Must-Read: The Federal Funds rate is currently bouncing around between 0.82 and 0.91%. When the Federal Reserve embarked on its tightening cycle in December 2015, its median expectation was that by now it would have raised the Federal Funds rate to between 2.25 and 2.50%—that it would have undertaken 9 25 basis point interest rate hikes rather than three. Its expectation was that, even after those nine hikes, PCE core inflation would be running at 1.9% per year rather than the 1.5% per year that the smart money currently sees.

A policy significantly looser than they thought they were embarking on. And inflation outcomes noticeably worse, in the sense of falling below target, than they anticipated even with the tighter policies they thought they would adopt.

Yet I have very little sense of how the Federal Reserve is adjusting its thinking to its forecasting overoptimism for 2016 and now for 2017. Nor do I have any great sense of how the Federal Reserve is dealing with the fact that it has now been overoptimistic in forecasting 2017, 2016, 2015, 2014, 2013, 2012, 2011, 2010, 2009, and 2008:

…When the PCE deflator is released next Tuesday, it will probably show the 12-month core inflation rate at 1.5 per cent in April, the lowest figure since the end of 2015…. The Fed’s decisions are supposed to be data dependent…. The Fulcrum inflation models… produce short term projections for inflation based on methods that extract underlying price increases from noisy monthly data. The models’ near term inflation projections (red line) have dropped sharply as a result of the March and April CPI announcements, and the inflation rate for the rest of 2017 is now projected to run well below the rates forecast by the Fed in March (blue dots)….

Where does that leave the FOMC? I agree with Tim Duy that their present stance is still biased towards gradual tightening, because they are not yet placing much weight on changes in data methodology, or in the Phillips Curve. They have now dug themselves into a position where they will be extremely reluctant to drop the intended 25 basis points increase in the fed funds rate on 14 June, or the start of balance sheet shrinkage, probably announced in September. Lowflation will probably be less evident in coming months. Only if that fails to happen will monetary policy normalisation be placed on hold.

Let me follow the example of our Lord and Master Alpha-Go as it takes the high ground first.

Let me, therefore, take the hyper-Olympian and very long run historical point of view.

The human brain is a massively parallel supercomputer that fits inside half a shoebox. It draws 50 watts of power. It is an amazing innovation, analysis, assessment and creation machine. 600 million years of proto-mammalian and mammalian evolution coupled with the genetic algorithm means that almost every single human can solve AI problems far beyond our current engineering reach—so much so that much of what our machines find impossible our brains find so trivially easy that we call such capabilities “unskilled”.

When combined with our brains, human fingers are amazingly fine manipulation devices.

Human back and leg muscles—especially when testosterone soaked—are quite good at moving heavy objects.

Thus back in the environment of evolutionary adaptation, we used our brains, our big muscles, and our fingers to lead cognitively interesting if stressful and short lives.

But history has rolled forward since the hunter-gatherer age. And as history has rolled forward, we have figured out other things to do to add economic and sociological value than their uses in the hunger-gathers paradigm. Over the long historical sweep, the ability to add value using our backs to move heavy objects and our fingers to perform fine manipulations in cognitively-interesting ways has, relatively, declined. We have, so far:

turned many of us into robots ourselves, performing simple routinized repetitive and vastly boring tasks to fill in the gaps in value chains between the robots that we know how to build.

found jobs as microcontrollers for domesticated animals and machines—the horse does not know what plowing the furrow is.

found jobs as relatively simple accounting and software bots, keeping track of stuff, what it is useful for, and how its use is to be decided.

become personal servitors.

become social engineers—trying to keep all those things and all those people—especially, perhaps, trying to keep those brains soaked in testosterone—somehow working in harmony, somehow pulling together, although admittedly with limited success.

remained innovators, analyzers, assessors, and creators as well.

Backs started to go out with the domestication of the horse. Fingers began to go out with the invention of the spinning jenny. But humans-as-microcontrollers, humans-as-accounting-‘bots—paper shufflers—and humans-as-the-robots we cannot yet build—took up all the job slack. Every horse needs a microcontroller. And a human

brain was the only possible option. Even today, to a large amount every textile machine needs a human watching it at least part of the time. It doesn’t know when it’s gone wrong. It has no clue how to fix itself. It no more understands the idea of “fixing” any more than Alpha-Go understands that it is playing Go, and not just solving a problem of outputting a two-element vector in response to a 19 x 19 matrix of inputs with the additional structure that the output changes the matrix and that the possible matrices have a value-function structure.

