Must-Read: : Yellen Today:

Yellen today: https://t.co/Y11CHp4sso

has come a long way since last September:https://t.co/sMHD4okJqd— Tim Duy (@TimDuy) March 29, 2016

Must-Read: : Yellen Today:

Yellen today: https://t.co/Y11CHp4sso

has come a long way since last September:https://t.co/sMHD4okJqd— Tim Duy (@TimDuy) March 29, 2016

Is it necessary to say that we hold Ben Bernanke, Mervyn King, Mark Carney, Janet Yellen, Stan Fischer, Lael Brainard, and company to the highest of high standards–demand from them constant triple aerial somersaults on the trapeze–because we have the greatest respect for and confidence in them? It probably is…

Back in 1992 Larry Summers and I wrote that pushing the target inflation rate from 5% down to 2% was a very dubious and hazardous enterprise because the zero-lower bound was potentially a big deal: “The relaxation of monetary policy seen over the past three years in the United States would have been arithmetically impossible had inflation and nominal interest rates both been three percentage points lower in 1989. Thus a more vigorous policy of reducing inflation to zero in the mid-1980s might have led to a recent recession much more severe than we have in fact seen…”

This does seem, in retrospect, to have been quite possibly the smartest and most foresightful thing I have ever written. Future historians will, I think, have a very difficult time explaining how the cult of 2%/year inflation targeting got itself established in the 1990s. And they will, I think, have an even harder time explaining why the first monetary policymaker reaction to 2008-2012 was not to endorse Olivier Blanchard et al.’s call for a higher, 4%/year, inflation target in the coded terms of IMF speak:

The great moderation (Gali and Gambetti 2009) lulled macroeconomists and policymakers alike in the belief that we knew how to conduct macroeconomic policy. The crisis clearly forces us to question that assessment….

The crisis has shown that large adverse shocks do happen. Should policymakers aim for a higher target inflation rate in normal times, in order to increase the room for monetary policy to react to such shocks? Are the net costs of inflation much higher at, say, 4% than at 2%, the current target range? Is it more difficult to anchor expectations at 4% than at 2%? Achieving low inflation through central bank independence has been a historic accomplishment. Thus, answering these questions implies carefully revisiting the benefits and costs of inflation.

A related question is whether, when the inflation rate becomes very low, policymakers should err on the side of a more lax monetary policy, so as to minimize the likelihood of deflation, even if this means incurring the risk of higher inflation in the event of an unexpectedly strong pickup in demand. This issue, which was on the mind of the Fed in the early 2000s, is one we must return to…

But instead we got a very different reaction. Sudeep Reddy reported on it back in 2009:

(2009): Sen. Vitter Presents End-of-Term Exam For Bernanke: “Earlier this month, Real Time Economics presented questions from several economists…

…for the confirmation hearing of Federal Reserve Chairman Ben Bernanke…. Sen. David Vitter (R., La.) submitted them in writing and received the responses from Bernanke….

D. Brad Delong, University of California at Berkeley and blogger: Why haven’t you adopted a 3% per year inflation target?

[Bernanke:] The public’s understanding of the Federal Reserve’s commitment to price stability helps to anchor inflation expectations and enhances the effectiveness of monetary policy, thereby contributing to stability in both prices and economic activity. Indeed, the longer-run inflation expectations of households and businesses have remained very stable over recent years. The Federal Reserve has not followed the suggestion of some that it pursue a monetary policy strategy aimed at pushing up longer-run inflation expectations.

In theory, such an approach could reduce real interest rates and so stimulate spending and output. However, that theoretical argument ignores the risk that such a policy could cause the public to lose confidence in the central bank’s willingness to resist further upward shifts in inflation, and so undermine the effectiveness of monetary policy going forward.

The anchoring of inflation expectations is a hard-won success that has been achieved over the course of three decades, and this stability cannot be taken for granted. Therefore, the Federal Reserve’s policy actions as well as its communications have been aimed at keeping inflation expectations firmly anchored.

