Overview

Over the past 20 years, major sectors of the U.S. economy have undergone sweeping consolidation, from airlines to brewing, cable television to drug companies, eyeglasses to finance, and grocery stores to hospitals to industrial chemicals—nearly the entire alphabet of industries in the United States. In many cases, this consolidation has reduced the number of significant competitors in these industries to only three or four, prompting concerns about diminished competition, higher prices, and a range of other harms to the U.S. economy and society. Highlighting these concerns the Obama administration, last year, issued an unprecedented executive order that instructed agencies to ensure that competition plays a role in their policy actions.1 Backing up that executive order was an issue brief from the White House Council of Economic Advisers, or CEA, titled “Benefits of Competition and Indicators of Market Power”—a title whose significance was lost on no one.2

Download FileU.S. antitrust and competition policy amid the new merger wave

Read the full report PDF in your browser

This dramatic and well-documented increase in concentration raises the question about its causes. Could it simply be the unfortunate side effect of the rise of information technology and network industries that typically do not support numerous firms? It’s certainly the case that those sectors of the economy have grown in visibility and importance, yet consolidation has affected lots of other, more traditional industries as well. Perhaps, then, the decline in competitiveness is due to the increased prevalence of barriers to entry used by incumbent firms to forestall competition by others. There is certainly evidence of this as well—some cited by CEA—but again, this appears to be localized in specific sectors. A third possible explanation is the role of antitrust policy, specifically the ways in which it has changed and permitted the emergence of ever-larger firms.

Without disputing the role of other factors, this report focuses on this last factor. Antitrust, of course, has a long and settled history in the United States, with some of the original legislation dating back to 1890. The key merger control statute in 1914—amended and strengthened in 1950—prohibits consolidations whose effect “may be substantially to lessen competition, or to tend to create a monopoly.”3 Much economic and legal analysis, together with precedent and evidence, have gone into making that objective operational. While enforcement priorities have shifted over time and with different presidential administrations, the fundamental importance of antitrust has rarely been disputed.

That said, this report will document that merger enforcement in recent times has narrowed its focus to those mergers at the very highest levels of concentration and adopted a substantially more permissive stance toward mergers that consolidate industries up to that point. Evidence also shows this more permissive view of consolidation is likely to result in higher prices and other competitive harms. Antitrust enforcement has, in short, shifted its enforcement priorities in ways that now permit ever more mergers, raising real competitive concerns.

The roots of this policy shift also will be examined. One likely factor has been resource constraints affecting the two federal antitrust agencies—the Federal Trade Commission, or FTC, and the Antitrust Division of the U.S. Department of Justice. Budgets have not kept pace with the number of complex antitrust issues over time. Another factor is the increasing judicial emphasis on avoiding so-called Type I errors—the possibility of erroneously challenging benign or even pro-competitive mergers. One method for minimizing Type I errors, of course, is simply to bring fewer cases against mergers whose anti-competitive potential is not entirely certain. Yet other reasons for this shift may be found in changes in economic thinking about mergers and the increasingly sophisticated techniques for analyzing them, which may be directing attention to an unduly narrow set of questions about the effects of mergers.

Common to both of these factors is a revolution in thinking about which mergers should be challenged—a revolution that has transformed the underpinnings of policy but that now has taken some useful changes to excess. This report will review these changes in concentration, in thinking, and in policy in three steps. First, it will document growing concentration in an array of sectors of the economy, such as those listed at the outset. Secondly, it will demonstrate the increasingly permissive stance of antitrust enforcement toward higher concentration in these industries. And finally, it will explain some of the economic and policy bases for this transformation, which by implication suggest ways of restoring and strengthening antitrust as the guardian of competition in our economy. Among these are a stronger presumption against mergers in already concentrated industries and a renewed determination to challenge mergers at the enforcement margin.

