…what we should now be calling “The Lesser Depression”, and what we are likely to someday call “The Longer Depression”:

Must-read: Wolfgang Munchau: “The Errors Behind Europe’s Many Crises”

Must-Read: : The Errors Behind Europe’s Many Crises: “The EU was wrong to construct a single currency without a proper banking union…

…wrong to create a passport-free travel zone without a common border police force and immigration policy. [And] I would add EU enlargement… the haste with which it was pursued. The cardinal mistake of our time was the decision to muddle through the eurozone crisis. Europe’s political leadership failed to generate the public support for what was needed: creating a political and economic union. Instead, the European Council did the minimum necessary…. There are four channels through which that policy contributed to the broader instability….

First… the EU has the capacity only to deal with one big crisis at a time…. Second… the conflation, real or imaginary, of two more crises. The Greek economy continues to contract… refugees have been trapped in Greece… since Macedonia closed the border…. There are the fake connections. Poland has used last week’s Brussels bombings as a pretext for questioning a commitment to accept 7,000 refugees… an interaction between the terrorist attacks and the prospect of British exit…. Third… the output of several eurozone countries has yet to return to pre-crisis levels. Security… was among the areas most affected by austerity…. The widening income gap between rich and poor — and north and south….

Fourth… a generalised loss of trust and political capital…. Populist parties on the left and the right are exploiting the union’s failures…. The combination of these four channels frustrates perfectly good ideas for further projects aimed at European integration–those that would benefit everybody, such as central agencies to co-ordinate the fight against terrorism and to deal with the influx of refugees. If the EU had not messed up the previous crises, people would look at a European immigration policy or an antiterrorism task force with a more open mind. But would you trust with your own security somebody who cannot even contain a medium-sized financial crisis?…

Economic history has shown… that efforts to muddle through financial crises never work…. For the EU it was a catastrophic policy error… an economic depression… destroyed public confidence in the EU and in the very idea of European integration.

Must-read: Martin Wolf: “Helicopter drops might not be far away”

Must-Read: The central banks of the North Atlantic seem to be rapidly digging themselves into a hole in which, if there is an adverse demand shock, their only options will be (a) dither, and (b) seize the power to do a degree of fiscal policy via helicopter money by some expedient or other…

: Helicopter drops might not be far away: “The world economy is slowing, both structurally and cyclically…

…How might policy respond? With desperate improvisations, no doubt. Negative interest rates… fiscal expansion. Indeed, this is what the OECD, long an enthusiast for fiscal austerity, recommends…. With fiscal expansion might go direct monetary support, including the most radical policy of all: the ‘helicopter drops’ of money recommended by the late Milton Friedman… the policy foreseen by Ray Dalio, founder of Bridgewater, a hedge fund….

Why might the world be driven to such expedients? The short answer is that the global economy is slowing durably…. Behind this is a simple reality: the global savings glut — the tendency for desired savings to rise more than desired investment — is growing and so the ‘chronic demand deficiency syndrome’ is worsening…. The long-term real interest rate on safe securities has been declining for at least two decades….

It is this background — slowing growth of supply, rising imbalances between desired savings and investment, the end of unsustainable credit booms and, not least, a legacy of huge debt overhangs and weakened financial systems — that explains the current predicament. It explains, too, why economies that cannot generate adequate demand at home are compelled towards beggar-my-neighbour, export-led growth via weakening exchange rates….

The OECD argues, persuasively, that co-ordinated expansion of public investment, combined with appropriate structural reforms, could expand output and even lower the ratio of public debt to gross domestic product. This is particularly plausible nowadays, because the major governments are able to borrow at zero or even negative real interest rates, long term. The austerity obsession, even when borrowing costs are so low, is lunatic (see chart). If the fiscal authorities are unwilling to behave so sensibly — and the signs, alas, are that they are not — central banks are the only players… send money… to every adult citizen. Would this add to demand? Absolutely….

The easy way to contain any long-term monetary effects would be to raise reserve requirements. These could then become a desirable feature of our unstable banking systems…. The economic forces that have brought the world economy to zero real interest rates and, increasingly, negative central bank rates are, if anything, now strengthening…. Policymakers must prepare for a new ‘new normal’ in which policy becomes more uncomfortable, more unconventional, or both…

Must-reads: March 25, 2016

Weekend reading: Hysteresis, wage setting, market concentration, and more

This is a weekly post we publish on Fridays with links to articles that touch on economic inequality and growth. The first section is a round-up of what Equitable Growth has published this week and the second is work we’re highlighting from elsewhere. We won’t be the first to share these articles, but we hope by taking a look back at the whole week, we can put them in context.

