…I did not dismiss the arguments of those who disagreed with me. There often has been reasonable, irreconcilable disagreement over the meaning of the Constitution…. Halbig and King… are different. I can accept… that the relevant provisions of the ACA are ambiguous. What I cannot accept as reasonable or responsible… is the argument… that the ACA Congress clearly and unambiguously accomplished what no Member of Congress, no one in the Congressional Budget Office, none of the four dissenting Justices in NFIB v. Sebelius, and no state official realized that Congress had accomplished when it passed the ACA: self-destructively limit the tax subsidies that make health insurance affordable for millions of Americans to those who have the good fortune of happening to reside in states that set up their own health insurance exchanges….

Some may conclude that I am not as tolerant of reasonable legal disagreement as I think I am or used to be. Others may conclude that I care too much about the draconian financial consequences for millions of Americans and insurance companies if this litigation succeeds. I have considered these possibilities, and I have rejected them. The plaintiffs’ case is so weak and transparently political that it is dismaying to see it be taken seriously.

Category: Equitablog

Weekend reading

This is a weekly post we publish every Friday with links to articles we think anyone interested in equitable growth should read. We won’t be the first to share these articles, but we hope by taking a look back at the whole week we can put them in context.

Saving our way out of wealth inequality?

Derek Thompson looks at the data on U.S. wealth inequality and considers how we can get the broad swath of Americans to save more [the atlantic]

Shane Ferro thinks the emphasis should be more on spurring income growth rather than directly increasing savings [business insider]

Requiems for quantitative easing

Steve Randy Waldman thinks quantitative easing is pretty terrible, but it was the best available option [interfluidity]

“The Fed needs a change in behaviour, a change in target, or a change in personnel.” Ryan Avent castigates the Federal Reserve for ending QE. [the economist]

He’s a businessman, not business, man

When hearing economic policy advice from business people, we need to remember that there is no representative business, says Ryan Decker. [updated priors]

The disconnect between profits and investment

“Financial engineering, in other words, is Apple’s hotly anticipated new product.” Matt O’Brien looks at why Apple is borrowing money while sitting on $155 billion in cash. [wonkblog]

Afternoon Must-Read: Nicholas Bagley: The Supreme Court Will Hear King. That’s Bad News for the ACA

In the other 31 states, Obamacare is doing fine and is likely to keep doing fine in spite of whatever the Supreme Court rules in King. In those 31 states, they either have state exchanges that are unaffected by King or will quickly add a state wrapper to their federal exchange: no state politicians of any party are going to accept ObamaCare money to cover their Medicaid poor and deny exchange subsidies to their middle class.

But the politicians and Obamacare are now in much bigger trouble in the nineteen states with one-third of the population: Alabama, Alaska, Florida, Georgia, Kansas, Louisiana, Maine, Mississippi, Missouri, Montana, Nebraska, North Carolina, Oklahoma, South Carolina, South Dakota, Tennessee, Texas, Wisconsin, Wyoming. If King brings down the hammer, will the politicians of the nineteen nullification states throw away the $40 billion in exchange subsidies to their middle-class citizens that are currently anticipated for 2016? That seems a very heavy political lift.

And I very much doubt that the King appellants will be able to round up their fifth vote: the Supreme Court would have to overrule long lines of statutory interpretation and break a great deal of administrative law in pieces to get there. They might: this is a very partisan Supreme Court that follows the election returns. But I think Roberts wishes to have a place in history different from that of MacReynolds.

the Supreme Court just agreed to review King v. Burwell, the Fourth Circuit’s decision upholding an IRS rule extending tax credits to federally established exchanges…. At least four justices… voted to take the case… The justices’ votes on whether to grant the case are decent proxies for how they’ll decide the case. The justices who agree with King wouldn’t vote to grant…. The justices who disagree with King… there are at least four such justices…. That means that either Chief Justice Roberts or Justice Kennedy will again hold the key vote. None of this bodes well for the government. That’s not to say the government can’t win. It might. As I’ve said many times, the statutory arguments cut in its favor. But the Court’s decision to grant King substantially increases the odds that the government will lose this case. The states that refused to set up their own exchange need to start thinking—-now—-about what to do if the Court releases a decision in June 2015 withdrawing tax credits from their citizens.”

