The other two-tiered U.S. tax system: How pass-through businesses let the ultra-wealthy dodge federal taxes

Key Takeaways

- The U.S. tax system is characterized by many loopholes and structures that tend to favor the well-off over average U.S. taxpayers. One two-tiered system embedded in the tax code is the tax treatment of C corporations compared to that of so-called pass-through firms.

- Wealthy pass-through business owners tend to pay a lower tax rate than owners of C-corporations because pass-through firms do not pay the corporate income tax, increasing inequality and reducing economic efficiency.

- To avoid tax increases, large, complex pass-through entities often claim they are small businesses—a powerful but false political narrative. In fact, most pass-through income accrues to the richest Americans.

- Distinguishing genuine small businesses from large, complex pass-throughs—and requiring that complex businesses above a certain size be taxed as C corporations—would raise revenue and spur equitable growth. Such a proposal is currently generating positive interest from tax policy analysts and has historically enjoyed bipartisan support.

Overview

Many Americans likely remember when the legendary value investor Warren Buffett drew attention to a glaring unfairness in the tax code by pointing out that he paid a lower effective tax rate than his assistant. That observation about this two-tiered tax system sparked a national conversation—and, eventually, a policy proposal—about how investment income should not be taxed more lightly than income from wages.

But there is another two-tiered system embedded in the federal tax code that receives far less attention—one that may be just as consequential for tax fairness and economic efficiency. It is not about the difference between capital gains and ordinary income, the point Buffett was making, but rather about the difference between two types of businesses: C corporations and so-called pass-through firms. To understand it, it helps to once again look at Warren Buffett’s taxes and contrast his tax treatment to other extraordinarily rich Americans. Michael Bloomberg, the founder of the giant, privately owned wire service Bloomberg LP, can serve as an instructive example.

Buffett and Bloomberg are estimated to become roughly $5 billion richer every year on average (a measure of what economists call “economic income,” which, importantly, includes unrealized capital gains), and they each own large, profitable companies. But their tax bills look nothing alike—not because of any difference in their personal financial savvy, but because of how their companies are legally structured.

Berkshire Hathaway Inc., Buffett’s conglomerate, is a C corporation. That means it pays a 21 percent corporate income tax. Of course, few companies actually pay that statutory rate, making use of deductions and other tax-avoidance opportunities, including shifting profits overseas. But in part due to recently improved corporate tax reporting requirements, we happen to know that Berkshire Hathaway has paid quite a bit in corporate taxes to the U.S. Treasury Department in recent years.

Because the incidence of the corporate tax falls largely on shareholders, Buffett effectively bears a substantial share of it—bringing his total tax rate well above what most people assume. University of California, Berkeley economists Emanuel Saez and Gabriel Zucman landed on an estimate for Buffett’s total tax rate of 18.4 percent on $8.2 billion of economic income in 2018—the most recent year the public data on which Saez and Zucman rely was available—but that includes corporate tax payments to non-U.S. jurisdictions and assumes 100 percent of the incidence of the corporate tax falls on shareholders, which is higher than the more standard assumption of 75 percent. Eighteen percent is still too low, as Buffett himself has acknowledged, but is meaningfully higher than Bloomberg, his billionaire counterpart.

The reason: Bloomberg LP is organized as a partnership, a type of pass-through entity (the other main types are sole proprietorships and S corporations). Pass-throughs pay no direct corporate taxes. Instead, profits flow directly onto the owner’s individual tax return, where a range of sophisticated accounting strategies can be used to dramatically reduce what is owed in taxes.

One especially helpful loophole for pass-throughs is the qualified business income deduction, or Section 199A, a giveaway to rich business owners included in the 2017 Tax Cut and Jobs Act and permanently extended in the 2025 One Big Beautiful Bill Act. In 2018, Bloomberg is estimated to have received $68 million in tax savings from that provision alone.

On average, over the 5 years between 2014 and 2018, Bloomberg’s effective federal tax rate was a staggeringly low 1.3 percent. Unlike Buffett’s aforementioned 2018 rate, however, Bloomberg’s low rate does not include state, local, or foreign taxes, which would likely add a substantial sum to the total, based on his New York City residence, though it would still not be as high as Buffett. And while both men are well-known philanthropists, Bloomberg’s charitable tax deduction is considerably more valuable than Buffett’s because C corporation executives cannot use personal donations to offset their business’s income, whereas pass-through business owners such as Bloomberg can.