This sounds like nothing so much as the explanations offered in the 1920s and 1930s for returning to and sticking with the gold standard at pre-WWI parities, and the explanations offered at the start of the 1990s by British Tories for sticking to the fixed parities of the then-Exchange Rate Mechanism. The short answer is that real useful positive credibility is not built by attempts to stick to policies that are in the long run destructive–and hence both incredible and stupid. As we learn more about the economy and as the structure of the economy changes, the optimal long-run policy strategy changes as well. Credibility arising from a commitment that the Federal Reserve will seek to follow an optimal long-run policy framework and to accurately convey its intentions but will revise that framework in light of knowledge and events is worth gaining and maintaining. Credibility arising from a commitment to stick, come hell or high water, to a number that Alan Greenspan essentially pulled out of the air with next to no substantive analytical backing in terms of optimal-control analysis is not.

Now, however, we have another answer from Janet Yellen: that the zero lower bound is not, in fact, such a big deal:

: The Outlook, Uncertainty, and Monetary Policy: “One must be careful, however, not to overstate the asymmetries affecting monetary policy at the moment…

…Even if the federal funds rate were to return to near zero, the FOMC would still have considerable scope to provide additional accommodation. In particular, we could use the approaches that we and other central banks successfully employed in the wake of the financial crisis to put additional downward pressure on long-term interest rates and so support the economy–specifically, forward guidance about the future path of the federal funds rate and increases in the size or duration of our holdings of long-term securities.10 While these tools may entail some risks and costs that do not apply to the federal funds rate, we used them effectively to strengthen the recovery from the Great Recession, and we would do so again if needed.

Over on the Twitter Machine, the very-sharp Tim Duy–I take it from his picture that there is ample snowpack for the ski resorts in the Cascade Range–is impressed by how different the tone of this speech is with the get-ready-for-liftoff speeches of last fall:

Yellen today: https://t.co/Y11CHp4sso

has come a long way since last September:https://t.co/sMHD4okJqd— Tim Duy (@TimDuy) March 29, 2016

And Dario Perkins and Mark Grady have chimed in in support: “suddenly she’s realised the rest of the world matters!…” and “lots of common messages, but emphasis v[ery] diff[erent] on the risks. And no mention of lags or falling behind the curve at all…”

I, by contrast, am still struck by the gap that remains between where she seems to be and where I am.

For there is a natural next set of questions to ask anyone who says that the zero lower bound and the liquidity trap are not big deals. That set is:

Why is the five-year ahead five-year market inflation outlook so pessimistic?

Why hasn’t the Federal Reserve pushed interest rates low enough so that investment as a whole counterbalances the collapse in government purchases we have seen since 2010?

I cannot help but be struck by the difference between what I see as the attitude of the current Federal Reserve, anxious not to do anything to endanger its “credibility”, and the Greenspan Fed of the late 1990s, which assumed that it had credibility and that because it had credibility it was free to experiment with policies that seemed likely to be optimal in the moment precisely because markets understood its long-term objective function and trusted it, and hence would not take short-run policy moves as indicative of long-run policy instability. There is a sense in which credibility is like a gold reserve: It is there to be drawn on and used in emergencies. The gold standard collapsed into the Great Depression in the 1930s in large part because both the Bank of France and the Federal Reserve believed that their gold reserves should never decline, but always either stay stable of increase.

It was Mark Twain who said that although history does not repeat itself, it does rhyme. The extent to which this is true was brought home to me recently by Barry Eichengreen’s excellent Hall of Mirrors…

I tell you, I have a brand new set of lectures to write for a large monetary-policy module in American Economic History…

Must-Read: Back in 1992 Larry Summers and I wrote that pushing the target inflation rate from 5% down to 2% was a very dubious and hazardous enterprise because the zero-lower bound was potentially a big deal: “The relaxation of monetary policy seen over the past three years in the United States would have been arithmetically impossible had inflation and nominal interest rates both been three percentage points lower in 1989. Thus a more vigorous policy of reducing inflation to zero in the mid-1980s might have led to a recent recession much more severe than we have in fact seen…”

Now we have an answer from Janet Yellen: that the zero lower bound is not, in fact, such a big deal:

: The Outlook, Uncertainty, and Monetary Policy: “One must be careful, however, not to overstate the asymmetries affecting monetary policy at the moment…

…Even if the federal funds rate were to return to near zero, the FOMC would still have considerable scope to provide additional accommodation. In particular, we could use the approaches that we and other central banks successfully employed in the wake of the financial crisis to put additional downward pressure on long-term interest rates and so support the economy–specifically, forward guidance about the future path of the federal funds rate and increases in the size or duration of our holdings of long-term securities.10 While these tools may entail some risks and costs that do not apply to the federal funds rate, we used them effectively to strengthen the recovery from the Great Recession, and we would do so again if needed.