Afternoon Must-Read: Ricardo Hausmann: The Economics of Inclusion

…often result from a particular form of exclusion….Thanks to more than two centuries of sustained growth, average per capita income in the OECD countries is just under $40,000–3.3, 11.3, and 17.7 times more than in Latin America, South Asia, and Sub-Saharan Africa, respectively. Sustained growth has obviously not included the majority of humanity…. GDP per worker in… Nuevo León in Mexico is eight times that of Guerrero…. Why would capitalists extract so little value from workers if they could get so much more out of them?…To form part of the modern economy, firms and households need access to networks…. But connecting to these networks involves fixed costs….It is the fixed costs that limit the diffusion of the networks. So, a strategy for inclusive growth has to focus on ways of either lowering or paying for the fixed costs that connect people to networks. Technology can help…. But in other areas, the issue involves public policy…. A strategy for inclusive growth must empower people by including them in the networks that make them productive. Inclusiveness should not be seen as a restriction on growth to make it morally palatable. Viewed properly, inclusiveness is actually a strategy that enhances growth.

Lunchtime Must-Read: Ryan Avent: Forget the 1%. It’s the Top 0.01% Who Are Really Getting Ahead in America

>…Saez and… Zucman… uses a richer variety of sources…. The share of wealth held by the bottom 90% is an effective measure of ‘middle class’ wealth…. In the late 1920s the bottom 90% held just 16% of America’s wealth—-considerably less than that held by the top 0.1%, which controlled a quarter of total wealth just before the crash of 1929…. By the early 1980s the share of household wealth held by the middle class rose to 36%—roughly four times the share controlled by the top 0.1%…. From the early 1980s… these trends have reversed…. The 16,000 families making up the richest 0.01%, with an average net worth of $371m, now control 11.2% of total wealth—-back to the 1916 share, which is the highest on record…. The top 0.1%… hold 22% of America’s wealth…. The outsize fortunes of the few would not be too worrying were they largely the product of entrepreneurial activity…. The club of young rich includes not only Mark Zuckerbergs… but also Paris Hiltons…. The share of labour income earned by the top 0.1% appears to have peaked… held in the form of shares… levelled off… held in bonds has risen… hint[ing] that America’s biggest fortunes may be starting to have less to do with building businesses…

1. Most wealth will be deployed, at least at the relevant margin, not in productive entrepreneurial or labor-complementary activities but in at best parasitic rent-seeking activities.

2. Democratic politics will not save us–that only exceptional circumstances in the twentieth century allowed for a democratic politics of progressive social insurance to level society and so promote social welfare in the face of the Gramscian hegemony of the *bourgeoisie*.

Both of these seem to me to be quite plausible, and perhaps true. But I think Piketty would have been very well-advised to have spent a lot more time backing them up in his book than he in fact did…

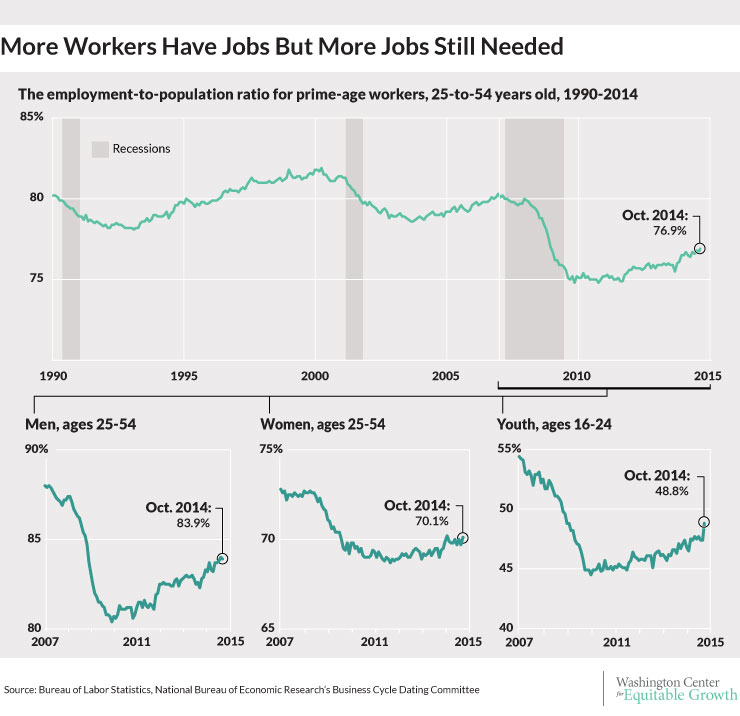

Employment gains continue without healthy wage growth

The U.S. Bureau of Labor Statistics today released their latest employment figures, which showed continuing jobs gains in October but with wage growth remaining weak. The share of prime-age workers (ages 25 to 54) with jobs rose 0.2 percentage points to 76.9 percent. Over the past three months, job growth averaged about 224,000 per month. But nominal wages (before factoring in inflation) only increased at an annual rate of 2.0 percent over the past quarter. This continuing inability to translate jobs gains into wage growth highlights the presence of slack in the U.S. economy, one of the reasons growing income inequality seems to be so stubbornly entrenched.

