Introduction

Most economists agree that contemporary levels of economic inequality in the United States are at near-record highs. And most economists also concur that innovation is a critical engine driving economic growth. In this report, I develop a framework connecting the two—rising inequality on one hand and declining levels of innovation and economic dynamism on the other. The result is a set of research questions designed to stimulate a conversation about how the innovation channel may be a key mechanism through which rising levels of inequality are affecting the overall health of the U.S. economy.

Download FileTrends in economic inequality and innovation and entrepreneurship report

The impact of economic inequality on innovation may work differently across the income distribution, and the framework presented in the pages to follow accordingly examines how inequality may be impeding innovation through its implications for the bottom, middle, and top echelons of U.S. society. When viewed this way, the potential mechanisms through which inequality may be affecting economic growth come into clearer focus, as do a set of policy implications worthy of consideration.

Briefly, this paper finds that economic growth and inequality, innovation, and entrepreneurship are inexorably linked, but in very different ways when examined across the wealth and income spectrum rather than through the usual lens of overall small business creation and direct investments in technology and innovation. From this perspective, perhaps the most telling indicators are the decline in the number of new startups in the U.S. economy and the declining amount of public and private investments in innovation and entrepreneurial human capital—all of which bode ill for future U.S. economic competitiveness and productivity.

The consequences of rising economic inequality at the top and the bottom of the ladder on innovation and entrepreneurship in the United States is most evident in the intergenerational accumulation of patents—a key measure of innovation and entrepreneurship—among those at the top compared to the shriveling number of patents among those at the bottom. Also troubling is the decline in risk-taking among middle-class Americans—a trend linked to increasing economic insecurity due to a range of factors. And at the top of the ladder, the steady “financialization” of the U.S. economy incentivizes short-term corporate investment decisions at the expense of a longer-term vision on markets and human capital.

Possible public policy solutions to declining innovation and entrepreneurship in the United States due to rising economic inequality await more detailed research on many of the factors examined in this report. This paper is meant to be more provocative and less prescriptive. Still, the available evidence suggests that policymakers focus on steps that can improve human capital and education, buttress social insurance programs, confront rising wealth and income inequality via the tax code and corporate governance reforms, and improve the family economic security of all citizens.

Rising economic inequality, declining innovative dynamism

The rise in economic inequality over the past quarter-century is well documented. University of California, Berkeley economist Emmanuel Saez finds that the share of pre-tax income going to the top 1 percent of U.S. taxpayers stood at 20 percent in 2012—the last year for which complete data are available—up from only 9 percent in 1970.1 The nonpartisan Congressional Budget Office finds that the share of income accruing to the top 1 percent of households, after accounting for taxes paid and for transfer income (Social Security payments, refundable tax credits, safety-net payments), grew by 275 percent between 1979 and 2007. In contrast, this post-tax-and-transfer income grew by less than 30 percent for those middle-class households in the middle three quintiles of the income distribution.2

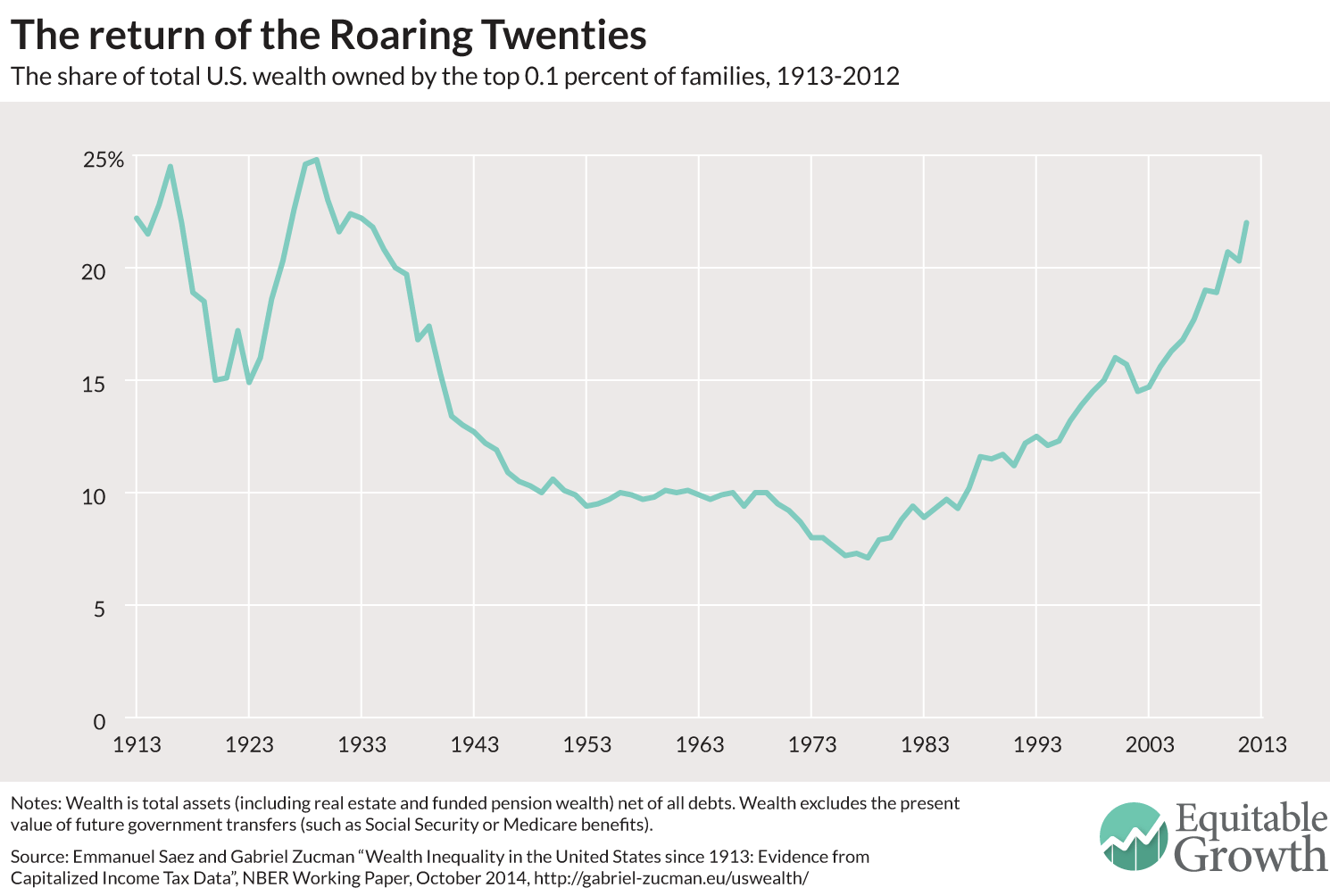

The growing concentration of wealth (as opposed to income) is even more dramatic. Gabriel Zucman at the London School of Economics finds that assets are highly concentrated at the pinnacle of the wealth distribution, with the richest 0.1 percent of taxpayers holding 22 percent of the nation’s capital in 2012, up from 7 percent in 1979.3 In short, no matter how you slice the economic pie, a larger and larger piece has gone to those at the tippity-top. (See Figure 1.)

