This is a weekly post we publish on Fridays with links to articles that touch on economic inequality and growth. The first section is a round-up of what Equitable Growth published this week and the second is the work we’re highlighting from elsewhere. We won’t be the first to share these articles, but we hope by taking a look back at the whole week, we can put them in context.

Equitable Growth round-up

Since 2000 the concentration of businesses in the United States has increased and the amount of business investment relative to profits has declined. Are these two trends connected? New research argues that less competition and increased consolidation is pushing down investment growth.

Gene Kimmelman of Public Knowledge and Mark Cooper of the Consumer Federation of America make the case for stronger antitrust enforcement and regulatory oversight in the digital communications industry.

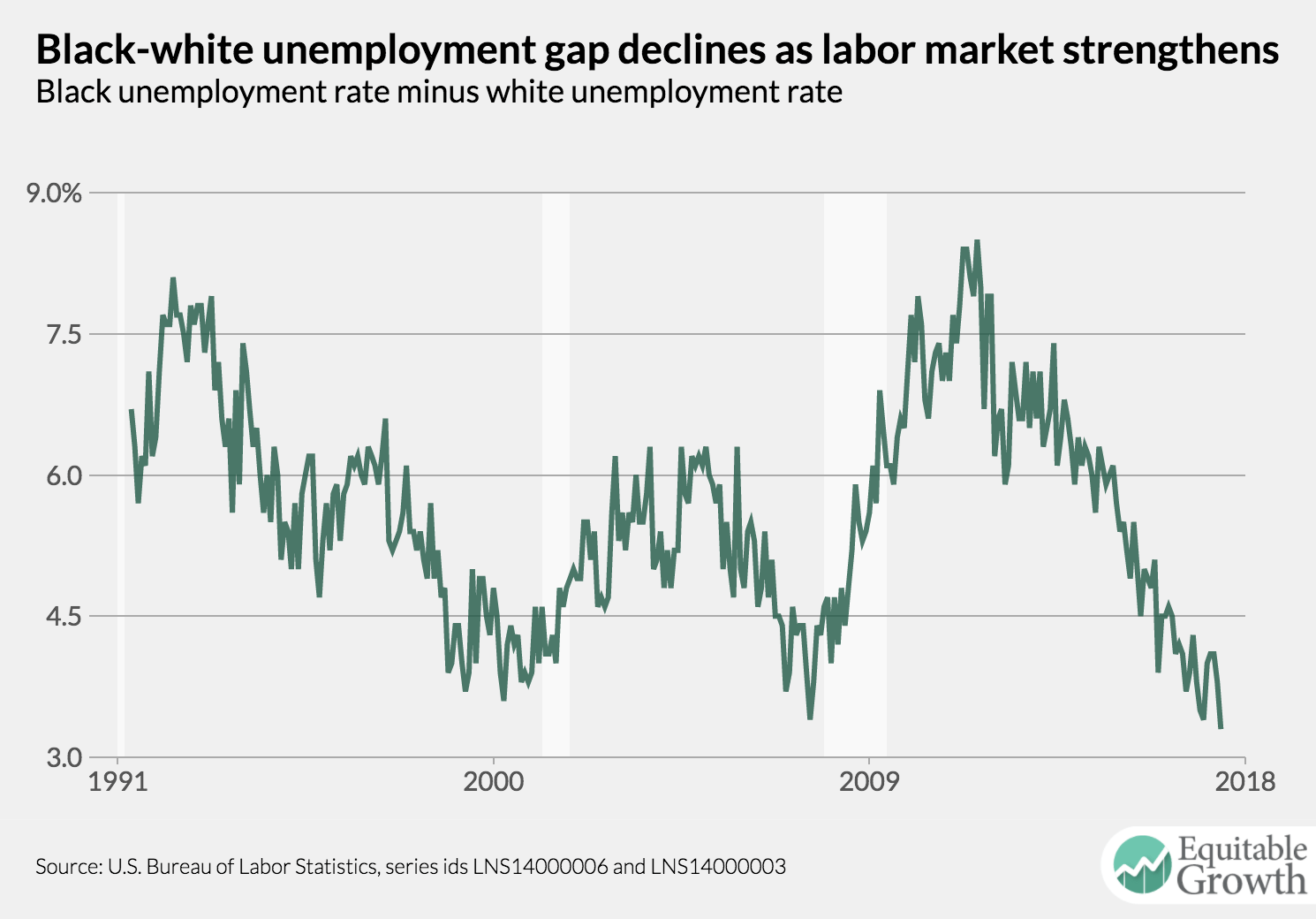

The gap between the unemployment rate for black and white Americans may be at a historical low, but the gap still exists. A recent research paper digs into why this gap remains and how it shrinks as the labor market gets stronger.

In the latest installment of Equitable Growth in Conversation, Heather Boushey talks with Robert Solow, institute professor, emeritus, and professor of economics, emeritus, at the Massachusetts Institute of Technology; Nobel laureate in economics; and a member of Equitable Growth’s Steering Committee.

Is excessive spending always and everywhere the reason for higher government debt? Summarizing some of his new research, John Jay College’s J.W. Mason explains how increasing debt is not equal to deficits.

Links from around the web

Despite increasing attention to the downsides of restrictive noncompete agreements, Idaho recently made it easier for employers to enforce them. Conor Dougherty goes to the state and sees how this new policy might hurt the local economy. [nyt]

How fast can the U.S. economy sustainably grow? Economists try to answer this question by calculating “potential GDP.” Matt Klein writes about new research that suggests most estimates are far underestimating potential GDP. [ft alphaville]

A recent study about the minimum wage increases in Seattle raised questions about the benefits and drawbacks of significantly higher minimum-wage levels. Arin Dube, economist at the University of Massachusetts, Amherst, writes that we should put more weight on studies that look at many minimum-wage increases across the country and not focus jUst on one state. [the upshot]

Many proposed solutions to the problem of “short-termism” in business and finance is to reward shareholders for holding stocks for a long time period. But Alex Edmans, professor of finance at London Business School, proposes “the focus should be on creating large shareholders, not long-term shareholders.” [hbr]

One of President Trump’s pledges on the campaign trail was to fight back against what he saw as unfair trade practices. In office, he seems likely to soon impose significant tariffs on steel. Annie Lowrey investigates into the possible effects doing so. [the atlantic]

Friday figure

Figure is from “Recessions, recoveries, and racial employment gaps in the United States” by Nick Bunker