral) rate of interest.

As I remember it, I then spent my lunchtime seated at my computer in my office on the third floor of the U.S. Treasury, frantically writing up just what Alan Greenspan was talking about. For over in the Capitol, Greenspan had just said:

Pay no attention to Federal Reserve policy forecasts of M2.

Instead, pay attention to our assessments of the relationship of interest rates to an equilibrium interest rate.

In Greenspan’s view:

[the] equilibrium interest rate [is]… the real rate… if maintained, [that] would keep the economy at its production potential…. Rates persisting above that level, history tells us, tend to be associated with slack, disinflation, and economic stagnation–below that level with eventual resource bottlenecks and rising inflation…

And I said: this is Wicksell. Greenspan is announcing that the Fed is no longer asking in a Friedmanite mode “do we have the right quantity of money?”, but rather asking in a Wicksellian mode “do we have the right configuration of interest rates”:

…the FOMC, as required by the Humphrey-Hawkins Act, set ranges for the growth of money and debt for this year and, on a preliminary basis, for 1994…. The FOMC lowered the 1993 ranges for M2 and M3–to 1 to 5 percent and 0 to 4 percent, respectively…. The lowering of the ranges is purely a technical matter, it does not indicate, nor should it be perceived as, a shift of monetary policy in the direction of restraint It is indicative merely of the state of our knowledge about the factors depressing the growth of the aggregates relative to spending….

In reading the longer-run intentions of the FOMC, the specific ranges need to be interpreted cautiously The historical relationships between money and income, and between money and the price level have largely broken down, depriving the aggregates of much of their usefulness as guides to policy. At least for the time being, M2 has been downgraded as a reliable indicator of financial conditions in the economy, and no single variable has yet been identified to take its place. At one time, M2 was useful both to guide Federal Reserve policy and to communicate the thrust of monetary policy to others. Even then, however, a wide range of data was routinely evaluated to assure ourselves that M2 was capturing the important elements in the financial system that would affect the economy…. The so-called “P-star” model, developed in the late 1980s, embodied a long-run relationship between M2 and prices that could anchor policy over extended periods of time But that long-run relationship also seems to have broken down with the persistent rise an M2 velocity.

M2 and P-star may reemerge as reliable indicators of income and prices…. In the meantime, the process of probing a variety of data to ascertain underlying economic and financial conditions has become even more essential to formulating sound monetary policy….

In assessing real rates, the central issue is their relationship to an equilibrium interest rate, specifically the real rate level that, if maintained, would keep the economy at its production potential over time. Rates persisting above that level, history tells us, tend to be associated with slack, disinflation, and economic stagnation–below that level with eventual resource bottlenecks and rising inflation, which ultimately engenders economic contraction. Maintaining the real rate around its equilibrium level should have a stabilizing effect on the economy, directing production toward its long-term potential.

The level of the equilibrium real rate–or more appropriately the equilibrium term structure of real rates–cannot be estimated with a great deal of confidence, though with enough to be useful for monetary policy. Real rates, of course, are not directly observable, but must be inferred from nominal interest rates and estimates of inflation expectations. The most important real rates for private spending decisions almost surely are the longer maturities. Moreover, the equilibrium rate structure responds to the ebb and flow of underlying forces affecting spending. So, for example, in recent years the appropriate real rate structure doubtless has been depressed by the head winds of balance sheet restructuring and fiscal

retrenchment.

Despite the uncertainties about the levels of equilibrium and actual real interest rates, rough judgments about these variables can be made and used in conjunction with other indicators in the monetary policy process. Currently, short-term real rates, most directly affected by the Federal Reserve, are not far from zero; long-term rates, set primarily by the market, are appreciably higher, judging from the steep slope of the yield curve and reasonable suppositions about inflation expectations. This configuration indicates that market participants anticipate that short-term real rates will have to rise as the head winds diminish, if substantial inflationary imbalances are to be avoided

While the guides we have for policy may have changed recently, our goals have not. As I have indicated many times to this Committee, the Federal Reserve seeks to foster maximum sustainable economic growth and rising standards of living. And in that endeavor, the most productive function the central bank can perform is to achieve and maintain price stability…

…historically strange. A few points: (1) David Davidson and Knut Wicksell debated the… concept very early in the twentieth century, in Swedish…. Most people believe Davidson won…. (2) Keynes devoted a great deal of effort to knocking down the natural rate of interest…. There could be multiple natural rates… [or] no rate of interest whatsoever…. (3) In postwar economics, the Keynesians worked to keep natural rates of interest concepts out….

(4) The older natural rate of interest used to truly be about price stability… [not] “two percent inflation a year.”… (5) Milton Friedman warned (pdf) not to assign too much importance to interest rates…. (6) When Sraffa debated Hayek and argued the natural rate of interest was not such a meaningful concept, it seems Sraffa won…. (7) I sometimes read these days that the “natural [real] rate of interest” consistent with full employment is negative. To me that makes no sense in a world with positive economic growth and a positive marginal productivity of capital….

Of course economic theory can change, and if the idea of a natural rate of interest makes a deserved comeback we should not oppose that development per se. But I don’t see that these earlier conceptual objections have been rebutted, rather there is simply now a Kalman filter procedure for coming up with a number…. In any case, this is an interesting case study of how weak or previously rebutted ideas can work their way back into economics. I don’t object to what most of the people working on this right now actually are trying to say. Yet I see the use of the term acquiring a life of its own, and as it is morphing into common usage some appropriately modest claims are taking on an awful lot of baggage from the historical connotations of the term…

In my view, all (7) of these are more than debatable. For example, (7): “[That] the ‘natural [real] rate of interest’ consistent with full employment is negative… makes no sense in a world with positive economic growth and a positive marginal productivity of capital…” misses the wedge–the wedge between the (positive) expected real rate of return from risky investments in capital and the (positive) temporal slope to the expected inverse marginal utility of consumption, on the one hand; and the (negative) equilibrium real low-risk interest rate, on the other hand.

In a world that is all of a global savings-glut world with large actors seeking portfolios that provide them with various kinds of political risk insurance, risk-tolerance gravely impaired by the financial crisis and the resulting deleveraging debt supercycle, moral hazard that makes the remobilization of societal risk-bearing capacity difficult and lengthly, and reduced demographic and technological supports for economic growth, it seems to me highly plausible that this wedge can be large enough to make the low-risk ‘natural [real] rate of interest’ consistent with full employment negative alongside positive economic growth and a positive marginal productivity of capital.

