Issue brief: What is the federal business-level tax on capital in the United States?

Overview

As Congress turns its attention to tax reform, dramatic reductions in the top statutory tax rates on business income are sure to be among the most important and most contentious elements of the debate. Under current law, the top statutory tax rate for traditional C corporations is 35 percent, and the top statutory tax rate for pass-through businesses is 39.6 percent. The Trump administration has proposed a top rate of 15 percent rate for both C corporations and pass-through businesses, and Republicans in the U.S. House of Representatives have proposed a top rate of 20 percent for C corporations and 25 percent for pass-through businesses.1

Download FileWhat is the federal business-level tax on capital in the U.S.?

Read the full PDF in your browser

Proponents of these sharp rate cuts often justify them by arguing that they will increase investment and thus economic growth. In a wide class of economic models, however, the statutory tax rate on business income has no direct relationship to investment or growth. It is instead the effective marginal tax rate on capital that most closely relates to the level of investment. The effective marginal tax rate relevant for investment decisions includes the impact of business-level taxes, investor-level taxes, and lender-level taxes. Statutory tax rates on business income only influence the portion of the effective marginal tax rate attributable to business-level taxes.

The business-level federal effective marginal tax rate on capital depends on many complex provisions of the tax code in addition to the statutory tax rate, including the rules governing the depreciation of business assets, the availability of deductions for interest payments, and tax credits for research and development. The tax rate on an investment varies depending on whether the firm making that investment is a C corporation or a pass-through business, on the amount of the investment financed using debt or equity, and on the assets that make up the investment. Businesses that rely on intellectual property for most of their income, for example, face very different tax rates than those that derive most of their income from rents on real estate—reflecting differences in their ability to benefit from different business tax breaks and in their ability to obtain debt financing for their investments.

This issue brief answers a key question facing policymakers as they debate changes in business taxation: What is the business-level federal effective marginal tax rate on capital today? The analysis in this brief finds that the average effective marginal tax rate is only 8 percent under current law, far less than the statutory tax rates on business income.2 The rate would rise to only 13 percent if a tax break known as bonus depreciation expires in 2020, as scheduled under current law.

Even though little tax is imposed on capital income at the business level, taxes on business income still raise substantial revenues because a large portion of the business-income tax base consists of excess returns (returns above the risk-free rate such as those due to monopoly pricing power), income attributable to labor that was not paid out as wages, and luck. These sources of business income are not included in the definition of capital income used in this brief, consistent with the definition of the effective marginal tax rate on capital, discussed in greater detail below.

While the average business-level effective marginal tax rate is low, rates vary widely for investments in different assets and for investments financed with different proportions of debt and equity. The tax rate on investments in inventories, for example, is 28 percent—relatively close to the statutory rates on business income—while the tax rate on investments in intellectual property is negative-25 percent, meaning an investment would yield excess deductions or credits that could be used to offset taxes owed on other income subject to certain limitations. Similarly, the tax rate on equity-financed investment is 21 percent, while the tax rate on debt-financed investment is negative-54 percent.

Given the low average effective marginal tax rate, it makes little sense to prioritize cutting statutory tax rates. Cutting the statutory tax rates on business income would do relatively little to encourage additional investment and thus have relatively little effect on growth, even before considering the effects of increased deficits resulting from the rate cuts or additional policies to offset that cost. Moreover, the tax cut resulting from a reduction in the statutory tax rates on business income would be severely regressive.

Instead, the combination of a low average effective marginal tax rate and substantial variation in rates for different investments means that there is an opportunity to pursue a superior approach to reform that would focus on reducing the disparity in tax rates between investments and thus generate a more efficient mix of investment projects.

More concretely, rather than cutting statutory tax rates, Congress should pursue a revenue-neutral or revenue-increasing reallocation of the current tax benefits for debt to equity that reduces the disparities in the tax rates on investments in different types of produced capital: equipment, structures, inventories, and intangibles. Such a reallocation could also lower the tax rate on produced capital and increase the tax rate on land. These reforms would offer a more plausible path to economic growth than reductions in the statutory tax rates on business income.

Federal taxation of business income

Income derived from business activity is subject to a complicated set of interconnected taxes. U.S. businesses can be structured as either traditional C corporations or as pass-through businesses. Traditional C corporations pay corporate income tax on their profits. Pass-through businesses—including S corporations, partnerships, and sole proprietorships—are not subject to the corporate income tax. Instead, owners of pass-through businesses pay tax on their share of the businesses’ profits as part of the computation of their individual income-tax liability. The choice between corporate and pass-through form is largely at the discretion of the owners. While the two forms impose different legal requirements and result in different legal and tax treatments, both forms are common and appear in a wide range of industries.