Now, however, we can finally peer into a future in which the microcontrollers and the accounting bots are on their way out in a manner analogous to the backs and the fingers. Fortunately, this brings with it the forthcoming extinction of the the jobs that treat humans as simple robots: simple cogs in the machine that is Henry Ford’s River Rouge assembly line. Many occupations that vastly underutilize the massively parallel supercomputer that fits in half a shoebox are on the way out—and good: for those are not properly “human” jobs at all.

That leaves us with a future of work—not next year, and not next decade, but further out by some unknown time—in which humans’ jobs will be as:

personal servitors,

social engineers, and

innovators, analyzers, assessors’ nd creators.

And here we might well, someday, have a huge problem.

The market economy will amply fund AI research that replaces workers in capital intensive production processes by machines. Such industries have mammoth returns to scale. They thus tend to be characterized by large oligopolies. And so the firm that funds such labor-replacing research will capture with its own scale and in its own value chain a substantial part of the benefits of such R&D. But the market economy will to amply fund AI research that assists and amplifies workers in labor intensive production processes. Such tend to be small scale. The inventors and the innovators cannot capture even a small part of the benefit in their own production processes and value chains. And intellectual property is a very weak reed indeed to rely on to fix the problem—in fact, intellectual property is more likely to be the problem than the solution, cf. Nathan Myhrvold, and Intellectual Ventures.

That means that the combination of coming AI with a market economy will be absolute poison for equity and equitable growth. It will race ahead with the first: shedding workers in capital intensive production processes. Yet AI could be gold for equity: amplifying the capabilities of workers in labor intensive production processes would, as John Maynard Keynes once said, bring us vastly closer to economic El Dorado.

Utopia or dystopia? Heaven or hell? I turn that over to you. And by “you”, I definitely include our engineering dean Shankar Sastry. Because firms will not invest on a large scale in AI that amplifies the capabilities of labor in labor intensive industries, it will not happen unless some NGO does. How about an engineering school? How about an engineering school like an engineering school at a public university?

Since I get to go first, I will preemptively take the hyper-Olympian and very long-run historical point of view…

The human brain is a massively parallel supercomputer that fits in half a shoebox. It draws 50 W of power. 600 million years of proto- and mammalian evolution mean that almost every single human can solve AI problems that our machines cannot—what our machines find very hard or impossible, our brains find so trivially easy that we call such capabilities “unskilled”.

Human fingers are amazingly fine manipulation devices. Human back and leg muscles—especially when testosterone soaked—are quite good at moving heavy objects. And so, back in the environment of evolutionary adaptation, we used our brains, big muscles, and fingers to lead interesting, if stressful and short, lives.

But as history has enrolled we have done other things to add economic and sociological value than use our backs, our fingers, and our brains to innovate and create. Over the long historical sweep, backs and fingers have declined and we have turned many of us into, instead:

robots performing repetitive tasks,

microcontrollers for domesticated animals and machines,

relatively simple accounting and recording software bots,

personal servitors,

social engineers trying to keep all those things controlled by brains—especially by the testosterone soaked ones—working together harmoniously. With limited success.

while remaining innovators and creators.

Backs started to go out with the domestication of the horse. Fingers with the invention of the spinning jenny. Microcontrollers and accounting ‘bots, we can see, are now on the way out too. So, fortunately, are the jobs that treat humans as simple robots.

That leaves us with a future of work made up of:

personal servitors,

social engineers,

innovators and creators.

The market economy will fund AI that replaces workers in capital-intensive production processes. Such are large scale and oligopolistic: firms profit from R&D because they capture a significant portion of efficiencies in their value chains. There is no equivalent market force funding AI that assists and amplifies workers in labor-intensive production processes.

The first is poison for equity and inclusion. The second is gold.

That second is one thing this NGO institution that surrounds us would be good at doing, and needs to do.

Utopia or dystopia? Heaven or hell?

Over to you, James. And, in a broader sense, over to all of you—in the audience, and out there in Internet land.