And the bond market agrees with me in email:

And (2): “Keynes devoted a great deal of effort to knocking down the natural rate of interest…” Indeed he did Keynes saw the natural rate of interest as part of a wrong loanable-funds theory of interest rates: that, given the level of spending Y, supply-and-demand for bonds determined the interest rate. Keynes thought that people must reject that wrong theory before they could adopt what he saw as the right, liquidity-preference, theory of interest rates: that, given the level of spending Y and the speculative demand for money S, supply-and-demand for money determined the interest rate.

I think Keynes was wrong. I think Keynes made an analytical mistake.

Hicks (1937) established that Keynes was wrong when he believed that you had to choose. You don’t. Because spending Y is not given but is rather jointly determined with the interest rate, you can do both. Indeed, you have to do both. Liquidity-preference without loanable-funds is just one blade of the scissors: it cannot tell you what the interest rate is. And loanable-funds without liquidity-preference is just the other blade of the scissors: it, too, cannot tell you what the interest rate is. You need both.

More important, however, in thinking about our present concern with the natural (“neutral”) (“equilibrium”) real rate of interest is knowledge of the historical path by which we arrived at our current intellectual situation. Alan Greenspan did it. On July 20, 1994, Alan Greenspan announced that the Federal Reserve was not a “Keynesian” institution, focused on getting the volume of the categories of aggregate demand–C, I, G, NX–right. He announced that the Federal Reserve was not a “Friedmanite” institution, focused on getting the quantity of money right. He announced that the Federal Reserve was now a “Wicksellian” institution, focused on getting the configuration of asset prices right:

…set[s] ranges for the growth of money and debt…. M2 has been downgraded as a reliable indicator…. [The] relationship between M2 and prices that could anchor policy over extended periods of time… [has] broken down…. M2 and P-star may reemerge as reliable indicators of income and prices….

In the meantime… in assessing real rates [of interest], the central issue is their relationship to an equilibrium interest rate, specifically the real rate level that, if maintained, would keep the economy at its production potential over time. Rates persisting above that level, history tells us, tend to be associated with slack, disinflation, and economic stagnation–below that level with eventual resource bottlenecks and rising inflation, which ultimately engenders economic contraction. Maintaining the real rate around its equilibrium level should have a stabilizing effect…. The level of the equilibrium real rate… [can] be estimated… [well] enough to be useful for monetary policy…. While the guides we have for policy may have changed recently, our goals have not…

Greenspan thus shifted the focus of America’s macroeconomic discussion away from the level of spending and the quantity of money to the configuration of asset prices. In some ways this is no big deal: “Keynesian”, “Friedmanite”, and “Wicksellian” frameworks are all perfectly-fine ways to think about macroeconomic policy. They are different–some ideas and some factors are much easier to express and focus on and are much more intuitive in one of the frameworks than in the others. But they are not untranslateable–I have not found any point that you can express in one framework that cannot be more-or-less adequately translated into the others.

The point, after all, is to find a macroeconomic policy that will make Say’s Law, false in theory, true enough in practice for government work. You can start this task by focusing your analysis first on either spending, or liquidity, or the slope of the intertemporal price structure. You will almost surely have to dig deeper into the guts of the economy in order to understand why the current emergent macro properties of the system are what they are. But any one of the languages will do as a place to start. Greenspan in the mid-1990s judged that the Wicksellian language provided the best way to communicate. And, looking back over the past 25 years, I cannot really disagree.

But at the time, back in 1994, the shift to a Wicksellian episteme led to substantial confusion. As I remember it, I spent my lunchtime on July 20, 1994, seated at my computer in my office on the third floor of the U.S. Treasury, frantically writing up just what Alan Greenspan was talking about when he said (1) pay no attention to Federal Reserve policy forecasts of M2; instead, (2) pay attention to our assessments of the relationship of interest rates to an equilibrium interest rate. Greenspan announced that the Fed was no longer asking in a Friedmanite mode “do we have the right quantity of money?”, but rather was asking in a Wicksellian mode “do we have the right configuration of interest rates”. And that still does not seem to me to be a bad place to be.

…Step right up! Be amazed, be enchanted, by the magic GOP unicorn-and-rainbow-producing tax cut machine! It takes a lot of energy to sustain a lie. When enough people do it together, over a sustained period of time, it wears on them. It also produces a certain kind of culture: one cut loose from the norms of fair conduct and trust that any organization requires in order to survive as something more than a daily, no-holds-barred war of all against all. A battle royale. A circus, if you prefer. And the act in the center ring? The Amazing Death Spiral. One performer does something so outrageous that anyone else who wishes to further hold the audience’s attention has to match or top it––even if they know it’s insane…. That’s what poor old John Kasich did. Hear him cry about his:

great concern that we are on the verge, perhaps, of picking someone who cannot do this job. I’ve watched people say that we should dismantle Medicare and Medicaid…. I’ve heard them talking about deporting 10 or 11 [million] people from this country…. I’ve heard about tax schemes that don’t add up.’

And what happened to him? Read the snap poll from Gravis research. Only 3 percent of Republicans thought he won the debate….

David Brooks says not to worry if candidates are lying about their economic plans, they are just exaggerating to make themselves more attractive to conservative voters…. Paul Krugman is, shall we say, unconvinced….

‘What matters is how a candidate signals priorities.’ Yes, and the priority seems to be lying is okay to get what you want. That’s a great trait to have in a president who might fact the decision to send our kids to die in a war he or she wants. Oh wait.”

And let me put the relevant Paul Krugman pieces down here below the fold… or, rather, below the second fold:

Paul Krugman (October 30, 2015): An Unteachable Moment: “It is, as Antonio Fatas notes, almost seven years since the Fed cut rates to zero…

…The era of lowflation-plus-liquidity-trap now rivals in length the 70s era of stagflation, and has been associated with much worse real economic performance. So where, asks Fatas, is the rethinking of economic theory and policy? I asked the same question a couple of years ago…. Some of us anticipated much though not all of what has gone wrong. [But as] Fatas says…

even those who agreed with this reading of the Japanese economy would have never thought that we would see the same thing happening in other advanced economies. Most thought that this was just a unique example of incompetence among Japanese policy makers….