Figure 1

The contemporary distribution of U.S. economic resources is the most unequal since the Roaring Twenties, by most measures, and this inequality is reflected in the unequal growth in family incomes up and down the economic ladder. Between 1947 and 1979, across the income spectrum, average family incomes grew at a pace of just over 2 percent a year. In the period from 1979 to 2007, families on the bottom fifth of the income ladder experienced virtually no growth while families on higher rungs saw increasingly greater annual income growth the higher the rung they occupied. Moreover, income growth for all but the very wealthiest in our society has sputtered over the past quarter-century, with average growth rates well below the 2 percent of the post-World War II period.4 The economic lives of those in the middle and bottom of the income distribution have shifted in fundamental ways as more of the returns to growth have flowed to the very top.

An emerging body of research is beginning to reinvestigate what trends in inequality mean for the dynamism of the economy as a whole. For more than half a century, Simon Kuznets’s Nobel Prize-winning observation that inequality was a transitional phase that would reverse itself once poor countries evolved into developed nations dominated conventional wisdom.5 Six decades later, and armed with far more sophisticated data and computational power than what Kuznets had available at Harvard University in the 1950s, today’s researchers offer serious challenges to the U-shaped Kuznets curve.

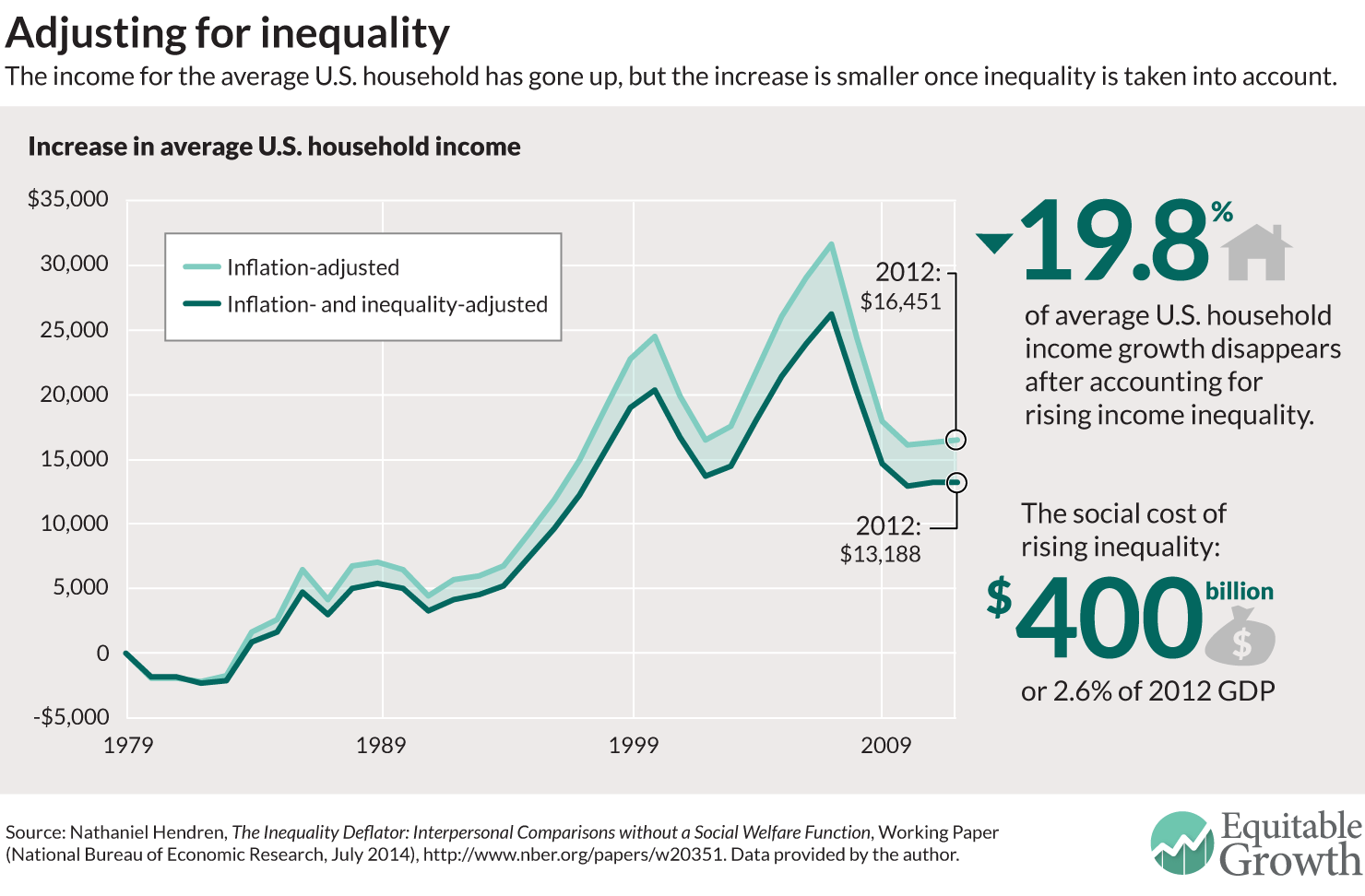

Economists Andrew Berg and Jonathan Ostry at the International Monetary Fund made waves with their 2011 study demonstrating the negative relationship between sustained economic growth spells and high levels of income inequality.6 World Bank economist Roy van der Weide and City University of New York Graduate Center economist Branko Milanovic use state-level data for the United States to find that high levels of income inequality decrease income growth for those at the bottom of the earnings distribution while simultaneously increasing income growth for those at the top.7 And Harvard economist Nathaniel Hendren calculates that income inequality reduced U.S. economic growth by 20 percent over the past four decades, adding up to a “social cost” of roughly $400 billion.8 (See Figure 2.)

Figure 2

While the empirical literature on the macroeconomic relationship between inequality and growth continues to evolve, a key set of questions urgently await answers. Even if macroeconomists were to come to a universal consensus tomorrow that inequality was negatively correlated with economic growth—the higher the inequality, the lower the growth—policymakers would still need evidence-backed guidance directing them to the appropriate levers for mitigating the problem of inequality and in turn jumpstarting more equitable growth. In order to gain traction—to make an abstract conceptual problem concrete and to give policymakers specific places to look for solutions—researchers need to shift the focus to include mechanisms that explain how widening inequality might affect economic growth and stability. Through what channels might the impact of inequality affect the broader economy? When we turn the research lens in this direction, the importance of innovation and economic dynamism begin to come into focus.

Innovation, dynamism, and economic growth

Innovation is a critical engine driving economic growth. As Council of Economic Advisers Chairman Jason Furman recently remarked, for an advanced economy such as the United States, “catching up to the productivity frontier is not possible when you are already there.”9 Borrowing from Simon Kuznets (via fellow Nobel Laureate Kenneth Arrow), the concept of innovation is best understood broadly, as “a new combination of existing knowledge to create something useful (in some sense).”10 A long history of economics research puts innovation at the center of most growth models, with more recent work focusing on small, young firms—startups—as the locus of a disproportionately large share of innovation.11

Startups’ unique role in fostering innovation stems from their ability to generate market turbulence, competition, and industry renewal. Indeed, they serve as particularly effective competitors in arenas that require flexibility and the ability to efficiently respond to niche markets.12 And startups generally require an individual actor, the business founder/owner—in other words, the entrepreneur.

Why are startups and their entrepreneurial founders so important for generating innovation, and in turn economic growth? The research points to two main channels: job creation and productivity. The contemporary evidence is less clear on productivity (more on that in a moment) but is more persuasive on job creation.13 Startups account for 20 percent of gross job creation in the United States, but high-growth firms (which are disproportionately successful startups) account for almost 50 percent of gross job creation. Taken together, new businesses and high-growth firms account for a whopping 70 percent of gross firm-level job creation annually.