Equitable Growth round-up

After recessions, there’s usually quite a bit of geographic variation in employment rates. Some areas of the country are hit much worse by a recession than others, but eventually those differences erode. But that hasn’t happened in the wake of the Great Recession—and a new paper says it might not happen until 2021.

The role of firms in income inequality is an increasingly popular topic of conversation for researchers and analysts. But sometimes those conversations conflate two different trends that result in firms paying more on average than other firms. Untangling the two has important ramifications for how we understand the labor market.

Tax credits have become some of the more popular policy interventions when it comes to improving the living standards of workers at the lower end of the wage distribution. While programs like the Earned Income Tax Credit have been quite successful, they certainly can be improved, as new research shows.

As the global economy seems to weaken, investors complain about the communications strategy of the Federal Reserve, and commentators ponder the usefulness of policies once deemed radical, a debate about the proper tools of monetary policy is raging. But maybe it’s time to expand that conversation even further.

Links from around the web

The last two decades have seen high levels of corporate profits, an increasing return to capital, and high levels of market concentration in the United States. In other words, the U.S. economy has a competition problem. The Economist details the extent of this problem. [the economist]

Despite continued gains, there’s still a significant gap between the earnings of men and women in the United States. While there are a number of reasons for that gap, a major cause is occupational segregation. Claire Cain Miller digs into new research on the topic. [the upshot]

The research Miller cites is an example of work that takes into account the role of gender and identity when it comes to economic matters. As Martin Sandbu argues, ignoring the role of gender can lead to economic analysis that misses major trends and significant issues. [free lunch]

“We’re out of the frying pan of speculative excess and into a subtler and more insidious problem of chronic undersupply.” Matt Yglesias details the next housing crisis the U.S. economy is facing. [vox]

Over the past four years, members of the Federal Open Markets Committee—the Federal Reserve’s policymaking arm—have been steadily lowering their estimate of “longer-run” interest rates. Matthew C. Klein notes that this indicates the central bank is starting to come to grips with the idea of secular stagnation. [ft alphaville]

