Affirming the decision to move the target for interest rates up by a quarter of a percentage point last week, Federal Reserve Chair Janet Yellen said that “we continue to feel that with a strong labor market and labor market that’s continuing to strengthen, the conditions are in place for inflation to move up.” This decision by the Federal Open Market Committee, the monetary-policy-setting committee of the Federal Reserve, was reached despite seemingly weak inflation data and the continued streak of missing the Fed’s own 2 percent inflation target.

Ascribing a policy decision to one factor might be hasty, but the recent hike seems inspired by the Phillips curve. The curve shows a relationship between the unemployment rate and the rate of inflation, where inflation increases when unemployment goes down and vice versa. The underlying logic was laid out by William Dudley, president of the Federal Reserve Bank of New York, earlier this week: “We think if the labor market continues to tighten, wages will gradually pick up, and with that, we’ll see inflation get back to 2%.”

In short, with unemployment close to 4 percent, the Fed thinks this means that inflation will soon head toward 2 percent. But is the Phillips curve—at least the specific curve that seems to be informing these policymakers—the best guide right now? Or is it perhaps misguiding the Fed?

There’s some reason to be skeptical of the Fed’s implicit Philips curve. First, are policymakers certain that wage growth will be picking up anytime soon? Greg Ip argues in The Wall Street Journal that the current levels of nominal wage growth are as good as they get. Nominal wage growth hasn’t picked up as much as most economists would expect if an unemployment rate of near 4 percent meant what it did in the past.

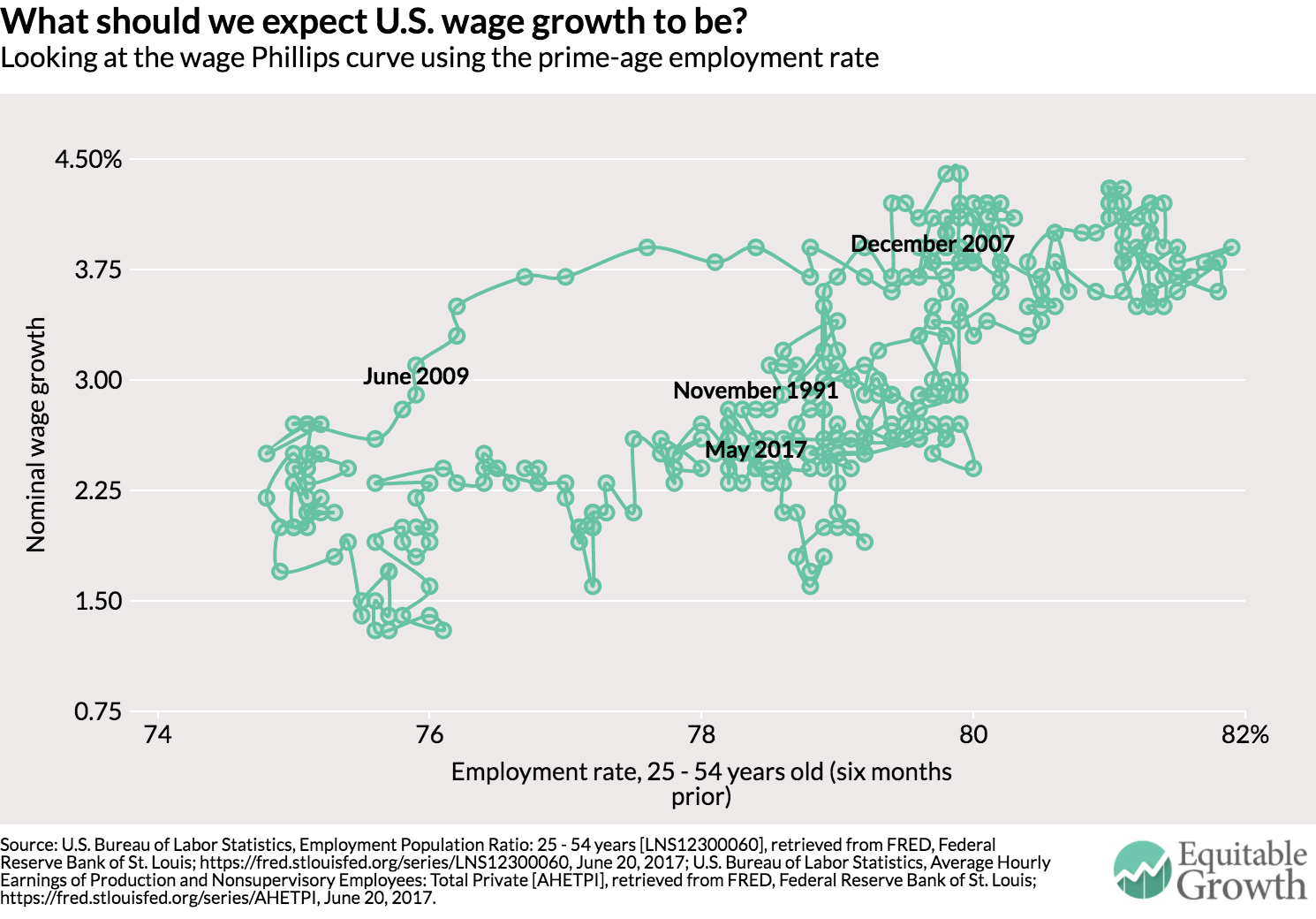

But with the decline in the labor force participation rate, perhaps 4 percent unemployment is not such a harbinger of more powerful wage growth. A look at the relationship between another measure of labor market tightness—the prime-age employment rate—and nominal wage growth shows the pre-recession relationship holding up. The levels of the employment rate and wage growth for May 2017, for example, are both around the levels for the early 1990s. (see Figure 1)