Dividends paid by C corporations are subject to tax at the individual level, but dividends or other distributions from pass-through entities are generally not subject to tax at the individual level. Investors in any type of business who sell an ownership stake that has increased in value realize a capital gain and pay tax on the resulting income. Lenders to any type of business pay tax on interest payments received from the business.

The corporate income tax and the individual income tax rely on similar measures of business profits for determining the tax on corporate income and pass-through income, respectively. Profits are defined as receipts less the cost of goods sold, employee compensation, operating expenses such as accounting and legal services, depreciation, and interest payments.3 The corporate income tax has graduated rates, but the top rate of 35 percent applies to the overwhelming majority of corporate income. Income derived from pass-through businesses is subject to tax according to the progressive rate schedule for the individual income tax.

In addition to the statutory tax rate on business income, the key determinants of the effective marginal tax rate on capital are the rules governing cost recovery, interest deductibility, and the research credit. Each of these components is examined in turn below.

Cost recovery

Cost recovery refers to the quantity and timing of depreciation deductions allowed for capital expenditures such as the purchase of new equipment or buildings. If a business can immediately deduct the cost of a capital expenditure, then the investment is said to be expensed. If a business can deduct only a portion of the cost each year over a multiyear period, then the investment is said to be depreciated. Depreciation at a rate that corresponds to the decline in value of the asset over time is referred to as economic depreciation, and depreciation at a faster pace is referred to as accelerated depreciation. Economic depreciation is required for the proper measurement of income. Under a system of economic depreciation, depreciation deductions correspond to the decline in value of the assets owned by the business, and thus sales less operating expenses and depreciation yields an accurate measure of the income generated by the business. A tax system that follows economic depreciation and has no other special deductions or credits would impose a business-level tax on equity-financed investment equal to the statutory tax rate.

Under current tax law, most investment in equipment and structures is eligible for accelerated depreciation, and most investment in intangible assets such as research and development is expensed. Both accelerated depreciation and expensing reduce the tax rate applied to capital income because deductions are allowed before the corresponding loss due to a decline in the value of the underlying asset. Because a dollar today is worth more than a dollar tomorrow, the value of the reduction in tax today exceeds the value of the future increase in tax, even though the nominal amounts are the same. In contrast to the treatment of equipment and structures, no depreciation deductions are allowed for land or inventories.

To illustrate how these calculations work, consider a simplified example involving the business purchase of a truck. Suppose the truck is expected to last for 8 years. A business that purchased the truck for $20,000 might depreciate it for accounting purposes over that 8-year period, deducting $2,500 from income each year. In contrast, the tax code allows businesses to write off trucks over 5 years. The business could then deduct $4,000 each year for 5 years and recover the value of the investment in the truck over a shorter period.4 Because the deductions are accelerated relative to the decline in value of the asset, they serve to reduce the tax rate on the income generated by the asset.

Depreciation of most equipment and software investment is further accelerated as a result of a temporary provision of law known as bonus depreciation. Bonus depreciation, which has been in effect since 2008, allows businesses to expense a percentage of equipment and software investment and then depreciate the remainder under the usual schedule. Under current law, bonus depreciation is available at a 50 percent rate in 2017, 40 percent rate in 2018, and 30 percent rate in 2019. Bonus depreciation expires in 2020.

Interest deductibility

The measure of business profits subject to tax under either the corporate income tax or the individual income tax consists of receipts less the cost of goods sold, operating expenses, depreciation deductions, and interest payments. As discussed above, economic depreciation is necessary for the proper measurement of capital income, and accelerated depreciation serves as an investment incentive. In contrast, interest deductions serve to assign the legal responsibility for paying tax on capital income to the lenders financing the activity instead of the business owners. As such, they have no direct relationship to the measurement of capital income generated by the underlying business activity. Because the deductibility of interest allows businesses to provide a return to lenders without paying any tax on the income that generated that return at the business level, it reduces the taxation of capital at the business level.

Consider a hypothetical tax system with economic depreciation and full interest deductibility. A firm finances an investment project solely with debt and realizes a return equal to the interest rate paid on the loan. The deductible interest payments would exactly offset the income from the investment such that the business’s income for tax purposes would be zero in every year and thus there would be no business-level tax on that investment.5

If all businesses and lenders were taxable at the same rate, repealing interest deductibility for businesses and exempting interest income from tax would reassign the legal responsibility for paying tax to business owners rather than lenders without changing the overall level of tax, including both the business- and lender-level taxes. (In practice, interest deductions reported by businesses exceed taxable interest income reported by lenders, suggesting that substantial interest income is avoiding tax at both levels.) For the purposes of evaluating proposals for reduced statutory tax rates on business income, however, the distinction between taxation at the business level and the lender level is crucial. Reducing the statutory tax rate on business income reduces the value of the deduction for interest payments received by the business and thus increases the tax rate on debt-financed investment.