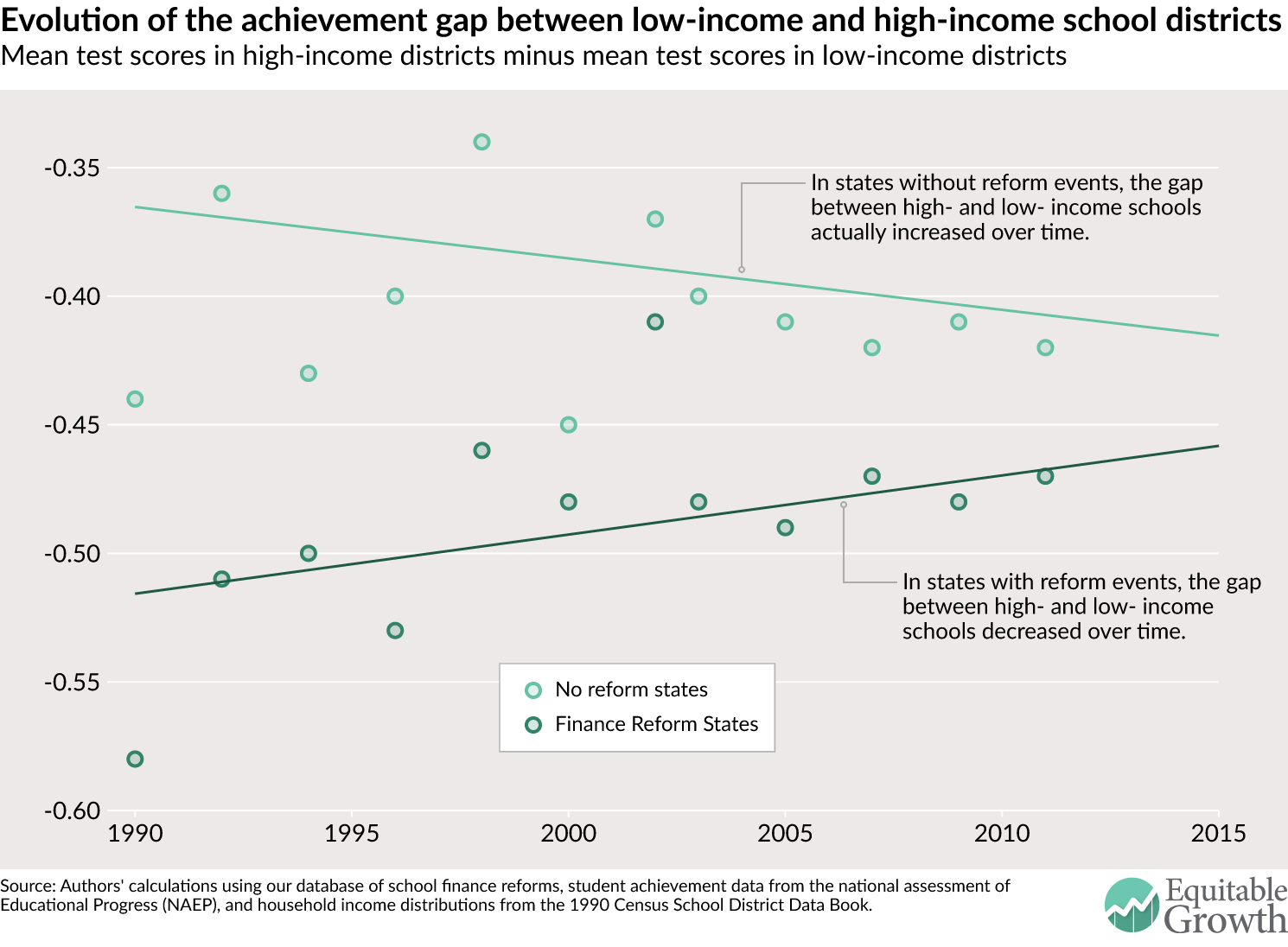

Friday figure

Figure from “Can school finance reforms improve student achievement?” by Julien Lafortune, Jesse Rothstein, and Diane Whitmore Schanzenbach.

Must-Read: Pam Samuelson et al.: About Us | Authors Alliance

Must-Read: A very worthy endeavor.

However, I feel like a gotta say here that Google Books was the best vehicle for them to realize their dreams.

What is the current state of Google Books, anyway?

: About Us | Authors Alliance: “Authors Alliance promotes authorship for the public good…

… by supporting authors who write to be read. We embrace the unprecedented potential digital networks have for the creation and distribution of knowledge and culture. We represent the interests of authors who want to harness this potential to share their creations more broadly in order to serve the public good. Unfortunately, authors face many barriers that prevent the full realization of this potential to enhance public access to knowledge and creativity. Authors who are eager to share their existing works may discover that those works are out of print, un-digitized, and subject to copyrights signed away long before the digital age. Authors who are eager to share new works may feel torn between publication outlets that maximize public access and others that restrict access but provide important value in terms of peer review, prestige, or monetary reward. Authors may also struggle to understand how to navigate fair use and the rights clearance process in order to lawfully build on existing works.

The mission of Authors Alliance is to further the public interest in facilitating widespread access to works of authorship by assisting and representing authors who want to disseminate knowledge and products of the imagination broadly. We provide information and tools designed to help authors better understand and manage key legal, technological, and institutional aspects of authorship in the digital age. We are also a voice for authors in discussions about public and institutional policies that might promote or inhibit the broad dissemination they seek.

Must-read: Avi Rabin-Havt: “Why Is the CBO Concocting a Phony Debt Crisis?”

Must-Read: : Why Is the CBO Concocting a Phony Debt Crisis?: “The CBO assumes that Social Security and Medicare Part A will draw on the general fund of the US Treasury…

…to cover benefit shortfalls following the depletion of their trust funds, which at the current rate will occur in 2034. That would obviously lead to an exploding debt, but it’s a scenario prohibited by law. In the case of both programs, benefits must be paid either from revenue collected via payroll taxes or from accumulated savings in the programs’ trust funds. When those funds run out, full benefits will simply not be paid. ‘Because there is no borrowing authority, there is really a hard stop,’ said Goss.