The rise of concentration

Several recent studies show that concentration increased in a large number of industries and sectors over the past 20 years. As noted above, the 2016 issue brief by the Council of Economic Advisers reported supporting data about rising concentration both at the broad sectoral level and for several specific industries. One set of data showed that the share of revenues among the top 50 firms rose in 10 of 13 sectors of the U.S. economy between 1997 and 2012. The CEA issue brief notes that these data are at a broad level, but the findings are corroborated by a number of other reports and studies. The Economist, for example, reported on changes in concentration for more than 900 sectors of the U.S. economy over the same period.4 Fully two-thirds of these sectors became more concentrated during this period, with the share of revenue among the top four firms rising an average of 6 percentage points. By contrast, the revenue share among fragmented indus-tries dropped 14 percentage points. Nearly one-tenth of all economic activity now arises in industries where the top four firms control more than two-thirds of sales. Noting further the persistence of profits at these large firms, The Economist concluded, “America needs a giant dose of competition.”

Some analysts questioned these data, but most of these criticisms have been answered by other recent studies. Economists David Autor at the Massachusetts Institute of Technology, David Dorn at the University of Zurich, Lawrence Katz at Harvard University, and Christina Patterson and John Van Reenen at MIT examine concentration changes throughout the U.S. economy from 1982 to 2012.5 For each of 676 industries in six broad sectors, they develop data on three different measures of concentration, both for purely U.S.-based firms and after controlling for imports. Across all of these measures, for each sector of the economy, their study details “a remarkably consistent upward trend in concentration in each sector.” Four-firm concentration—the share of industry revenues controlled by the largest four firms—rose from 38 percent to 43 percent in manufacturing, from 24 percent to 35 percent in finance, from 11 percent to 15 percent in utilities, from 29 percent to 37 percent in retail trade, and from 22 percent to 28 percent in wholesale trade.

Further analysis by economists Gustavo Grullon at Rice University, Yelena Larkin at York University, and Roni Michaely at Cornell University uses stock market data on publicly traded firms aggregated to their respective industries and reports on changes in concentration—measured by the Herfindahl-Hirschman Index, or HHI, a measure of overall industry concentration6—over the past 40 years.7 They find that computed HHIs in manufacturing industries declined from the beginning of the 1980s until the late 1990s, a decline they attribute to reductions in regulation and tariffs. But thereafter, HHIs increased by 50 percent—a change that was widespread throughout all industries. This study also reports that the absolute number of publicly traded firms in the United States decreased by about 50 percent over the past two decades, underscoring concerns about diminished opportunities to enter markets voiced in the CEA issue brief.

While each of these studies has its limitations, the totality of this body of work provides a compelling portrayal of rising concentration throughout large segments of the U.S. economy over the past 20 years. Complemented by evidence of high and persistent profits accumulated by large companies and by evidence of the rise of entry barriers and diminished rates of entry—both also documented in the CEA issue brief—many antitrust experts and policymakers have concluded that competition in the U.S. economy has been in retreat.

The decline of enforcement

This report already noted several possible causes of rising concentration and reduced competition. Without disputing these other causes, the role of changing antitrust policy and enforcement practices is equally important. Specifically, broad changes in merger control policy at the Federal Trade Commission and the Antitrust Division at the U.S. Department of Justice have contributed to these outcomes.

The connection between merger policy and concentration can be documented from enforcement data published by the FTC. These data cover all reported mergers that are subject to so-called second requests, which are document demands made by the agency in cases where proposed mergers raise sufficient competitive concerns as to justify full investigations.8 The FTC first released enforcement data covering the years 1996 through 2003, and then followed up with data from 1996 through 2005, then through 2007, and finally through 2011.9 Over that entire period, the FTC investigated a total of 264 horizontal mergers—that is, mergers between direct competitors involving some 1,359 “antitrust markets,” or markets that are typically considerably narrower than everyday definitions of markets or industries. Of these, the agency brought some type of enforcement action in 1,055 cases, or 77.6 percent of the total. “Enforcement actions,” according to the FTC, include not just formal legal challenges, which are few in number, but also instances in which mergers are approved subject to remedies, as well as also voluntary withdrawals of merger proposals by the parties in the face of likely opposition.

