Should-Read: The very sharp Binyamin Applebaum had an interesting rant yesterday: Binyamin Applebaum: @BCAppelbaum on Twitter: “I am not sure there is a defensible case for the discipline of macroeconomics if they can’t at least agree on the ground rules for evaluating tax policy…

…What does it mean to produce the signatures of 100 economists in favor of a given proposition when another 100 will sign their names to the opposite statement? How does Harvard, for example, justify granting tenure to people who purport to work in the same discipline and publicly condemn each other as charlatans? How are ordinary people, let alone members of Congress, supposed to figure out which tenured professors are the serious economists?…

I would say, first, that journalists (and others) are supposed to use their eyes and their brains. They can take a look at the Nine Unprofessional Republican Economists who placed their letter in the Wall Street Journal last Saturday containing:

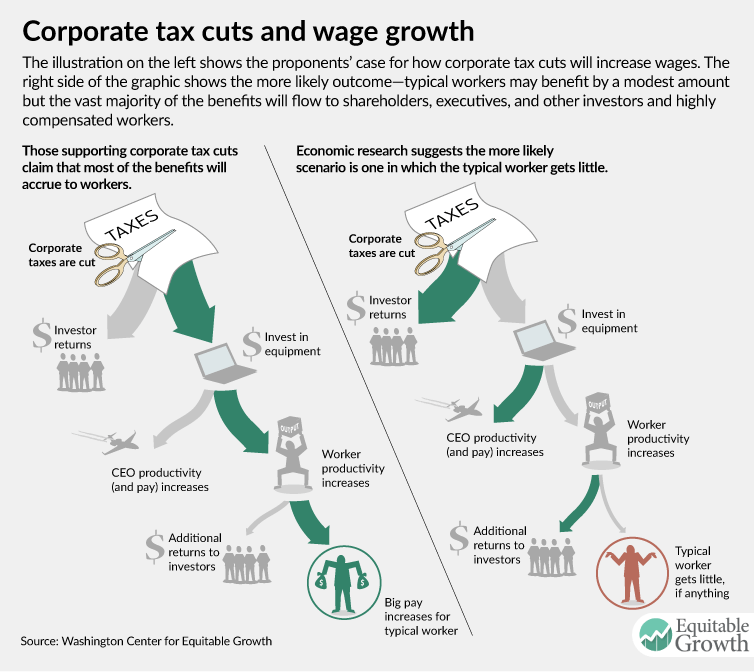

A conventional approach to economic modeling suggests that such an increase in the capital stock would raise the level of GDP in the long run by just over 4%. If achieved over a decade, the associated increase in the annual rate of GDP growth would be about 0.4% per year…

And note that by Wednesday they were saying:

Our letter addresses the impact of corporate tax reform on GDP; we did not offer claims about the speed of adjustment to a long-run result…

That degree of—four days later—”who are you going to believe: us or your lying eyes?” is a definite tell.

Similarly, they can take a look at the Hundred Unprofessional Republican Economists who placed their letter in Business Insider containing:

The enactment of a comprehensive overhaul—complete with a lower corporate tax rate—will ignite our economy with levels of growth not seen in generations… produce a GDP boost ‘by between 3 and 5 percent’…. Sophisticated economic models show the macroeconomic feedback generated by the TCJA will… [be] more than enough to compensate for the static revenue loss…

They should then ask: would a boost to GDP of 3% over 10 years—0.3% per year—generate growth “not seen in generations”? No, it would not. That claim is simply false, as a glance at the GDP growth graph immediately reveals.

They should then ask: what are the “sophisticated economic models [that] show the macroeconomic feedback generated by the TCJA will… [be] more than enough to compensate for the static revenue loss…” And, when the response is “[crickets]”, understand that there are no such models.

These tells of unprofessional behavior will inform them who to trust.

And they should go to organizations that at least have a track record of surveying a consistent group of well-regarded economists, like the IGM Panel. When only one economist on the panel—Stanford’s Darrell Duffie—says that they agree with the statement that the tax bill will make “US GDP… substantially higher a decade from now than under the status quo…” you can conclude that economists claiming it letters that it will are far outside the professional consensus.

Now there is the question of where this unprofessional behavior by economists comes from, and what should be done about it.

Professional economists simply should not say on Saturday that the long run of their forecasts could come in as short a time as a decade (“if achieved over a decade, the associated increase in the annual rate of GDP growth would be about 0.4% per year…) and then the following Wednesday deny what they had said (“we did not offer claims about the speed of adjustment to a long-run result”). They should have not made the might-be-ten-years claim in the first place. Having made it, they should have withdrawn it—hell, they should still withdraw it: they could use the <strike>…</strike> html tag. Having made it, they should not deny that they made it.

Professional economists should not say that an 0.3%-point increase in economic growth would carry us to “levels of growth not seen in generations”. Professional economists should not say that “sophisticated economic models show the macroeconomic feedback generated by the TCJA will… [be] more than enough to compensate for the static revenue loss…” for their are no such models. They are, as one Twitter wit said and as I endorse, the equivalent of the girlfriend-who-lives-in-Canada.

In universities—and thinktanks—concern for one’s academic reputation and the good opinion of colleagues in the context of a community that places the highest value on truth-seeking, truth-telling, and high-quality debate is supposed to keep such unprofessional behavior to a minimum.

Just before he was canned from Berkeley during the Red Scare, medieval history professor Ernst Kantorowicz argued that the academic robe worn by scholars on formal occasions was a sign of this dedication to truth-seeking, truth-telling, and high-quality debate: academics had placed themselves under a geas to think hard and say what they believed to be true, and that in carrying out this geas they were responsible to “their conscience and their God”.

But what if we find that there are large numbers of university professors and thinktank fellows who fear neither God nor their consciences—and who value the support of donors and the approval of partisans more than their internal academic reputations? The process of socialization and acculturation was supposed to keep such people out of universities and thinktanks, and in law and lobbying firms where it was understood that people were simply offering arguments rather than claiming to be setting forth truths, and from which their arguments could be assessed with boatloads of salt. What if this process fails?

It is a serious problem.

I do not have an answer.

Calling out people who I judge behave unprofessionally and cross the line, so that I can no longer credit that they are trying as hard as they can to think and to tell the truth—that is one small thing I can do.