I did write a 1999 book titled The Return of Depression Economics, basically warning that Japan might be a harbinger…. [But even] I never expected policy to be so bad that Japan ends up looking like a role model…. We should have expected… as major a rethink as… in the 70s… [but] we’ve seen almost no rethinking. Economists who wrote that ‘inflation is looming’ in 2009 continued to warn about looming inflation five years later. And that’s the professional economists. As Josh Barro notes, conservatives who imagine themselves intellectuals have increasingly turned to Austrian economics, which explicitly denies that empirical data need to be taken into account….

Back to Fatas: how long will it take before the long stagnation has the kind of intellectual impact that stagflation did… before people stop holding up the 1970s as the ultimate cautionary tale, even… in the midst of a continuing disaster that makes the 70s look mild? I don’t know…. It’s clear that we have to understand this phenomenon in terms of politics and sociology, not logic.

Paul Krugman (October 20, 2015): Rethinking Japan: “The IMF held a small roundtable discussion on Japan yesterday…

…and in preparation for the event I thought it was a good idea to update my discussion of Japan…. I find it useful to approach this subject by asking how I would change what I said in my 1998 paper on the liquidity trap… one of my best papers; and it has held up pretty well…. But… there are two crucial differences between then and now. First, the immediate economic problem is no longer one of boosting a depressed economy, but instead one of weaning the economy off fiscal support. Second, the problem confronting monetary policy is harder than it seemed, because demand weakness looks like an essentially permanent condition.

Back in 1998 Japan was in the midst of its lost decade… good reason to believe that it was operating far below potential output. This is… no longer the case…. Output per working-age adult has grown faster than in the United States since around 2000, and at this point the 25-year growth rates look similar (and Japan has done better than Europe)…. Japan [may be] closer to potential output than we are.

So if Japan isn’t deeply depressed at this point, why is low inflation/deflation a problem?The answer… is largely fiscal. Japan’s relatively healthy output and employment levels depend on continuing fiscal support… large budget deficits, which in a slow-growth economy means an ever-rising debt/GDP ratio. So far this hasn’t caused any problems…. But even those of us who believe that the risks of deficits have been wildly exaggerated would like to see the debt ratio stabilized and brought down at some point. And here’s the thing: under current conditions, with policy rates stuck at zero, Japan has no ability to offset the effects of fiscal retrenchment with monetary expansion.

The big reason to raise inflation, then, is to make it possible to cut real interest rates… allowing monetary policy to take over from fiscal policy…. The fact that real interest rates are in effect being kept too high by insufficient inflation at the zero lower bound also means that debt dynamics for any given budget deficit are worse than they should be…. Raising inflation would both make it possible to do fiscal adjustment and reduce the size of the adjustment needed.

But what would it take to raise inflation? Back in 1998… I envisaged an economy in which the current level of the Wicksellian natural rate of interest was negative, but that rate would return to a normal, positive level…. It was easy to show that this proposition applied only if the money increase was perceived as permanent, so that the liquidity trap became an expectations problem. The approach also suggested that monetary policy would be effective if… the central bank could ‘credibly promise to be irresponsible’…. But what is this future period of Wicksellian normality of which we speak?…

Japan looks like a country in which a negative Wicksellian rate is a more or less permanent condition. If that’s the reality, even a credible promise to be irresponsible might do nothing: if nobody believes that inflation will rise, it won’t. The only way to be at all sure of raising inflation is to accompany a changed monetary regime with a burst of fiscal stimulus…. While the goal of raising inflation is, in large part, to make space for fiscal consolidation, the first part of that strategy needs to involve fiscal expansion. This… is unconventional enough that one despairs of turning the argument into policy (a despair reinforced by yesterday’s meeting…)

How high should Japan set its inflation target?… High enough so that when it does engage in fiscal consolidation it can cut real interest rates far enough to maintain full utilization…. It’s really, really hard to believe that 2 percent inflation would be high enough…. Japan may face a version of the timidity trap. Suppose it convinces the public that it will really achieve 2 percent inflation… engages in fiscal consolidation, the economy slumps, and inflation falls well below 2 percent… the whole project unravels–and the damage to credibility makes it much harder to try again. What Japan needs (and the rest of us may well be following the same path) is really aggressive policy, using fiscal and monetary policy to boost inflation, and setting the target high enough that it’s sustainable. It needs to hit escape velocity. And while Abenomics has been a favorable surprise, it’s far from clear that it’s aggressive enough to get there.

Paul Krugman (March 21, 2014): Timid Analysis: IAn issue I’ve worried about for a long time…

…which I think I’ve been able to formulate a bit better. Here goes: If you look at the extensive theoretical literature on the zero lower bound since my 1998 paper, you find that just about all of it treats liquidity-trap conditions as the result of a temporary shock… [that] leads to a period of very low demand, so low that even zero interest rates aren’t enough to restore full employment. Eventually, however, the shock will end. So the way out is to convince the public that there has been a regime change, that the central bank will maintain expansionary monetary policy even after the economy recovers, so as to generate high demand and some inflation.

But if we’re talking about Japan, when exactly do we imagine that this period of high demand… is going to happen?… What does it take to credibly promise inflation? Well, it has to involve a strong element of self-fulfilling prophecy: people have to believe in higher inflation, which produces an economic boom, which yields the promised inflation. But a necessary (not sufficient) condition for this to work is that the promised inflation be high enough that it will indeed produce an economic boom if people believe the promise will be kept. If it isn’t, then the actual rate of inflation will fall short of the promise even if people believe in the promise–which means that they will stop believing after a while, and the whole effort will fail….

Suppose that the economy really needs a 4 percent inflation target, but the central bank says, ‘That seems kind of radical, so let’s be more cautious and only do 2 percent.’ This sounds prudent–but may actually guarantee failure.

Paul Krugman (March 20, 2014): The Timidity Trap: “In Europe… they’re crowing about Spain’s recovery…

…growth of 1 percent, versus 0.5 percent, in a deeply depressed economy with 55 percent youth unemployment. The fact that this can be considered good news just goes to show how accustomed we’ve grown to terrible economic conditions…. People seem increasingly to be accepting this miserable situation as the new normal…. How did this happen?… I’d argue that an important source of failure was what I’ve taken to calling the timidity trap–the consistent tendency of policy makers who have the right ideas in principle to go for half-measures in practice, and the way this timidity ends up backfiring, politically and even economically….