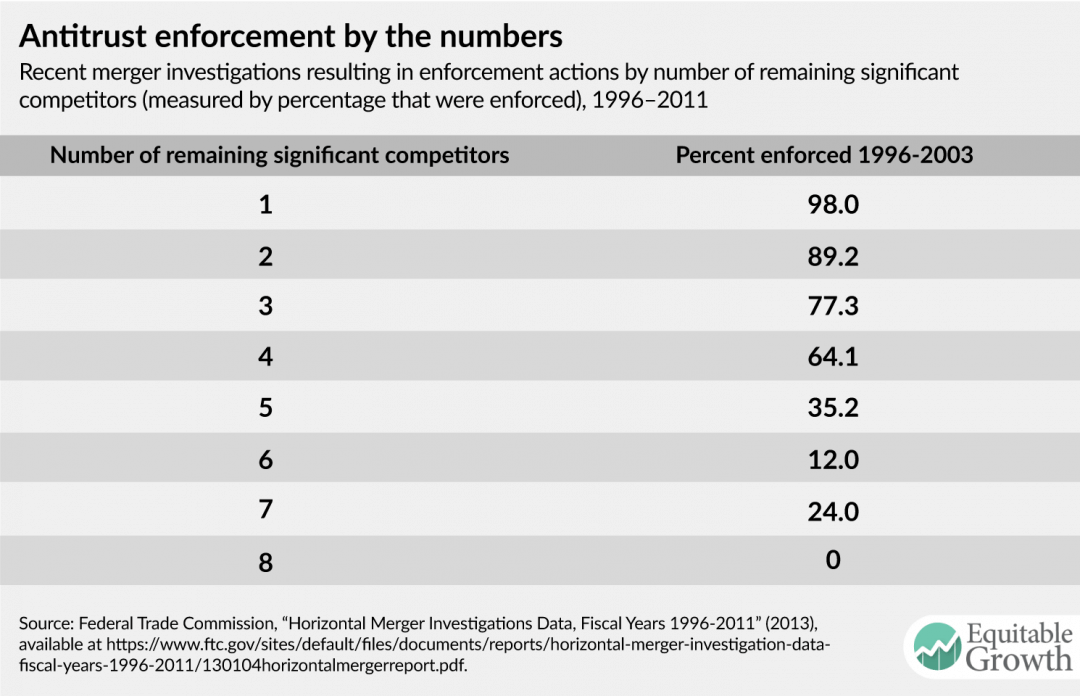

The FTC breaks down these data on investigations and enforcement by several characteristics of the relevant antitrust markets, including their measured concentration. The two basic concentration measures are the previously mentioned HHI and the number of remaining significant competitors after the proposed merger. The FTC defines a significant competitor as “a firm whose independence could affect the ability of the merged firms to achieve an anticompetitive result” and suggests that a cutoff of 10 percent might roughly define such a firm. (See Table 1.)

Table 1

Table 1 reports the frequency of enforcement actions in these merger investigations over the entire 16-year period according to the number of remaining significant competitors. As is clear—and certainly to be expected—the rate of enforcement actions declines systematically as the number of remaining significant competitors increases. Thus, virtually all mergers to monopoly prompt agency action. Those with three or four remaining competitors elicit actions in two-thirds to three-quarters of cases, while even those with six or seven remaining competitors are subject to enforcement actions in a significant fraction of cases.

