Only a hint of new thinking at Jackson Hole

This past weekend, economists and central bankers gathered in Jackson Hole, Wyoming for an annual conference hosted by the Kansas City Federal Reserve Bank. The conference is a combination of an academic forum with authors presenting papers and a place where the Federal Reserve chair can lay out thinking behind U.S. monetary policy. This year, the symposium was surrounded by a bit of hype. Its title, “Designing Resilient Monetary Policy Frameworks for the Future,” along with a recent paper by San Francisco Federal Reserve Bank President John Williams on rethinking monetary policy in a world of low interest rates, had some observers believing that the discussion in Wyoming might be the very beginning in a rethink of monetary policy.

That did not happen as envisioned. Federal Reserve chair Janet Yellen’s speech on Friday morning instead pointed toward a view within the Federal Reserve that the current monetary policy path is adequate to prepare for the next recession. With the federal funds rate still only at 0.25 percent, many observers fear that the central bank won’t have enough room to cut interest rates the next time the economy hits a downturn. Yellen, however, argues that the key interest rate is on pace to get to 3 percentage points, enough space to cut rates before the next time the central bank has to cut rates.

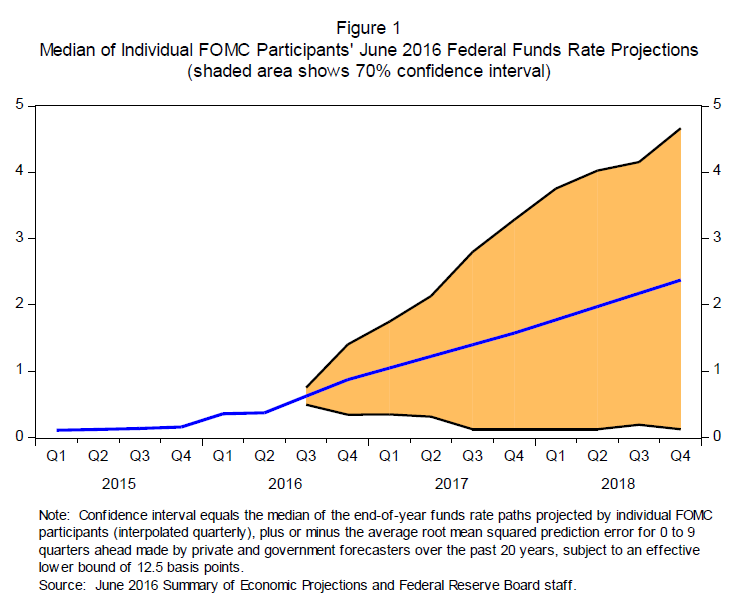

But getting to 3 percent might not be so easy. As a chart from Yellen’s presentation shows, the future path of short-term interest rates, based on the projections of Federal Open Market Committee participants, is incredibly uncertain. Given the uncertainty of the world, short-term rates might be at about 4.5 percent by the end of 2018, but they could still be sitting at 0.25 percent or somewhere in between those two levels.

{kind=link}

Secondly, as Jared Bernstein points out, the financial markets don’t seem to believe the Federal Open Market Committee-implied path of interest rates. The markets are signaling that they think that rates will end up being much lower that 3 percent. Given that the FOMC has, as Larry Summers notes, consistently pushed down its estimates of the level of interest rates, the markets might be forgiven for thinking the federal funds rate won’t get to 3 percent.

Finally, it’s not clear that 3 percent is the correct resting place for the Fed’s benchmark rate. Several estimates of the natural rate of interest put it lower than 3 percent, with some people saying it’s at zero percent. If long-run inflation is 2 percent, this means the Federal Reserve should try to get nominal interest rates to 2 percent. So if those estimates are correct, the Fed can’t get to 3 percent without pushing the economy into a recession. But even if the Fed can’t cut from 3 percent, it still has quantitative easing—a program of purchasing longer-term assets—in its back pocket.

How many long-term assets would the Federal Reserve need to buy in the market in order to stimulate the economy with interest rates starting lower than they were in late 2007 at beginning of the Great Recession? Perhaps, as Yellen notes, the central bank could expand the kind of assets it purchases to include corporate bonds, stocks, real estate investment trusts or foreign currency as other central banks have. She also remarked that “some observers” have contemplated a higher inflation target or targeting the price level or the level of income growth. While it seems unlikely anytime soon, some observers hope Yellen and others are at the Federal Reserve will join in that contemplation.