Figure 1

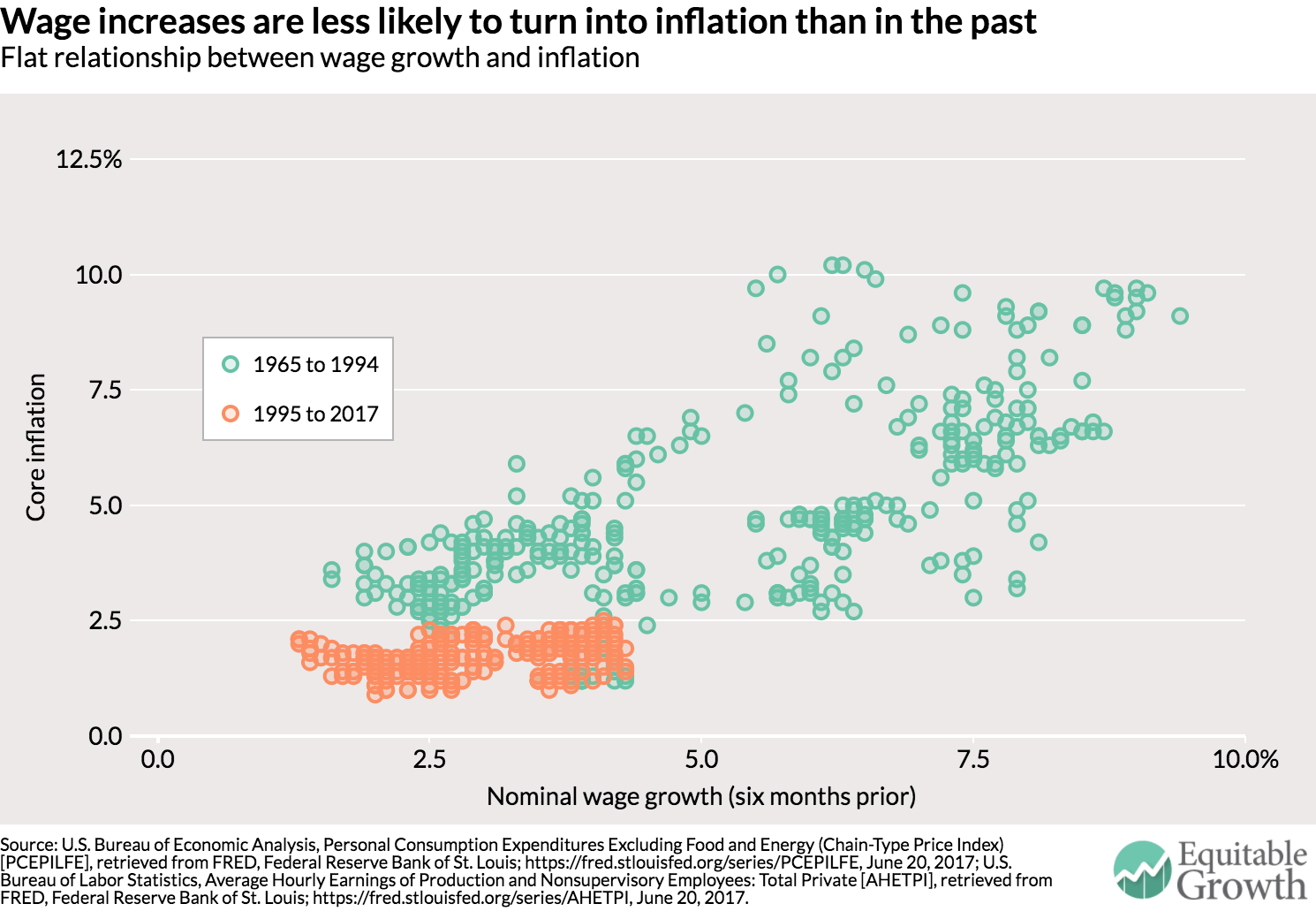

Looking at the prime-age employment rate, the labor market might have a bit more tightening to do before wage growth is going to pick up significantly. But if and when significantly higher wage growth does arrive, will it necessarily translate into higher inflation? That would require a strong passthrough of wage growth into higher inflation. But perhaps the recent increase in the share of income going to labor as the U.S. economy recovers indicates that companies are more willing to cut into their own share of income before hiking prices. Certainly, the relationship between wage growth and inflation today is quite flat. (see Figure 2)

Figure 2

Cardiff Garcia points out at FT Alphaville that the members of the Federal Open Market Committee have continuously underestimated how low the U.S. unemployment rate can go. Perhaps inflation will pick up once the effects of nearly 4 percent unemployment are felt, but if unemployment can go lower, then underestimating inflation again will result in fewer people with jobs and lower wage growth for those with them. That would be an unfortunate miscalculation based on perhaps misguided reliance on the Philips curve.

{kind=link}