The natural next question to ask then is: Then why isn’t nominal GDP on its pre-2008 trend growth path? Why is the five-year ahead five-year market inflation outlook so pessimistic? Why hasn’t the Federal Reserve pushed interest rates low enough so that investment as a whole counterbalances the collapse in government purchases we have seen since 2010?

Must-Read: : The Fed’s Credibility Dilemma: “What will happen if inflationary pressures prove stronger than expected…

…over the next year or so. In principle, the Fed can curb inflation by raising its interest-rate target sufficiently rapidly. In practice… it must break either its commitment to move gradually, or to keep inflation close to 2 percent… [and] will lose credibility. Worse, suppose that economic growth turns out to be weaker…. Again… communication becomes an obstacle: By expressing its strong preference for normalization, the Fed has been telling investors that they can safely ignore the possibility of a reduction in rates (at the end of her March 16 press conference, for example, Chair Janet Yellen stressed that officials are not even discussing the possibility of adding stimulus). So to respond appropriately… the Fed would have to renege….

Ironically, the Fed’s perceived commitment not to cut interest rates could actually make it reluctant to raise them…. To maintain flexibility… they might choose not to raise rates in the first place. That way they’ll run a smaller risk of being forced to go back on their normalization commitment. So what, if any, plans should the Fed communicate?… They should be much clearer about their willingness to make large and rapid changes in monetary policy… stress that they are ready to do ‘whatever it takes’ to keep employment up and inflation near target…

Nouriel Roubini writes:

: “Worries about a hard landing in China… China is more likely to have a bumpy landing than a hard one…

…[but] investors’ concerns have yet to be laid to rest…. Emerging markets are in serious trouble…. The Fed probably erred in exiting its zero-interest-rate policy in December…

And it is not clear how the Federal Reserve can correct what is now widely-recognized as a probable error.

First, the Federal Reserve would have to be willing to admit that the asymmetric loss function meant that exiting zero last December was a probable error.

It was a probable error in retrospect today, and was unwise in prospect last December. Right now we are worried about global deflation. It is difficult to envision an alternative counterfactual scenario today in which we are equally worried about global inflation and equally regret that the Federal Reserve did not exist zero last December. When there is a substantial loss associate with a Type A error and only a minor loss associated with a Type B error, one risks making the Type B error unless the odds are overwhelming. The odds last December were to overwhelming.

The problem for the Federal Reserve is that admitting it made a policy error last December requires an all-but-explicit climbdown from the last two years’ worth of public risk judgments, and an explanation of why, given the obvious asymmetries, those public risk judgments were explained. And there is no face-saving way to undertake such a climbdown.

Second, the Federal Reserve would have to take steps to neutralize the contractionary pressure its policy move in December and the previous telegraphing of that move have put on the world economy. And that would be a difficult task indeed.

It looks like Ben Bernanke is about to go through the options. And that will definitely be worth reading.

Must-Read: : The Fed and the Quest to Raise Rates: “The justification for raising rates is to prevent inflation from getting out of control…

…but inflation has been running well below the Fed’s 2.0 percent target for years. Furthermore, since the 2.0 percent target is an average inflation rate, the Fed should be prepared to tolerate several years in which the inflation rate is somewhat above 2.0 percent… [and] allow for a period in which real wage growth slightly outpaces productivity growth in order to restore the pre-recession split between labor and capital…. The most recent data provide much more reason for concern that the economy is slowing more than inflation is accelerating….