This is the other two-tiered tax system: one tier for C corporations and another far more favorable one for pass-through businesses.

The hidden wealth of pass-through owners

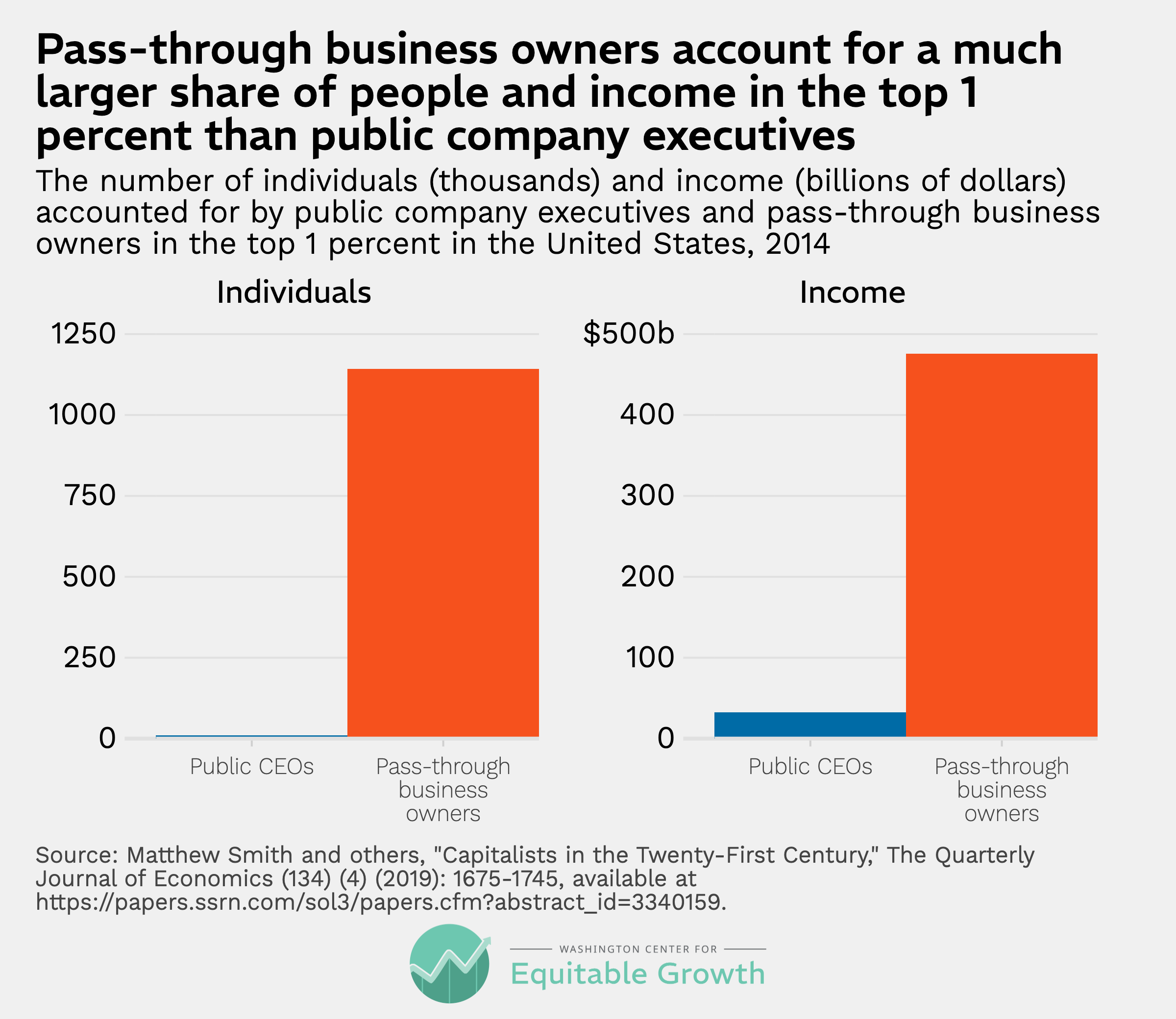

Bloomberg’s tax treatment is not an outlier. Pass-through income is concentrated heavily at the top of the U.S. income distribution. The top 1 percent of earners receives a disproportionate share of all pass-through income, and yet this group rarely features in public debates about taxing the wealthy. Such debates tend to focus on the CEOs of publicly traded companies, such as Mark Zuckerberg (of Meta Platforms Inc.) and Elon Musk (of Tesla Inc. and of SpaceX, which is expected to go public later this year). This group of executives represents the blue-chip face of American capitalism. Pass-through owners make up an enormous and largely invisible slice of the ultra-wealthy. (See Figure 1.)

