This is a weekly post we publish on Fridays with links to articles that touch on economic inequality and growth. The first section is a round-up of what Equitable Growth published this week and the second is the work we’re highlighting from elsewhere. We won’t be the first to share these articles, but we hope by taking a look back at the whole week, we can put them in context.

Equitable Growth round-up

Some critics of the disability insurance system in the United States think it is too easy to access. They argue that if the cost of applying for disability goes up, then the people who don’t really need disability coverage will be the ones to not apply. New research finds, in fact, the opposite happens.

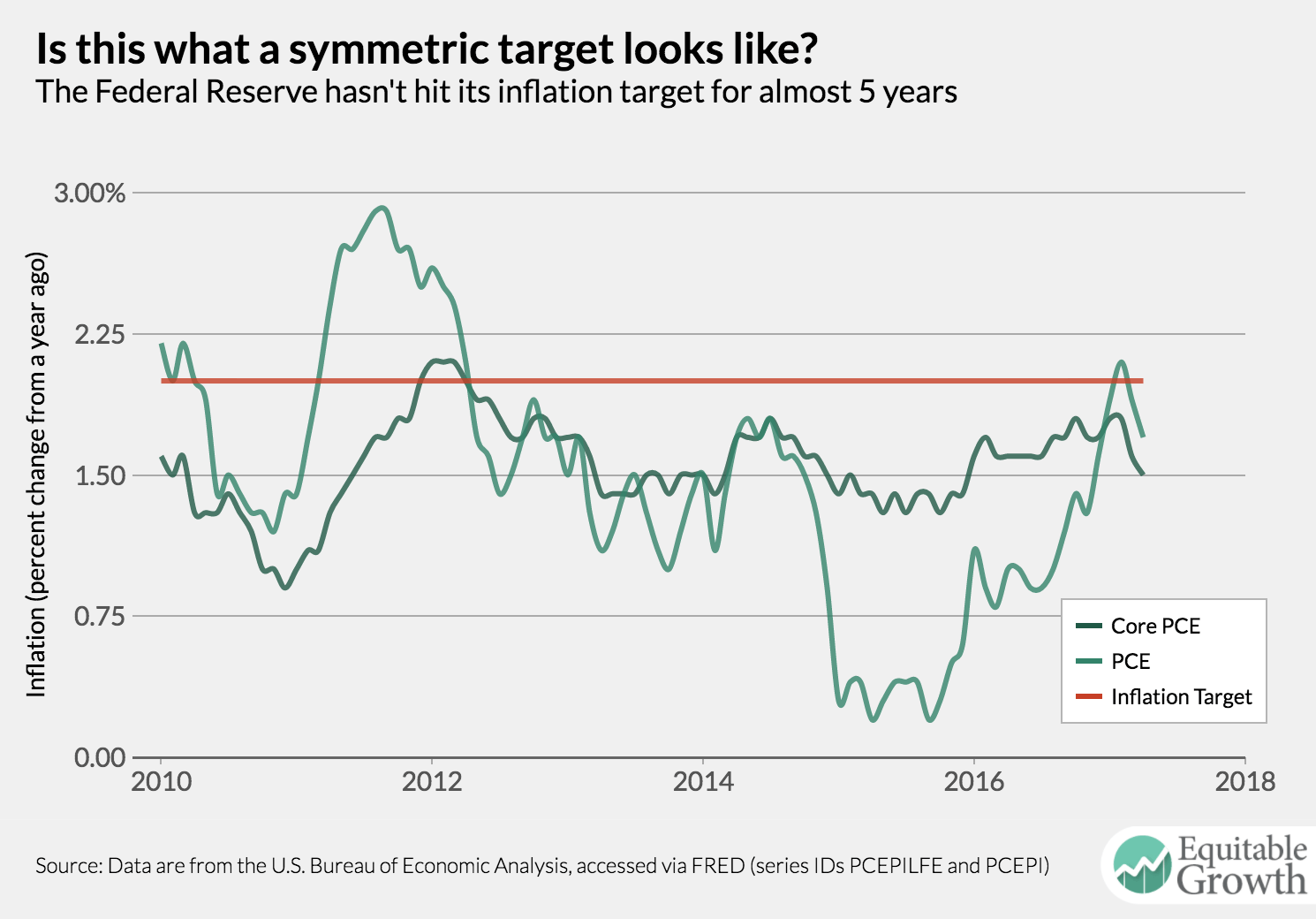

The Federal Reserve raised interest rates on Wednesday afternoon despite data showing a weakening in inflation. Given that inflation has been below 2 percent for almost five years, perhaps it’s time to rethink the current targeting regime.

Seventeen percent of workers in the United States have unpredictable, variable schedules as the result of “lean labor strategies.” The effects of these kind of schedules are just now starting to be understood. Bridget Ansel rounds up some research in this area.

The Kansas supply-side tax cut experiment failed. Understanding why it failed is important given that the same model underlies the proposed tax reform of the Trump administration. Greg Leiserson runs through the flaws in the line of thinking bedind the Kansas experiment.

A tax deduction for migrating birds? Kavya Vaghul shows how conservation easements have been exploited and turned into another inequitable feature of the U.S. tax system.

Links from around the web

The number of job openings as a share of total employment is near historic highs. The time it takes to fill an open job is also quite high. Is this a sign of a major skill-gap in the labor market? Noam Scheiber talks to a number of researchers and they all don’t think that’s the case. [nyt]

Over the courses of the current U.S. economic recovery, the Federal Reserve has continuously underestimated how much lower the unemployment rate can go. Cardiff Garcia floats the idea that this discounting of how much the labor market can heal is behind its “continued failure to produce an economy that sustainably keeps inflation near the target, and which includes healthier wage growth.” [ft alphaville]

“It is not just that tax cuts didn’t achieve their purpose,” writes Max Ehrenfreund. “New research suggests that the cuts were, in fact, counterproductive.” Here’s his look at new research on the Kansas tax cuts. [wonkblog]

“Today’s inconspicuous consumption is a far more pernicious form of status spending than the conspicuous consumption of Veblen’s time,” argues Elizabeth Currid-Halkett. She finds that spending by elites is now less about demonstrating financial capital and more about showing off cultural capital than in the Robber Baron era. [aeon]

The effects of a losing your job might have an effect on you for the rest of your life, but also on your community and the young people who live there. Alana Semuels writes about new research connecting widespread layoffs in a community to lower rates of college attendance rates for low-income children. [the atlantic]

Friday figure

Figure from “Time for the Fed to look beyond 2 percent target inflation?” by Nick Bunker