Khadeeja Safdar: J.Crew’s Mickey Drexler Confesses: I Underestimated How Tech Would Upend Retail: “Retail legend didn’t understand how speed and price would drive internet shoppers; 10 quarters of falling sales…. Now, competitors with high-tech, data-driven supply chains can copy styles faster and move them into stores in a matter of weeks…” https://www.wsj.com/articles/j-crews-big-miss-how-technology-transformed-retail-1495636817

Harvard Class of 1982 35th Reunion :: Science Center B :: Saturday, May 27, 2018, 10:45-12:00 noon

Seth Lloyd, MIT: Moderator

Brad DeLong, U.C. Berkeley

Ivonne Garcia, Kenyon

Noel Michele Holbrook, Harvard

William Sakas, CUNY

Carol Steiker, Harvard

In the spring of our freshman year, then-young economics professor Richard Freeman came to Ec 10 to tell us that going to Harvard would not make us rich.

He was wrong.

Up until 1980 America was winning, and Richard Freeman expected it to keep on winning, the race between education and technology: Thus there were ample numbers of people to take the increasing number of jobs requiring formal education for first class performance. Thus the amount the market paid you extra for taking a college requiring rather than a high school requiring job was modest: 30% or so–not enough to make up for the income you would’ve earned, had you taken the tuition you would not have spent and the extra wages you would have made from working, and put them into some reasonable investment.

But after 1980 America began to lose the race between education and technology.

The expansion of American higher education slowed massively. Higher education for native-born males simply froze in its tracks. As a result, in the world in which we have worked for the past 35 years employers have been betting up the relative price of college graduates: Rather than making 30% more than our counterparts who went straight into the job market after high school did, we have on average received double.

The freezing and of the relative numbers of native born American males taking advantage of hire education as demand, supply, and heterogeneity components.

On the demand-side, states withdrew tuition subsidies. Public college ceased to be free. Those whose parents were not rich worried about their student loans: what if they didn’t succeed and finish and could not get one of those high paying jobs? How were they going to pay back their loans? Americans almost surely over worry about this. But people are who they are, and not who economic theory dictates they should rationally be.

On the supply side, states stopped building campuses. Getting the courses you wanted and needed at public universities became iffy: five or six years rather than four.

And on the heterogeneity side, our colleges are designed for those who take to print literacy and to Arabic mathematics like ducks to water–if you do not have that, or are not trained to have that, learning the way we are taught to teach becomes much more difficult. We economists see this every semester, as even Ec 10 requires great facility in reading, in arithmetic, in algebra, and in algebraic geometry. The extra slice of the population that we would have been sending to higher education in a better counterfactual world in which America had not lost the race between education and technology would have been less well prepared and less suited to benefit.

What is the balance between these supply, demand, and heterogeneity considerations? That, we say, is a research problem.

How important is all this? I would say that about 1/3 of the problem is with America that have developed over the past 35 years–1/3 of the ways in which I see America today falling far short of what I confidently helped America would be by now–are due to our losing the race between education and technology.

Let me make one final point: Over the past generation, Harvard has not helped. We had 1600 in our class. Last week’s graduating class was essentially the same size. Worldwide, between five and ten times as many people are well-qualified to join my niece as freshmen this fall. In our class there were perhaps four times as many people well-qualified to attend as Harvard admitted. Today there are between twenty and forty. Yet Presidents Bok, Pusey, and Rudenstine seemed to have little interest in helping America and the world in the race between education and technology. Contrast that with the University of California, which, under Chancellor and President Clark Kerr and California Governor Pat Brown, set in motion the plan to clone itself across the state and increase enrollment tenfold.

If you are thinking about giving money to help America win this race with education and technology, I would not recommend Harvard. U.C. Berkeley, Columbia, and MIT for moving people whose parents’ were in the bottom quintile into the top 1%. And for overall bottom fifth to top fifth mobility? CUNY. U.T.-Pan American. TCI. SUNY Stonybrook. Pace. and Cal State-LA. That is what Yagan, Turner, Saez, Friedman, and Chetty say… http://www.equality-of-opportunity.org/papers/coll_mrc_paper.pdf.

Paul Krugman: Trade and Tribulation and A Protectionist Moment?: “Protectionists almost always exaggerate the adverse effects of trade liberalization…

…Globalization is only one of several factors behind rising income inequality, and trade agreements are, in turn, only one factor in globalization. Trade deficits have been an important cause of the decline in U.S. manufacturing employment since 2000, but that decline began much earlier. And even our trade deficits are mainly a result of factors other than trade policy, like a strong dollar buoyed by global capital looking for a safe haven.