There are some important differences between the U.S. and European pain caucuses, but both now have truly impressive track records of being always wrong, never in doubt…. In America… a faction both on Wall Street and in Congress… has spent five years and more issuing lurid warnings about runaway inflation and soaring interest rates. You might think that the failure of any of these dire predictions to come true would inspire some second thoughts, but, after all these years, the same people are still being invited to testify, and are still saying the same things…. In Europe, four years have passed since the Continent turned to harsh austerity programs. The architects of these programs told us not to worry about adverse impacts on jobs and growth–the economic effects would be positive, because austerity would inspire confidence. Needless to say, the confidence fairy never appeared….

So what has been the response of the good guys?… The Obama administration’s heart–or, at any rate, its economic model–is in the right place. The Federal Reserve has pushed back against the springtime-for-Weimar, inflation-is-coming crowd. The International Monetary Fund has put out research debunking claims that austerity is painless. But these good guys never seem willing to go all-in…. The classic example is the Obama stimulus… obviously underpowered given the economy’s dire straits. That’s not 20/20 hindsight….

The Fed has, in its own way, done the same thing. From the start, monetary officials ruled out the kinds of monetary policies most likely to work–in particular, anything that might signal a willingness to tolerate somewhat higher inflation, at least temporarily. As a result, the policies they have followed have fallen short of hopes, and ended up leaving the impression that nothing much can be done.

And the same may be true even in Japan… finally adopting the kind of aggressive monetary stimulus Western economists have been urging for 15 years and more. Yet there’s still a diffidence… a tendency to set things like inflation targets lower than the situation really demands… [that] increases the risk that Japan will fail to achieve ‘liftoff’–that the boost it gets from the new policies won’t be enough to really break free from deflation.

You might ask why the good guys have been so timid, the bad guys so self-confident. I suspect that the answer has a lot to do with class interests. But that will have to be a subject for another column.

…There is a well-known joke about economic methodology. Two friends are walking along when one spots a €50 note on the floor. “Look!” he says, “Let’s pick up the money.” His friend, an economist, replies: “No, don’t bother. If it were really there, somebody would have picked it up already.” The joke of course is about the lack of realism in the assumptions economists conventionally make in order to analyse the real world….

In practice, the version of this assumption used in applied analysis is rarely as strong. In practice, it is more like: given the limited information available to them, and the various transaction costs they face in taking certain courses of action, and given that the future is very uncertain, we’ll assume people act broadly in their self-interest, however they would define that. I would strongly defend the use of this contingent version of the standard assumption as it’s a powerful analytical tool…. Modern institutional economics, which is a thriving area of research, is founded on the use of the rationality assumption as a tool of analysis. If people do not seem to be making the rational choice, then looking at the difference between what would happen if they did so and the reality is instructive….

I would defend using the assumption of rational choice as long as one realises that it is not a description of reality. But there is one area where for 30 years economists – and others – have been making that mistake. That is, unfortunately, of course, in the financial markets. Practitioners and policy makers acted as if the strong form of the Efficient Markets Hypothesis held true – in other words that prices instantly reflect all relevant information about the future – even though this evidently defies reality. What’s more, a political philosophy valuing limited government leapt on what was taken as proof that markets left to themselves deliver better economic outcomes. This was translated as the deregulation of markets, especially financial markets, and became entwined with the growing importance of the finance sector in the economy globally. So politics fed the trend. The computer and communications technologies fed the trend as well, by making more and more financial transactions possible.

I think an honest conventionally-trained economist has to at least acknowledge that we grew intellectually lazy…. A particular ideological version of economics became the framework for analysing public policy, and very few mainstream economists challenged that. We got on with our work and ignored the importance of the public rhetoric….

A looser version is that a public sphere founded on the world view of narrow, rational choice economic models has over time led people to behave like the selfish, calculating beings assumed in those models. If regulations assume that you are going to behave in a certain way, there must surely be a temptation to live up to the assumption. I don’t know if this theory of economic performativity is true; perhaps the causality runs the other way, and a period of free-market politics especially in the US and UK changed the character of economics? We can’t test these alternatives, but this criticism is worth considering….

The financial and economic crisis [thus] spells a crisis for certain areas of economics, or approaches to economics. Financial economics and macroeconomics are particularly vulnerable. They are the subject areas where the consequences of the standard assumptions have been most damaging, because they are actually least valid. Financial market traders are not remotely like Star Trek’s Mr Spock, making rational calculations unaffected by emotion or by the decisions of other people. Macroeconomics – the study of how millions of individual decisions aggregate into economy-wide measures – is essentially ideological. How macroeconomists answer a question like ‘What will be the effect of cutting the budget deficit on growth next year?’ depends on their political views. This is not remotely a scientific area of the discipline….

I can’t omit here a few other problems with economics as it has been practised… the economics curriculum in universities… gives too much time to macroeconomics, on which as I just argued there is no professional consensus…. They have little sense of economic history…. Students are also not systematically taught new aspects of the subject…. Undergraduates are also taught as if they are all planning to go on to study for a doctorate and become academic economist…. Finally, many of these under-cooked economics graduates go on to work in government…. There are some good reasons for this special status – I’m about to come on to those – but the influence economists have in government needs seasoning with a corresponding degree of humility. One side-effect of the crisis may be to make economists a bit more humble, which would be a good result.

This is a weekly post we publish on Fridays with links to articles that touch on economic inequality and growth. The first section is a round-up of what Equitable Growth has published this week and the second is work we’re highlighting from elsewhere. We won’t be the first to share these articles, but we hope by taking a look back at the whole week, we can put them in context.

Equitable Growth round-up

The evidence shows that the proliferating number of tax expenditures in the United States intended to replace some function of the welfare state are inefficient. They’re also inequitable, as most benefits go to high-income households. And they’re opaque to both policymakers and the public.

