How tight is the U.S. labor market? And how tight do we want it?

Is the U.S. labor market at “full employment”? This question may seem open and shut with the unemployment rate at 4.6 percent, according to the latest Employment Situation report. But some other data show some slack remaining in the labor market, including the employment rate for prime-age workers and wage growth that, while increasing, still has some room to grow. Data released this morning as part of the Job Openings and Labor Turnover Survey might be helpful not only when looking at the health of the labor market, but also predicting when policymakers will decide that the labor market hits “full employment.”

{kind=link}

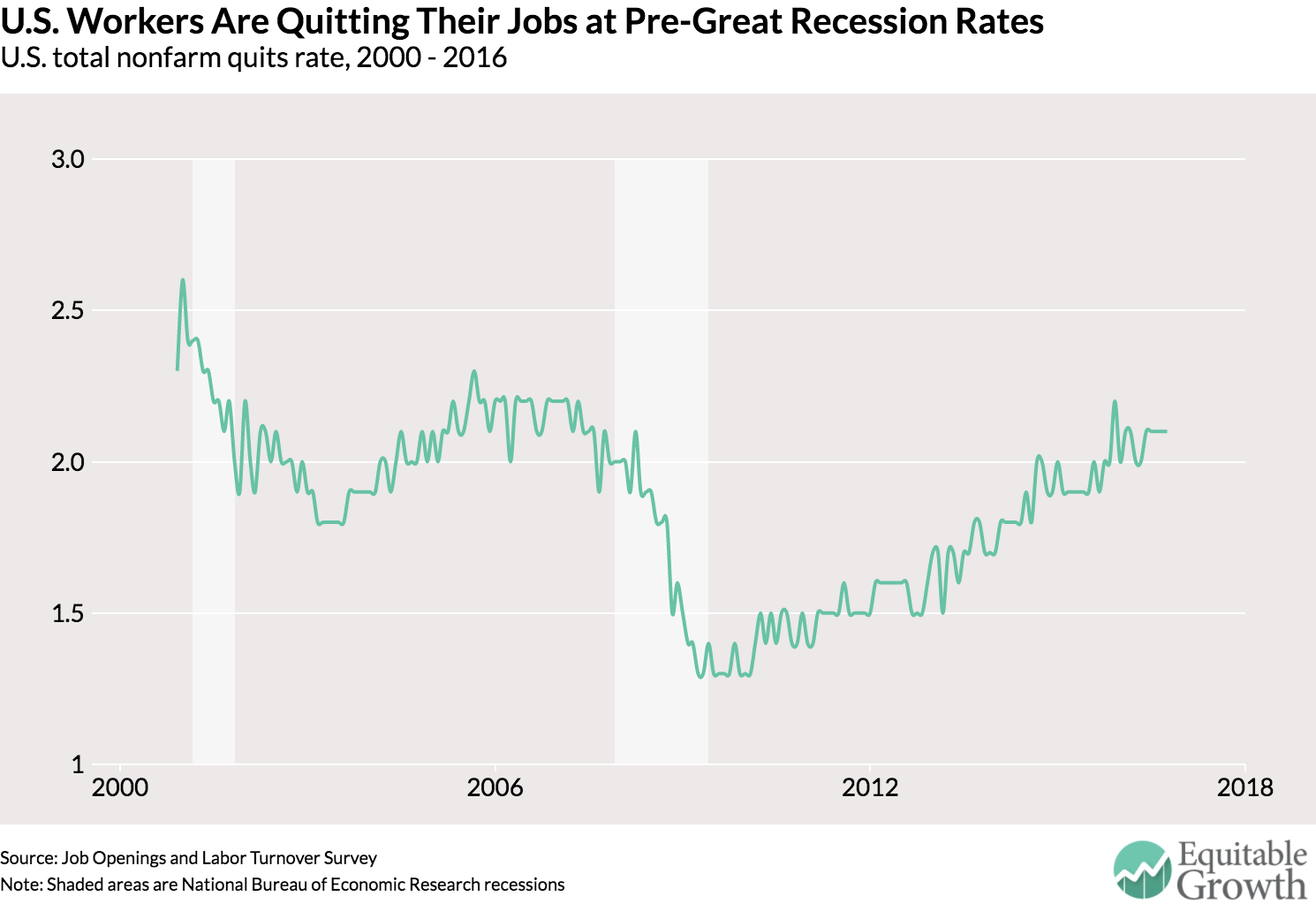

The rate at which workers quit their jobs is a good window into the health of the labor market. Quitting is a sign of worker confidence in their ability to find a new job. Workers will be more likely to quit when they see the labor market improving. Higher rates of quitting also are a sign that companies see the labor market tightening and are poaching more workers from other firms. As today’s Job Openings and Labor Turnover Survey shows, the quits rate is close to pre-recession levels, but data that cover a longer time than JOLTS show the current rates far below levels seen in the 1990s. (See Figure 1.)