And yes, Mr. Sanders is demagoguing the issue…. If Sanders were to make it to the White House, he would find it very hard to do anything much about globalization…. The moment he looked into actually tearing up existing trade agreements the diplomatic, foreign-policy costs would be overwhelmingly obvious. In this, as in many other things, Sanders currently benefits from the luxury of irresponsibility….

But on the other hand:

That said… the elite case for ever-freer trade, the one that the public hears, is largely a scam…. [The] claims [are] that trade is an engine of job creation, that trade agreements will have big payoffs in terms of economic growth and that they are good for everyone. Yet… the models… used by real experts say… agreements that lead to more trade neither create nor destroy jobs… make countries more efficient and richer, but that the numbers aren’t huge….

False claims of inevitability, scare tactics (protectionism causes depressions!), vastly exaggerated claims for the benefits of trade liberalization and the costs of protection, hand-waving away the large distributional effects that are what standard models actually predict…. A back-of-the-envelope on the gains from hyperglobalization — only part of which can be attributed to policy — that is less than 5 percent of world GDP over a generation…. Furthermore, as Mark Kleiman sagely observes, the conventional case for trade liberalization relies on the assertion that the government could redistribute income to ensure that everyone wins—but we now have an ideology utterly opposed to such redistribution in full control of one party…. So the elite case for ever-freer trade is largely a scam, which voters probably sense even if they don’t know exactly what form it’s taking….

And, Paul summing up:

Why, then, did we ever pursue these agreements?… Foreign policy: Global trade agreements from the 1940s to the 1980s were used to bind democratic nations together during the Cold War, Nafta was used to reward and encourage Mexican reformers, and so on. And anyone ragging on about those past deals, like Mr. Trump or Mr. Sanders, should be asked what, exactly, he proposes doing now.… The most a progressive can responsibly call for, I’d argue, is a standstill on further deals, or at least a presumption that proposed deals are guilty unless proved innocent.

The hard question to deal with here is the Trans-Pacific Partnership…. I consider myself a soft opponent: It’s not the devil’s work, but I really wish President Obama hadn’t gone there…. Politicians should be honest and realistic about trade, rather than taking cheap shots. Striking poses is easy; figuring out what we can and should do is a lot harder. But you know, that’s a would-be president’s job…. [But] he case for more trade agreements—including TPP, which hasn’t happened yet—is very, very weak. And if a progressive makes it to the White House, she should devote no political capital whatsoever to such things.

So I guess it is time to say “I think Paul Krugman is wrong here!” and fly my neoliberal freak flag high…

On the analytics, the standard HOV models do indeed produce gains from trade by sorting production in countries to the industries in which they have comparative advantages. That leads to very large shifts in incomes toward those who owned the factors of production used intensively in the industries of comparative advantage: Big winners and big losers within a nation, with relatively small net gains.

But the map is not the territory.

The model is not the reality.

An older increasing-returns tradition sees productivity depend on the division of labor, the division of labor depends on the extent of the market, and free-trade greatly widens the market. Such factors can plausibly quadruple the net gains from trade over those from HOV models alone, and so create many more winners.

Moreover, looking around the world we see a world in which income differentials across high civilizations were twofold three centuries ago and are tenfold today. The biggest factor in global economics behind the some twentyfold or more explosion of Global North productivity over the past three centuries has been the failure of the rest of the globe to keep pace with the Global North.

And what are the best ways to diffuse Global North technology to the rest of the world?

Free trade: both to maximize economic contact and opportunities for learning and imitation, and to make possible the export-led growth and industrialization strategy that is the royal and indeed the only reliable road to anything like convergence.

So I figure that, all in all, not 5% but more like 30% of net global prosperity—and considerable reduction in cross-national inequality—is due to globalization. That is a very big number indeed. But, remember, even the 5% number cited by Krugman is a big number and a deal: $4 trillion a year, and perhaps $130 trillion in present value.

As for the TPP, the real trade liberalization parts are small net gains. The economic question is whether the dispute-resolution and intellectual-property protection pieces are net gains. And on that issue I am agnostic leaning negative. The political question is: Since this is a Republican priority, why is Obama supporting it without requiring Republican support for a sensible Democratic priority as a quid pro quo?

That said, let me wholeheartedly endorse what Paul (and Mark) say here:

As Mark Kleiman sagely observes, the conventional case for trade liberalization relies on the assertion that the government could redistribute income to ensure that everyone wins—but we now have an ideology utterly opposed to such redistribution in full control of one party…. So the elite case for ever-freer trade is largely a scam, which voters probably sense even if they don’t know exactly what form it’s taking…

This is a weekly post we publish on Fridays with links to articles that touch on economic inequality and growth. The first section is a round-up of what Equitable Growth published this week and the second is the work we’re highlighting from elsewhere. We won’t be the first to share these articles, but we hope by taking a look back at the whole week, we can put them in context.