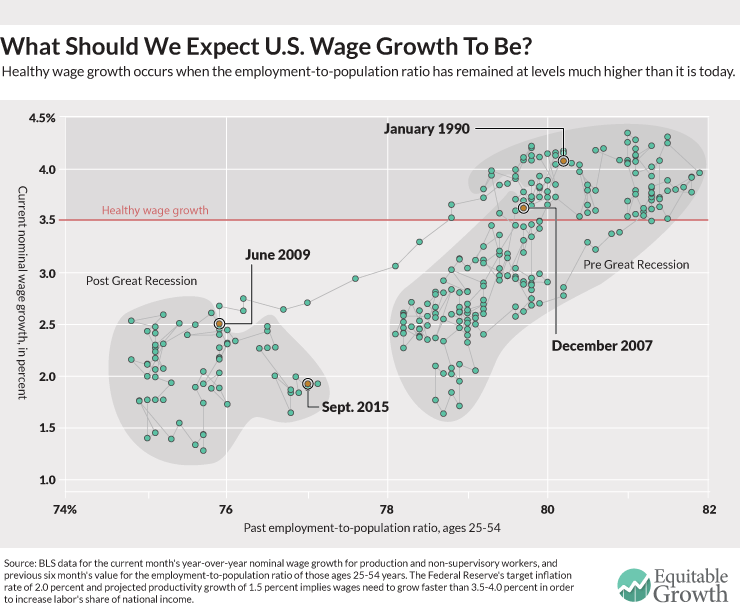

The Phillips curve has been at the center of recent discussions about the health of the U.S. economy and the future actions of the Federal Reserve. While the traditional Phillips curve that looks at inflation might be dead, we might want to look at what happens to wages.

The rise of companies like Uber, Airbnb, and Dropbox has sparked a fascination with these so-called “unicorn” companies. These privately held companies valued at more than $1 billion might seem like the future of the firm, but they are very much horses of a different color.

The unencumbered movement of capital among countries is supposed to be one of the great tenets of globalization. But economists have started to wonder if the case for free capital isn’t as strong as they once thought.

Links from around the web

George Akerlof and Robert Shiller, both winners of the Nobel Prize in economics, have a new book out about the ways in which markets can deceive consumers. Jeff Guo interviews the pair, and the conversation touches on Shiller’s cat, the Kardashians, and the morality of gambling. [wonkblog]

A recent column by economist Mike Spence and former Federal Reserve Governor Kevin Warsh on the relationship between monetary policy and business investment didn’t make a lot of sense to former U.S. Treasury Secretary Larry Summers. “I would put the Spence-Warsh doctrine that easy money reduces investment in a class of propositions backed by neither logic nor evidence.” [wonkblog]

Speaking of business investment, J.W. Mason agrees that monetary policy probably didn’t hold back investment growth. But is investment growth really that strong? Mason finds evidence that, in fact, it seems to be below historical levels. [the slack wire]

If you’ve read any tax reform plans, there’s a good chance they call for a reduction in tax brackets. But the idea that a reduction in brackets will make the system simpler in the face of all our deductions and credits seems misguided. In fact, there’s a good case for adding more brackets—and Jeff Spross makes it. [the week]

Thinking about a world without scarcity might not seem sensible in the wake of a large financial crisis. But the rise of information technology companies, increasing business concentration, and declining investment might make us rethink that hesitancy. [ft alphaville]

Jack Morton Auditorium, George Washington University :: April 15-16, 2015

It has now been seven years since the onset of the global financial crisis. A central question is how the crisis has changed our view on macroeconomic policy. The IMF originally tackled this issue at a 2011 conference and again at a 2013 conference. Both conferences proved very successful, spawning books titled In the Wake of the Crisis and What Have We Learned? published by the MIT Press.

The time seemed right for another assessment. Research has continued, policies have been tried, and the debate has been intense. How much progress has been made? Are we closer to a new framework? To address these questions the IMF organized a follow up conference on “Rethinking Macro Policy III: Progress or Confusion?”, which took place at the Jack Morton Auditorium in George Washington University, Washington DC, on April 15–16, 2015.

The conference was co-organized by IMF Economic Counselor Olivier Blanchard, RBI Governor Raghu Rajan, and Harvard Professors Ken Rogoff and Larry Summers. It brought together leading academics and policymakers from around the globe, as well as representatives from civil society, the private sector, and the media. Attendance was by invitation only.

Wrap Up Video:

J. Bradford DeLong

On the Proper Size of the Public Sector, and the Proper Level of Public Debt, in the Twenty-First Century

Introduction

Olivier Blanchard, when he parachuted me into the panel, asked me to “be provocative.”

So let me provoke:

My assigned focus on “fiscal policy in the medium term” has implications. It requires me to assume that things are or will be true that are not now or may not be true in the future, at least not for the rest of this decade and into the next. It makes sense to distinguish the medium from the short term only if the North Atlantic economies will relatively soon enter a regime in which the economy is not at the zero lower bound on safe nominal interest rates. The medium term is at a horizon at which monetary policy can adequately handle all of the demand-stabilization role.

The focus on a medium run thus assumes that answers have been found and policies implemented for three of the most important macroeconomic questions facing us right now, here in the short run, today. Those three are:

What role does fiscal policy have to play as a cyclical stabilization policy?

What is the proper level of the inflation target so that open-market operation-driven normal monetary policy has sufficient purchase?

Should truly extraordinary measures that could be classified as “social credit” policies—mixed monetary and fiscal expansion via direct assignment of seigniorage to households, money-financed government purchases, central bank–undertaken large-scale public lending programs, and other such—be on the table?

Those three are still the most urgent questions facing us today. But I will drop them, and leave them to others. I will presume that satisfactory answers have been found to them, and that they have thus been answered.

As I see it, there are three major medium-run questions that then remain, even further confining my scope to the North Atlantic alone, and to the major sovereigns of the North Atlantic. (Extending the focus to emerging markets, to the links between the North Atlantic and the rest of the world, and to Japan would raise additional important questions, which I would also drop on the floor.) These three remaining medium-run questions are:

What is the proper size of the twenty-first-century public sector?

What is the proper level of the twenty-first-century public debt for growth and prosperity?

What are the systemic risks caused by government debt, and what adjustment to the proper level of twenty-first-century public debt is advisable because of systemic risk considerations?

To me, at least, the answer to the first question—what is the proper size of the twenty-first-century public sector?—appears very clear:

The optimal size of the twenty-first-century public sector will be significantly larger than the optimal size of the twentieth-century public sector. Changes in technology and social organization are moving us away from a “Smithian” economy, one in which the presumption is that the free market or the Pigovian-adjusted market does well, to one that requires more economic activity to be regulated by differently tuned social and economic arrangements (see DeLong and Froomkin 2000). One such is the government. Thus, there should be more public sector and less private sector in the twenty-first century than there was in the twentieth.