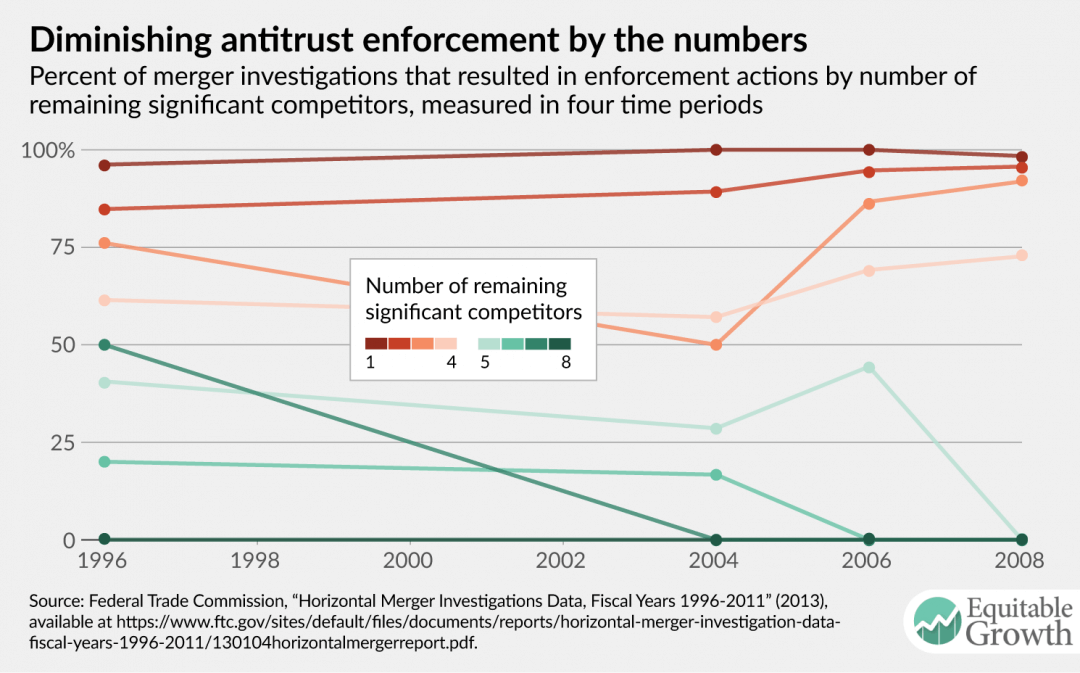

On their face, these data suggest a vigorous enforcement policy, properly directed at the most problematic mergers. But a closer look at the data reveals a somewhat different reality. As noted, the data on investigations and enforcement are reported on a cumulative basis from 1996 through four different end dates. Simple differencing of the totals permits calculation of enforcement rates in each subperiod—that is, from 1996 through 2003, then for 2004 and 2005, for 2006 and 2007, and from 2008 through 2011. Those enforcement rates over time are shown in Figure 1 and reveal a sharp bifurcation in FTC enforcement practice. For mergers result-ing in four or fewer remaining significant competitors, enforcement rates not only remained high but also increased marginally over time.

But for mergers in the high-to-moderate range of concentration, where the number of remaining significant competitors was more than four, the FTC data tell quite a different story. Here, not only did enforcement fall throughout this 16-year period, but by the final four reported years, enforcement had quite literally ceased. That is, for mergers resulting in five competitors, the rate of enforcement varied between about 30 percent and 45 percent through 2007, after which the rate went to zero. Actions against mergers with six remaining competitors ceased even earlier, in 2005, and for those with seven, there were zero enforcement actions after 2003. (See Figure 1.)

Figure 1

The implication of this finding seems incontrovertible: By permitting mergers in this mid-to-high range of industry concentration, merger policy has directly contributed to the rise in measured concentration in the economy overall.

These data have some limitations. They reflect only FTC actions, not those of the Department of Justice, and they do not extend fully to the present time. But they do cover an important period of consolidation in the U.S. economy documented in the previously cited studies. Moreover, while no single example can illustrate this paradigm shift perfectly, anecdotal evidence can be found in the record of both antitrust agencies.

One noteworthy example concerns the airline industry, where the Department of Justice has historically opposed most mergers. It did so in several proposed mergers in the late 1980s and more recently in US Airways’ proposed acquisition of United Airlines Inc. in 2001. As a result, 10 years ago, there were six major legacy airlines; a large seventh carrier, Southwest Airlines Co.; plus several low-cost carriers that provided considerable pricing discipline.