Equitable Growth round-up

It’s all about the President’s budget this week. Well, almost.

Anticipating the Trump administration’s fiscal year 2018 budget, Greg Leiserson discusses the possibility of double-counting of the benefits of improving the outlook for the federal deficit thanks to fantasy budgeting around policies and plans that have yet to be developed.

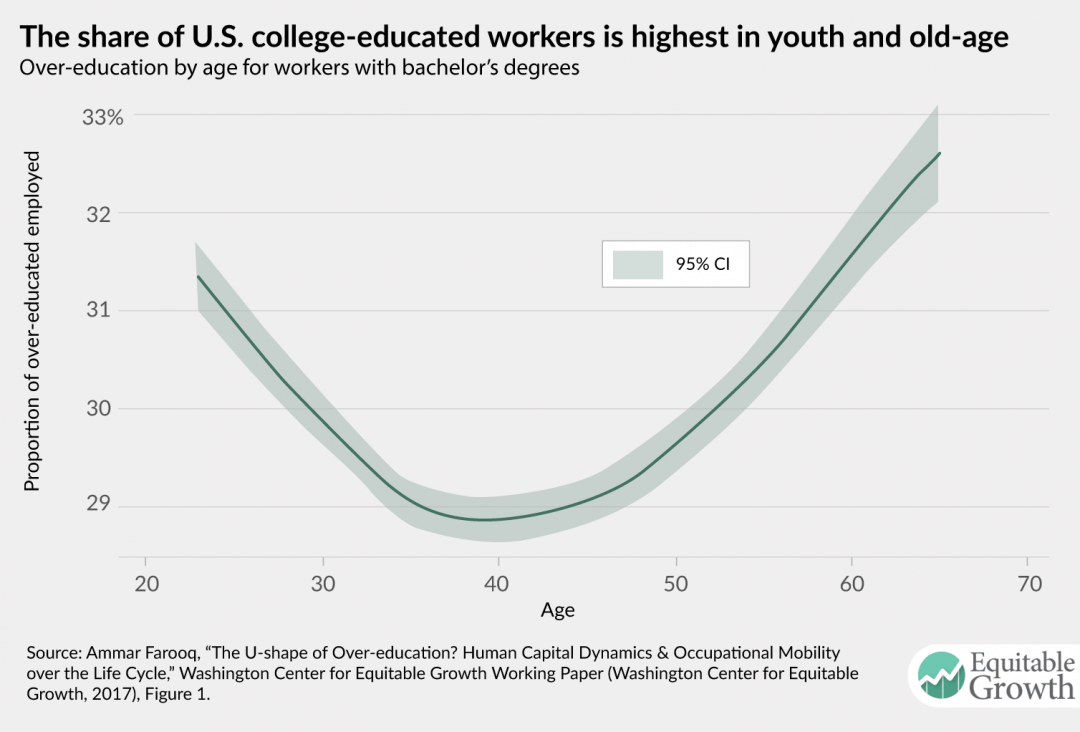

Equitable Growth released a new working paper by grantee Ammar Farooq, which takes a close look at the proportion of college-educated workers in occupations that don’t require a college degree. The findings suggest that the share of over-educated workers appears to be U-shaped over the life cycle.

Nick Bunker also writes on the incidence of over-education across a lifetime, noting that Farooq’s paper helps shed light on the fact that the “cruel game of musical chairs” is not just a problem for young people but also for the middle-aged and the elderly.

Getting back to the budget, concerns over enforcing labor standards and worker protections are on the rise as the Trump administration proposed large cuts to the U.S. Department of Labor. Recent structural changes in the labor market—including the rise of the “fissured” workplace, the decline of union density, the lack of synergy between regulatory frameworks and industrial organization, and the rapid growth of technology—make enforcement even more important in this day and age, explains Elisabeth Jacobs.

In the latest installment of Equitable Growth in Conversation, John Schmitt sits down with Sandra Black, the Audre and Bernard Rapoport Centennial Chair in Economics and Public Affairs, professor of economics at The University of Texas at Austin, and former member of President Barack Obama’s Council of Economic Advisors, to talk about transitioning from academia to the policy world and the importance of bridging the gap between the two. Read the full interview transcript here.