There are many other measures indicating that there continues to be considerable slack in the labor market despite the relatively low unemployment. There are no plausible explanations for the sharp drop in the employment rate of prime-age workers at all education levels from pre-recession levels, apart from the weakness of the labor market. The amount of involuntary part-time employment continues to be unusually high…. And the duration measures of unemployment spells and the share of unemployment due to voluntary quits are both much closer to recession levels than business cycle peaks…

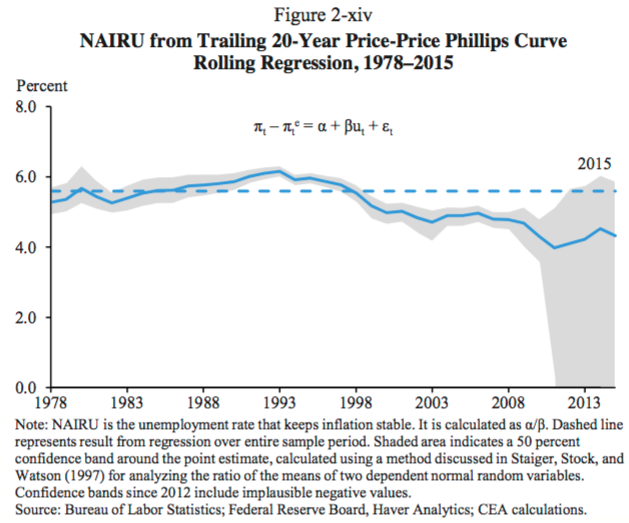

Must-Read: When I look at these five graphs below, this paragraph from Stan Fischer seems to me to be simply the wrong one-paragraph summary of the issues. Just wrong:

: Reflections on Macroeconomics Then and Now: “Estimated Phillips curves appear to be flatter than they were estimated to be many years ago…

…in terms of the textbooks, Phillips curves appear to be closer to what used to be called the Keynesian case (flat Phillips curve) than to the classical case (vertical Phillips curve). Since the U.S. economy is now below our 2 percent inflation target, and since unemployment is in the vicinity of full employment, it is sometimes argued that the link between unemployment and inflation must have been broken. I don’t believe that. Rather the link has never been very strong, but it exists, and we may well at present be seeing the first stirrings of an increase in the inflation rate–something that we would like to happen.

https://www.whitehouse.gov/sites/default/files/docs/ERP_2016_Book_Complete%20JA.pdf | https://www.evernote.com/l/AAE6xHSsx8VH54YkkTp_visEwoz4UEAKtxwB/image.png

Must-Read: Very nice. But why “Galilean”, Gavyn? I do note that in the end Gavyn’s “insider” argument boils down to “we must keep the hawks on the FOMC on board with policy”, which is a declaration that:

Also, “we have already allowed for these asymmetrical risks by holding interest rates below those suggested by the Taylor Rule for a long time” is simply incoherent: sunk costs do not matter for future actions.

The dialogue:

: Splits in the Keynesian Camp: a Galilean Dialogue: “As Paul Krugman pointed out a year ago…

…a sharp difference of views about US monetary policy has developed between two camps of Keynesians who normally agree about almost everything. What makes this interesting is that, in this division of opinion, the fault line often seems to be determined by the professional location of the economists concerned. Those outside the Federal Reserve (eg Lawrence Summers, Paul Krugman, Brad DeLong) tend to adopt a strongly dovish view, while those inside the central bank (eg Janet Yellen, Stanley Fischer, William Dudley, John Williams) have lately taken a more hawkish line about the need to ‘normalise’ the level of interest rates [1]. My colleague David Blake suggested that this blog should carry a Galilean ‘Dialogue’ between representatives of the two camps. Galileo is unavailable this week, but here goes”

Fed Insider: The US has now reached full employment and the labour market remains firm. The Phillips Curve still exists, so wage inflation is headed higher. Core inflation is not far below the Fed’s 2 per cent target. While the economy is therefore close to normal, interest rates are far below normal, so there should be a predisposition to tighten monetary conditions gradually from here. That would still leave monetary policy far more accommodative than normal for a long period of time.