The high-tech sector plays a particularly important role in job creation. High-tech firms, defined as the group of industries with disproportionately high shares of employees in the STEM fields of science, technology, engineering, and math, were 23 percent more likely than the private sector as a whole to witness a new business formation over the past three decades. While high-tech business formation was once consolidated to the Route 128 corridor and Silicon Valley, these startups are increasingly geographically dispersed.14

As Federal Reserve Board economist Ryan Decker and his colleagues summarize, “startups and young businesses are small, the underlying reason why many commenters describe small businesses as the engine of job growth.”15 It is worth noting that firm age is more important than firm size because once researchers control for firm age, a business’s size has no relationship to its growth trajectory.16 Also worth noting is this: Most startups fail, and the majority that last create only a handful of jobs. Massachusetts Institute of Technology economist Antoinette Schoar calls young businesses with low rates of job creation “subsistence” entrepreneurship, which she contrasts with “transformational” entrepreneurship that creates jobs at a rapid pace.17 These “transformational” startups are the engine of American job growth.

Entrepreneurship, then, is a high-risk, high-reward enterprise on multiple levels. On a micro level, the prospect of business failure for a given individual entrepreneur is high, and comes with substantial costs. On a macro level, an economy based on the dynamism inherent in the creation of new businesses in general and in high-tech startups in particular requires substantial tolerance for failure and volatility.

The second key role for startups in generating economic growth is their role in boosting productivity. While startups’ disproportionate role in job creation is well documented, their contribution to overall productivity is less clear. Productivity is central to any growth model—it’s a key source of long-run economic growth and gains for workers. Total factor productivity (sometimes called the Solow residual—after Nobel Laureate Robert Solow—or simply “technology”) captures how well a given economic unit combines capital and labor to produce output. A sizable body of research posits that startup firms are an important source of productivity growth, because of their unique ability to successfully combine capital and labor to produce high levels of innovative output.

For instance, New York University economist William Baumol posits a “David and Goliath” partnership between small startup businesses and large corporations, whereby the small startups excel at generating radical innovations and the larger established corporations then improve upon them by adding capacity, usability, and marketability.18 The symbiotic relationship between the two types of firms in turn generates the products that have revolutionized our lives and grown the economy over time. From a theoretical perspective, this is why startups may play a key role in the productivity growth rate.

Figure 3

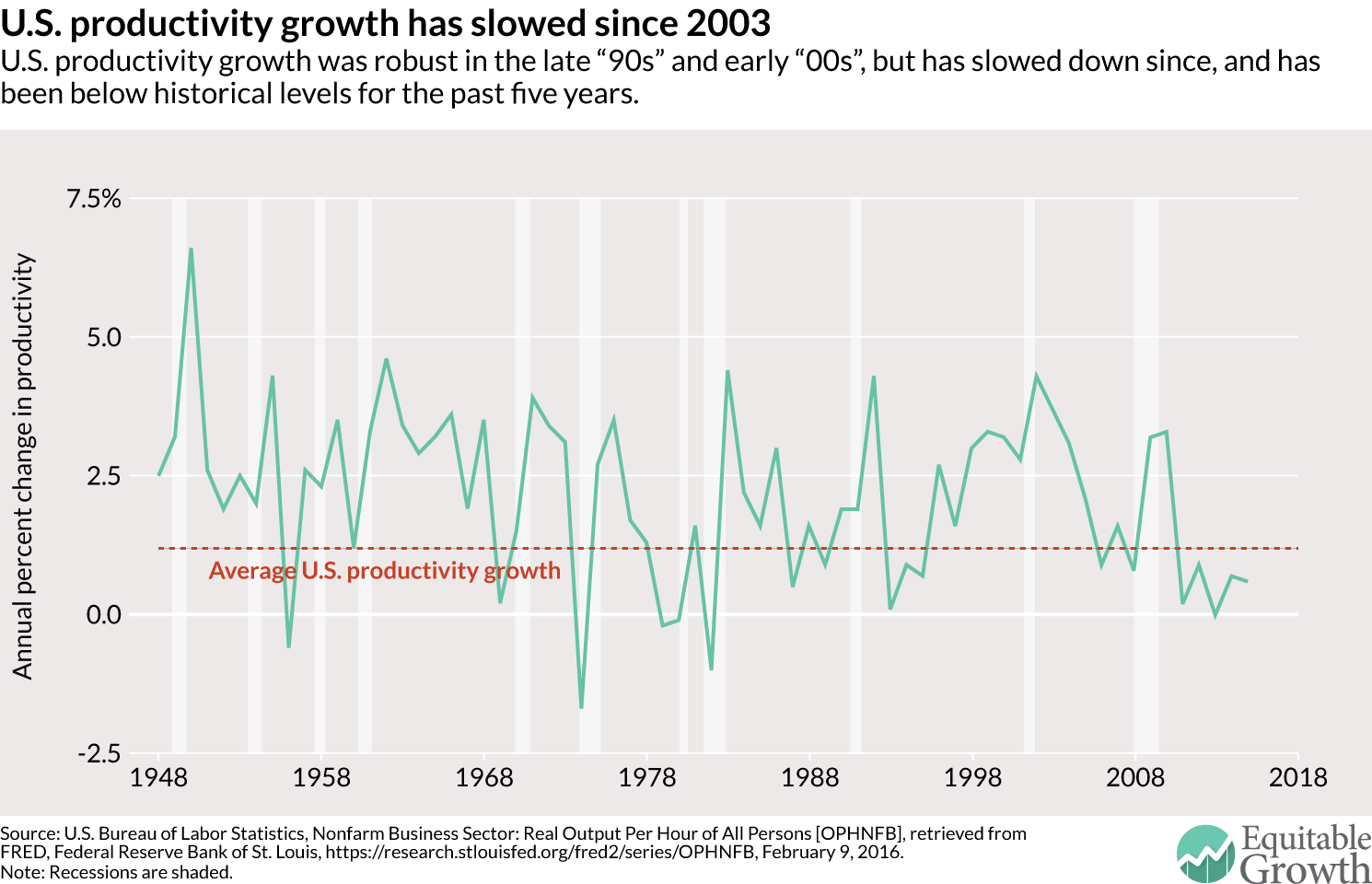

Research from the Organisation for Economic Co-operation and Development shows that firms across its 34 member nations exhibit high levels of total factor productivity. Yet productivity growth since 2003 has slowed considerably from its pace in the late 1990s and early 2000s, and remains well below the rate of growth seen in earlier post-World War II periods.19 (See Figure 3.) The “diffusion mechanism” that translates productivity growth in vanguard firms to productivity growth on behalf of the macro economy as a whole appears to be broken, or at least not functioning as it once did.

As a result, the role of startup businesses in spurring economic growth is less clear than it once was. A recent paper from Federal Reserve Board economist Ryan Decker and colleagues suggests that the declining rate of business dynamism may be explained by a decreased response to productivity shocks.20 In other words, when a firm experiences an innovation that makes workers more productive, they are less responsive to those shocks today than they were before 2000. As a result, the relationship between innovation, productivity, and job creation looks weaker now than previously. Decker and his colleagues restrict their study to firms in the high-tech manufacturing space, but it provides clues as to what might be driving forces in other industries as well.