The fiscal year 2018 budget put forward a 13 percent spending cut for the U.S. Department of Education and redirecting funding efforts toward school choice. Despite this focus on school choice, the administration has not yet unveiled their tax credit scholar program. Kavya Vaghul unpacks some of the key controversies with these programs.

Links from around the web

Dylan Matthews breaks down the details of the trillions of dollars of cuts in President Donald Trump’s tax plan, calls out the “magical economic assumptions” in the plan, and predicts the possibility of these changes actually taking effect. [vox]

Why has wage growth stagnated over the last three decades? Pedro Nicolaci da Costa explores the question, reflecting on the weak state of the labor market and how investments in workers and wages are low. [business insider]

The American Health Care Act was scored by the U.S. Congressional Budget Office. According to the report, the House-passed legislation would reduce the deficit but render 23 million more people uninsured. Additionally, the CBO score makes clear that the American Health Care Act will help underwrite tax cuts, explains Casey Quinlan. [think progress]

“Inclusive prosperity” in the United States has become increasingly unattainable, writes Richard Florida, though unemployment has decreased and economic output has increased since the Great Recession of 2007-2009. These gains appear to be accruing to certain advantaged groups across race and class in metro areas. [city lab]

In a new report, Lawrence Mishel and Josh Bivens strike down on the argument that increasing automation—the robot apocalypse—leads to inequality and job displacement by reviewing key literature and refocusing attention to the importance of securing full employment. [epi]

Must-Read: This first part reads as though Ben Bernanke is not talking just about the Bank of Japan, but rather about the Federal Reserve as well—or perhaps more about the Federal Reserve. The argument against a 4%/year inflation target—or a price level-path target with catchup—is that there is value in keeping inflation too low to be salient in people’s decisions. But that benefit is uncertain and speculative. The costs of being unable to use monetary policy to offset a negative demand shock are very concrete and real, and very dire indeed:

…Getting inflation and interest rates higher will promote economic stability by increasing the BOJ’s ability to respond to future recessions…. Kuroda’s program of “qualitative and quantitative easing” has had important benefits, including higher inflation and nominal GDP growth and tighter labor markets. Recent changes to the BOJ’s framework will make it more sustainable….

What tools remain if current policies are not enough? The scope for significant further easing by Japanese monetary authorities on their own seems limited, as interest rates are near zero for government bonds even at long maturities and raising inflation expectations—a way to lower real interest rates—has proved difficult. If more stimulus is needed, the most promising direction would be through fiscal and monetary cooperation, in which the BOJ agrees to temporarily raise its inflation target as needed to offset the effects of new fiscal spending or tax cuts on the debt-to-GDP ratio…

…scuppering Gladstone’s attempts to keep the UK together by granting home rule to Ireland… his imperialist vision of a Greater Britain proved to be a fantasy… “imperial preference”….

It fell to Joe’s son, Neville, finally to implement imperial preference in 1932. The policy was of course a failure, contributing to the general contraction of world trade in the 1930s. It was swept away by the move towards multilateral agreements after the second world war. Henry Campbell-Bannerman, Liberal prime minister between 1905 and 1908, and JM Keynes probably provide the most fitting epitaphs to Chamberlain’s career. The former said of him that he used “the foolishness of the fool and the vices of the vicious to overwhelm the sane and wise and sober”. The latter described him as a “fanatical charlatan”. It is a wonder that such a man can continue to have any influence today.

President Donald Trump’s budget for fiscal year 2018 beginning October 1 and released this past Tuesday contains some potentially bad news for the state of education in the United States. Under the guise of “refocusing” funding priorities, the budget proposes a 13 percent, or $9 billion, cut for the Department of Education. On the chopping block are programs such as public service student loan forgiveness,Supporting Effective Instruction State Grants, and 21st Century Community Learning Centers. Despite these, and other, rollbacks on spending for Kindergarten through 12th grade and higher education, the budget did reflect the Trump administration’s misplaced commitment to advancing one aspect of education—school choice—using mechanisms such as vouchers to help students access schools that best suit their needs.

A more detailedstatement released by the Department of Education reveals that approximately $1.4 billion in the education budget will be directed toward expanding investments in public and private school choice options. This includes $1 billion for Furthering Options for Children to Unlock Success grants, which allow students in high-poverty schools to choose to attend other public schools and take their voucher with them. Additionally, it calls for a $250 million increase for programs that award scholarships for low-income children to attend private school and a $167 million increase to expand state efforts on charter schools.