Similarly, the answer to the second question appears clear, to me at least:

Thus, at the margin, additional government debt has not required a greater primary surplus but rather has allowed a greater primary deficit—a consideration that strongly militates for higher debt levels unless interest rates in the twenty-first century reverse the pattern we have seen in the twentieth century, and mount to levels greater than economic growth rates.

The answer to the third question—what are the systemic risks caused by government debt?—is much more murky:

To be clear: the point is not that additional government debt imposes an undue burden in the form of distortionary taxation and inequitable income distribution on the future. When current and projected interest rates are low, they do not do so. The point is not that additional government debt crowds out productive investment and slows growth. When interest rates are unresponsive or minimally responsive to deficits, they do not do so. Were either of those to fail to hold, we would have exited the current regime of ultra-low interest rates, and the answer to the second question immediately above would become different.

The question, instead, is this: in a world of low current and projected future interest rates—and thus also one in which interest rates are not responsive to deficits—without much expected crowding out or expected burdens on the future, what happens in the lower tail, and how should that lower tail move policies away from those optimal on certainty equivalence? And that question has four subquestions: How much more likely does higher debt make it that interest rates will spike in the absence of fundamental reasons? How much would they spike? What would government policy be in response to such a spike? And what would be the effect on the economy?

The answer thus hinges on:

the risk of a large sudden upward shift in the willingness to hold government debt, even absent substantial fundamental news, and

the ability of governments to deal with such a risk that threatens to push economies far enough up the Laffer curve to turn a sustainable into an unsustainable debt.

I believe the risk in such a panicked flight from an otherwise sustainable debt is small. I hold, along with Reinhart and Rogoff (2013), that the government’s legal tools to finance its debt through financial repression are very powerful. Thus I think this consideration has little weight. I believe that little adjustment to one’s view of the proper level of twenty-first-century public debt of reserve-currency-issuing sovereigns with exorbitant privilege is called for because of systemic risk considerations.

But my belief here is fragile. And my comprehension of the issues is inadequate.

Let me expand on these three answers:

The Proper Size of Twenty-First-Century Government

Suppose commodities produced and distributed are properly rival and excludible:

Access to them needs to be cheaply and easily controlled.

They need to be scarce.

*They need to be produced under roughly constant-returns-to-scale conditions.

Suppose, further, that information about what is being bought and sold is equally present on both sides of the marketplace—that is, limited adverse selection and moral hazard.

Suppose, last, that the distribution of wealth is such as to accord fairly with utility and desert.

If all these hold, then the competitive Smithian market has its standard powerful advantages. And so the role of the public sector should then be confined to:

antitrust policy, to reduce market power and microeconomic price and contract stickinesses,

demand-stabilization policy, to offset the macroeconomic damage caused by macroeconomic price and contract stickinesses,

financial regulation, to try to neutralize the effect on asset prices of the correlation of current wealth with biases toward optimism or pessimism, along with

largely fruitless public-sector attempts to deal with other behavioral economics-psychological market failures—envy, spite, myopia, salience, etc.

The problem, however, is that as we move into the twenty-first century, the commodities we will be producing are becoming:

less rival,

less excludible,

more subject to adverse selection and moral hazard, and

more subject to myopia and other behavioral-psychological market failures.

The twenty-first century sees more knowledge to be learned, and thus a greater role for education. If there is a single sector in which behavioral economics and adverse selection have major roles to play, it is education. Deciding to fund education through very long-term loan financing, and thus to leave the cost-benefit investment calculations to be undertaken by adolescents, shows every sign of having been a disaster when it has been tried (see Goldin and Katz 2009).

The twenty-first century will see longer life expectancy, and thus a greater role for pensions. Yet here in the United States the privatization of pensions via 401(k)s has been, in my assessment, an equally great disaster (Munnell 2015).

The twenty-first century will see health care spending as a share of total income cross 25 percent if not 33 percent, or even higher. The skewed distribution across potential patients of health care expenditures, the vulnerability of health insurance markets to adverse selection and moral hazard, and simple arithmetic mandate either that social insurance will have to cover a greater share of health care costs or that enormous utilitarian benefits from health care will be left on the sidewalk.

Moreover, the twenty-first century will see information goods a much larger part of the total pie than in the twentieth. And if we know one thing, it is that it is not efficient to try to provide information goods by means of a competitive market for they are neither rival nor excludible. It makes no microeconomic sense at all for services like those provided by Google to be funded and incentivized by how much money can be raised not fromthe value of the services but fromthe fumes rising from Google’s ability to sell the eyeballs of the users to advertisers as an intermediate good.

And then there are the standard public goods, like infrastructure and basic research.

Enough said.

The only major category of potential government spending that both should not—and to an important degree cannot—be provided by a competitive price-taking market, and that might be a smaller share of total income in the twenty-first century than it was in the twentieth? Defense.

We thus face a pronounced secular shift away from commodities that have the characteristics—rivalry, excludability, and enough repetition in purchasing and value of reputation to limit myopia—needed for the Smithian market to function well as a societal coordinating mechanism. This raises enormous problems: We know that as bad as market failures can be, government failures can often be little if any less immense.

We will badly need to develop new effective institutional forms for the twenty-first century.

But, meanwhile, it is clear that the increasing salience of these market failures has powerful implications for the relative sizes of the private market and the public administrative spheres in the twenty-first century. The decreasing salience of “Smithian” commodities in the twenty-first century means that rational governance would expect the private-market sphere to shrink relative to the public. This is very elementary micro- and behavioral economics. And we need to think hard about what its implications for public finance are.

The Proper Size of the Twenty-First-Century Public Debt

Back in the Clinton administration—back when the US government’s debt really did look like it was on an unsustainable course—we noted that the correlation between shocks to US interest rates and the value of the dollar appeared to be shifting from positive to zero, and we were scared that the United States was alarmingly close to its debt capacity and needed major, radical policy changes to reduce the deficit (see Blinder and Yellen 2000).

Whether we were starting at shadows then, or whether we were right then and the world has changed since, or whether the current world is in an unstable configuration and we will return to normal within a decade is unclear to me.

But right now, financial markets are telling us very strange things about the debt capacity of reserve-currency-issuing sovereigns.