In 2008, however, Delta Air Lines Inc. and Northwest Airlines announced their intent to merge, and to the surprise of many observers, the Department of Justice permitted that merger to go forward. That in turn encouraged other carriers to attempt merging as well, and indeed United Airlines and Continental Airlines did so in 2010—combining under the United brand name—followed by Southwest and AirTran Airways in 2011, now Southwest Airlines Co., and American Airlines Inc. and US Airways in 2013, now American Airlines Inc. Thus, over a period of five years, mergers eliminated three legacy carriers plus a significant low-cost competitor.

The Department of Justice’s antitrust policy decision first permitted a merger reducing the number of significant competitors from seven to six, followed by a six-to-five merger, then another reducing the number to four. Some of these mergers would have faced a significant likelihood of challenge in the past—almost certainly the last two of them—but all of these mergers down to four remaining competitors were in fact permitted by the Department of Justice.10

Data and examples such as this indicate that mergers reducing competitor numbers down to the point of creating four-firm oligopolies have increasingly been permitted. Crucial to proper interpretation of this trend is the question

of whether it has resulted in competitive harm or whether, as some economists argue, it reflects the fact that such mergers are efficiency-enhancing and ultimately beneficial. On this question there is abundant work in economics establishing an empirical relationship between high concentration and harm in the form of above-competitive prices.11

Indeed, this relationship forms the basis of the Horizontal Merger Guidelines that explain FTC and Department of Justice interpretation of concentration and market shares. The guidelines set out criteria for various levels of concern, up to a category of large mergers in highly concentrated industries where a presumption of competitive harm holds. As the guidelines stress, however, the relationship is not mechanical; rather, concentration should be viewed as a reliable, but not infallible, predictor.

Recent research casts some light on the issue of the level of concentration at which anti-competitive outcomes become nearly certain. This research reports that in carefully studied mergers that resulted in six or fewer significant competitors, prices rose in nearly 95 percent of cases. For mergers with a greater number of remaining competitors, the percentage that were anti-competitive fell off steadily. This suggests that a presumption against mergers in the range of six, or certainly five, competitors would make few errors.12

It is notable, therefore, that it is in precisely this range of five to seven significant competitors where enforcement policy has shifted so dramatically in the past 20 years. Whereas actions had been taken in 36 percent of FTC merger investigations with five or more remaining significant competitors, by 2007, this percentage had gone to zero. Yet if competitive harm extends out through six competitors, this would represent the margin on which policy has diverged from the evidence, effectively setting the enforcement line in the wrong place. The consequences of this retreat in enforcement have been rising concentration and harm to competition and consumers.

Evolving and renewing antitrust standards

There are several possible explanations for this rather dramatic shift in merger enforcement policy. As noted, one is agency budgets. Despite broad public and political support for antitrust enforcement, agency resources have not kept up with the number and complexity of recent mergers. In a $20 trillion economy, antitrust budgets of a few hundred million dollars permit only so much oversight and enforcement. Agencies probably have increasingly had to choose which mergers to challenge and which other mergers or possible antitrust violations cannot be fully investigated and perhaps challenged. By themselves, resource constraints could explain the trend toward enforcement actions directed against the largest mergers in the most concentrated markets.

But other forces are at work as well. Among them are the historically important changes in the economic perspective on mergers, in the standards and practices for merger control, and in the judicial emphasis on harms versus benefits that have contributed to this policy shift. Let’s consider each of these in turn.

The economic perspective on mergers and merger policy has undergone major changes over the past 50 years. Three broad phases can be identified. The first, or “structural,” era was characterized by the belief that market structure to a large degree determined performance, so that even modest increases in measured concentration would predictably result in above-competitive prices and profits. This era overlapped with a populist interpretation of the statutes, which held that concentration itself resulted in broad societal harms. These included the adverse effects of corporate power on small business, politics, and communities.

The policy implications of the structural view, which was fairly widely shared at this time, were reflected in the stringent standards of the 1968 Merger Guidelines and in a number of important U.S. Supreme Court findings against mergers of even modest size. Those guidelines, for example, stated that in a “highly concentrated market,” defined as one where the four-firm concentration ratio exceeded 75 percent, a merger between two firms, each with a 4 percent market share, would “ordinarily” be challenged. Consistent with this view of concentration, the Supreme Court in that era upheld blocking a merger of two Los Angeles super-market chains that together would have had about 7 percent of retail grocery sales.13 Absent some extraordinary circumstances, such mergers would not even attract serious antitrust investigation in the modern era.