Starting with the job gains, prime-age working women with jobs rose 0.4 percentage points last month to 70.1 percent, compared to 69 percent a year ago. Employment for prime-age men, however, remained relatively unchanged. The overall employment-to-population ratio for prime-age workers is now 1.5 percentage points higher than it was last year, yet it remains 4.4 percentage points lower than its prior peak more than seven years ago, before the start of the Great Recession in December 2007. (See Figure 1.)

Figure 1

Perhaps the brightest spot in the jobs numbers released today was youth employment, which improved significantly. The share of workers ages 16 to 24 with jobs rose 1.4 percentage points in October. The employment-to-population ratio for young workers is now 48.8 percent, the highest rate for this age group in the past five years. At the same time, the youth employment needs substantial gains in order to reach its prior peak of 54.8 percent in 2006, let alone its high of 59.9 percent in 2000. Employment for 16-to-24 year-old workers never recovered from the 2001 recession, and then suffered steep losses again in the most recent recession.

The wage figures released today remain disheartening as nominal wages continue to increase at the less than satisfactory annual rate of 2.0 percent. We will not see sustained real wage growth until nominal average wages reliably increase at an annual rate of more than 3.5 percent, assuming the Federal Reserve’s target inflation rate of 2.0 percent and productivity growth of 1.5 percent. Nominal wage growth has been below the 3.5 percent threshold for more than five years.

Employment growth by sector was strongest in services industries. Much of the employment growth in October came from restaurants, with nearly 42,000 jobs added last month, and the retail sector, which increased by about 27,000 jobs. Both restaurants and the retail trade sector rely substantially on minimum wage workers—one reason real wage growth remains anemic across the country. Restaurant employment is up by about 3.1 percent over the past year, whereas retail grew by about 1.6 percent. In contrast, government employment remained essentially unchanged last month. For the overall private sector, average weekly hours increased slightly to 34.6 hours.

The employment gains from the October report are positive, but continued anemic wage growth is consistent with considerable weakness in the U.S. labor market. In addition, the latest economic growth statistics do not suggest we will make sustained improvements in eliminating the slack from the Great Recession, as the U.S. economy is not expected to rely on increased government spending and net exports. Until policymakers steer our economy toward more sustainable growth, broad-based real income gains for the vast majority of workers will remain elusive.

Things to Read at Lunchtime on November 7, 2014

Must- and Shall-Reads:

-

: Ben Bernanke: “Very Difficult” for ECB to Do QE: “‘The barriers to doing it are not really economic. The legal and political barriers being thrown up are going to make it very difficult to do that.’ Bernanke also fired back at critics of the Fed’s own easing programs, accusing them of ‘bad economics’ for saying that QE… would lead to inflation…. ‘There never was any risk of inflation. The economy was in great slack. If anything we were worried about deflation. Four years later there’s not a sign of inflation. The dollar is strengthening. They’re saying, “Wait another five years, it’s going to happen”. It’s not going to happen.'” -

: Here’s the latest dumb argument from a billionaire that will hurt the economy: “Hedge fund billionaire Paul Singer…. Never underestimate the ingenuity of inflation truthers…. His latest investor letter recycles all these ideas, inveighing against the Fed’s ‘fake prices,’ ‘fake money,’ and ‘fake jobs,’ before zeroing in on where inflation is really showing up–his wallet: ‘Check out London, Manhattan, Aspen and East Hampton real estate prices, as well as high-end art prices, to see what the leading edge of hyperinflation could look like.’ That’s right: Paul Singer thinks Weimar-style inflation might be coming because he has to pay more for his posh vacation homes and art pieces…. The Fed, you see, isn’t worried about the Billionaire Price Index. It’s worried about inflation on goods and services we all face…. Just because the super-rich are bidding up the prices of houses in the Hamptons doesn’t mean that middle-class people, whose wages are flat, are going to bid up the price of, well, anything…. If this is the best the inflation truthers can do, they should probably follow Mark Twain’s advice and keep their mouths closed…” -