Innovation, entrepreneurship, and economic growth across the U.S. wealth and income spectrum

Given the importance of young firms for innovation, it is worth pausing here to review the contemporary empirical state of affairs for these firms in the United States. Recent evidence suggests that many U.S. entrepreneurs do not have aspirations to create high-growth or innovative firms but rather started their businesses for non-pecuniary reasons such as flexibility in work hours.21 These less-than-multimillionaire aspirations are consistent with the industry characteristics of most small businesses, which are concentrated among skilled craftsmen, lawyers, real estate agents, doctors, small shopkeepers, and restaurateurs.22 So it is perhaps unsurprising that the majority of startups exhibit low net rates of job creation.

Multiple studies note a marked decline in the rate of new business creation over the past four decades, from 12 percent in the 1980s to an average of 10.6 percent just before the Great Recession of 2007-2009, during which it plunged to less than 8 percent. The rate of this decline has varied across business sectors, but applies broadly across the economy.23

The slowing average rate of new business creation has not been counterbalanced by an increase in the size of the average new business. Depending on the data used, the average size of these new firms has either decreased or remained stable since the 1980s.24 The combined result of these two trends is that newly created businesses play a smaller role in the U.S. economy today than they did in the past. Firms five years old or younger comprised 47 percent of all firms in the late 1980s, but declined to 39 percent prior to the Great Recession.25

Concurrently, recent empirical work shows that the slowdown in new business formation accounts for 32 percent of the observed decline in net job creation since the 1980s. Similarly, this slowdown contributed to a 20 percent decline in job destruction over the same period.26 And finally, the falling rate of new business formation also led to a 26 percent decline in job reallocations between the 1980s and 2000s, meaning that fewer workers switched jobs over this period.27 Lower rates of job switching may have contributed to stagnant wages for workers, as a substantial body of research suggests that job-to-job mobility is key for boosting a worker’s paycheck over time.28

Given their role in fostering innovation and driving job creation, the startup slowdown has obvious implications for economic dynamism and growth. An open question, and the focus of the remainder of this report, is how economic inequality might be playing a role in the startup slowdown as well as on other indicators of economic dynamism, especially innovation and entrepreneurialism in general. For the sake of introducing some analytic clarity, I approach inequality slice by slice, suggesting ways that inequality’s impacts may flow through the economic realities for the bottom, middle, and top of the income distribution. Doing so necessarily requires a focus not just on firms but also on individuals—a departure from much of the research on growth, dynamism, and entrepreneurship, but a critical one. The bottom-middle-top framework below provides an analytic lens for structuring a research agenda with many critical yet unanswered questions.

Inequality and innovation at the bottom: Wasted potential?

Entrepreneurship is at the heart of the rags-to-riches mythology, the lifeblood of the American Dream. The idea that poor kids with gumption and a great idea can rise out of poverty and lift themselves and their families into the vaunted top echelons of society has been echoed time and time again, from literary figures such as Horatio Alger to Jay Gatsby to scrappy business go-getters from Andrew Carnegie to Mark Cuban.

A wealth of new empirical work, however, suggests that the intergenerational mobility embodied by the American Dream has been largely overstated.29 What remains an open question is whether the broken promise of the American Dream is linked to trends in entrepreneurship and innovation. Are low-income individuals more or less likely to succeed in entrepreneurship compared to their wealthier counterparts, all things being equal? How has increasing economic inequality in recent decades affected the likelihood of entrepreneurial success among the poor?

New research from a team of economists from Harvard University, the U.S. Treasury Department, and the London School of Economics quantifies just how far out of reach entrepreneurial success is for the vast majority of children born into low-income families in the United States.30 The team matches up data on patents in the United States with tax returns of the people receiving the patents, and the tax returns of those patent recipients’ parents. This multigenerational match allows them to see not only how much these inventors earn as adults, but also their families’ economic resources during the inventor’s childhood.31 As a result, for the first time ever, we have the beginnings of a picture of the lifecycle of an inventor.

Unsurprisingly, children born to wealthy parents are far more likely than poor children to obtain a patent later in life. More surprising is the sheer magnitude of that patent gap. Early research findings suggest that for every 10,000 children born to families in the top 1 percent, 22.5 will receive a patent in adulthood. In contrast, just 2.2 of every 10,000 children born to families with incomes below the U.S. median income will receive a patent in adulthood. Worth noting: Just as income inequality is characterized by runaway rates at the very top of the income distribution, so too are patent rates. Children born into families in the top 1 percent are twice as likely to obtain a patent in adulthood compared to children born into the top 10 percent.32

Importantly, the data indicate that the vast majority of the patent gap is not explained by inherent skills differences between low- and high-income children. The researchers merge test score data for third-graders in their study and find that patent rates in adulthood are roughly equal for low- and high-income kids with similar test scores—except for the high performers. Among high-performing children, those born into high-income families are about four times as likely to obtain patents than their peers born into low-income families.

What explains the patent gap, then? The lion’s share of the gap is explained by the cumulative consequences of educational disadvantage. The share of the patent gap explained by test scores grows by nearly 5 percent per grade from the third-grade baseline through eighth grade, the last year for which the researchers have testing data available. And when the researchers look at the role of college quality in determining who files successfully for a patent, the importance of this human capital channel of education grows even starker: 90 percent of the income-innovation relationship is explained by whether or not an individual attended a high-quality college.33

In sum, the empirical evidence suggests that low-income children face major barriers to successful entrepreneurship, even when they show significant promise. Despite early measured ability, poor children are significantly less likely to file successfully for a patent than their wealthy peers. Subsequent schooling essentially accounts for this difference, which suggests that human capital policy is hugely important for fostering innovation across the income spectrum. Research from Stanford University economist Caroline Hoxby and Harvard University economist Chris Avery tells us that even the highest-achieving low-income students are not attending the most selective colleges.34 In general, we need far more research quantifying the lifecycle of inventors, and entrepreneurs more generally.

The Harvard team’s cutting-edge creation of a dataset with multigenerational layers of administrative data represents the frontier for research that will allow us to better understand the implications of inequality for entrepreneurship at the bottom of the income ladder. Better understanding macro-level phenomena requires the application of novel, large-scale micro-level data to answer key questions—an exciting, promising endeavor that remains in its early days.

Inequality and innovation in the middle: Risk aversion?