Fed Outsider: I am not so sure about the Phillips Curve. It seems much flatter than it was in earlier decades. But in any case you do not seem to have noticed that the economy is slowing down. This is probably because of the increase in the dollar, which has tightened monetary conditions much more than the Fed intended. The Fed should not make this slowdown worse by raising domestic interest rates as well.

Insider: I concede that the economy has slowed, and I am worried about the tightening in financial conditions caused by the dollar. But I think that this will prove temporary. The dollar effect will not get much worse from here, and the economy has also been affected by inventory shedding and the drop in shale oil investment. As these effects subside, GDP growth will return to above 2 per cent. The pace of employment growth may slow, but remember that payrolls need to grow by under 100,000 per month to keep unemployment constant at the natural rate. Some slowdown is not only inevitable, it is desirable.

Outsider: I do not know how you can be so confident that growth will recover. All your forecasts for growth in recent years have proven far too optimistic. You should be worried that the economy is stuck in a secular stagnation trap. The equilibrium real interest rate is lower than the actual rate of interest. To emerge from secular stagnation, the Fed should be cutting interest rates, not raising them.

Insider: The case for secular stagnation is a bit extreme. Economies tend to return to equilibrium after shocks. The US has been held back by a series of major headwinds since 2009, but these are now abating. Fiscal policy is easing, the euro shock is healing and deleveraging is ending. As these headwinds abate, the equilibrium real rate of interest will return to its normal level around 1.5 per cent, so the nominal Fed funds rate should be 3.5 per cent. It is right to warn people now that this is likely to happen.

Outsider: The hawkish forward guidance shown in your ‘dot plot’ will slow demand growth further. It is unnecessary – in fact, outright damaging. I am pleased that you are rethinking the presentation of the dots. But, more important, the economic recovery is already long in the tooth. There is a 60 percent chance of a recession within 2 years. In a normal recession, the Fed has to cut interest rates by 4 percentage points. Because of the zero lower bound, it will not be able to do so in the next recession, so it needs to avoid a recession at all costs.

Insider: Oh dear. Recoveries do not die of old age, as Glenn Rudebusch at the San Francisco Fed has just conclusively proved. Expansions, like Peter Pan, do not grow old. Provided that we avoid a build up of inflation pressures, or excessive risk taking in markets, there is no reason to believe that this recovery will spontaneously run out of steam. It is much more likely to persist.

Outsider: Maybe, but have you ever considered the possibility that you might be wrong? The future path of the equilibrium interest rate is subject to huge uncertainty, as your own estimations demonstrate. If you kill this recovery, it will subsequently be impossible to use monetary policy to get out of recession. If, on the other hand, you allow inflation to rise, you can easily bring it back under control, simply by raising interest rates. So the risks are not symmetrical.

Insider: Well, we have already allowed for these asymmetrical risks by holding interest rates below those suggested by the Taylor Rule for a long time. And anyway I do not agree with you about inflation risks. If we allow inflation to become embedded in the system, we will then have to raise interest rates abruptly. That is the most likely way that this recovery can end in a severe recession.

Outsider: Inflation cannot rise permanently unless inflation expectations rise as well. In case you have not noticed, inflation expectations have been falling and are now out of line with your 2 per cent inflation target. This is dangerous because real (inflation adjusted) interest rates are actually rising when they should be falling.

Insider: I used to worry a lot about the inflation expectations built into the bond market, but I now think that these are affected by market imperfections that should be downplayed. Inflation expectations in the household and corporate sectors are still broadly in line with the Fed target. And, anyway, I am increasingly concerned that inflation could rise because productivity growth is now so low. With the economy at full employment, inflation pressures could be building, even with GDP growth still very subdued.

Outsider: I am also very worried about the slowdown in productivity growth. But I think this could be happening because you have allowed the actual GDP growth rate to be so low for so long. Because of hysteresis, you may be making things progressively worse. You may have permanently shifted the equilibrium of the economy in a bad direction.

Insider: I am not so sure about this hysteresis stuff. I would not rule it out entirely. But you cannot rely on the Fed to solve all of our economic problems. At the moment, the Fed’s main priority is to return monetary policy to normal, and I am determined to continue this process unless something really bad happens to the economy.

