: The Optimism Error: “When a slump threatened… a government could stimulate spending…

…by cutting interest rates and by incurring budget deficits. This was the main point of the Keynesian revolution…. In the 1980s… unemployment prevention became confined to interest-rate policy… by the central bank, not the government. By keeping… inflation constant, the monetary authority could keep unemployment at its ‘natural rate’. This worked quite well for a time, but… the world economy collapsed in 2008. In a panic, the politicians, from Barack Obama to Gordon Brown, took Keynes out of the cupboard, dusted him down, and ‘stimulated’ the economy like mad. When this produced some useful recovery they got cold feet….

Why had the politicians’ nerve failed and what were the consequences? The answer is that in bailing out leading banks and allowing budget deficits to soar, governments had incurred huge debts that threatened their financial credibility. It was claimed that bond yields would rise sharply, adding to the cost of borrowing. This was never plausible in Britain, but bond yield spikes threatened default in Greece and other eurozone countries early in 2010. Long before the stimulus had been allowed to work its magic in restoring economic activity and government revenues, the fiscal engine was put into reverse, and the politics of austerity took over. Yet austerity did not hasten recovery; it delayed it and rendered it limp when it came.

Enter ‘quantitative easing’ (QE). The central bank would flood the banks and pension funds with cash. This, it was expected, would cause the banks to lower their interest rates, lend more and, by way of a so-called wealth effect, cause companies and high-net-worth individuals to consume and invest more. But it didn’t happen. There was a small initial impact, but it soon petered out…. Institutions sat on piles of cash and the wealthy speculated in property. So we reach the present impasse…. Monetary expansion is much less potent than people believed; and using the budget deficit to fight unemployment is ruled out by the bond markets and the Financial Times. The levers either don’t work, or we are not allowed to pull them….