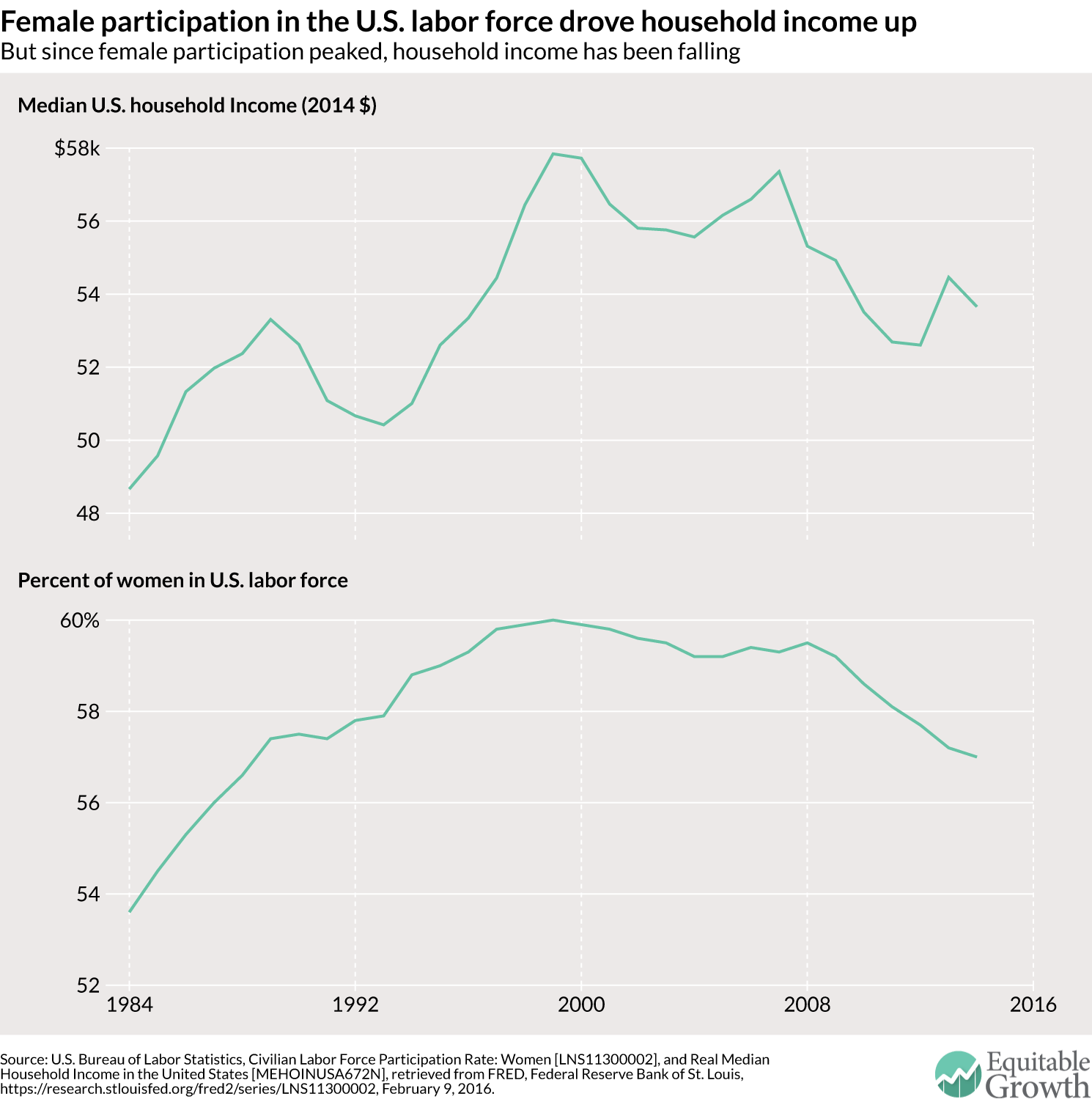

For millions of middle-class Americans, the idea of “striking it rich” these days is sadly far from their imaginations. Middle-class incomes have stagnated, with only the rise of women in the labor force keeping the vast majority of middle-class families afloat over the past half-century.35 (See Figure 4.) This wage-constrained, dual-income working experience of the typical American family may well blunt entrepreneurship for multiple reasons.

First, the time crunch faced by millions of American families may crowd out the potential for the development of successful business plans. Second, the increase in both perceived and real economic insecurity may mean the middle class is substantially more risk averse than in the past. Third, the middle class may face serious capital constraints in the face of low and eroding wealth, with implications for the rate of new business formation and especially the time and thinking and money needed to launch a high-tech startup.

Figure 4

Working middle-class families face a serious time crunch. Delayed marriage and child-bearing, more births outside of marriage, the increase in women’s labor force participation, and the aging of the U.S. population have altered family life and created new challenges for those with caregiving demands.36 Mothers in the United States have decreased the time they spend on housework as their time in the labor market has gone up, but they also have increased the time spent on child care. Fathers have increased the time spent on child care as well. Intensive child-rearing practices are more common, perhaps in response to the rat race that comes along with rising inequality and higher perceived costs of failure.37 Workers increasingly must contend with non-standard work schedules, with the resulting high levels of unpredictability adding additional stress for families balancing care responsibilities.38

Whether dual-earner families or single parents, these factors all translate into unprecedented levels of time pressure for many working American families. How is this multilayered time crunch affecting the entrepreneurial success rate of the American middle class? If potential entrepreneurs are collapsing at the end of a busy day, exhausted after a long day of work and “second-shift” responsibilities caring for children (and, increasingly, aging parents), what’s the likelihood that they have the energy to push their nascent big idea—be it a new restaurant or the latest idea for a new app for a mobile phone—into a transformational new venture?

As noted earlier, entrepreneurship inherently involves risk. The vast majority of new businesses fail. Recent empirical work raises serious questions about whether the middle class may have grown more risk averse, even among those whose lives are currently financially stable enough to serve as fertile ground for potential entrepreneurship.

Even prior to the Great Recession, public opinion polls suggested high levels of economic anxiety among Americans. A 2007 poll revealed that more than half of all Americans felt they had not moved forward, while nearly a third said they had fallen back.39 Only 41 percent said they were better off than they were five years ago, the lowest level in nearly 50 years. Meanwhile, the share saying they were worse off than they were five years ago rose to 31 percent, the highest level in almost half a century.

These perceptions picked up by pollsters match the reality of the American experience fairly closely. Income growth among lower- and middle-income families has been very slow over recent decades, and has declined somewhat over recent years. In contrast, among higher-income households, income growth has been strong—much stronger than growth for everyone else over the past four decades. So it is easy to see why many middle-class Americans feel they are falling further and further behind.

Survey data provide ample evidence of the precarious economic experiences of most Americans. For instance, the 2009 TNS Economic Crisis survey asked households about their capacity to come up with $2,000 in 30 days. About one-quarter of Americans reported that they would certainly not be able to come up with such funds, and an additional 19 percent reported they would do so by pawning or selling possessions, or taking payday loans. Based on this finding, Dartmouth University economist Annamaria Lusardi and her colleagues determined that nearly half of Americans are financially fragile, including a sizable fraction of seemingly “middle-class” Americans.40

Families simply don’t cope with risk using “precautionary savings,” either. While savings come first in the “pecking order” of coping methods, the typical household relies heavily on family and friends, formal and alternative credit, increased work hours, and selling items. Empirical studies of short-term income volatility—for instance, the likelihood of experiencing a large monthly or annual drop in income—suggest a rising risk of economic insecurity. More than one in seven families experienced a drop of income of at least 50 percent in a given four-month period, on average between 1996 and 2004. The probability of not fully recovering from a substantial drop in income within a year rose sharply between 1996 and 2004, with 81.9 percent failing to recover in 1996 versus 92.4 percent in 2004.41

Stagnant incomes, financial fragility, and a relatively high probability of experiencing a substantial and irredeemable drop in income in the short term all combine to provide good reason to wonder whether risk tolerance among America’s middle class has indeed shifted. In the face of such economic insecurity, what happens to the probability of entrepreneurial success? How, if at all, does the half-century-long shift toward higher individual and family economic risk impact the entrepreneurial spirit?42

Finally, consider the effects of the erosion of middle-class wealth on the probability of entrepreneurial success. There are plenty of good reasons to imagine that liquidity constraints impact an individual’s likelihood of starting a business. Simply put, starting a business costs money. Personal wealth can be seed capital or loan collateral. One way of quantifying liquidity constraints is through individual or household wealth. Early seminal work from Global Economics Group economist David Evans and his colleagues established a positive relationship between wealth and the probability of becoming an entrepreneur.43 More recent work from World Bank economist Camilo Mondragón-Vélez expands on this analysis to show that most potential entrepreneurs in the economy—especially those below the top of the wealth distribution—face capital constraints when making the decision to start a business.44 Moreover, given the role of liquidity constraints, differential access to financial markets can help determine who becomes a successful entrepreneur. Increased financing costs and limited access to borrowing for low- and middle-income individuals can hamper entrepreneurship.

