Inflation, Federal Reserve policymaking, and liquidity traps

Fighting inflation in a liquidity trap is difficult, but with inflation cooling, the gains from doing it right are becoming harder to ignore

The Federal Reserve is fighting inflation, but more importantly, the Fed wants everyone to know that it is fighting inflationary expectations. This means, in the short term, that with inflation seemingly trending lower but not as fast as the Fed wants it to, interest rates are likely to go significantly higher until indications of the persistence of inflation abate further. The recent turmoil in U.S. regional bank stocks after the failure of Silicon Valley Bank and Signature Bank will complicate the Fed’s decision-making, but the federal government’s rescue of the two banks’ depositors is unlikely to upend its medium-term effort to quell inflationary expectations.

That’s why it’s worth stepping back to revisit a longer-term driver of inflation in the current economic recovery, both mechanically and through policy responses: the lost decade of U.S. economic growth and investment that followed the Great Recession of 2007–2009. Simply put, fighting recessions and inflation is more complicated and riskier when an economy starts in a liquidity trap—that is, when inflation and interest rates are too low such that investment is disincentivized.

In addition to the typical risk that too much support for a faltering economy can trigger temporary inflation, there is the far greater risk that too timid a response can deepen economic decline and permanently shrink the economy. That was still the situation when the recovery from the COVD-19 recession began less than 3 years ago.

This relatively recent surge in inflation, the Fed’s policymaking in reaction to that surge, and the yield curve inversions that the U.S. financial markets have experienced recently all reflect the challenges of making sound fiscal and monetary policy responses amid that liquidity trap. The Fed is well aware that it does not understand all the precise causes of inflation today, but the decades-long low-growth, low-inflation economic environment that preceded today’s inflationary pressures strongly caution against excessively strident monetary and fiscal policy that risks pushing the economy back toward a liquidity trap—a far worse outcome than today’s inflation.

To be sure, the Fed, the Biden and Trump administrations, corporations, workers, and the U.S. Congress have all received some blame for the initial surge in inflation and some continuing inflationary pressures. And more precisely calibrated monetary and fiscal policies and more competitive markets may have reduced the inflationary surge, as several recent studies suggest.

Yet the focus on these more immediate real-time culprits for inflation is overly simplistic. To understand why, let’s step back to early 2022, when the Fed’s monetary policy was not maximally anti-inflation and should not have been—and not just due to the short-term supply shocks caused by the start of the war in Ukraine early that year. The U.S. economy was still being lashed by the COVID-19 pandemic that began in 2020 amid a long-persistent liquidity trap. Since the so-called dot-com recession ended in 2001, the federal funds rate has been below 1 percent more often than it has been above it, and below 2 percent more than three-quarters of the time. Engineering an economic recovery in a liquidity trap is difficult because it requires more aggressive monetary and fiscal policies to spark strong and sustained economic growth.