This period extended up until the 1970s, when the so-called Chicago school upended economic understanding and antitrust policy with respect to mergers (as well as much else). A central contention of the Chicago school of thought was that the relationship between profit and concentration could also be due to the greater efficiencies achieved by large firms. This view held that the tough merger standards of the previous period that were oriented toward maintaining fragmented industries sacrificed cost efficiencies. These views had a transformative effect on policy and in turn led to new Merger Guidelines in 1982 and thereafter.

These new guidelines differed from their predecessors in a number of significant ways. For one, the market structure criteria for what constituted a likely anti-competitive merger were relaxed, thus permitting a considerably wider range of consolidations to be essentially legal. In addition, these structural criteria were no longer determinative but rather represented a rebuttable presumption against certain mergers. Furthermore, two major defenses against the presumption were explicitly endorsed and discussed in ways that encouraged their use. These were that an otherwise problematic merger might be approved if it achieved, and passed on, significant efficiencies or if the market were subject to sufficiently easy entry as to constrain the resulting firm.

The common feature of these changes was the evolving concern that tough merger enforcement standards and practices attacked too many benign or pro-competitive mergers—what were identified above as Type I errors. Despite the lack of systematic evidence for this concern, it nonetheless made significant inroads in the judiciary and in the enforcement process. Perhaps most explicitly, in its Verizon Communications Inc. v. Law Offices of Curtis V. Trinko LLP decision, the Supreme Court stated its preference for minimizing Type I errors. In this case, the defendant Verizon acted in a manner that indisputably excluded a competitor, but the court viewed the effects as possibly efficiency-enhancing and as a result opined:

Against the slight benefits of antitrust intervention here, we must weigh a realistic assessment of its costs. … Mistaken inferences and the resulting false condemnations “are especially costly, because they chill the very conduct the antitrust laws are designed to protect.” … The cost of false positives counsels against an undue expansion of §2 liability.14

While false positives are a legitimate concern for antitrust enforcement, appeal to that concern without evidence is a poor basis for policy. After all, conclusive evidence is often lacking and opinions often differ, but the difficult task of weighing available evidence and making hard decisions is not properly avoided by dismissing one side of the argument. What results is more a statement of faith than fact. This report has already cited evidence demonstrating that the small risk of false positives should not constrain merger enforcement.

Beginning in the 1990s, a third wave of antitrust policy—what is sometimes called the “post-Chicago” view—gained support in economics. The post-Chicago view is not so much a single framework as it is a recognition that much of the classic Chicago view rested on strong assumptions and pure cases rarely if ever found in the real world. By employing economic theory to identify limits to those propositions—and more sophisticated empirical work into the causal connections between market characteristics, strategic behavior, and anti-competitive outcomes—post-Chicago work countered the strict efficiency-based interpretation of mergers and various practices of the Chicago school in a number of areas. Modern scholarship, for example, has demonstrated that the necessary conditions for entry to be a realistic constraint are not so readily met. Just one case in point: Whereas several airline mergers were approved in the 1980s based on the belief in quick and easy entry—the so-called contestable market theory—empirical evidence confirms, and policy now reflects, the obvious fact that entry into airlines is subject to a variety of constraints.15 In addition, economic research now includes new empirical work demonstrating that concentration really does affect prices, even if some older research was subject to significant caveats. The so-called New Empirical Industrial Organization approach has focused on prices in single industries where concentration varies across geographic markets or over time, and it finds support for the effect of higher concentration.16

A particularly important advance has been the theory of unilateral anti-competitive effects from mergers. This theory emphasizes the profit increases that accrue to a single firm from acquiring a competitor to whom business would otherwise be lost by raising prices. This theory is fundamentally different from the traditional view that mergers increased the likelihood of collusion or coordination among fewer firms, and it has represented a powerful new tool with which to analyze possible market power from mergers. For instance, the Department of Justice’s successful opposition to the proposed acquisition of Blucora Inc.’s TaxACT subsidiary by H&R Block Inc. was based on the evidence that as a result of the acquisition, H&R Block could have raised prices knowing that it would no longer lose profits on customers that TaxACT would gain—customers that would now be part of the larger customer base of the merged company.17 Both theories of competitive harm—unilateral effects and the more traditional concern over coordination and collusion from mergers—now appear in the Merger Guidelines.

