This is a weekly post we publish on Fridays with links to articles that touch on economic inequality and growth. The first section is a round-up of what Equitable Growth published this week and the second is the work we’re highlighting from elsewhere. We won’t be the first to share these articles, but we hope by taking a look back at the whole week, we can put them in context.

Equitable Growth round-up

Corporate profit-shifting is a problem for a source-based U.S. corporate tax system, but it’s also a problem for the measurement of gross domestic product. A new paper shows how increased profit-shifting has caused us to underestimate U.S. productivity growth.

In a paper released this week as part of the Equitable Growth working paper series, Owen Zidar of the University of Chicago finds that “the positive relationship between tax cuts and employment growth is largely driven by tax cuts for lower-income groups.”

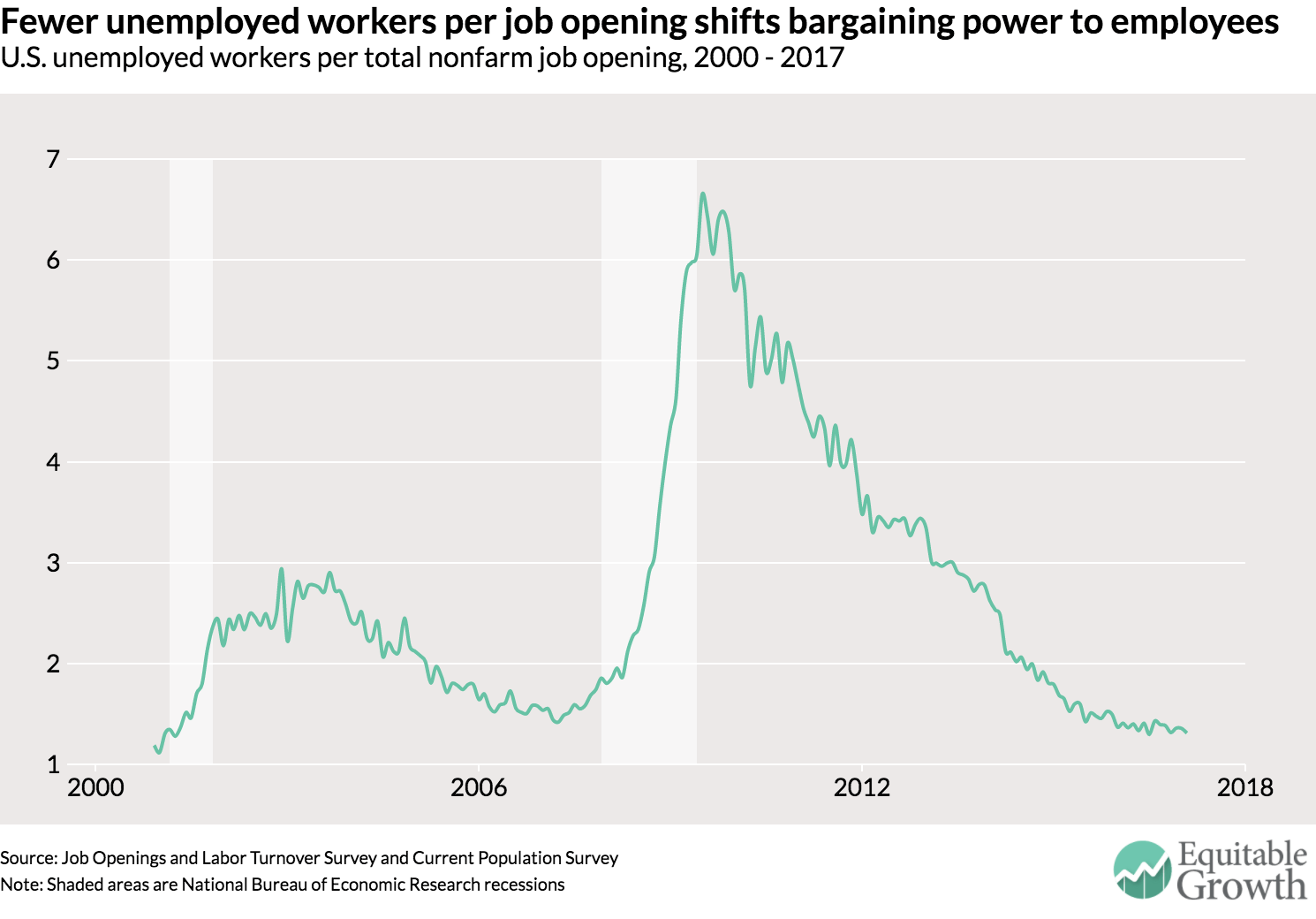

Data on labor market flows (hiring, firing, and quitting) from the Job Openings and Labor Turnover Survey for the month of February were released this week. Check out three key graphs from the new data.

Economists are increasingly drawing attention to the influence that firms have on levels of income inequality. A new paper shows that not only do firms decide which rungs workers start on a wage ladder, but also how fast they move up the income ladder.

Links from around the web

“[G]iven the broader trends in the U.S. economy away from manufacturing and toward services, . . . American men may need to move into traditionally female roles in coming years if they want to thrive.” Ana Swanson reports on new research on trends in occupations in the United States. [wonkblog]

Responding to new research, former Federal Reserve Chairman Ben Bernanke looks at how monetary policymakers can react to a world in which there is an increased likelihood of monetary policy hitting the zero lower bound. [brookings]

Why are some firms doing so much better than others these days? Maybe the answer is very simple: they have much better management. Noah Smith writes about new economics research on the impact of management. [bloomberg view]

The Economist writes about a recent conference on the decline of competition in the U.S. economy and concerns about the power of large firms and its interesting location: the University of Chicago. [the economist]

What’s the best macroeconomics model? Well, it depends on what question you want to answer. Former International Monetary Fund chief economist Olivier Blanchard writes about the need for (at least) five different kinds of macro models. [piie]

Friday figure

Figure from “JOLTS Day Graphs: February 2017 Report Edition” by Nick Bunker