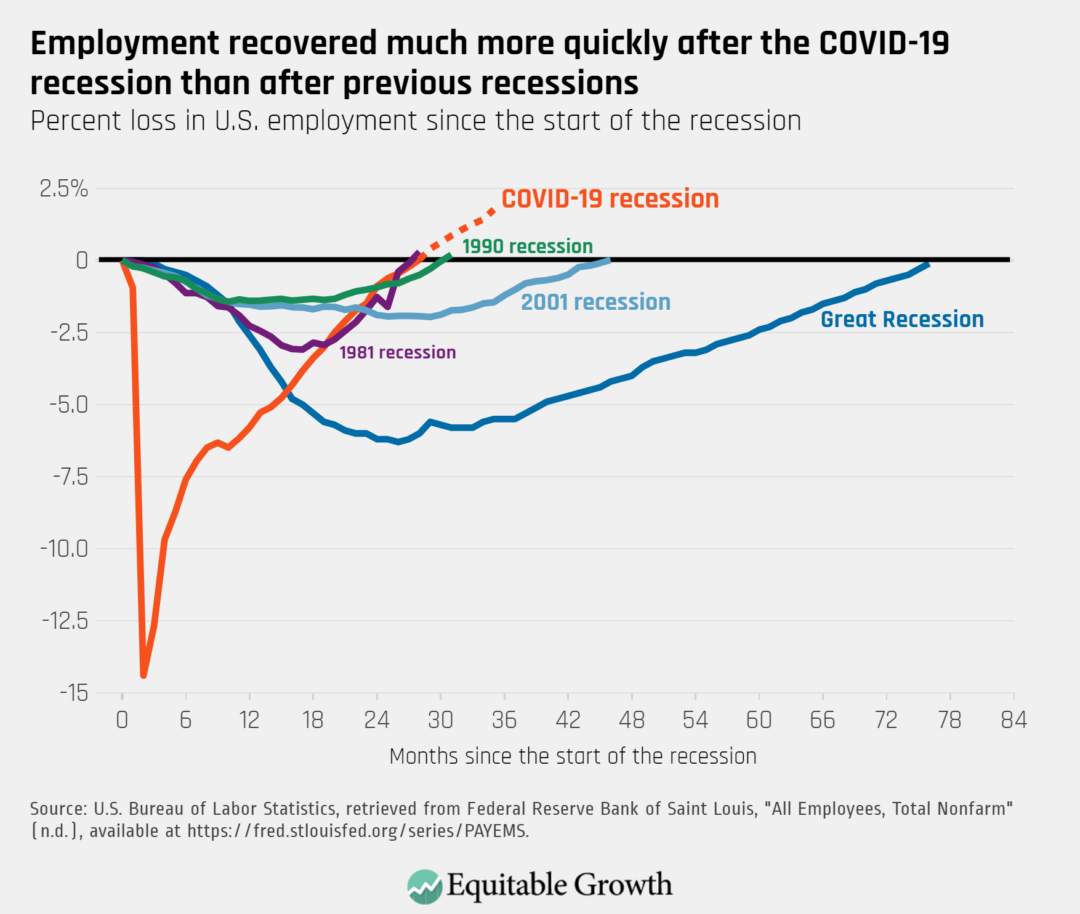

Fast-forward to the fiscal and monetary policy responses to the COVID-19 recession. The aggressive fiscal policy and (at the very least the de facto) lower-for-longer monetary policy the Fed pursued in 2020 and 2021 were precisely the prescriptions of macroeconomics for this condition. None of these policy choices was a mystery. Policymakers and Fed officials repeatedly stated that the goal, well into the recovery, was to err on the side of being too aggressive to avoid choking off growth or causing a deflationary recession. The result is the strongest jobs recovery the U.S. economy has experienced in 40 years. (See Figure 1.)

Figure 1

This approach contrasts sharply with the fiscal and monetary policies pursued after the end of the dot-com recession and the Great Recession—periods characterized as “jobless” economic recoveries, where more timid responses brought very low inflation but at the cost of a permanently smaller economy, weak job growth, and increased income and wealth inequality. The weak recoveries deepened the U.S. economy’s decline into secular stagnation—slow growth and underinvestment during economic expansions.