Research and development tax credit

Research and development expenses are generally expensed rather than depreciated over time, in line with the decline in value of the intellectual property created by those expenses. In addition, federal tax law also provides a credit for research expenses. Businesses can use one of two different formulas to compute the credit. The regular credit is equal to 20 percent of the amount by which research expenses exceed a base amount. The alternative credit is equal to 14 percent of the amount by which research expenses exceed 50 percent of average research expenses over the prior 3 years.6 For purposes of computing depreciation deductions, the cost of the asset is reduced by the value of the credit received. The credit serves to reduce the taxation of investments in intangible capital generated through research and development.

Effective marginal tax rates

The effective marginal tax rate on capital is the percentage of the pre-tax return paid in taxes on an investment that yields the minimum return required to obtain financing in the capital markets. This rate is not specified in statute, but rather is an analytic quantity that summarizes the impact of many different aspects of the tax system, including the statutory tax rate on business income, the generosity of cost-recovery rules, and the treatment of interest payments over the entire life of an investment project.

This brief presents estimates of the federal effective marginal tax rate on produced domestic capital imposed at the business level. For C corporations, this is the rate imposed by the corporate income tax. For pass-through businesses, this is the rate imposed on owners via the individual income tax, excluding the tax on interest paid by lenders. Produced capital—defined here as equipment, structures, inventories, and intangibles—consists of those types of capital for which the stock can vary in accordance with investment. In contrast, land—the other major type of capital—is available in relatively fixed supply. Domestic capital refers to firms’ investments located in the United States.7

Effective marginal tax rates are typically estimated by applying current tax law to hypothetical investments by C corporations and pass-through entities in a wide array of assets using different financing arrangements, and then aggregating these estimated tax rates for narrowly defined investment projects into averages for broad classes of assets, financing arrangements, and corporate or pass-through tax treatment. The methods used in this brief are similar to those used by other analysts, including the Congressional Budget Office, U.S. Treasury Department, and the Congressional Research Service.8

The effective marginal tax rate influences the size of the capital stock in a wide class of economic models and thus has direct relevance for judging the economic effects of the tax system. If this rate is zero for a particular type of investment, then the tax system imposes no tax on an investment of that type that yields the return required to obtain financing in capital markets. Thus, it neither increases nor decreases the financial incentive to engage in such investment.9 A negative tax rate indicates that an investment would yield excess deductions or credits that could be used to offset taxes owed on other income subject to certain limitations.

In addition to the effective marginal tax rate, numerous other tax rates also relevant for economic decisions can be defined and analyzed. The statutory tax rate on business income, for example, is relevant for avoidance behavior such as international profit shifting or shifting between the individual and business base. The effective average tax rate can be relevant for multinational corporations planning a single large investment that must decide in which country to make the investment.10 And several possible definitions of the average tax rate exist that measure the overall level of tax paid by business owners.11 This brief focuses on the effective marginal tax rate due its importance for the evaluation of claims about changes in the level of investment resulting from tax reform.

The estimates reported in this brief are broadly similar to those produced by other analysts when the definitions used are the same. Two definitions used in this analysis are noteworthy relative to those used by other analysts. First, while the business-level tax rate is frequently discussed in the context of corporate taxes, estimates of the effective marginal tax rates for pass-throughs typically do not draw the same distinction between the business-level and investor-level taxes. The distinction is made here because it is directly relevant to evaluating recent proposals for sharply reduced statutory rates on business income.

Second, analysts use widely varying definitions of intangible capital.12 This analysis, similar to that of the Congressional Research Service, uses a broad definition of intangible capital, including information technology, research and development, advertising, creative works, strategic planning, and firm-specific employee training. The U.S. Treasury Department typically uses a narrower definition, including only software, research and development, advertising, and creative works. In its most recent analysis, the Congressional Budget Office excluded intangible capital, apart from certain types of software.

