A tale of three U.S. employment-to-population ratios

The press received the most recent labor market data from the U.S. Bureau of Labor Statistics late last week as unexpected bad news because employment growth slowed and wage growth continued to be weak. Yet the U.S. unemployment rate sits at 5.1 percent, around its range before the Great Recession. Given the lack of wage growth in the economy, it’s become quite obvious that the current unemployment rate is overstating the health of the U.S. labor market.

But exactly how much further do we have to go? A look at a few different metrics, specifically employment-to-population ratios, might shed some light on the answer.

Perhaps the surest way to know the labor market is approaching full employment is to look at wage growth. Full employment really can’t be pinned down to one specific number, but one would expect to see strong nominal wage growth (before accounting for inflation) consistent with long-run productivity growth. Given that labor productivity growth in the long run is about 1.5 percent, and the inflation rate per the Federal Reserve’s target should be 2 percent over the long term, nominal wage growth should be 3.5 percent at the very least in a healthy labor market. Current wage growth isn’t even close to that threshold yet.

But the problem in waiting for wage growth is that you really don’t know until you get there. As University of Michigan economist Justin Wolfers points out, monetary policy acts on a lag and therefore it shouldn’t ease too much for too long given the potential for inflation to pick up. Now, that might not be so terrible given central banks’ tendencies to take away the punch bowl too early in recent years. But it’d still be nice to have an idea of how much further the labor market has to go.

Enter a new statistic from researchers at the Federal Reserve Bank of Atlanta: the Z-POP. The statistic, formally known as the utilization-to-population ratio, is an attempt by senior policy adviser John Robertson and economic policy analysis specialist Ellyn Terry to build a more accurate representation of how well labor is being used.

The ratio counts a member of the population fully utilized unless they are officially unemployed, working part-time but wanting full-time work, or out of the labor force but wanting a job. So workers who don’t want a job—say, because they’re in school or retired—are counted as fully utilized. As Josh Zumbrun of The Wall Street Journal said on Twitter, it’s like somewhere between the U-6 unemployment rate and the employment-to-population ratio. The Z-POP in September 2015 was 92.1 percent, still below its pre-Great Recession level of 92.7 percent in December 2007.

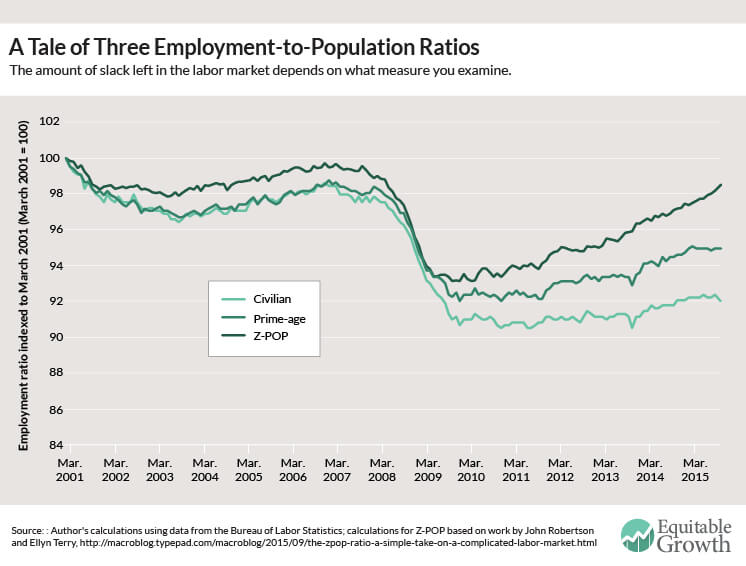

What does this new statistic tell us about the labor market compared to more traditional measures? Take a look at Figure 1, which looks at the relative changes in the Z-POP, the civilian employment-to-population ratio, and the prime-age (25-to-54 year old) employment-to-population ratio since March 2001, the peak before the dotcom-bust recession.

Figure 1

The three measures tell different stories about the pace of the current labor market recovery. The civilian ratio, which looks at the entire working-age population, shows almost no recovery. The obvious problem with this measure is that the population has undergone a demographic transformation as the Baby Boomers have started to retire, pushing down the share of the population with a job. To adjust for this demographic change, we can look at the employment-to-population ratio for workers in their prime working years. That metric shows a more significant recovery, but it has stalled out over the course of 2015. While the Z-POP is also below its pre-recession peak, it’s much closer to that March 2001 level.

So should we believe the Z-POP or the prime-age EPOP? At this point, frankly, it’s hard to tell. The prime-age employment-to-population ratio has a history of predicting wage growth well, but it doesn’t distinguish between workers out of the labor force who want to stay there and those who’d like to jump back in. Either way, both measures indicate that we have a ways to go before seeing a truly healed labor market.