The empirical trends in middle-class families’ asset portfolios provide reason to ask whether liquidity constraints are hampering successful entrepreneurship. Median wealth in America in 2013 was at its lowest rate since the early 1980s.45 The average family’s net worth plummeted between 2007 and 2010, mainly due to the high debt leverage of the average U.S. household prior to the recession, and the prominence of housing in the average asset portfolio of most middle-class families.46 What’s more, the racial and ethnic wealth gap, largely stable from 1983 to 2007, widened dramatically over the course of the Great Recession. And the wealth of households under the age of 45 has taken an especially hard hit in recent years.47

Taken together, these three basic sets of trends have potentially important implications for successful entrepreneurship. Middle-class families face serious time pressures, which may be constraining their ability to do the work necessary to move from the daydreaming stage to the reality of starting their own business. Economic precariousness may be holding back potentially transformative ideas from taking flight as Americans become more risk averse in the face of rising downside risk. And liquidity constraints stemming from eroding wealth and limited access to borrowing for credit-constrained individuals may be an additional roadblock. All three of these pathways are key channels through which the effects of inequality on the middle class may be holding back innovation, and in term hampering broader economic growth and dynamism.

Inequality and innovation at the top: Perverse incentives?

Top-end income and wealth have skyrocketed over the past half-century. Twenty percent of pre-tax income in the United States now goes to the top 1 percent of U.S. taxpayers.48 The wealthiest 0.1 percent of taxpayers held 22 percent of the nation’s assets in 2012.49 How does the pulling away of those individuals and families at the top of the economic ladder affect trends in innovation and entrepreneurship? Below, I work through two potential mechanisms worthy of further exploration.

First, an increasing fraction of top-end income earners in the United States are employed in the financial sector. Think investment bankers and highly paid money managers, and private equity and hedge fund investors.50 How has financialization possibly harmed innovation and entrepreneurship? The transition of the U.S. economy over the past three decades from manufacturing-dominated to finance-driven is well established.51 Corporate governance is increasingly more responsive to financial markets than to product markets.52

Financialization has reshaped managerial priorities away from battling for ever-growing market share and toward short-term profits, which has implications for investments in research and development. This dynamic, in turn, has potential consequences for innovation as firms are more inclined to take a short-term approach to business rather than a long-term approach.53 The research and development funding necessary for breakthrough innovations, for example, may have long-term payoffs but yields limited short-term results, and thus takes a backseat in an economy characterized by high levels of financialization.

Relatedly, investing in workers’ skills and talents may also be disincentivized in a world where short-term shareholder value trumps a longer-term vision. Underinvesting in workers may have hidden negative spillover effects for innovation and entrepreneurship. Today’s large firms are the incubators of tomorrow’s high-growth startups, places where employees see market opportunities that their employers are either uninterested in or too big to care about.54 If financialization means a shift in focus from long-term goals to short-term goals, the role of the firm as a locus for human capital development may have shifted in fundamental ways. And, for reasons noted below, the public sector has not accordingly responded to the erosion of a key private-sector capacity.

Second, consider the potential political dynamics at play. The outsized influence of money in the political process means that a well-organized conservative movement deeply committed to reducing the size and scope of government plays a powerful role in shaping political debates and outcomes.55 Continued cuts in public investment in research and development, including cuts to the National Institutes of Health, the National Science Foundation, and elsewhere, are arguably a consequence of organized economic elites determined to rein in the role of government. Starving the country of investments in critical research and development that could spur important innovations is potentially a serious consequence of rising economic inequality.

Likewise, the anemia of the social insurance system that protects against some of the risks faced by middle- and lower-class households can also plausibly be traced down the same path. Consider the organized fight against the Affordable Care Act. A growing body of empirical work shows that access to affordable, universal health insurance can play a critical role in stimulating entrepreneurship, by untethering workers’ health care needs from an employer.56 Yet the push by a small but highly organized, well-resourced economic elite jeopardizes a key element of social insurance policy with the potential to jumpstart entrepreneurial activity.

From research frameworks to policy implications

On both a micro and macro level, the risk inherent in an entrepreneur-driven economy such as the United States requires a set of public policy solutions designed to incentivize “smart” risk-taking and to protect against the major downsides of that risk. But it remains an open question whether and how policy shifts could incentivize more “subsistence entrepreneurs,” whose self-employment plays a key role for the individual and their family but with only a small role in overall job creation to make the leap into “transformational entrepreneurs” who play a key role in both innovation and job creation.57

These are not easy policy questions to answer. The analysis in this paper is meant to be more provocative and less prescriptive. More research is needed if we are to fully understand whether and how inequality affects economic growth via innovation and entrepreneurship. But the analytic framework presented in this paper implies that there is a constellation of policy areas worthy of consideration by those looking to rejuvenate a dynamic, growing economy overall.

First, human capital policies are critical. The research on the relationship between childhood economic status and adult patent receipt suggests that the U.S. educational system is fundamentally failing students born into low-income families, especially those who show academic/intellectual promise in their early years. Gifted and talented programs for promising low-income youth, mentorship programs, rigorous college (and other postsecondary degree) counseling services, and other creative investments in public schools are all worth putting on the table.

Second, the evidence suggests that success in filing for a patent may be just as much about who an individual knows as it is about what that person knows. As a result, policies that more effectively connect talented low-income young adults with mentorship opportunities and connections to investors are worth considering. And given the early age at which these education gaps open up, universal pre-kindergarten programs belong in the discussion—especially because of the important role these classes can play for families across the income distribution. Pre-kindergarten is an investment in children, but it is also an investment in parents, including middle-class families facing a major time crunch that may be affecting their ability to act on their entrepreneurial instincts.

Third, social insurance policies are a key element of a new entrepreneurial policy framework. Recent empirical work on the role of social insurance suggests the key role it plays in fostering entrepreneurship, especially for those in the lower and middle tiers of the income distribution. For instance, HEC Paris economist Johan Hombert and his colleagues find that extending unemployment benefits to individuals who start their own companies (and further extending those benefits if the new company fails) increased the rate of new business creation by 10 percent across all industries.58 These new businesses facilitated by the extension of unemployment benefits were just as high quality as their counterparts founded by better-funded entrepreneurs, as measured by job creation, growth, and survival rates. And entrepreneurs who used unemployment benefits to finance their new businesses reported higher levels of ambition than other entrepreneurs.

While Hombert’s study used French data, two recent studies from Harvard Business School economist Gareth Olds find similarly positive impacts of access to social safety-net programs in the United States, including the State Children’s Health Insurance Program and Supplemental Nutrition Assistance Program, commonly known as food stamps.59 In short, reducing downside risks through robust social insurance programs can incentivize entrepreneurial entry and promote entrepreneurial success.

Fourth, policies designed to lessen the impact of economic inequality on innovation cannot ignore the top-end inequality. A constellation of tax reforms is almost certainly a necessary part of this solution, given the erosion of the top income tax rates over time. But tax policy alone cannot be the only answer. As noted above, financialization is likely a major culprit in the shift in the American way of doing business, with implications for innovation and entrepreneurship flowing through several financial capital and human capital channels. Undoing the consequences of financialization may require corporate governance reforms that tackle the problems associated with shareholder value theory—the prevailing corporate ethos of maximizing short-term returns at the expense of longer-term growth, stability, and innovation, often at the expense of the worker.60

Finally, and critically: The vast majority of Americans don’t work for a new business or a high-tech startup, and they aren’t entrepreneurs. Half of private-sector employment in the United States is accounted for by the less than 1 percent of firms with more than 500 employees.61 This basic fact has critical implications for policy, namely that boosting economic dynamism and promoting entrepreneurship requires boosting the quality of life for all Americans. We don’t know where the next blockbuster idea might come from, and therefore we should be promoting an economy where all people have the capacity to pursue those great ideas, regardless of their current economic status.