Current effective marginal tax rates

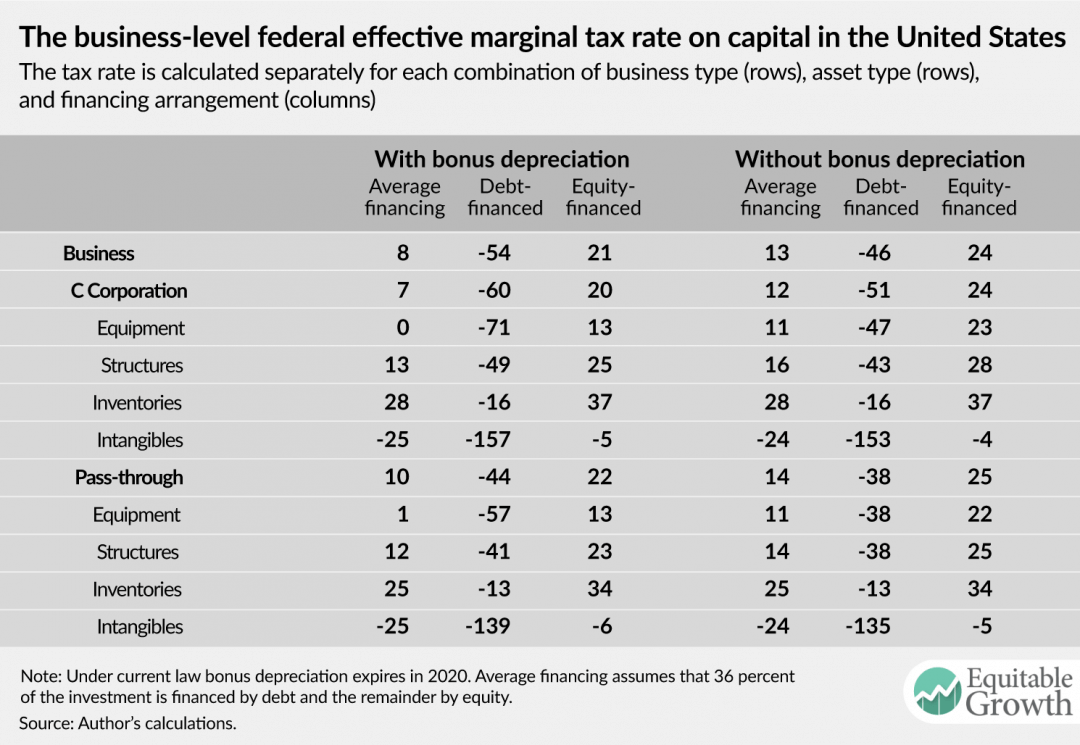

Table 1 below presents estimates of the business-level effective marginal tax rate on produced domestic capital under current law. The first three columns provide estimates assuming 50 percent bonus depreciation, and the second three columns provide estimates assuming bonus depreciation has expired. (Bonus depreciation is available at a 50 percent rate through 2017 and phases down to zero at the beginning of 2020.) The average effective marginal tax rate for produced domestic-business capital at the business level is 8 percent under current law today and 13 percent without bonus depreciation, as would be the case for current law in 2020. These rates reflect the average of strongly negative tax rates for fully debt-financed investment (negative-54 percent) and a positive tax rate for fully equity-financed investment (21 percent).

Table 1

Some caution should be applied in interpreting the tax rates for fully debt-financed investment shown in Table 1. Large negative tax rates indicate that an investment yields deductions or credits more than sufficient to eliminate the tax on that investment over its useful life, but a business may not be able to recognize the full benefit of those deductions or credits due to limitations on the deductibility of business losses. Moreover, it would be difficult, if not impossible, for a small or new business to finance an investment solely through debt. In the case of a large business, an investment could be financed solely with debt, though in that case there would be generally be an implicit transfer of risk onto the broader business. (The underlying methodology, as is standard for effective marginal tax rate computations, abstracts from risk.) The role of debt finance will be explored further in the next section.

The estimated effective marginal tax rates on capital are far below the statutory rates on business income. The underlying model assumes the statutory rate on corporate income is 34 percent, reflecting an assumed statutory rate of 35 percent and a 1 percentage point reduction attributable to the domestic-production activities deduction, and the statutory rate on pass-through income is 31 percent, reflecting an income-weighted average of the tax rate on pass-through income.13

The difference between the assumed statutory rates in the modeling and the effective rates is driven by four primary factors: accelerated depreciation of tangible investment, expensing of most intangible investment, largely unrestricted interest deductibility, and the research credit.

In the case of an equity-financed investment, the tax preference for interest is not relevant. The difference between the effective tax rate and the statutory tax rate reflects the value of accelerated depreciation, expensing, and the research credit. Accelerated depreciation and expensing cause federal tax law to understate income and thus result in tax at a lower rate. The research credit directly offsets tax, thus reducing the tax rate on eligible investment.

In the case of a debt-financed investment, it is useful to recall the hypothetical tax system with economic depreciation and interest deductibility discussed above. Under this system, a debt-financed investment would face no tax. Thus, offering accelerated depreciation reduces the tax rate below zero for a debt-financed investment, subsidizing the investment rather than taxing it. Moreover, the theoretical result that economic depreciation and interest deductibility jointly impose zero tax assumes deductibility of real (inflation-adjusted) interest payments. In practice, interest payments include both the real interest payment and an additional payment to compensate the lender for the decline in the value of the principal due to inflation. As the U.S. tax system allows for the deduction of nominal interest payments, it further subsidizes debt-financed investments at the business level.

