New York Times columnist David Leonhardt made an excellent point in a column yesterday about the pace of U.S. economic growth and where the gains of that growth have accrued. Commenting on a graph made using data from a distributional national accounts data set, Leonhardt notes that the growth of the past several decades hasn’t resulted in most families getting much in the way of raises. It may be all but impossible to get back to the levels of aggregate growth levels of the postwar era, he argues, but “there is nothing natural about the distribution of today’s growth.”

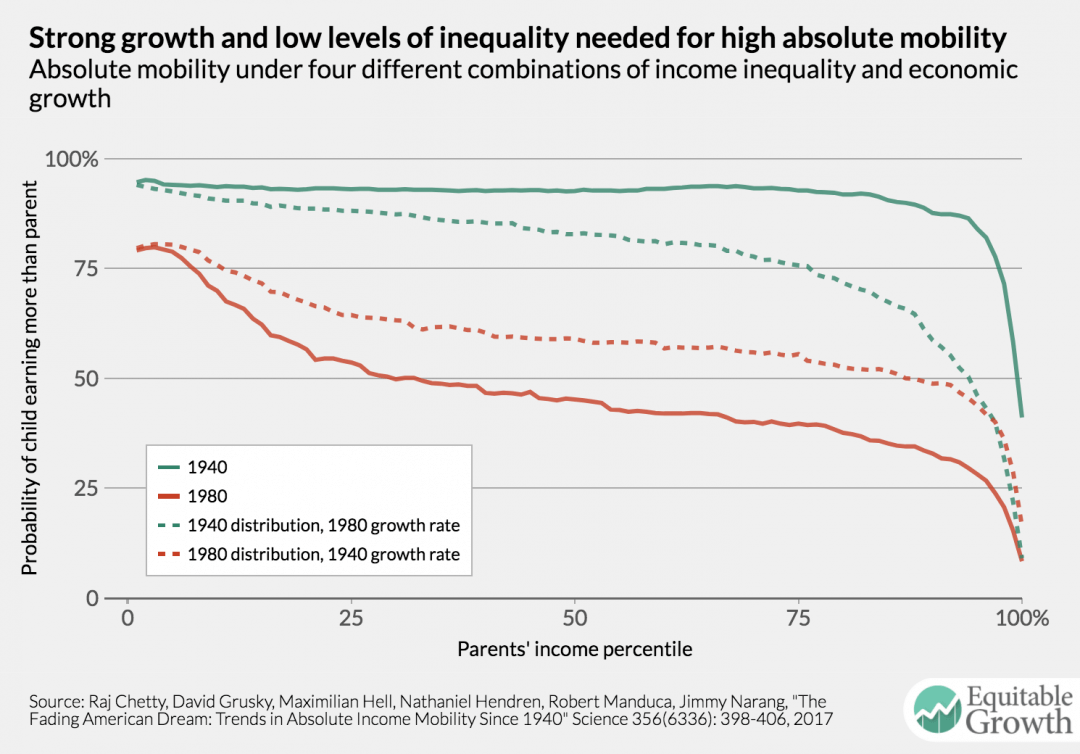

The consequences of such inequitable growth don’t just weigh on the living standards of one generation. They also affect the course of growth for future generations. Stanford University economist Raj Chetty and a group of researchers recently looked at the state of absolute mobility in the United States, or the likelihood that a child would earn the same amount of money or more than their parents at the same age. They found that the American dream, defined by levels of absolute mobility, is fading. A child born in 1940 had an almost 92 percent chance of earning more than their parents. Forty years later, someone born in 1980 would only have a 50 percent chance of outearning their parents.

The two big differences between the 1940–1970 period of high mobility and the 1980–2010 period of low mobility is that the second period had higher levels of income inequality and a lower rate of economic growth. Boosting both would almost certainly increase absolute mobility, but is one factor more significant than the other?

Chetty and his co-authors help answer this question by calculating how absolute mobility would change if they changed the income distribution and/or the level of growth. Figure 1 below shows four different scenarios. Two are easy enough to understand—the actual trends in mobility for the cohorts born in 1940 (the solid green line) and 1980 (the solid red line). But the other two lines are counterfactual trends. One line (the red dashed line) imagines a world where we keep the trends of high income inequality for the 1980 cohort but manage to boost growth from 1980 to 2010 to the fast pace that the U.S. economy experienced from 1940 to 1970. The other line (the green dashed line) imagines that we keep the slower growth of 1980 to 2010, but the growth ended up being distributed like the growth during 1940 to 1970. (See Figure 1.)

Figure 1

What the graph shows is that a faster-growing economy, but one that is still highly unequal, boosts mobility, but the increase in mobility is much higher when the distribution of slower growth is more equitable. The average rate of mobility when inequality and growth are both high would have been about 62 percent, compared with the average rate of about 80 percent when inequality and growth were both low.

Of course, absolute mobility is highest—an average of about 92 percent—when growth is both strong and equitably distributed. If we want to boost the living standard of future generations, policymakers need to take steps to boost economic growth and ensure that its benefits are broadly distributed.