The very-sharp Tyler Cowen gets one, I think, more wrong than right. He writes:

Tyler Cowen: What’s the Natural Rate of Interest?: “I… find all this talk of natural rates of interest…

…historically strange. A few points: (1) David Davidson and Knut Wicksell debated the… concept very early in the twentieth century, in Swedish…. Most people believe Davidson won…. (2) Keynes devoted a great deal of effort to knocking down the natural rate of interest…. There could be multiple natural rates… [or] no rate of interest whatsoever…. (3) In postwar economics, the Keynesians worked to keep natural rates of interest concepts out….

(4) The older natural rate of interest used to truly be about price stability… [not] “two percent inflation a year.”… (5) Milton Friedman warned (pdf) not to assign too much importance to interest rates…. (6) When Sraffa debated Hayek and argued the natural rate of interest was not such a meaningful concept, it seems Sraffa won…. (7) I sometimes read these days that the “natural [real] rate of interest” consistent with full employment is negative. To me that makes no sense in a world with positive economic growth and a positive marginal productivity of capital….

Of course economic theory can change, and if the idea of a natural rate of interest makes a deserved comeback we should not oppose that development per se. But I don’t see that these earlier conceptual objections have been rebutted, rather there is simply now a Kalman filter procedure for coming up with a number…. In any case, this is an interesting case study of how weak or previously rebutted ideas can work their way back into economics. I don’t object to what most of the people working on this right now actually are trying to say. Yet I see the use of the term acquiring a life of its own, and as it is morphing into common usage some appropriately modest claims are taking on an awful lot of baggage from the historical connotations of the term…

In my view, all (7) of these are more than debatable. For example, (7): “[That] the ‘natural [real] rate of interest’ consistent with full employment is negative… makes no sense in a world with positive economic growth and a positive marginal productivity of capital…” misses the wedge–the wedge between the (positive) expected real rate of return from risky investments in capital and the (positive) temporal slope to the expected inverse marginal utility of consumption, on the one hand; and the (negative) equilibrium real low-risk interest rate, on the other hand.

In a world that is all of a global savings-glut world with large actors seeking portfolios that provide them with various kinds of political risk insurance, risk-tolerance gravely impaired by the financial crisis and the resulting deleveraging debt supercycle, moral hazard that makes the remobilization of societal risk-bearing capacity difficult and lengthly, and reduced demographic and technological supports for economic growth, it seems to me highly plausible that this wedge can be large enough to make the low-risk ‘natural [real] rate of interest’ consistent with full employment negative alongside positive economic growth and a positive marginal productivity of capital.

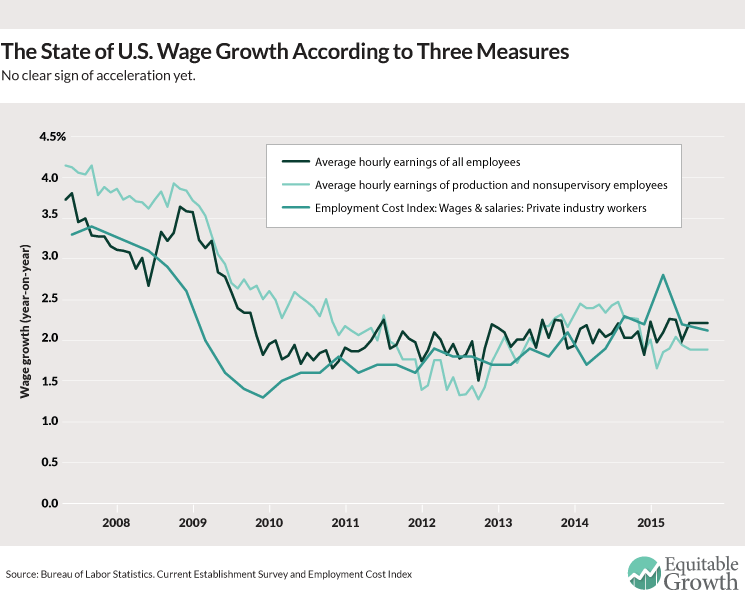

And the bond market agrees with me in email:

And (2): “Keynes devoted a great deal of effort to knocking down the natural rate of interest…” Indeed he did Keynes saw the natural rate of interest as part of a wrong loanable-funds theory of interest rates: that, given the level of spending Y, supply-and-demand for bonds determined the interest rate. Keynes thought that people must reject that wrong theory before they could adopt what he saw as the right, liquidity-preference, theory of interest rates: that, given the level of spending Y and the speculative demand for money S, supply-and-demand for money determined the interest rate.