The tax rate on investments financed by a mix of debt and equity reflects an average of the pure debt and pure equity cases. One useful way to think about the economics of this case is that the debt-financed portion of the investment is exempt from tax at the business level as a result of economic depreciation plus interest deductibility. Yet the debt-financed portion entitles the business to an additional tax benefit attributable to the excess of actual depreciation deductions over economic depreciation on that portion of the investment—and this benefit can be used to further shelter the return on the equity-financed portion of the investment. Thus, by using debt finance, equity owners can effectively shelter an additional portion of their return on investment from tax.

Table 1 above presents estimates of tax rates by form of business and asset type. The business-level effective marginal tax rate is slightly higher for pass-throughs than for C corporations, though this finding is primarily the result of a different weighting of investments across asset types rather than higher tax rates for each asset type. Consistent with other analyses, the effective marginal tax rate is highest for inventories, which are not depreciated, and lowest for intangibles, which are generally expensed and often eligible for the research credit. But the results in Table 1 are highly sensitive to assumptions about the use of debt finance, as will be discussed in the next section.

The role of debt finance

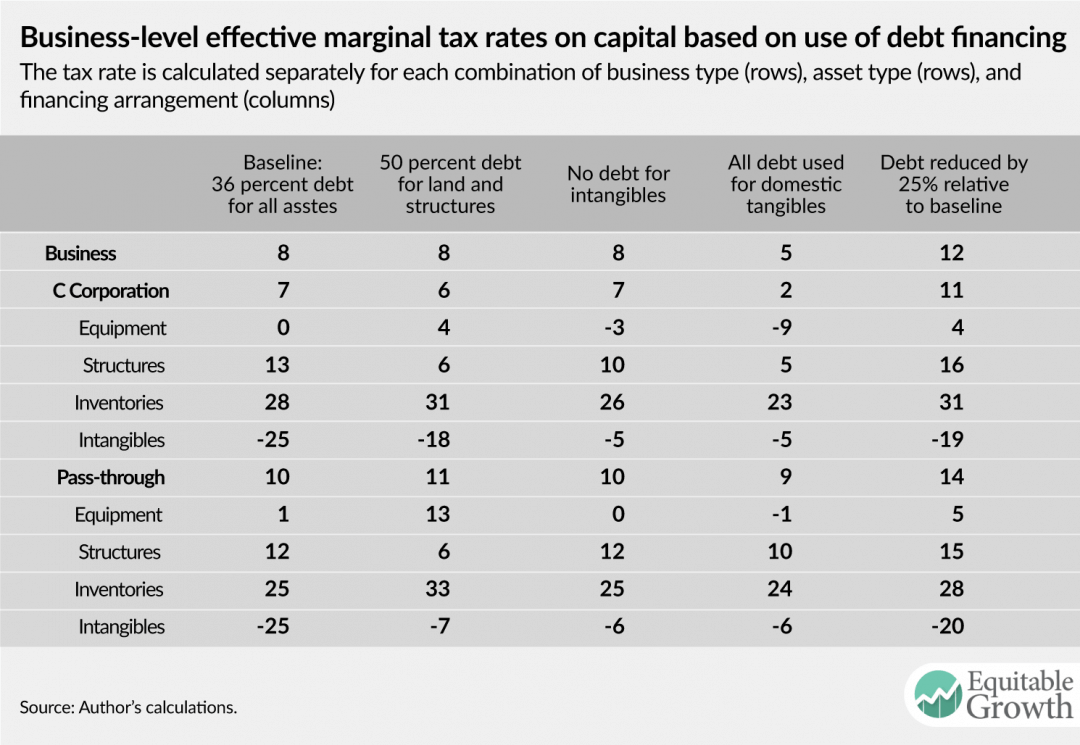

Estimated effective marginal tax rates on capital are highly sensitive to the assumptions about the use of debt finance. Table 2 below shows effective marginal tax rates under the baseline assumption about the use of debt finance and four alternatives. Under the baseline assumption used above in Table 1, all investments are financed with the same share of debt. The first column of Table 2 repeats the baseline estimates. The second column reports estimates assuming debt is used to finance 50 percent of land and structures. The share of debt financing for all other asset types is reduced to hold fixed the aggregate quantity of debt. The third column reports estimates assuming debt is fully allocated to tangible investment. The fourth column reports estimates assuming debt is fully allocated to domestic tangible investment (debt issued in the United States is not used to finance firms’ overseas investments). The fifth column uses the base case assumption of equal use of debt finance across types of investments but reduces the share of debt finance for all investments by 25 percent. Note that while the table only reports tax rates on produced domestic capital, the underlying model includes land and foreign investment. Thus, the aggregate quantity of debt implicit in the tax rates reported in Table 2 varies across columns, as debt assigned to asset classes not shown—land and foreign investment—changes.