Figure 1

One reason this group stays relatively hidden is structural. With few exceptions, a company must be organized as a C corporation to be listed on a public stock exchange. Pass-through owners remain private by definition.

The ‘small business’ shield

Whenever policymakers try to raise taxes on wealthy pass-through owners, a powerful political narrative emerges to stop them: “These are small businesses!” The argument goes that they are the engines of the U.S. economy. They create jobs. They take risks. Targeting them means targeting the local laundromat, the family-owned restaurant, the neighborhood hardware store, and so on.

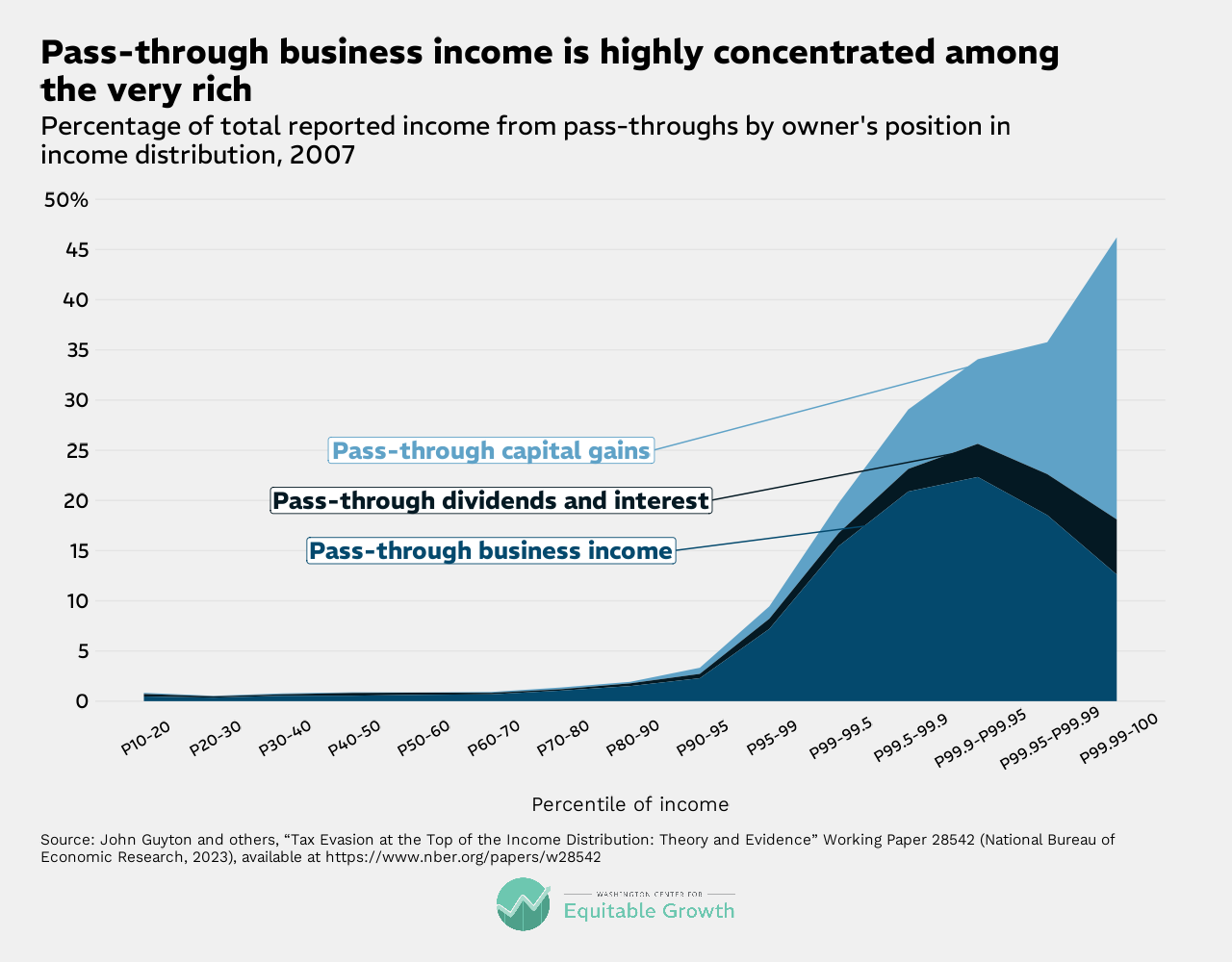

This is a compelling story, but it is mostly wrong. While it is true that many small businesses are organized as pass-throughs, the vast majority of pass-through income flows not to Main Street entrepreneurs but to massive privately held conglomerates, private equity funds, hedge funds, real estate investment vehicles, and venture capital firms. Moving up the income distribution, pass-through income becomes an increasingly dominant share of total earnings—and it increasingly looks like investment income, not the profits of a small business owner paying herself a salary and keeping the lights on. (See Figure 2.)