Since 2005, the interest rate on US ten-year Treasury bonds has fallen from roughly the growth rate of nominal GDP—5 percent/year—to 250 basis points below the growth rate of nominal GDP. Because the duration of the debt is short, the average interest rate on Treasury securities has gone from 100 basis points below the economy’s trend growth rate to nearly 350 basis points below. Maybe you can convince yourself that the market expects the ten-year rate over the next generation to average 50 basis points higher than it is now. Maybe.

Taking a longer run view, Richard Kogan and co-workers (2015) of the Center on Budget and Policy Priorities have been cleaning the data from the Office of Management and Budget. Over the past two hundred years, for the United States, the government’s borrowing rate has averaged 100 basis points lower than the economy’s growth rate. Over the past one hundred years, 170 basis points lower. Over the past fifty years, 30 basis points lower. Over the past twenty years, the Treasury’s borrowing rate has been on average greater than g by 20 basis points. And over the past ten years, it has been 70 basis points lower.

When we examine the public finance history of major North Atlantic industrial powers, we find that the last time that the average over any decade of government debt service as a percentage of outstanding principal was higher than the average growth rate of its economy was during the Great Depression. And before that, in 1890.

Since then, over any extended time period for the major North Atlantic reserve-currency-issuing economies, g > r, for government debt.

Only those who see a very large and I believe exaggerated chance of global thermonuclear war or environmental collapse see the North Atlantic economies as dynamically inefficient from the standpoint of our past investments in private physical, knowledge, and organizational capital: r > g by a very comfortable margin for investments made in private capital. Investments in wealth in the form of private capital are, comfortably, a cash flow source for savers.

But the fact that g > r with respect to the investments we have made in our governments raises deep and troubling questions.

Since 1890, a North Atlantic government that borrows more at the margin benefits its current citizens, increases economic growth, and increases the well-being of its bondholders (for they do buy the paper voluntarily): it is win-win-win. That fact strongly suggests that North Atlantic economies throughout the entire twentieth century suffered from excessive accumulation of societal wealth in the form of net government capital—in other words, government debt has been too low.

The North Atlantic economies of major sovereigns throughout the entire twentieth century have thus suffered from a peculiar and particular form of dynamic inefficiency. Over the past one hundred years, in the United States, at the margin, each extra stock 10 percent of annual GDP’s worth of debt has provided a flow of 0.1 percent of GDP of services to taxpayers, either in increased primary expenditures, reduced taxes, or both.

What is the elementary macroeconomics of dynamic inefficiency? If a class of investment—in this case, investment by taxpayers in the form of wealth held by the government through amortizing the debt—is dynamically inefficient, do less of it. Do less of it until you get to the Golden Rule, and do even less if you are impatient. How do taxpayers move away from dynamic inefficiency toward the Golden Rule? By not amortizing the debt, but rather by borrowing more.

Now we resist this logic. I resist this logic.

Debt secured by government-held social wealth ought to be a close substitute in investors’ portfolios with debt secured by private capital formation. So it is difficult to understand how economies can be dynamically efficient with respect to private capital and yet “dynamically inefficient” with respect to government-held societal wealth. But it appears to be the case that it is so. But there is this outsized risk premium, outsized equity and low-quality debt premium, outsized wedge. And that means that while investments in wealth in the form of private capital are a dynamically efficient cash flow source for savers, investments by taxpayers in the form of paying down debt are a cash flow sink.

I tend to say that we have a huge underlying market failure here that we see in the form of the equity return premium—a failure of financial markets to mobilize society’s risk-bearing capacity—and that pushes down the value of risky investments and pushes up the value of assets perceived as safe, in this case the debt of sovereigns possessing exorbitant privilege. But how do we fix this risk-bearing capacity mobilization market failure? And isn’t the point of the market economy to make things that are valuable? And isn’t the debt of reserve-currency-issuing sovereigns an extraordinarily valuable thing that is very cheap to make? So shouldn’t we be making more of it? Looking out the yield curve, such government debt looks to be incredibly valuable for the next half century, at least.

These considerations militate strongly for higher public debts in the twenty-first century then we saw in the twentieth century. Investors want to hold more government debt: the extraordinary prices at which it has sold since 1890 tell us that. Market economies are supposed to be in the business of producing things that households want whenever that can be done cheaply. Government debt fits the bill, especially now. And looking out the yield curve, government debt looks to fit the bill for the next half century at least.

Systemic Risks and Public Debt Accumulation

One very important question remains very live: Would levels of government debt issue large enough to drive r > g for government bonds create significant systemic risks? Yes, the prices of the government debt of major North Atlantic industrial economies are very high now. But what if there is a sudden downward shock to the willingness of investors to hold this debt? What if the next generation born and coming to the market is much more impatient? Governments might then have to roll over their debt on terms that require high debt-amortization taxes, and if the debt is high enough, those taxes could push economies far enough up a debt Laffer curve. That might render the debt unsustainable in the aftermath of such a preference shift.

Two considerations make me think that this is a relatively small danger:

When I look back in history, I cannot see any such strong fundamental news-free negative preference shock to the willingness to hold the government debt of the North Atlantic’s major industrial powers since the advent of parliamentary government. The fiscal crises we see—of the Weimar Republic, Louis XIV Bourbon, Charles II Stuart, Felipe IV Habsburg, and so forth—were all driven by fundamental news.

As [Reinhart and Rogoff (2013)(http://www.imf.org/external/pubs/ft/wp/2013/wp13266.pdf) have pointed out at substantial length, twentieth- and nineteenth-century North Atlantic governments proved able to tax their financial sectors through financial repression with great ease. The amount of real wealth for debt amortization raised by financial repression scales roughly with the value of outstanding government debt. And such taxes are painful for those taxed. But only when even semi-major industrial countries have allowed large-scale borrowing in potentially harder currencies than their own—and thus have written unhedged puts on their currencies in large volume—is there any substantial likelihood of major additional difficulty or disruption.

Now, Kenneth Rogoff (2015) disagrees with drawing this lesson from Reinhart and Rogoff (2013). And one always disagrees analytically with Kenneth Rogoff at one’s great intellectual peril. He sees the profoundly depressed level of interest rates on the debt of major North Atlantic sovereigns as a temporary and disequilibrium phenomenon that will soon be rectified. He believes that excessive debt issue and overleverage are at the roots of our problems—call it secular stagnation, the global savings glut, the safe asset shortage, the balance sheet recession, whatever.