Table 2

Findings about the relative tax rate on different assets are highly sensitive to assumptions about the use of debt finance. Assuming 50 percent of investment in land and structures is financed with debt results in nearly equal tax rates on equipment and structures, rather than a 13 percentage point gap between the tax rates. Allocating a greater share of debt to tangible assets rather than intangible assets results in a modest reduction in the effective marginal tax rate for tangible assets. Allocating a greater share of debt to domestic investment more substantially reduces the rate for domestic-produced assets. Finally, reducing the share of debt finance across the board results in a modest increase for all assets.

The variation in tax rates apparent in Table 2 also highlights the extent to which there is no single tax rate on investments, even for a particular mix of assets. The tax rate on a project will depend on the financing arrangements for that project. The importance of debt in avoiding business-level taxes can be seen by examining how these provisions apply to real estate partnerships.

Case study: Real estate partnerships

Statistics on the rental income of partnerships in the real estate industry provide a useful illustration of how accelerated depreciation and interest deductibility operate to shelter capital income from tax at the business level and thus generate low effective marginal tax rates. Moreover, as real estate partnerships account for more than $2 trillion of depreciable assets (judged at book value), these results are relevant for the broader economy.14

Real estate partnerships reported $524 billion in gross rents, $484 billion in rental expenses, and $2 billion in gains from the sale of rental property in 2014, the most recent year for which data are available. Net income from rental activities for tax purposes was thus $43 billion.15 Of the rental expenses, interest payments accounted for $114 billion and depreciation deductions for $109 billion.

Because depreciation for tax purposes differs from economic depreciation, it would not be appropriate to use the $43 billion in income reported on tax returns plus interest payments as an estimate of the economic income generated by the sector. Instead, estimating the economic income of these businesses requires an adjustment to the reported depreciation values. Using the ratio of economic depreciation to tax depreciation reported in the National Income and Product Accounts for sole proprietorships and partnerships to adjust the depreciation reported on real estate partnership tax returns yields an estimate of $59 billion for economic depreciation in the sector.16 This approximation suggests the economic income generated by rental partnerships—on behalf of equity owners and lenders—was about $208 billion, equal to the net income reported on tax returns plus interest and tax depreciation less economic depreciation. Thus, the taxable income reported from real estate activities was only 21 percent of the economic income generated by the sector.17 Of course, as partnerships are pass-through entities, the tax paid on the taxable share depends on the characteristics of the partners.

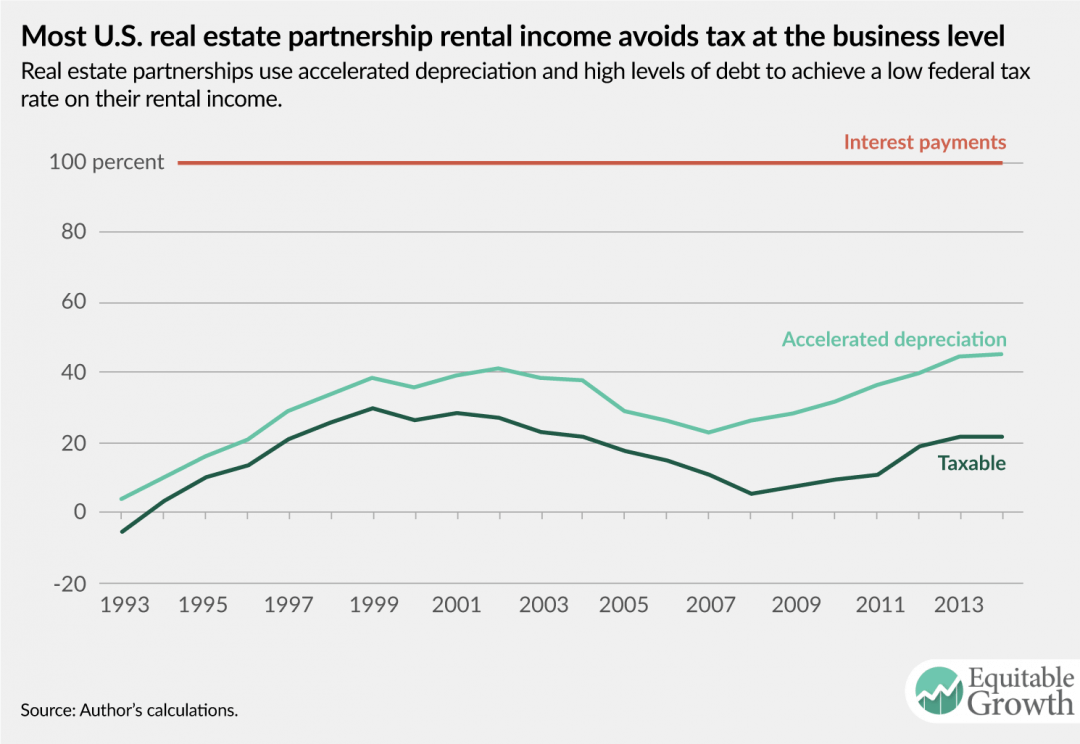

Figure 1 shows the same calculation for the years 1993 to 2014. Average net income at the business level for rental partnerships is only 16 percent of the economic income generated by these businesses over this period.