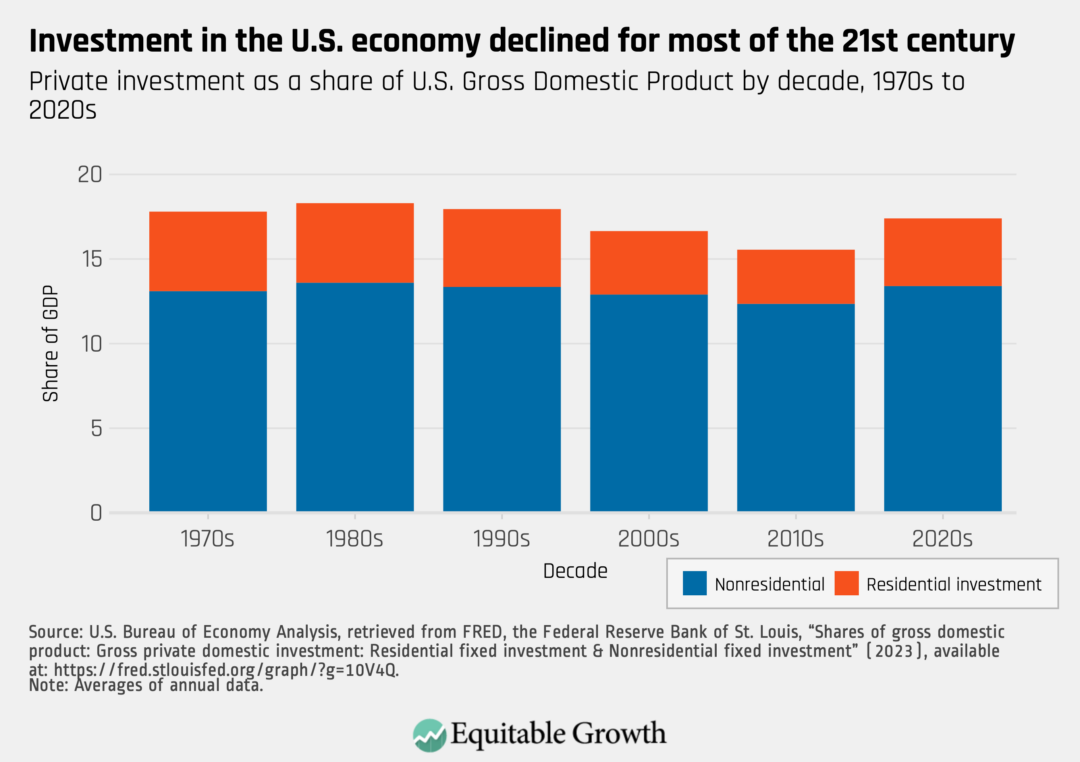

Escapes from liquidity traps are rare—just look at how Japan has struggled for nearly a half-century in its liquidity trap—and returning the U.S. economy to a sustained healthier growth trajectory is a resource strain, and not only due to short-term factors. Two decades of underinvestment in the 21st century meant capacity constraints may have generated price inflation longer than they should for a healthy recovery economy. This investment decline is readily apparent in private-sector investment data overall. (See Figure 2.)

Figure 2

U.S. private investment in the 2010s was just 15.5 percent of Gross Domestic Product, compared to around 18 percent of GDP for the last 3 decades of the 20th century. The well-publicized nature of the home mortgage crisis that sparked the Great Recession makes residential investment an obvious culprit, but nonresidential investment as a share of GDP fell a full percentage point from the pre-2000 levels on top of that. Taken together, this underinvestment can have significant effects on the supply side of the economy—even when this is a downstream effect.

A 20-year trend such as this is not the kind of short-term supply shock that monetary policymakers can ignore. Indeed, this is the result of the very secular stagnation that economists such as Olivier Blanchard at the Peterson Institute for International Economics and Larry Summers at Harvard University have been raising alarms about for much of this time.

The robust U.S. economic recovery today, even amid inflation, is unambiguously better for the United States than a weaker recovery with lower inflation. This is one reason why the nonpartisan Congressional Budget Office’s projected 2030 GDP is stronger now than its pre-pandemic projections, when the CBO anticipated shrinking economic growth for years after the previous recovery beginning in 2009.

Inflation is going to remain a major concern, but the record on inflation so far does not point to a dire future. Inflation has been much higher than forecast over the past year, owing to both demand- and supply-side factors. Yet expected inflation has remained well-anchored, suggesting that policy has finally overcome the liquidity-trap challenge of committing to being irresponsible, while maintaining long-term price stability. This is not a reason for complacency, but a clear signal that markets’ longer-term expectations are that the Fed will, perhaps more slowly than it wants, bring inflation back toward its target of 2 percent.

There are two major macroeconomic questions for economic policy over the next year—one a challenge and one an opportunity. The challenge is well-understood: With inflation having peaked and now poised to decline for multiple reasons, the Fed must balance patience with credibility in its pursuit of its 2 percent target. If it is far too patient, then inflationary expectations could increase significantly, but if it is too impatient, it could damage the economy.

The more interesting, more exciting question is whether the higher rates that the Fed is imposing on the U.S. economy now are a sign that the era of secular stagnation is over. This is a speculative question without a simple answer yet. Why? Well, if the higher rates that Fed officials are contemplating prove excessive, then that would strengthen the chances of a return to secular stagnation. But if the Fed’s long-term rate targets, known as neutral rates, can rise as much as some are discussing—much higher than the less than 3 percent levels that the Fed’s median projection has not exceeded since mid-2014—then that suggests the economic successes of this decade may also include an escape from secular stagnation.

Now that is a singular opportunity, given recent U.S. economic history.