Unlike secular stagnation, a debt supercycle is not forever.… Modern macroeconomics has been slow to get to grips with the analytics of how to incorporate debt supercycles.… There has been far too much focus on orthodox policy responses and not enough on heterodox responses.… In a world where regulation has sharply curtailed access for many smaller and riskier borrowers, low sovereign bond yields do not necessarily capture the broader “credit surface” the global economy faces.… The elevated credit surface is partly due to inherent riskiness and slow growth in the post-Crisis economy, but policy has also played a large role.

The key here is Rogoff’s assertion that the low borrowing rate faced by major North Atlantic sovereigns “do[es] not necessarily capture the broader ‘credit surface’”—that the proper shadow price of government debt issue is far in excess of the sovereign borrowing rate. Why? Apparently because future states of the world in which private bondholders would default are also those in which it would be very costly in social utility terms for the government to raise money through taxes.

I do not see this. A major North Atlantic sovereign’s potential tax base is immensely wide and deep. The instruments at its disposal to raise revenue are varied and powerful. The correlation between the government’s taxing capacity and the operating cash flow of private borrowers is not that high. A shock like that of 2008–2009 temporarily destroyed the American corporate sector’s ability to generate operating cash flows to repay debt at the same time that it greatly raised the cost of rolling over debt. But the US government’s financial opportunities became much more favorable during that episode.

Moreover, Rogoff also says:

When it comes to government spending that productively and efficiently enhances future growth, the differences are not first order. With low real interest rates, and large numbers of unemployed (or underemployed) construction workers, good infrastructure projects should offer a much higher rate of return than usual.

and thus, with sensible financing and recapture of the economic benefits of government spending, have little or no impact on debt-to-income ratios.

Conclusion

Looking forward, I draw the following conclusions:

North Atlantic public sectors for major sovereigns ought, technocratically, to be larger than they have been in the past century.

North Atlantic relative public debt levels for major sovereigns ought, technocratically, to be higher than they have been in the past century.

With prudent regulation—that is, the effective limitation of the banking sector’s ability to write unhedged puts on the currency—the power major sovereigns possess to tax the financial sector through financial repression provides sufficient insurance against an adverse preference shock to the desire for government debt.

The first two of these conclusions appear to me to be close to rock-solid. The third is, I think, considerably less secure.

Nevertheless, in my view, if the argument against a larger public sector and more public debt in the twenty-first century than in the twentieth for major North Atlantic sovereigns is going to be made successfully, it seems to me that it needs to be made on a political-economy government-failure basis.

The argument needs to be not that larger government spending and a higher government debt issued by a functional government would diminish utility but rather that government itself will be highly dysfunctional. Government needs to be viewed not as one of several instrumentalities we possess and can deploy to manage and coordinate our societal division of labor, but rather as the equivalent of a loss-making industry under really existing socialism. Government spending must be viewed as worse than useless. Therefore relaxing any constraints that limit the size of the government needs to be viewed as an evil.

Now the public choice school has gone there. As Lawrence Summers (2011) said, they have taken the insights on government failure and “driven it relentlessly towards nihilism in a way that isn’t actually helpful for those charged with designing regulatory institutions,” or, indeed, making public policy in general. In my opinion, if this argument is to be made, it needs a helpful public choice foundation before it can be properly built.

Figure 20.1: Ten-year Constant Maturity U.S. Treasury Nominal Rate:

Source: Federal Reserve Economic Data, Federal Reserve Bank of St. Louis.

Figure 20.2: Economic Growth and Interest Rates Have Become More Closely Aligned:

Nominal Interest Rate & Smoothed Forward Nominal GDP Growth Rate:

Source: Richard Kogan and colleagues of the Center on Budget and Policy Priorities http://CBPP.org

References

Blinder, Alan, and Janet Yellen. 2000. The Fabulous Decade: Macroeconomic Lessons from the 1990s. New York: Century Foundation.

DeLong, J. Bradford. 2014. “Notes on Fiscal Policy in a Depressed Interest-Rate Environment.” Faculty blog, Department of Economics, University of California, Berkeley, March 16. http://delong.typepad.com/delonglongform/2014/03/talk-preliminary-notes-on-fiscal-policy-in-a-depressed-interest-rate-environment-the-honest-broker-for-the-week-of-february.html.

DeLong, J. Bradford, and A. Michael Froomkin. 2000. “Speculative Microeconomics for Tomorrow’s Economy.” First Monday 5 (2), February 7. http://firstmonday.org/ojs/index.php/fm/article/view/726.

Goldin, Claudia, and Lawrence Katz. 2009. The Race between Education and Technology. Cambridge, MA: Harvard University Press.

Kogan, Richard, Chad Stone, Bryann Dasilva, and Jan Rezeski. 2015. “Difference between Economic Growth Rates and Treasury Interest Rates Significantly Affects Long-Term Budget Outlook.” Washington, DC: Center on Budget and Policy Priorities, February 27. http://www.cbpp.org/research/federal-budget/difference-between-economic-growth-rates-and-treasury-interest-rates.

Munnell, Alicia. 2015. “Falling Short: The Coming Retirement Crisis and What to Do About It.” Brief 15-7. Center for Retirement and Research, Boston College,April. http://crr.bc.edu/briefs/falling-short-the-coming-retirement-crisis-and-what-to-do-about-it-2.

Reinhart, Carmen M., and Kenneth S. Rogoff. 2013. “Financial and Sovereign Debt Crises: Some Lessons Learned and Those Forgotten.” Working Paper 266. Washington, DC: IMF, December 24. https://www.imf.org/external/pubs/cat/longres.aspx?sk=41173.0.

Rogoff, Kenneth. 2015. “Debt Supercycle, Not Secular Stagnation.” VoxEU. Centre for Economic Policy and Research, April 22. http://www.voxeu.org/article/debt-supercycle-not-secular-stagnation.

Summers, Lawrence. 2011. “A Conversation on New Economic Thinking.” LarrySummers.com, April 8. http://larrysummers.com/commentary/speeches/brenton-woods-speech.

Summers, Lawrence. 2014. “U.S. Economic Prospects: Secular Stagnation, Hysteresis, and the Zero Lower Bound.” Business Economics 49 (2): 65–73.