The latest version of the merger guidelines, published in 2010, embodies this eclectic post-Chicago perspective on mergers. It acknowledges the importance of efficiencies and entry conditions but also emphasizes the diverse mechanisms and the multiplicity of relevant factors in evaluating the likelihood of possible harms from a merger. Yet these guidelines further relax the numerical thresholds for the level and change in concentration at which a merger might be presumed to raise competitive concern.18 to create or enhance market power, rather than that they are simply presumed to do so—diminishes the force of the sup-posed presumption. ] In addition, with pressure from the courts, the guidelines effectively offer to provide insight into the specific mechanism by which challenged mergers would likely result in competitive harm—often a difficult task.19 Despite these obstacles, they have nonetheless formed the basis for recent successful efforts by the Federal Trade Commission and the Department of Justice to prevent mergers of insurance companies (Anthem Inc. and Cigna Corp., Aetna Inc. and Humana Inc.), drug store chains (Rite-Aid Corp. and Walgreens Boots Alliance Inc.), and several others.

The most recent guidelines and related policy documents from the agencies can be said to reflect the current state of economic analysis of mergers, but in practice, these often seem to reflect an undue degree of caution—an excessive concern with Type I errors, a weakening of the presumption against mergers in very concentrated industries, and a narrowing of the focus of merger challenges.

These policy shifts have arguably contributed to the documented excessive tolerance toward mergers at the enforcement margin and, in turn, to the troubling rise in industry concentration that this report initially documented.

Conclusion

Antitrust policy toward mergers has undergone major changes over time. It would be tempting to view this as part of a longer progression toward sounder and more effective enforcement, but that notion is subject to doubt. After all, there have been three quite distinct phases of antitrust policy, which have taken merger enforcement from stringent to lax to more moderate, and there is no assurance that more change might not be forthcoming. Indeed, even within this last post-Chicago period, there has been a substantial shift of policy away from merger enforcement actions in all but the most concentrated markets.

In addition, progress in analytical techniques for merger evaluation has been uneven, and some issues and areas have been underutilized in the enforcement process. These various imbalances have contributed to this narrowing of merger enforcement actions and the increase in concentration in numerous major markets. Policy can be strengthened by revisiting some of these issues, by invest-ing in further analytical and empirical work in support of them, by expanding agency budgets, and by vigorous pursuit of merger cases that raise these issues most directly. In this manner, antitrust can better serve its purposes of protecting competition and consumers.

About the author

John E. Kwoka is the Neal F. Finnegan distinguished professor of economics at Northeastern University. He is the author or editor of three books and more than 75 articles in the areas of industrial economics, antitrust, and regulation. His co-edited book of antitrust cases, The Antitrust Revolution, is going into its seventh edition, and his book titled Mergers, Merger Control, and Remedies: A Retrospective Analysis of U.S. Policy, was published by MIT Press in December 2015.

Kwoka is presently a research fellow of the American Antitrust Institute and is on the boards of the Industrial Organization Society and the Review of Industrial Organization. He previously served as president of the Industrial Organization Society, vice president of the Southern Economic Association, and editor of the Review of Industrial Organization, as well as an ENCORE fellow at the University of Amsterdam and a member of the Advisory Council to the Competition Commission of Mauritius.

Kwoka has taught at the University of North Carolina at Chapel Hill and George Washington University and held visiting positions at Northwestern University and Harvard University. He has also served at the Federal Trade Commission, the Antitrust Division of the Department of Justice, and the Federal Communications Commission.