Figure 2

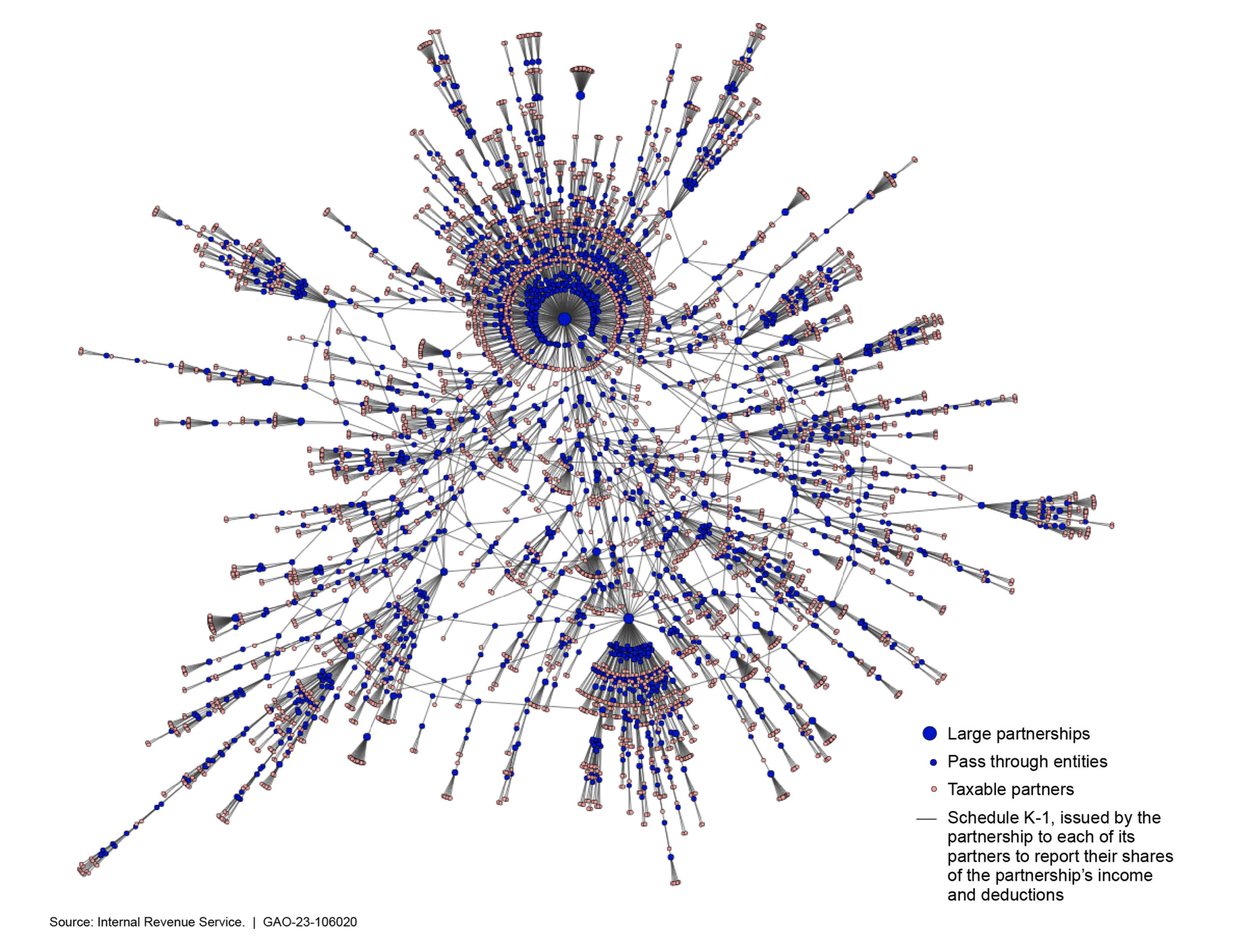

The complexity of these pass-through businesses is itself revealing. A single large partnership might involve dozens of separate legal entities, each a distinct pass-through, layered on top of one another. This complexity is not accidental. It serves to obscure the identities of the ultimate owners, complicate IRS audits, and—in some cases—facilitate the movement of money offshore. These are not your local laundromats. (See Figure 3.)

Figure 3

Large, complex partnerships involve a multitiered spiderweb of owners, including other partnerships

Illustrative example of a complex ownership structure for a large partnership in the United States

A path forward: Tax parity for large businesses

The good news is that the murkiness of this two-tiered business tax system also points toward a solution. If the problem is that large, complex pass-through entities are masquerading as small businesses, the answer is to stop allowing them to do so. By distinguishing genuine small businesses from large, complex pass-throughs—and requiring that complex businesses above a certain size be taxed as C corporations—policymakers can accomplish several things at once.

First, this would create tax parity between businesses of equivalent size and complexity, regardless of legal structure. Right now, the tax code creates a distorted incentive for large, complex companies to stay private precisely to preserve their pass-through status. Eliminating that incentive would make the tax system more neutral and economically efficient, spurring faster and more equitable economic growth. According to one rigorous estimate from economists Katarzyna Bilicka and former American Economics Association summer economics fellow at the Washington Center for Equitable Growth Sepideh Raei, both from Utah State University, fully equal treatment would increase U.S. Gross Domestic Product by 6.8 percent.

In the debate about Section 199A, pass-through lobbyists argue that their clients need the qualified business income deduction to achieve rough tax parity with C corporations. While their claims are mostly unsubstantiated, parity is a worthwhile objective and there is no better way to achieve it than by actual equal treatment.

Second, this policy reform would raise substantial revenue from the wealthiest Americans. With large pass-throughs brought into the U.S. corporate tax system, any increase in the corporate tax rate—from the currently very low 21 percent—would apply uniformly, without the current loophole that lets pass-through owners escape it entirely.