Figure 1

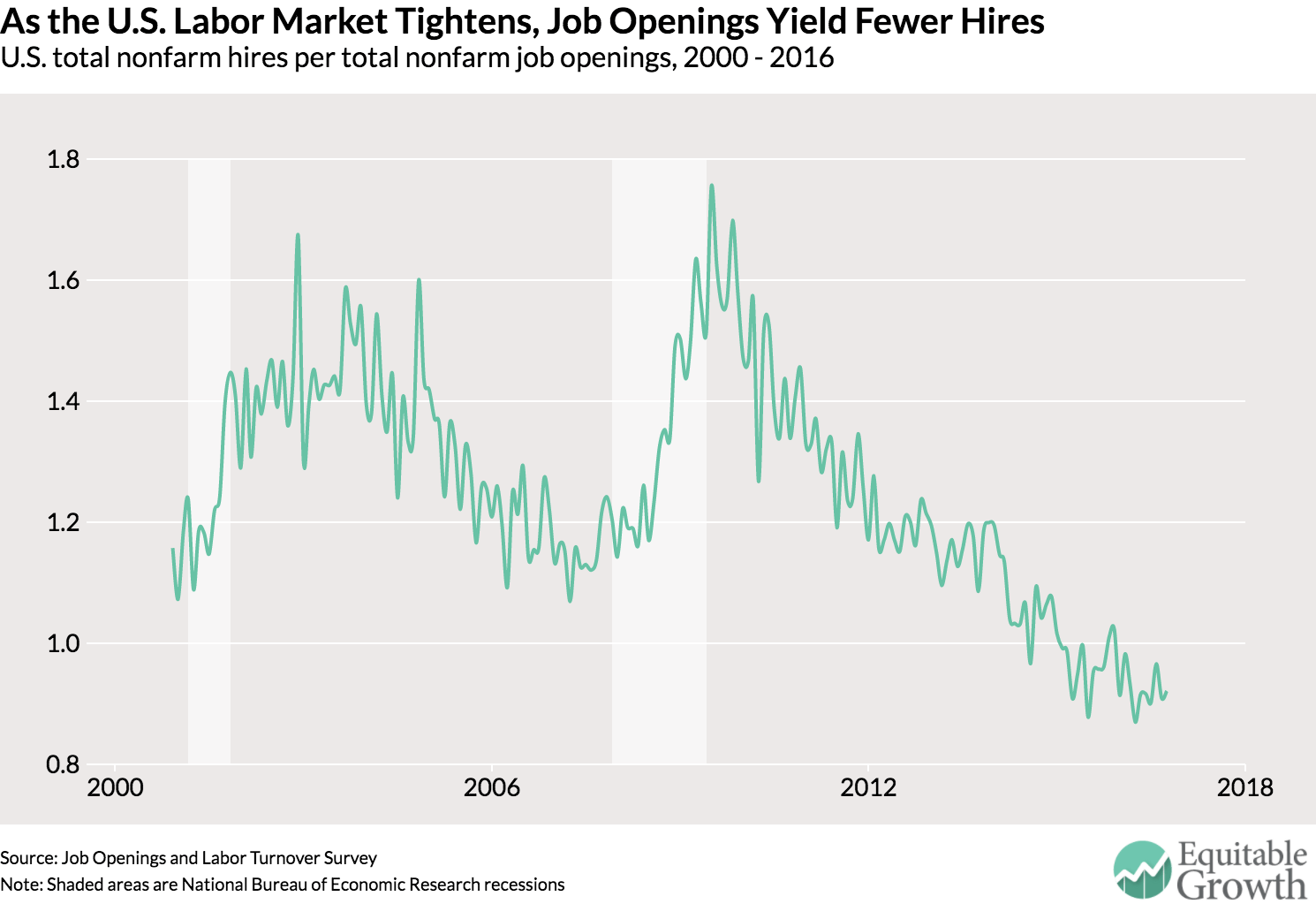

Another metric is the number of hires per job opening, or the rate at which open jobs are being filled. When the labor market is weak, employers will have a relatively easy time filling open jobs. More unemployed workers means employers will have an easy time picking workers they find acceptable. As the labor market improves, job openings will be harder to fill and the number of hires per job opening will decline. Today’s figures show this “vacancy yield” has fallen over the course of the current recovery. (See Figure 2.) By this metric, the U.S. labor market is tighter than its pre-recession levels. But this may be due to a structural change in how easily employers can create jobs. So it may be difficult to look at this graph and know what level of the yield would constitute full employment.