End Notes

1. Obama White House Office of the Press Secretary, “Executive Order—Steps to Increase Competition and Better Inform Consumers and Workers to Support Continued Growth of the American Economy,” Press release, April 15, 2016, available at https://obamawhitehouse.archives.gov/the-press-office/2016/04/15/executive-order-steps-increase-competition-and-better-inform-consumers.

2. Council of Economic Advisers, Benefits of Competition and Indicators of Market Power (Executive Office of the President, 2016), available at https://obamawhitehouse.archives.gov/sites/default/files/page/files/20160414_cea_competition_issue_brief.pdf.

3. Clayton Antitrust Act of 1914, as amended by the Celler-Kefauver Act of 1950.

4. The Economist, “Too Much of a Good Thing,” March 26, 2016, available at https://www.economist.com/news/briefing/21695385-profits-are-too-high-america-needs-giant-dose-competition-too-much-good-thing.

5. David Autor and others, “Concentrating on the Fall of the Labor Share,” American Economic Review: Papers & Proceedings 107 (5) (2017): 180–185, available at http://ddorn.net/papers/ADKPV-LaborShare.pdf.

6. The Herfindahl-Hirschman Index is a more sophisticated measure of overall industry concentration, calculated as the sum of squared market shares of all firms.

7. Gustavo Grullon, Yelena Larkin, and Roni Michaely, “Are US Industries Becoming More Concentrated?” (April 2017). Available at SSRNL https://ssrn.com/abstract=2612047.

8. Of about 1,500 mergers reported to the Federal Trade Commission and the Department of Justice each year, 50 or so are subject to second requests and full investigation. These data cover those that are analyzed by the FTC only. No comparable data are available from the Department of Justice. Mergers over certain size thresholds must be reported to both agencies.

9. Federal Trade Commission, “Horizontal Merger Investigations Data, Fiscal Years 1996-2011” (2013), available at https://www.ftc.gov/sites/default/files/documents/reports/horizontal-merger-investigation-data-fiscal-years-1996-2011/130104horizontalmergerreport.pdf.

10. Two of these were subject to some minor remedies. Underscoring the significance of this count of remaining competitors was the Department of Justice’s opposition to the proposed merger of AT&T Inc. and Deutsche Telekom AG’s T-Mobile US Inc. subsidiary, which would have reduced the number of national wireless carriers from four to three.

11. A review of this evidence can be found in John E. Kwoka, Mergers, Merger Control, and Remedies (Cambridge, MA: MIT Press, 2015).

12. John E. Kwoka Jr., “The Structural Presumption and the Safe Harbor in Merger Review: False Positives, or Unwarranted Concerns?” (May 19, 2016), available at https://ssrn.com/abstract=2782152.

13. United States v. Von’s Grocery Co. 384 U.S. 270 (1966).

14. Verizon Communications Inc. v. Law Offices of Curtis V. Trinko LLP, 540 U.S. 398, 414 (2004), available at https://www.law.cornell.edu/supct/html/02-682.ZO.html. While this was a nonmerger case, this guidance is reflected in other areas of antitrust.

15. See, for example, Federico Ciliberto and Jonathan W. Williams, “Limited Access to Airport Facilities and Market Power in the Airline Industry,” The Journal of Law and Economics 53 (3) (2010): 467–495.

16. For a summary of some of this literature, see Jeffrey Church and Roger Ware, Industrial Organization: A Strategic Approach (New York: McGraw-Hill Publishing Co., 2000).

17. For discussion, see, for example, Scott Sher and Andrea Murino, “Unilateral Effects in Technology Markets: Oracle, H&R Block, and What It All Means,” Antitrust 26 (3) (2012): 46–52, available at https://www.wsgr.com/publications/PDFSearch/sher-summer-12.pdf.

18. The actual language—that such mergers are “presumed to be likely” [emphasis added

19. U.S. Department of Justice and Federal Trade Commission, Horizontal Merger Guidelines (2010), p. 25.