Figure 1

While interest payments reflect a permanent avoidance of business-level tax, accelerated depreciation allowances only change the timing of tax payments. Thus, for a specific investment project, an additional dollar of depreciation allowances today results in a dollar less of depreciation allowances in the future. But depending on the pattern of investment returns and asset sales over time, the aggregate taxable share of income for all partnerships could remain less than economic income less interest payments in all years.

Moreover, real estate partnership tax returns suggest that tax rates similar to those reported in this brief may overstate the tax paid on investments in that industry. The largest single source of income reported by these partnerships in many years is not rental income, but section 1231 gains. These gains are likely generated in large part by the sale of rental property, and the tax rates applied to such gains are often substantially lower than the rates that apply to rental income. The modeling underlying the estimates reported in this brief rules out the sale of business property and assumes that the tax rate applicable to business income is constant over time. Thus, if depreciation deductions are increased by a dollar today and reduced by a dollar in the future, then the tax savings today and the additional tax in the future are the same before discounting. If, instead, businesses benefit from depreciation deductions today at a higher tax rate and then sell assets later while facing a lower tax rate, accelerated depreciation can be worth more than the modeling assumes.

Finally, while this brief focuses on produced capital consisting of equipment, structures, inventories, and intangible assets, the rental industry relies to a substantial extent on land, which is available in relatively fixed quantity. Real estate partnerships report land equal to roughly one-third of the value of depreciable assets, judged at book value. A substantial fraction of the income reported by rental partnerships thus reflects returns on land rather than returns on produced capital. In fact, assuming debt financing of roughly 60 percent—a higher share than assumed in the tax rate estimates presented in this brief but not unreasonable given the estimates in Figure 1 above—the business-level effective marginal tax rate on structures would be about zero, and the effective marginal tax rate on land would be about 10 percent for both C corporations and pass-through businesses. These tax rates suggest that nearly all the rental income reported on real estate partnership returns is a return to land, excess returns, or labor income—not to investments in structures.

Implications for tax reform

Business-level federal effective marginal tax rates on capital income are quite low: 8 percent under current law and 13 percent if bonus depreciation expires. Rates are strongly negative for debt-financed investment, at negative-54 percent, and positive for equity-financed investment, at 21 percent. Moreover, other recent research suggests that the overwhelming majority of the corporate tax base consists of excess returns and labor income, not the risk-free return on produced capital.18

In light of these findings, the case for reductions in the statutory business tax rate as a means of spurring additional capital investment is weak. A reduction in the business tax rate would come at a very high cost, as it would apply to the entire business tax base, including excess returns and labor income, as well as to returns on investments made in the past.19 The impact on capital investment would be highly attenuated, as debt-financed investments face a negative rate at the business level, and thus a rate cut would increase the tax rate on such investments by reducing the value of the deductions they generate. Moreover, as lowering the cost of capital is the channel through which a reduced effective marginal tax rate can increase investment, deficit-financed tax cuts that increase the cost of capital can be actively counterproductive.

While the average rate is low, there is substantial variation in tax rates across asset types and financing arrangements. If 36 percent of each investment is financed with debt—the baseline assumption about the use of debt finance in this brief—then inventory investment is taxed at 28 percent, and intangible investment is taxed at a rate of negative-25 percent. Equipment is taxed at a near-zero rate, and structures are taxed at a rate of 13 percent. If, instead, 50 percent of investment in structures is financed with debt, then the effective marginal tax rate on such investment is only 6 percent. The tax rate that would apply to any real-world investment would almost certainly differ from any of these tax rates, as it would rely on financing and legal arrangements different from any of the scenarios presented.

A better approach to reform would therefore focus on reducing the disparities in tax rates across types of produced capital and across financing arrangements. This variation is largely driven by variation in the extent to which tax depreciation is accelerated relative to economic depreciation and variation in the use of debt finance. Well-designed reform should thus pursue a revenue-neutral or revenue-increasing reallocation of the current tax benefits for debt to equity that reduces the disparities in the tax rates on investments in different types of produced capital. Such a reallocation could also lower the tax rate on produced capital and increase the tax rate on land. These reforms would offer a more plausible path to economic growth than reductions in the statutory tax rates on business income.

