In many businesses, the explicit or implicit human-resources policy is LHFF–last hired, first fired. That means that workers who jump from a job in one firm to a job in another purchase a greater beta with respect to the business cycle along with the higher wages, better working conditions, and more interesting responsibilities that would lead them to jump. This seems the most likely explanation for the fact that more than one-fifth of the hiring we would expect to get at the current aggregate level of unemployment relative to job openings is not there. After the catastrophic downturn of 2008-9 and the subsequent half a decade noncovery, workers’ assessments of the risks taken on in jumping firms and thus going to the back of the tenure-in-job queue are likely to be greatly elevated. Everybody knows people who lost their jobs in 2008-9 and then had the devil’s own time finding another one.

How big a drag is this on productivity growth, if it is indeed the case that diminished risk tolerance is thus affecting not only physical investment but human capital investment in diminishing workers’ willingness to “invest” in a new (and better) employer-employee match? Does this have implications for where full employment is? My first thoughts are:

- If workers are indeed stickier, it becomes more expensive for firms to expand employment by raising wages–you have to raise everyone’s wages and yet you attract fewer good workers from other firms. This makes the Phillips Curve even flatter in a boom, and makes inflation less of a threat, meaning we are further from full employment than we thought.

-

Productivity growth is slower, which means that the NAIRU is higher in any model in which workers have labor market tightness-dependent expectations as to the warranted rate of real wage increase and the NAIRU equilibrates at a level at which that warranted rate is sustainable.

How big are these factors? I don’t even have a back-of-the-envelope guess as to whether they are important, or how important they are.

Nick?

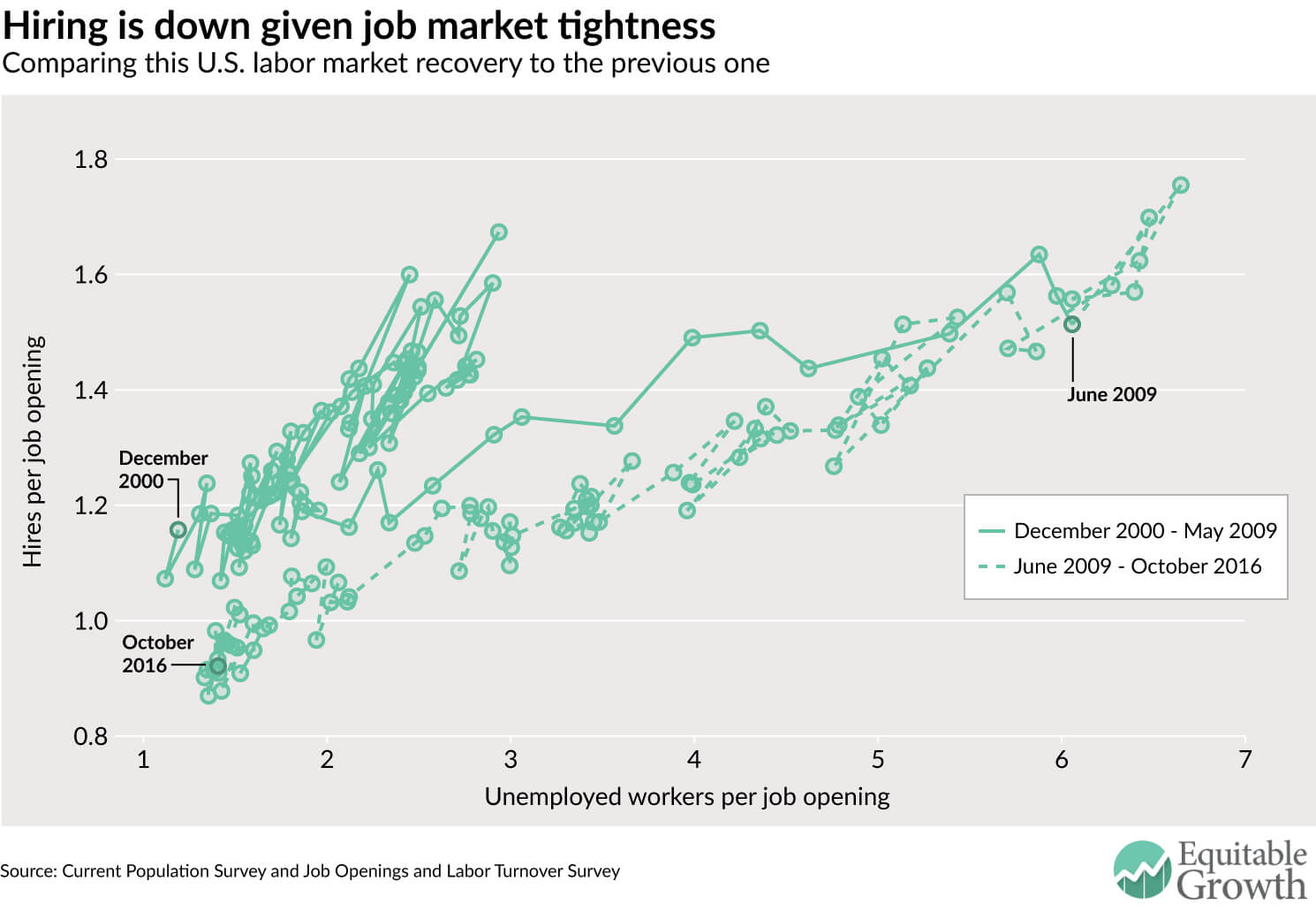

Nick Bunker: Labor Market Tightness and the Decline in Job Switching: “There’s less hiring for each job opening…

…Peter Diamond… and Ayşegül Şahin…. Hires of those out of the labor force are in line with previous recoveries, and hires of those who were unemployed are slightly lower, but… hires of… already employed workers has been quite weak compared to the tightness of the labor market. Such “job switching” has been trending downward for all age groups since 2000…. Something is amiss with either the willingness of workers to switch jobs or employers’ interest in hiring already employed workers…

Peter A. Diamond and Ayşegül Şahin: Disaggregating the Matching Function: :Decompositions of aggregate hires show how the hiring process differs across different groups of workers and of firms…

…Decompositions include employment status in the previous month, age, gender and education. Another separates hiring between part-time and full-time jobs, which show different patterns in the current recovery. Shift-share analyses are done based on industry, firm size and occupation to show what part of the residual of the aggregate hiring function can be explained by the composition of vacancies…