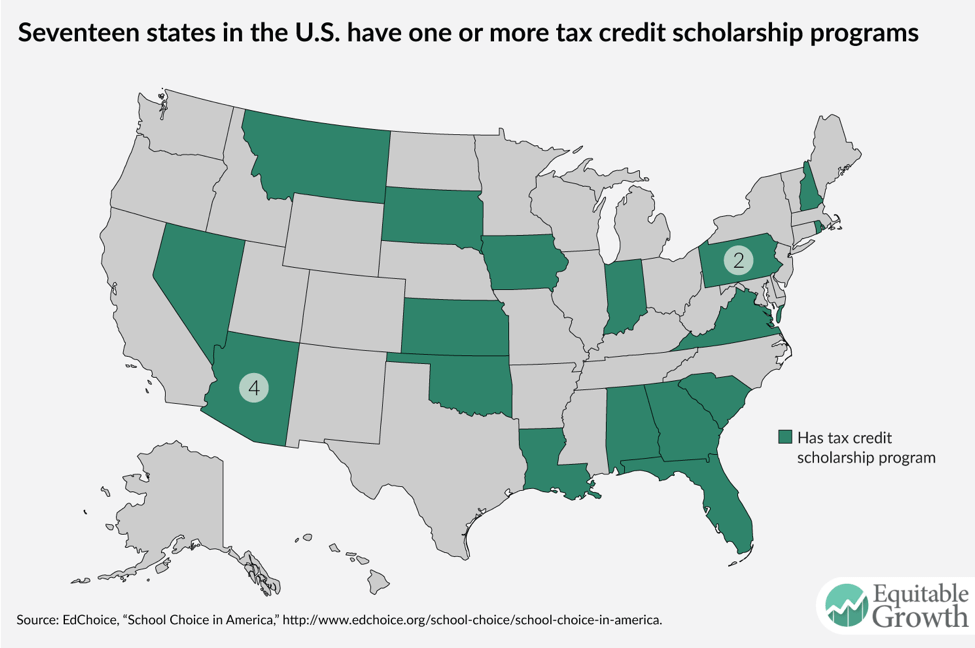

All this said, the Department of Education’s detailed budget leaves out much-anticipated information about the administration’s controversial school choice program—tax credit scholarships. In general, tax credit scholarships, sometimes called “neovouchers,” work by giving individuals, businesses, or both partial to full tax credits for their donations to nonprofit organizations that offer scholarships to private and religious primary and secondary schools. Currently, 17 states operate one or more tax credit scholarship programs, with roughly 250,000 enrollees nationwide. In some states, such as Indiana and Oklahoma, tax credits are slated at 50 cents on the donated dollar, but in several others, such as Alabama, Arizona, Florida, Georgia, Montana, Nevada, and South Carolina, taxpayers can receive up to dollar for dollar tax credits. (See Figure 1.)

Figure 1

While in theory using tax credit scholarships can increase K-through-12 school choice, there are two key problems with these programs.

The most egregious problem, as a matter of tax policy, with tax credit scholarships is that in some states, taypayers can turn a profit on them through a loophole. According to a new report by Carl Davis of the Institute on Taxation and Economic Policy, in the states in which credits equal a dollar on the dollar donated, donors not only get the tax credit but also can claim the charitable federal tax deduction. As a result of this double-dipping, individuals may actually realize a profit on their donation.

The more fundamental problem is that there isn’t much evidence that school choice programs, specifically vouchers, have substantial positive effects on the students they are meant to serve. A review of the literature in 2011 by researchers at the Center on Education Policy at The George Washington University found that school vouchers had no concrete positive impact on students’ educational achievement. A more recent study of the Louisiana Scholarship Program—a voucher program that provides publicly financed scholarships for K-through-12 students to go to private schools—even found negative effects. Scholarship recipients who were performing at the median level prior to entering the program were 13 percentile points lower than their non-scholarship counterparts after two years in the program.

Given these concerns, the Trump administration and the Department of Education should reconsider (or flat-out ditch) their yet-to-be unveiled tax credit scholarship program. But beyond tax credit scholarships and supporting school choice, investing in programs that more reliably shrink educational achievement gaps and improve the quality of publicly funded education can best promote more equitable outcomes for all students.