Congress could pass a law saying that Social Security and Medicare Part A would begin drawing on the US Treasury general fund after 2034. Or, Congress could preemptively pass laws to avert the situation before the deadline; it could take the approach favored by progressives and increase revenue to the programs by lifting the payroll tax cap, or alternatively raise the retirement age and lower benefits. But the bottom line is the CBO projections disregard the actual law and assume a worst-case legislative scenario—and one that is politically unlikely, to boot…

Must-read: Jon Faust: “Still Crazy After All These Years”

Must-Read: : Still Crazy After All These Years: “For the past several years, the Congressional Budget Office has been offering frightening forecasts…

…about government debt growing out of control unless strong action is taken. While these forecasts have played a prominent role in policy debates, the CFE’s Jonathan Wright and Bob Barbera have for several years been arguing that those forecasts are, well, crazy. Or as the headline on Bob’s 2014 FT piece put it: ‘Forecasts of U.S. Fiscal Armageddon are Wrong.’ The key… is that the CBOs economic growth and interest rate projections jointly make no sense…. Under the CBO’s projected tepid growth projection, interest rates were highly unlikely to rise to the assumed levels….

We were glad to read in Greg Ip’s recent column that Doug Elmendorf, the CBO director responsible for those forecasts until recently, now agrees. Elmendorf and Louise Scheiner of the Hutchins Institute make the argument that:

the fact that U.S. government borrowing rates are at historical lows and likely to stay low for some time, implies spending cuts and tax increases should be delayed and smaller in size than widely believed.

It was Elmendorf’s CBO that helped stoke those widely-believed views now labelled as misguided. And as noted above, the CBO is still stoking. For the sake of coherent public policy, we hope that the CBO will listen to Elmendorf and Scheiner.

Must-read: Jared Bernstein and Ben Spielberg: “Preparing for the Next Recession: Lessons from the American Recovery and Reinvestment Act”

Must-Read: : Preparing for the Next Recession: Lessons from the American Recovery and Reinvestment Act: “Measures that can quickly respond to a recession by bolstering the economy…

…and at least moderating the downturn’s negative impacts are important. While the Federal Reserve lowers interest rates and expands access to credit, the President and Congress can tap various ‘stabilizers’ through budget and tax policy that can offset some of the financial losses that households experience and help them maintain higher levels of consumer spending…. The depth of the Great Recession and the slow recovery, however, serve as poignant reminders that monetary policy and automatic stabilizers don’t always do enough. Meanwhile, state balanced-budget requirements present a serious obstacle to recovery efforts…. But while ARRA was clearly effective, many of its interventions ended too soon, as the economic need for them persisted both at the macroeconomic level (growth and unemployment) and the household level….

Moving forward in anticipation of further recessions, a stronger set of automatic stabilizers would help…. Make UI’s EB program more responsive to economic conditions by having it take effect more quickly and remain in effect until hardship and labor market weakness are alleviated sufficiently, encourage ‘worksharing’ among employees by creating incentives for it through UI, strengthen basic UI benefits, and bolster UI’s financing system. Have temporarily higher SNAP benefits (and perhaps higher SNAP administrative funds for states) take effect automatically when a trigger, possibly tied to state unemployment rates, reaches certain thresholds. Make state fiscal relief, in the form of higher federal payments to help states cover their Medicaid costs, take effect automatically, possibly via the same mechanism that is used to trigger a temporary increase in SNAP benefits. PPrepare for additional discretionary steps during downturns by establishing a dedicated fund for subsidized jobs and job creation programs and considering one-time housing vouchers that can help struggling families keep their homes, pay their rents, and avoid homelessness…

Must-reads: March 24, 2016

- (1936): The General Theory of Employment, Interest and Money

- : The State of American Politics

- : Global Inequality: A New Approach for the Age of Globalization

- (1936): A somewhat comprehensive socialization of investment…

- : Mission still not accomplished: To reach full employment we need to move fiscal policy from austerity to stimulus

- : Moving to the Innovation Frontier

- (2011): Zombie Marx

- : The Affordable Care Act at Six: Progress on Coverage, Costs, and Quality

- (1829): Contra Say’s Law: “Money, consequently, was in request, and all other commodities were in comparative disrepute…”

- (1819): The “General Glut”

- : Inputs in the Production of Early Childhood Human Capital: Evidence from Head Start

- : MMT and Mainstream Macro

- : Worthwhile Canadian Initiative: Reverse-Engineering the MMT Model