Outsider: In that case, something bad is quite likely to happen. It seems that it will take a disaster to shake your orthodoxy. Do you really want to be responsible for making a historic economic mistake?

Insider: It is easy for you on the outside to make dramatic points like that. If you had been entrusted with the responsibility of office, you would be more circumspect. Although we went to the same graduate school, we are now in different positions. The hawks on the FOMC need to be kept on board with the majority. And I do not want to inflame the Fed’s Republican critics in Congress by appearing soft on inflation. That means I sometimes have to make difficult compromises that you do not have to make.

Outsider: The hawks are giving too much weight to the health of the banks. You should be worrying more about Main Street, and less about Wall Street.

Must-Read: Narayana Kocherlakota has been on quite a roll recently:

: What We’ve Learned About Unconventional Monetary Policy: “Lesson 1: Even over relatively long periods of time…

…unconventional monetary policy tools don’t have extreme downside risks…. Lesson 2: Central banks are able to guide inflation close to its desired level using unconventional tools…. One could certainly ask: why was the FOMC consistently aiming for such a low inflation rate in this time frame, given that they expected such a high unemployment rate? (I have posed that question here.) But let’s leave that question aside. Throughout much of the 2008-10 period, many observers outside of the Fed expressed strong concerns about the risk of unduly high or unduly low inflation. Given that level of background uncertainty, I would say that the FOMC did a very good job at using unconventional tools to achieve what policymakers wanted in terms of inflation outcomes. Lesson 3: Hitting inflation objectives does not translate into hitting growth objectives…

Plus:

: Interest Rate Increases Are Hard to Undo?: “Yellen made the following statement…

I do not expect that the FOMC [Federal Open Market Committee] is going to be soon in the situation where it is necessary to cut rates….

I argue that her statement suggests that the FOMC’s policy moves will be inappropriately insensitive to adverse information about the evolution of the economy…. There’s some set of economic conditions for which a range of a quarter to half a percent for the target range for the fed funds rate is appropriate. Under an appropriately data-sensitive approach… the FOMC should slightly lower the fed funds rate target range if it confronts a slightly worse set of economic conditions [than that]…. If a move of zero is highly likely, surely a downward move of a quarter percent point should be more than a little possible? But Chair Yellen’s statement suggests that this isn’t the way that the FOMC is thinking about the situation…. She seems to be saying that it will take a pretty bad turn of events for the FOMC to be willing to reverse its December move. Such an approach means that the FOMC’s December has created a new higher floor….

The FOMC could be a lot more data-sensitive than I’ve described when it considers interest rate cuts. Failing that, the other response is to realize that any future rate increase will push upwards on the new soft floor. That realization should make the FOMC very cautious about undertaking any future rate increase.

And:

: Negative Rates: A Gigantic Fiscal Policy Failure: “Since October 2015, I’ve argued that the Federal Open Market Committee (FOMC)…

…should reduce the target range for the fed funds rate below zero. Such a move would be appropriate for three reasons:

- It would facilitate a more rapid return of inflation to target.

- It would help reduce labor market slack more rapidly.

- It would slow and hopefully reverse the ongoing and dangerous slide in inflation expectations.

So, going negative is daring but appropriate monetary policy. But it is a sign of a terrible policy failure by fiscal policymakers.

The reason that the FOMC has to go negative is because the natural real rate of interest r* (defined to be the real interest rate consistent with the FOMC’s mandated inflation and employment goals) is so low. The low natural real interest rate is a signal that households and businesses around the world desperately want to buy and hold debt issued by the US government. (Yes, there is already a lot of that debt out there – but its high price is a clear signal that still more should be issued.) The US government should be issuing that debt that the public wants so desperately and using the proceeds to undertake investments of social value.

But maybe there are no such investments? That’s a tough argument to sustain quantitatively. The current market real interest rate – which I would argue is actually above the natural real rate r* – is about 1% out to thirty years. This low natural real rate represents an incredible opportunity for the US. We can afford to do more to ensure that all of our cities have safe water for our children to drink. We can afford to do more to ensure that our nuclear power plants won’t spring leaks. We can afford to do more to ensure that our bridges won’t collapse under commuters.