: Rashomon in Euro Land: “Expansionary monetary policy is better than nothing, but a more stable euro zone requires expansionary fiscal policy now…. The problem is that northern countries do not want to implement expansionary fiscal policy…. Public debt is riskier in countries that cannot print their own currency… and the fiscally fragile periphery cannot implement expansionary policy without a backstop that can rule out debt runs. The only institution that can play this role is the European Central Bank…. If peripheral countries undershoot ECB’s ‘close, but below 2%’ inflation target, somebody needs to overshoot it. If Germany wants peripheral countries to become more like Germany, Germans may need to become more like southern Europeans….The euro zone is flirting with deflation and yet there are members of the ECB board who oppose a more aggressive policy stance. It would be good to know what economic model they have in mind. Charles Wyplosz asked; Mr Weidmann did not answer.” -

: Are Central Banks Losing Their Credibility on Inflation?: “We now have three major economies—the US, Japan, and Europe—which have persistently undershot their own inflation targets despite having enormous incentives to at least meet them as they try to recover from the Great Recession…. Everyone has assumed all along that if they were sufficiently motivated, central banks could always generate high inflation…. But what if it turns out that in practice it’s all but impossible for a modern central bank to meet even a modest inflation target during a severe economic downturn? How do we know whether this is due to lack of will; lack of technical firepower; or lack of political support? And how long does it take before markets decide it doesn’t much matter? After all, at some point there’s no practical difference between unwillingness and inability…. The longer this goes on, the more their credibility gets shredded. It’s a mystery why this isn’t an issue of bigger concern.” -

: Big Data: “In this period of ‘big data,’ it seems strange to focus on sampling uncertainty, which tends to be small with large datasets, while completely ignoring model uncertainty, which may be quite large. One way to address this is to be explicit about examining how parameter estimates vary with respect to choices of control variables and instruments.” -

: International Mensch Fund: “The IMF… concludes that it messed up by embracing fiscal austerity in 2010. It failed to understand that you need to differentiate between economies that borrow in someone else’s currency and those that don’t; it failed to appreciate that the negative effects of fiscal contraction would be much larger in a zero-lower-bound environment than historical patterns might suggest…. Let us nonetheless celebrate the IMF’s willingness to look honestly at its own record and learn from it…. Being a mensch… is all too rare in modern economic discourse, as the comedic evasions of the open-letter crew demonstrate. The Fund, it turns out, is better than that, and deserves praise.” -

: The Tacit Knowledge Economy: “Brazil in 2010… better social indicators than the United Kingdom had in 1960…. Colombia, Tunisia, Turkey, and Indonesia in 2010 compare favorably to Japan, France, the Netherlands, and Italy, respectively, in 1960. Not only did these countries achieve better social indicators in these dimensions; they also could benefit from the technological innovations of the past half-century…. So today’s emerging-market economies should be richer than today’s advanced economies were back then, right? Wrong…. Why can’t today’s emerging markets replicate levels of productivity that were achieved in countries with worse social indicators and much older technologies?… To make stuff, you need to know how to make it, and this knowledge is, to a large extent, latent–not available in books, but stored in the brains of those who need to use it…. Human capital is knowledge that is hard to transfer. Information is knowledge that is easy to transfer.”

Should Be Aware of:

-

: Salon Writer Condemns Arithmetic As Racist: “Salon’s Jenny Kutner… refuses to concede… that Davis lost among women: ‘The Tribune cited CNN exit polls to illustrate the landslide, saying Abbott “beat Davis… with… women (52-47)…. Last time I checked, though, there were thousands upon thousands of women in Texas considered Latina and African-American… their votes were solidly in Davis’ favor: 94 percent of black women and 61 percent of Latinas voted for her. Only 32 percent of white women did. That’s certainly not enough women to say that Abbott won the whole gender….’ It’s… not? My admittedly crude method of answering the question ‘Did Greg Abbott or Wendy Davis win the female vote’ would be to compare the number of women who voted for Abbott with the number of women who voted for Davis, and define the larger number as the winner. No way, says Kutner, citing Andrea Grimes…. ‘You’ll hear that Greg Abbott “carried” women voters in Texas. Anyone who says that is also saying this: that Black women and Latinas are not “women”… that carrying white women is enough…. As if women of color are some separate entity, some mysterious other, some bizarre demographic of not-women.’ Nobody is saying the votes of women of color don’t count. Everybody’s vote counts for one vote. I am comfortable stating that Barack Obama won the women’s vote in 2012, even though he lost white women. Kutner calls this method ‘the erasure of votes from women of color’. Well, no. Being outvoted is not erasure. Until somebody develops a new, less racist way of comparing the value of two numbers, people are going to define the winner of a group as the candidate with more votes.” -