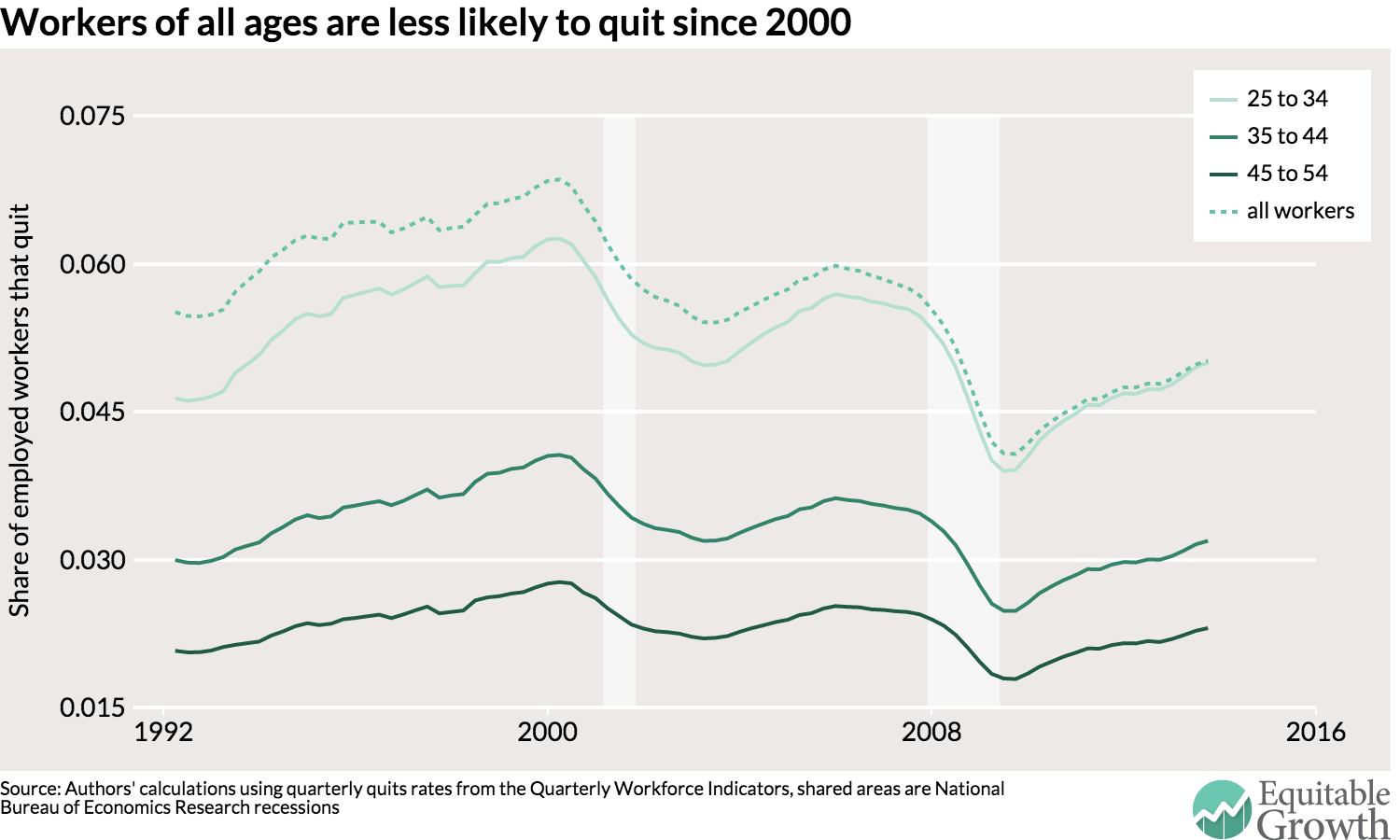

How much recovery has there been in Britain?… The OECD’s most recent estimate of this [output] gap in the UK stands at a negligible -0.017 per cent. We might conclude from this that the British economy is running full steam ahead and that we have, at last, successfully recovered from the crash…. But… although we are producing as much output as we can, our capacity to produce output has fallen…. Growth in output per person in Britain (roughly ‘living standards’) averaged 2.25 per cent per year for the half-century before 2008. Recessions in the past have caused deviations downward from this path, but recoveries had delivered above-trend growth…. This time it was different. The recovery from the financial crisis was the weakest on record, and the result of this is a yawning gap between where we are and where we should have been. Output per head is between 10 and 15 per cent below trend….

Why is it that the recession turned spare capacity into lost capacity? One answer lies in the ugly word ‘hysteresis’…. The recession itself shrinks productive capacity: the economy’s ability to produce output is impaired…. Much of the new private-sector job creation lauded by the Chancellor is… in such low-productivity sectors. The collapse of investment is particularly serious, because investment is the main source of productivity. The challenge for policy is to liquidate the hysteresis – to restore supply. How is this to be done?…

On the monetary front, the bank rate was dropped to near zero; this not being enough, the Bank of England pumped out hundreds of billions of pounds between 2009 and 2012, but too little of the money went into the real economy. As Keynes recognised, it is the spending of money, not the printing of it, which stimulates productive activity, and he warned: ‘If… we are tempted to assert that money is the drink which stimulates the system to activity, we must remind ourselves that there may be several slips between the cup and the lip.’ That left fiscal policy… deliberately budgeting for a deficit. In Britain, any possible tolerance for a deficit larger than the one automatically caused by a recession was destroyed by fearmongering about unsustainable debt. From 2009 onwards, the difference between Labour and Conservative was about the speed of deficit reduction…. From 2009 onwards the main obstacle to a sensible recovery policy has been the obsession with balancing the national budget…. ‘We must get the deficit down’ has been the refrain of all the parties….

It is right to be concerned about a rising national debt (now roughly £1.6trn). But the way to reverse it is not to cut down the economy, but to cause it to grow in a sustainable way. In many circumstances, that involves deliberately increasing the deficit. This is a paradox too far for most people to grasp. But it makes perfect sense if the increased deficit causes the economy, and thus the government’s revenues, to grow faster than the deficit…. In our present situation, with little spare capacity, the government needs to think much more carefully about what it should be borrowing for. Public finance theory makes a clear distinction between current and capital spending. A sound rule is that governments should cover their current or recurrent spending by taxation, but should borrow for capital spending, that is, investment. This is because current spending gives rise to no government-owned assets, whereas capital spending does. If these assets are productive, they pay for themselves by increasing government earnings, either through user charges or through increased tax revenues. If I pay for all my groceries ‘on tick’ my debt will just go on rising. But if I borrow to invest in, say, my education, my increased earnings will be available to discharge my debt….

Now is an ideal time for the government to be investing in the economy, because it can borrow at such low interest rates. But surely this means increasing the deficit? Yes, it does, but in the same unobjectionable way as a business borrows money to build a plant in the expectation that the investment will pay off. It is because the distinction between current and capital spending has become fuzzy through years of misuse and obfuscation that we have slipped into the state of thinking that all government spending must be balanced by taxes – in the jargon, that net public-sector borrowing should normally be zero. George Osborne has now promised to ‘balance the budget’ – by 2019-20. But within this fiscal straitjacket the only way he can create room for more public investment is to reduce current spending, which in practice means cutting the welfare state.

How can we break this block on capital spending? Several of us have been advocating a publicly owned British Investment Bank. The need for such institutions has long been widely acknowledged in continental Europe and east Asia, partly because they fill a gap in the private investment market, partly because they create an institutional division between investment and current spending. This British Investment Bank, as I envisage it, would be owned by the government, but would be able to borrow a multiple of its subscribed capital to finance investment projects within an approved range. Its remit would include not only energy-saving projects but also others that can contribute to rebalancing the economy – particularly transport infrastructure, social housing and export-oriented small and medium-sized enterprises (SMEs). Unfortunately, the conventional view in Britain is that a government-backed bank would be bound, for one reason or another, to ‘pick losers’, and thereby pile up non-performing loans. Like all fundamentalist beliefs, this has little empirical backing….

George Osborne has rejected this route to modernisation. Instead of borrowing to renovate our infrastructure, the Chancellor is trying to get foreign, especially Chinese, companies to do it, even if they are state-owned. Looking at British energy companies and rail franchises, we can see that this is merely the latest in a long history of handing over our national assets to foreign states. Public enterprise is apparently good if it is not British….

Setting up a British Investment Bank with enough borrowing power to make it an effective investment vehicle is the essential first step towards rebuilding supply. Distancing it from politics by giving it a proper remit would create confidence that its projects would be selected on commercial, not political criteria. But this step would not be possible without a different accounting system. The solution would be to make use of comprehensive accounting that appropriately scores increases in net worth of the bank’s assets…