I think Keynes was wrong. I think Keynes made an analytical mistake.

Hicks (1937) established that Keynes was wrong when he believed that you had to choose. You don’t. Because spending Y is not given but is rather jointly determined with the interest rate, you can do both. Indeed, you have to do both. Liquidity-preference without loanable-funds is just one blade of the scissors: it cannot tell you what the interest rate is. And loanable-funds without liquidity-preference is just the other blade of the scissors: it, too, cannot tell you what the interest rate is. You need both.

More important, however, in thinking about our present concern with the natural (“neutral”) (“equilibrium”) real rate of interest is knowledge of the historical path by which we arrived at our current intellectual situation. Alan Greenspan did it. On July 20, 1994, Alan Greenspan announced that the Federal Reserve was not a “Keynesian” institution, focused on getting the volume of the categories of aggregate demand–C, I, G, NX–right. He announced that the Federal Reserve was not a “Friedmanite” institution, focused on getting the quantity of money right. He announced that the Federal Reserve was now a “Wicksellian” institution, focused on getting the configuration of asset prices right:

Alan Greenspan (1994): Testimony before the Subcommittee on Economic Growth and Credit Formation of the Committee on Banking, Finance and Urban Affairs, U S House of Representatives, July 20: “The FOMC, as required by the Humphrey-Hawkins Act…

…set[s] ranges for the growth of money and debt…. M2 has been downgraded as a reliable indicator…. [The] relationship between M2 and prices that could anchor policy over extended periods of time… [has] broken down…. M2 and P-star may reemerge as reliable indicators of income and prices….

In the meantime… in assessing real rates [of interest], the central issue is their relationship to an equilibrium interest rate, specifically the real rate level that, if maintained, would keep the economy at its production potential over time. Rates persisting above that level, history tells us, tend to be associated with slack, disinflation, and economic stagnation–below that level with eventual resource bottlenecks and rising inflation, which ultimately engenders economic contraction. Maintaining the real rate around its equilibrium level should have a stabilizing effect…. The level of the equilibrium real rate… [can] be estimated… [well] enough to be useful for monetary policy…. While the guides we have for policy may have changed recently, our goals have not…

Greenspan thus shifted the focus of America’s macroeconomic discussion away from the level of spending and the quantity of money to the configuration of asset prices. In some ways this is no big deal: “Keynesian”, “Friedmanite”, and “Wicksellian” frameworks are all perfectly-fine ways to think about macroeconomic policy. They are different–some ideas and some factors are much easier to express and focus on and are much more intuitive in one of the frameworks than in the others. But they are not untranslateable–I have not found any point that you can express in one framework that cannot be more-or-less adequately translated into the others.

The point, after all, is to find a macroeconomic policy that will make Say’s Law, false in theory, true enough in practice for government work. You can start this task by focusing your analysis first on either spending, or liquidity, or the slope of the intertemporal price structure. You will almost surely have to dig deeper into the guts of the economy in order to understand why the current emergent macro properties of the system are what they are. But any one of the languages will do as a place to start. Greenspan in the mid-1990s judged that the Wicksellian language provided the best way to communicate. And, looking back over the past 25 years, I cannot really disagree.

But at the time, back in 1994, the shift to a Wicksellian episteme led to substantial confusion. As I remember it, I spent my lunchtime on July 20, 1994, seated at my computer in my office on the third floor of the U.S. Treasury, frantically writing up just what Alan Greenspan was talking about when he said (1) pay no attention to Federal Reserve policy forecasts of M2; instead, (2) pay attention to our assessments of the relationship of interest rates to an equilibrium interest rate. Greenspan announced that the Fed was no longer asking in a Friedmanite mode “do we have the right quantity of money?”, but rather was asking in a Wicksellian mode “do we have the right configuration of interest rates”. And that still does not seem to me to be a bad place to be.