End Notes

1. “The 1-page White House Handout on Trump’s Tax Proposal,” available at http://www.cnn.com/2017/04/26/politics/white-house-donald-trump-tax-proposal/index.html (last accessed September 2017); House GOP, “A Better Way, Our Vision for a Confident America: Tax,” (2016), available at http://abetterway.speaker.gov/_assets/pdf/ABetterWay-Tax-PolicyPaper.pdf.

2. Details of the methods used to compute the tax rates presented in this brief are available from the author upon request.

3. Special rules apply to certain industries and organizations, including insurance companies, mutual funds, and real estate investment trusts. These rules are beyond the scope of this brief.

4. For simplicity, this example assumes straight line depreciation even though a declining balance method would likely be more advantageous in practice. In addition, it ignores the half-year (or other applicable) convention that would determine the allowable depreciation deduction for the year the asset is placed in service.

5. This example assumes repayment of principal at a rate consistent with the decline in value of the underlying asset and ignores the complications arising from deducting nominal rather than real interest payments on debt.

6. For a more detailed discussion of the research credit, see Gary Guenther, “Research Tax Credit: Current Law and Policy Issues for the 114th Congress” (Washington: Congressional Research Service, 2015).

7. Due to data limitations, foreign investment is measured as the value of U.S. firms’ financial holdings. In contrast, domestic investment is measured using direct estimates of the stock of equipment, structures, inventories, intangibles, and land.

8. Congressional Budget Office, “Taxing Capital Income: Effective Marginal Tax Rates Under 2014 Law and Selected Policy Options” (2014); Congressional Budget Office, “Computing Effective Tax Rates on Capital Income” (2006); Jane Gravelle, “The `Better Way’ House Tax Plan: An Economic Analysis” (Washington: Congressional Research Service, 2017); Jane Gravelle and Donald Marples, “The Effect of Base-Broadening Measures on Labor Supply and Investment: Considerations for Tax Reform” (Washington: Congressional Research Service, 2015); U.S. Treasury Department, “Effective Marginal Tax Rates on New Investments Methodology” (2014), available at https://www.treasury.gov/resource-center/tax-policy/tax-analysis/Documents/New-Investment-Rates-Methodology.pdf; Joseph Rosenberg and Donald Marron, “Tax Policy and Investment by Startups and Innovative Firms” (Washington: Tax Policy Center, 2015).

9. The tax system can still affect business investment through other channels such as the treatment of risk and international shifting of lumpy investments. Moreover, computations of the effective marginal tax rate exclude many features of the tax system and thus do not apply in all circumstances. Perhaps most notably, computations of the effective marginal tax rate typically ignore the role of loss limitations, which can reduce the value of depreciation and interest deductions and limit the extent to which negative tax rates can be realized in practice. However, for an analysis that examines the role of loss limitations, see Rosenberg and Marron, “Tax Policy and Investment by Startups and Innovative Firms.”

10. Michael P. Devereux and Rachel Griffith, “The Taxation of Discrete Investment Choices.” Working Paper W98/16 (The Institute for Fiscal Studies, 1999); Michael P. Devereux and Rachel Griffith, “Evaluating Tax Policy for Location Decisions,” International Tax and Public Finance 10 (2) (2003): 107–126.

11. Laura Power, “The Devil is in the Details: A Comparison of the Corporate Average Effective Tax Rate Calculations Used by Government Agencies.” Working Paper 105 (U.S. Treasury Office of Tax Analysis, 2016).

12. See supra note 8.

13. These rates are taken from U.S. Treasury, “Effective Marginal Tax Rates on New Investments Methodology.”

14. “SOI Tax Stats – Partnership Statistics by Sector or Industry,” available at https://www.irs.gov/uac/soi-tax-stats-partnership-statistics-by-sector-or-industry (last accessed September 2017).

15. This estimate excludes net income from rental real estate activities from partnerships, estates, and trusts in which a partnership is a partner or beneficiary, but includes ordinary income from the sale of property used in rental real estate activities.

16. The ratio of economic depreciation to tax depreciation in the NIPAs applies to the sum of equipment, structures, and certain types of intangible capital. However, for sole proprietorships and partnerships, equipment accounts for a substantial majority of the capital stock.

17. The estimate of economic depreciation used in this calculation is highly uncertain. A larger estimate of economic depreciation would reduce the importance of accelerated depreciation in avoiding business-level tax and increase the importance of interest payments. A smaller estimate would have the opposite effect. In either case, the taxable share would remain modest.

18. Laura Power and Austin Frerick, “Have Excess Returns to Corporations Been Increasing Over Time?” National Tax Journal 69 (4) (2016): 831–846.

19. For an extended version of this argument, see Greg Leiserson, “In Defense of the Statutory U.S. Corporate Tax Rate” (Washington: Washington Center for Equitable Growth, 2017), available at https://equitablegrowth.org/research-analysis/in-defense-of-the-statutory-u-s-corporate-tax-rate/.