: Knowing That Pundits Don’t Know What They’re Talking About Is A Huge Strategic Advantage: “Most political coverage is premised on some potentially noble lies about how the public will punish politicians who subvert basic institutional norms or prevent popular things from being done. McConnell’s evil genius is to see that it’s all nonsense. The public generally doesn’t pay attention to the details of political squabbles. For all intents and purposes nobody in Congress pays a real price for obstructionism; even if the popularity of the party is dragged down it doesn’t affect the election chances of the vast majority of members. By the same token, Republican statehouses can refuse the Medicaid expansion and Obama will get more blame than the Republicans who turn it down, and so on. This cold strategic logic presents a serious problem because the structure of American government requires certain norms of comity to function in most circumstances — we’re about to get a lot of grim lessons about the superiority of parliamentary systems that don’t massively dilute and misallocate accountability–but this isn’t McConnell’s problem.” -

: President Obama Can Safely Keep His Veto Pen in Mothballs: Ramesh Ponnuru is completely correct about this: ‘A strange amnesia has settled over much of the political world. I can’t count the number of articles I’ve read saying that the new Republican Congress is going to pass all sorts of legislation that President Barack Obama will veto. The latest example: George Will’s syndicated column urging the Republicans to pass several bills even if it results in ‘”a blizzard of presidential vetoes”.’ There’s no blizzard in the forecast. Senate Democrats will have the power to subject almost all legislation to filibuster (a word that does not appear in Will’s column).’…I’ve noticed the same thing Ponnuru did, and it’s weird. Is there some kind of unspoken assumption among pundits that Democrats aren’t going to routinely insist on a 60-vote threshold for Republican legislation? If so, I don’t know why. It seems pretty obvious to me that they will. At the very least, it allows them to keep most legislative negotiating leverage safely within the Senate, which is just where they want it. Basically, the next two years are going to be just like the last two. The only thing that will change is the order of the signatures on the consent agreements.”

-

: Reading Is Fundamental, Charles C.W. Cooke!: “I would indeed be a hypocrite if I were now advocating that Democrats threaten a debt default or to refuse to staff a Republican administration. But I am not advocating this…. Cooke’s entire argument is sub-coherent…. He is calling me a hypocrite because one argument that he claims I made but didn’t contradicts another argument he claims I made but didn’t. National Review should withdraw Cooke’s column, donate his day’s pay to a foundation promoting adult literacy, and impose a probationary period in which he is restricted to the use of no more than one middle initial.”

A Decent Monthly Establishment Employment Report This Morning: +214K Jobs: Daily Focus

But more important is to look at the Household Report trends: at the 59.2% for the adult employment-to-population ratio:

That means that the past year is the first year–the very first year–of the so-called “recovery” in which the employment-to-population ratio has not flatlined:

This past year is the first year in which we can say that anything like a labor market “recovery” is in process. (Yes, I know population aging–but there is a lot of data suggesting that the real estate crash of 2006-2009 induced a lot of unretirement to keep the voluntarily retired proportion of the adult population roughly constant.)

Of course, we are still very far away from anything like the normal we had grown used to from 1990-2007:

With a 59.2% adult employment-to-population ratio, we have no business having a 5.8% unemployment rate: no business at all:

But it is vastly better than having–as we had last October–a 58.5% employment-to-population ratio

Evening Must-Read: Hal Varian: Big Data

…it seems strange to focus on sampling uncertainty, which tends to be small with large datasets, while completely ignoring model uncertainty, which may be quite large. One way to address this is to be explicit about examining how parameter estimates vary with respect to choices of control variables and instruments.

Afternoon Must-Read: Ben Bernanke: “Very Difficult” for ECB to Do QE

…are not really economic. The legal and political barriers being thrown up are going to make it very difficult to do that.’ Bernanke also fired back at critics of the Fed’s own easing programs, accusing them of ‘bad economics’ for saying that QE… would lead to inflation…. ‘There never was any risk of inflation. The economy was in great slack. If anything we were worried about deflation. Four years later there’s not a sign of inflation. The dollar is strengthening. They’re saying, “Wait another five years, it’s going to happen”. It’s not going to happen.'”