Third, taking this step would allow policymakers to credibly claim they are protecting small businesses—because they would be. By drawing a clear line between large, complex pass-throughs and true small businesses, reformers can defuse the most potent political weapon used against them. The corporate income tax is already one of the more popular and relatively straightforward mechanisms for taxing the wealthy. Building on it—rather than, say, defining a new tax base from scratch—offers a pragmatic path to a fairer system.

A number of tax policy analysts have recently reached similar conclusions. The Institute on Taxation and Economic Policy argues for strengthening the corporate tax by closing the “pass-through loophole,” among other improvements. Similarly, scholars from Columbia University, the University of Michigan, and Yale University make the case in a recent paper that the corporate tax better targets investment incentives and that “multi-tiered partnerships have rendered a growing share of business activity illegible to enforcement.” The co-authors urge policymakers to consider taxing all businesses as entities.

Some owners of bona fide small businesses also are expressing exasperation with this two-tiered business tax system, arguing for equal treatment. Historically, this has been a bipartisan idea, with expert commissions during both the George W. Bush and Obama administrations recommending this sort of unified business tax treatment.

Pinning down the technical details will be a challenge but is not insurmountable. There are ways to simply and cleanly define businesses of various sizes—by, say, gross revenue—while guarding against companies’ potential bad-faith attempts to stay under the threshold. Similarly, defining complex firms as those with multiple tiers of ownership and/or a certain number of nonindividual owners would be relatively straightforward to enforce and unlikely to ensnare any true small businesses, which have neither the resources nor the motivation to set up a multitentacled ownership structure.

However the policy details are designed, the core idea is simple: Two businesses of equal size and complexity should face the same tax rules. Right now, they do not. And the people who benefit most from that inequity are among the wealthiest Americans.

Note: Anthropic’s Claude AI tool helped draft an initial version of this column.

Did you find this content informative and engaging?

Get updates and stay in tune with U.S. economic inequality and growth!

Stay updated on our latest research