We don’t know where the next great American breakthrough innovation will come from, which means that bread-and-butter economic policy issues are important, including policies that don’t immediately come into play in the entrepreneurship debate—or, if they do, typically get treated as anti-small business. Consider policies such as the minimum wage, paid sick and parental leave, and expanded access to child care. All have potential implications for promoting overall economic growth and dynamism in the United States, and belong on the table. If the goal is to stimulate transformational entrepreneurship, it is not enough just to push narrow policies designed to “support entrepreneurs.” We need a comprehensive package of creative solutions that move the entire economy toward broad-based health and growth for all.

About the author

Elisabeth Jacobs is Senior Director for Policy and Academic Programs at the Washington Center for Equitable Growth. Her research focuses on economic inequality and mobility, family economic security, poverty, employment, social policy, social insurance, and the politics of inequality. Prior to joining Equitable Growth, she was a Fellow in Governance Studies at the Brookings Institution, a co-founder of Brookings’ popular Social Mobility Memos blog, and a frequent public commentator on inequality, mobility, and the implications of the Great Recession for American families. Earlier in her career, Elisabeth served as Senior Policy Advisor to the Joint Economic Committee of the United States Congress, and as an advisor to the U.S. Senate Committee on Health, Education, Labor and Pensions. She holds a Ph.D. and an A.M. from Harvard University, where she was a Fellow in the Multidisciplinary Program in Inequality and Social Policy at the Kennedy School of Government, and a B.A. from Yale University, where she served on the Board of Directors of Dwight Hall, the Center for Public Service and Social Justice.

Acknowledgements

I would like to thank the Ewing Marion Kauffman Foundation for its invitation to participate in a roundtable retreat dedicated to “America’s New Entrepreneurial Growth Agenda,” for which I prepared an earlier version of this paper for presentation. Many thanks to my colleagues Heather Boushey and John Schmitt for their comments, and Nick Bunker for his help researching aspects of this paper. I also would like to thank my art and editorial colleagues Austin Clemens, Dave Evans, David Hudson, and Ed Paisley for their telling graphics and sharp editing. Any mistakes or errors in the paper are of course my own.

End Notes

1. Saez, Emmanuel. 2013. “Striking It Richer: The Evolution of Top Incomes in the United States.” Berkeley, CA: University of California.

2. Congressional Budget Office. 2011. “Trends in the Distribution of Household Income Between 1979 and 2007.” Washington, DC: Congressional Budget Office.

3. Zucman, Gabriel. 2014. “Wealth Inequality in the United States Since 1913: Evidence from Capitalized Income Tax Data.” NBER Working Paper No. 20625. Cambridge, MA: National Bureau of Economic Research.

4. Mishel, Lawrence, Josh Bivens, and Heidi Shierholz. 2012. The State of Working America (12th Edition). Ithaca: Cornell University Press.

5. Kuznets, Simon. 1955. “Economic Growth and Income Inequality.” American Economic Review XLV(1): 1-28.

6. Berg, Andrew G. and Jonathan D. Ostry. 2011. “Inequality and Unsustainable Growth: Two Sides of the Same Coin?” 2011. IMF Staff Discussion Note. Washington, DC: International Monetary Fund.

7. Van der Weide, Roy and Branko Milanovic. 2014. “Inequality is Bad for Growth of the Poor (But Not for That of the Rich). World Bank Policy Research Working Paper 6963. Washington, DC: World Bank.

8. Hendren, Nathanael. 2014. “The Inequality Deflator: Interpersonal Comparisons without a Social Welfare Function.”

9. Furman, Jason. 2014. “Patents, Innovation, and Productivity.” Speech to the Sixth Annual Patent Law and Policy Conference, Georgetown University Law Center and University of California, Berkeley Center for Law and Technology.

10. Arrow, Kenneth. 2012. “The Economics of Inventive Activity over Fifty Years.” In The Rate and Direction of Inventive Activity Revisited, eds. Josh Lerner and Scott Stern. Chicago, IL: University of Chicago Press.

11. Simon Kuznets observed in 1962 that the greatest challenge to understanding the role of innovation in economic processes has been the lack of meaningful measures of innovative inputs and outputs. Despite major advances in data collection capturing innovation (patents, research and development, stock market values of inventive output), precise operationalization of innovation remains a slippery task. See, for instance, Acs, Zoltan J. and David Audretsch. 1988. “Innovations in Large and Small Firms: An Empirical Analysis.” American Economic Review 78(4): 678-690.

12. Acs, Zoltan J. and David Audretsh. 1990. Innovation in Small Firms. Cambridge, MA: MIT Press.

13. Decker, Ryan et. al. 2014. “The Role of Entrepreneurship in U.S. Job Creation and Economic Dynamism.” Journal of Economic Perspectives 28(3): 3-24.

14. Hathaway, Ian. 2013. “Tech Starts: High-Technology Business Formation and Job Creation in the United States.” Kauffman Foundation Research Series: Firm Formation and Economic Growth. Kansas City, MO: Ewing Marion Kauffman Foundation.

15. Decker et. al. 2014.

16. Haltiwanger, John et. al. 2013. “Who Creates Jobs? Small versus Large versus Young.” Review of Economics and Statistics XCV(2): 347-361.

17. Schoar, Antoinette. 2010. “The Divide Between Subsistence and Transformational Entrepreneurship.” In Innovation Policy and the Economy, eds. Joshua Lerner and Scott Stern. Chicago, IL: University of Chicago Press.

18. Baumol, William J. 2008. “Entrepreneurship and Innovation: The (Micro) Theory of Price and Profit.” Paper prepared for the Annual Meeting of the American Economic Association. https://www.aeaweb.org/annual_mtg_papers/2008/2008_345.pdf. See also Baumol, William J. 2004. The Free-Market Innovation Machine: Analyzing the Growth Miracle of Capitalism. Princeton, NJ: Princeton University Press.

19. OECD. 2015. “The Future of Productivity.” http://www.oecd.org/eco/growth/OECD-2015-The-future-of-productivity-book.pdf.

20. Decker, Ryan, John Haltiwanger, Ron Jarmin, and Javier Miranda. 2016. “Changing Business Dynamism: Volatility or Responses to Shocks?” Paper presented at the 2016 Meeting of the Allied Social Science Associations. January 5, 2016. San Francisco, CA.

21. Hurst, Erik and Benjamin Wild Pugsley. 2011. “What Do Small Businesses Do?” NBER Working Paper No. 17041. Cambridge, MA: National Bureau of Economic Research.

22. Hurst and Pugsley, 2011.

23. Decker et. al., 2014.

24. Reedy, E.J. and Robert E. Litan. 2011. “Starting Smaller, Staying Smaller: America’s Slow Leak in Job Creation.” Kauffman Foundation Research Series: Firm Formation and Economic Growth. Kansas City, MO: Ewing Marion Kauffman Foundation.