These opportunities barely scratch the surface. With a 30-year r* below 1%, our government can afford to make progress on a myriad of social problems. It is choosing not to.

If the government issued more debt and undertook these opportunities, it would push up r*. That would make life easier for monetary policymakers, because they could achieve their mandated objectives with higher nominal interest rates. But, more importantly, the change in fiscal policy would make life a lot better for all of us.

I don’t think that Chair Yellen will say the above in her Humphrey-Hawkins testimony tomorrow – but I also think that it would be great if she did.

: Dovish Actions Require Dovish Talk (To Be Effective): “The Federal Open Market Committee (FOMC) has bought a lot of assets and kept interest rates extraordinarily low…

…Yet all of this stimulus has accomplished surprisingly little (for example, inflation and inflation expectations remain below target and are expected to do so for years to come)…. Over the past seven years, the FOMC’s has consistently talked hawkish while acting dovish. This communications approach has weakened the effectiveness of policy choices, probably in a significant way…. In December 2008, the FOMC lowered the fed funds rate target range to 0 to a quarter percent. It did not raise the target range until December 2015, when the unemployment rate had fallen back down to 5%. But – with the benefit of hindsight – a shocking amount of this eight years’ worth of unprecedented stimulus was wasted, because it was largely unanticipated by financial markets…

Must-Read: But being “behind the cycle” is good, no? On a lee shore you need more sea room, lest the wind strengthen, no?

: FOMC Minutes and More: “The Fed may be turning toward my long-favored policy position…

…the best chance they have of lifting off from the zero bound is letting the economy run hot enough that inflation becomes a genuine concern. That means following the cycle, not trying to lead it. And I would argue that if the recession scare is just that, a scare, they are almost certainly going to fall behind the curve. The unemployment rate is below 5 percent and wage pressures are rising. The economy is already closing in on full-employment. If we don’t have a recession, then how much further along will the economy be by the time the Fed deems they are sufficiently confident in the economy that they can resume raising rates? And note the importance of clearly progress on inflation….

Bullard noted that the FOMC has repeatedly stated in official communication and public commentary that future monetary policy adjustments are data dependent. He then addressed the possibility that the financial markets may not believe this since the SEP may be unintentionally communicating a version of the 2004-2006 normalization cycle, which appeared to be mechanical…. You might forgive market participants for believing that the SEP infers some calendar-based guidance when Federal Reserve Vice Chair Stanley Fischer says things like:

WELL, WE WATCH WHAT THE MARKET THINKS, BUT WE CAN’T BE LED BY WHAT THE MARKET THINKS. WE’VE GOT TO MAKE OUR OWN ANALYSIS. WE MAKE OUR OWN ANALYSIS AND OUR ANALYSIS SAYS THAT THE MARKET IS UNDERESTIMATING WHERE WE ARE GOING TO BE. YOU KNOW, YOU CAN’T RULE OUT THAT THERE IS SOME PROBABILITY THEY ARE RIGHT BECAUSE THERE’S UNCERTAINTY. BUT WE THINK THAT THEY ARE TOO LOW.

Saying the markets are wrong implies that the policy direction is fairly rigid. In any event, I am not confident there is yet much support for Bullard’s position…. Bullard has also gone full-dove. He remembered that he thought inflation expectations were supposed to be important, and the decline in 5-year, 5-year forward expectations has him spooked. And he thinks that the excess air has been released from financial markets, so his fears of asset bubbles has eased. Hence, the Fed can easily pause now….

Bottom Line: The Fed is on hold, stuck in risk management mode until the skies clear. If you are in the ‘recession’ camp, the path forward is obvious. The Fed cuts back to zero, drags its heals on more QE, and fumbles around as they try to figure out if negative rates are a good or bad thing. Not pretty. But if you are in the ‘no recession’ camp, it’s worth thinking about the implications of a Fed pause now on the pace of hikes later. Being on hold now raises the risk that by the time the Fed moves again, they will be behind the cycle.

{kind=link}