Figure 2

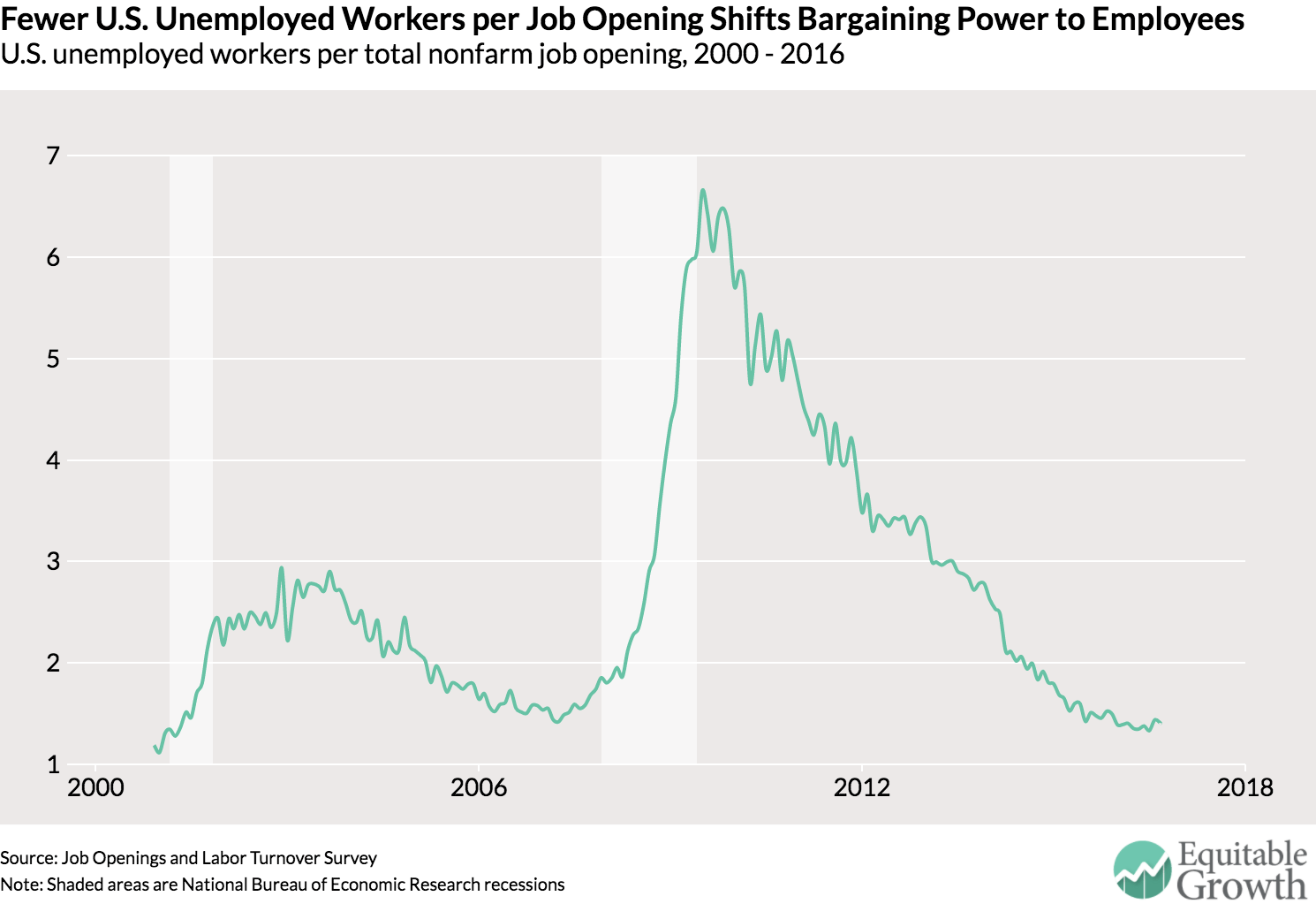

A third and final metric from the JOLTS data is the number of unemployed workers per job opening. A slack or weak labor market will have a high ratio of workers who are laid off and employers who aren’t looking to hire. A higher ratio means employers have relatively more implicit bargaining power as there are more workers competing for a set number of job openings. Workers’ ability to bargain over pay or working conditions starts moving back to workers as the ratio declines. Of course, with so few workers having a union to support them in any negotiations, the ability to bargain with an employer (or potential employer) is based on the individual’s capacity. The current ratio is now at levels slightly lower than pre-recession levels. (See Figure 3.)

A third and final metric from the JOLTS data is the number of unemployed workers per job opening. A slack or weak labor market will have a high ratio of workers who are laid off and employers who aren’t looking to hire. A higher ratio means employers have relatively more implicit bargaining power as there are more workers competing for a set number of job openings. Workers’ ability to bargain over pay or working conditions starts moving back to workers as the ratio declines. Of course, with so few workers having a union to support them in any negotiations, the ability to bargain with an employer (or potential employer) is based on the individual’s capacity. The current ratio is now at levels slightly lower than pre-recession levels. (See Figure 3.)

Figure 3

This metric also shows that the labor market is back at prerecession levels, but notice again that it was much lower in 2000 (a bit over 1) when the labor market has generally regarded at full employment. This ratio might be a good indicator of full employment—if by it we mean a situation where workers can easily find a job and have strong bargaining power. In his book “Full Employment in a Free Society,” the late British economist Sir William Beveridge wrote that full employment “means always more vacant jobs than unemployed men.” Updating this definition based on today’s JOLTS data, policymakers might want to shoot for an economy where the ratio of unemployed workers to job openings can be below 1 sustainably.

This metric also shows that the labor market is back at prerecession levels, but notice again that it was much lower in 2000 (a bit over 1) when the labor market has generally regarded at full employment. This ratio might be a good indicator of full employment—if by it we mean a situation where workers can easily find a job and have strong bargaining power. In his book “Full Employment in a Free Society,” the late British economist Sir William Beveridge wrote that full employment “means always more vacant jobs than unemployed men.” Updating this definition based on today’s JOLTS data, policymakers might want to shoot for an economy where the ratio of unemployed workers to job openings can be below 1 sustainably.

Overall these data show the U.S. labor market to be healthy and continuing its current trajectory toward full employment. How long it’ll take for the labor market to hit full employment is still up for debate.