25. Decker et. al. 2014.

26. The decline in job destruction associated with the slowdown in new business formation is the result of a somewhat complicated set of forces. Some of the job destruction associated with new firms may be because of “creative destruction”—new firms successfully challenging business models of older firms and putting them out of business. More of the job destruction associated with new business formation is due to the fact that most new businesses fail, so an uptick in the number of new businesses also means an uptick in the number of jobs destroyed. The successes of gangbusters new businesses outweigh the many small failures of the low-performing small businesses, which means that on average new business formation does more to create jobs than it does to destroy jobs.

27. Decker et. al. 2014.

28. See, for instance, Topel, Robert H. and Michael P. Ward. 1992. “Job Mobility and the Careers of Young Men.” Quarterly Journal of Economics 107(May): 441-79; Patricia M. Anderson and Bruce D. Meyer, “The Extent and Consequences of Job Turnover,” Brookings Papers on Economic Activity: Microeconomics (1994): 177–248; Henry S. Farber, “Mobility and Stability: The Dynamics of Job Change in Labor Markets,” in Handbook of Labor Economics, ed. Orley Ashenfelter and David Card (New York: Elsevier, 1999), 2439–2483; Monica Galizzi and Kevin Lang, “Relative Wages, Wage Growth, and Quit Behavior,” Journal of Labor Economics 16, no. 2 (April 1998): 367–391.

29. See, for example: Chetty, Raj et. al. 2014. “Where is the Land of Opportunity? The Geography of Intergenerational Mobility in the United States.” NBER Working Paper 19843. Cambridge, MA: National Bureau of Economic Research; Corak, Miles. 2013. “Income Inequality, Equality of Opportunity, and Intergenerational Mobility.” Journal of Economic Perspectives 27(3): 79-102.

30. Bell, Alex, et. al. 2015. “Innovation Policy and the Lifecycle of Inventors.” Presentation of preliminary research. Brussels, Belgium. As Bell and his co-authors note, patents are a widely used yet imperfect metric for innovation.

31. Bell, Alex, et. al. 2015.

32. Bell, Alex, et. al. 2015.

33. Bell, Alex, et. al. 2015.

34. Hoxby, Caroline, and Christopher Avery. “The Missing ‘One-Offs’: The Hidden Supply of High-Achieving, Low-Income Students.” Brookings Papers on Economic Activity 46, no. 1 (Spring) (2013): 1–65

35. White House Council of Economic Advisers. June 2014. “Nine Facts About American Families and Work.” https://www.whitehouse.gov/sites/default/files/docs/nine_facts_about_family_and_work_real_final.pdf.

36. Bianchi, Suzanne M. 2011. “Family Change and Time Allocation in American Families.” The Annals of the American Academy of Social and Political Science 636(1): 21-44.

37. Cooper, Marianne. 2014. Cut Adrift: Families in Insecure Times. Berkeley, CA: University of California Press; Ramey, Garey and Valerie Ramey. 2010. “The Rug Rat Race.” Brookings Papers on Economic Activity 41(1): 129-199. Washington, DC: Brookings Institution.

38. Bianchi, Suzanne M. 2011. “Changing Families, Changing Workplaces.” Future of Children 21(2): 15-36.

39. Taylor, Paul, et. al. 2008. “Inside the Middle Class: Bad Times Hit the Good Life.” Washington, DC: Pew Research Center.

40. Lusardi, Annamaria, et. al. 2011. “Financially Fragile Households: Evidence and Implications.” NBER Working Paper 17072. Cambridge, MA: National Bureau of Economic Research.

41. Acs, Greg and Austin Nichols. 2010. “America Insecure: Changes in the Economic Security of American Families.” Washington, DC: Urban Institute. See also Jacob S. Hacker and Elisabeth Jacobs. 2008. “The Rising Instability of American Family Income, 1968-2004: Evidence from the Panel Study of Income Dynamics.” Washington, DC: Economic Policy Institute.

42. For more on the shift of economic risk from institutions to individuals, see Hacker, Jacob S. The Great Risk Shift: The New Economic Security and the American Dream. New York, NY: Oxford University Press.

43. Evans, David, et. al. 1989. “An Estimated Model of Entrepreneurial Choice Under Liquidity Constraints.” Journal of Political Economy 97:808-827.

44. Mondragón-Vélez, Camilo. 2009. “The Probability of Transitioning to Entrepreneurship Revisited: Wealth, Education, and Age.” Annals of Finance 5:421-441.

45. Fry, Richard and Rakesh Kochhar. 2014. “America’s Wealth Gap Between Middle-Income and Upper-Income Families Is Widest on Record.” Washington, DC: Pew Research Center. http://www.pewresearch.org/fact-tank/2014/12/17/wealth-gap-upper-middle-income/.

46. Wolff, Edward N. “The Asset Price Meltdown and the Wealth of the Middle Class.” NBER Working Paper 18559. Cambridge, MA: National Bureau of Economic Research.

47. Ibid.

48. Saez, Emmanuel. 2013.

49. Zucman, Gabriel. 2014.

50. Kaplan, Steven N. and Joshua Rauh. 2010. “Wall Street and Main Street: What Contributes to the Rise in the Highest Incomes? Review of Financial Studies 23(3): 1004-1050.

51. Lin, Ken-Hou and David Tomaskovic-Devey. 2013. “Financialization and U.S. Income Inequality, 1970-2008.” American Journal of Sociology 118(5): 1284-1329.

52. Davis, Gerald. 2009. Managed by Markets: How Finance Reshaped America. New York, NY: Oxford University Press.

53. Stockhammer, Engelbert. 2013. “Why Have Wage Shares Fallen? A Panel Analysis of the Determinants of Functional Income Distribution.” ILO Conditions of Work and Employment Working Paper Series Report No. 35. Geneva, Switzerland: International Labor Organization.

54. Gompers, Paul, et. al. 2003. “Entrepreneurial Spawning: Public Corporations and the Genesis of New Ventures, 1986-1999.” NBER Working Paper No. 9816. Cambridge, MA: National Bureau of Economic Research. See also Mason, J.W. “Disgorge the Cash: The Disconnect Between Corporate Borrowing and Investment.” New York, N.Y.: Roosevelt Institute, February 25, 2015. http://rooseveltinstitute.org/disgorge-cash-disconnect-between-corporate-borrowing-and-investment-1/.

55. Gilens, Martin and Benjamin Page. 2014. “Testing Theories of American Politics: Elites, Interest Groups, and Average Citizens.” Perspectives on Politics Fall(2014).

56. Fairlie, Robert, et. al. 2010. “Is Employer-Based Health Insurance a Barrier to Entrepreneurship?” Santa Monica, CA: Kauffman-RAND Institute for Entrepreneurship Public Policy.

57. The distinction between “subsistence” and “transformational” entrepreneurs is from MIT economist Antoinette Schoar, who developed the concepts to apply to developing economies. Schoar, Antoinette. 2010. “The Divide Between Subsistence and Transformational Entrepreneurship.” In Innovation Policy and the Economy, eds. Joshua Lerner and Scott Stern. Chicago, IL: University of Chicago Press.

58. Hombert, Johan, et. al. 2014. “Can Unemployment Insurance Spur Entrepreneurial Activity?” NBER Working Paper 20717. Cambridge, MA: National Bureau for Economic Research.

59. Olds, Gareth. 2014. “Entrepreneurship and Health Insurance.” Manuscript. Cambridge, MA: Harvard Business School; Olds, Gareth. 2014. “Food Stamp Entrepreneurs.” Manuscript. Cambridge, MA: Harvard Business School.

60. Stout, Lynn. “The Shareholder Value Myth.” European Financial Review April 13, 2013.

61. Decker et. al., 2014.