The unintended macroeconomic effects of U.S. climate policy uncertainty

Key takeaways

- Climate policy uncertainty is stagflationary, behaving like a supply shock. When climate policy uncertainty rises, output, investment, and employment fall, and prices rise.

- Climate policy uncertainty also shapes firm-level behavior, with firms postponing investment, scaling back production plans, and reducing R&D expenditures in times of greater uncertainty, suggesting firms view climate policy uncertainty as a material financial risk.

Overview

Recent policy developments in the United States highlight just how quickly climate policies can change. In January 2026, the U.S. Environmental Protection Agency announced that it would stop considering lives saved when setting rules on air pollution. Also this year, the agency overturned its own 2009 endangerment finding—the legal basis for regulating greenhouse gas emissions under the Clean Air Act of 1963.

These developments are emblematic of a broader pattern of policy reversals and debates over climate regulations in recent years. Such shifts in climate policies create uncertainty about the future direction of climate regulations. This uncertainty may affect the U.S. economy in ways that go beyond the direct effects of any particular regulation.

In a new paper, “The Macroeconomic Effects of Climate Policy Uncertainty,” by me and my co-authors Konstantinos Gavriilidis at the University of Stirling, Ramya Raghavan at Northwestern University, and Jim Stock at Harvard University, we study how uncertainty about climate policies affects the U.S. macroeconomy.

Our central finding is that uncertainty in climate policymaking behaves like a supply shock: Increases in uncertainty reduce output, investment, and employment while simultaneously pushing prices upward. This contrasts with other types of uncertainty shocks, which tend to propagate as aggregate demand shocks, moving output and prices in the same direction. We also find strong firm-level responses: Investment and R&D expenditures fall, with larger declines when firms have greater exposure to climate change.

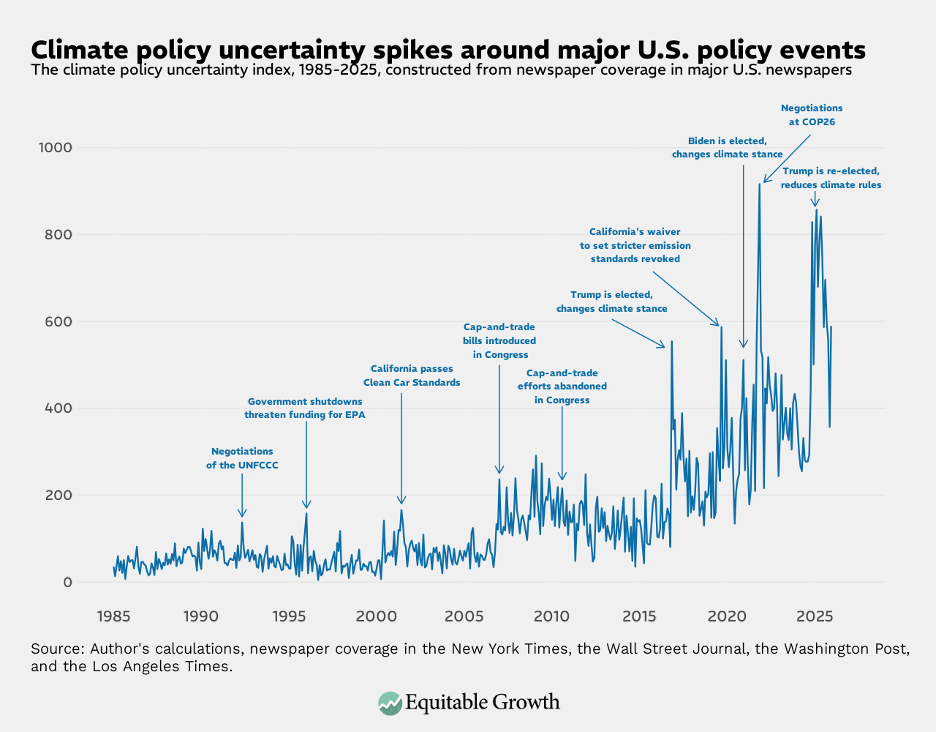

We define climate policy uncertainty as a lack of clarity and predictability about government actions to address climate change and related regulations. Measuring such policy uncertainty is very difficult. To overcome this challenge, we develop a news-based approach. We construct a dataset combining information from millions of news articles published in major U.S. newspapers since the mid-1980s. We identify articles that discuss uncertainty related to climate policies—such as debates over legislation, regulatory reversals, or shifts in international commitments—and aggregate them into a monthly index. The resulting index spikes around major policy events and captures movements that are largely distinct from broader economic policy uncertainty. (See Figure 1.)

Figure 1

Estimating the macroeconomic effects of climate policy uncertainty presents another challenge because movements in uncertainty may themselves be driven by economic conditions or other policy news. To isolate causal effects, we construct a narrative instrument based on 146 historically significant U.S. climate policy events that plausibly shifted uncertainty for reasons unrelated to the current state of the economy. Uncertainty rose sharply in 2009, for example, with the introduction of the Waxman-Markey American Clean Energy and Security Act, which proposed a national cap-and-trade system but faced an uncertain legislative path. Uncertainty also increased in June 2017, when the United States announced its withdrawal from the Paris Climate Agreement, creating ambiguity about the country’s long-run climate commitments.

An additional complication arises because policy news often contains two elements: information about the direction of policymaking (for example, whether regulation is tightening or loosening) and information about the uncertainty surrounding such policy changes. In many settings, these components move together—for instance, bad economic news often increases uncertainty. In the climate policy context, however, policy changes can either resolve or exacerbate uncertainty, depending on their credibility and permanence.

A clear and credible policy announcement, for example, may reduce uncertainty, even if it tightens a regulation. Conversely, contested or reversible policies may increase uncertainty even when they loosen regulations. We exploit this feature to separate the uncertainty component from changes in expected policy stringency. For instance, uncertainty rose both with the introduction of the Waxman-Markey cap-and-trade proposal in 2009 and with the U.S. withdrawal from the Paris Climate Agreement in 2017, even though these events implied opposite directions for future U.S. climate policy.

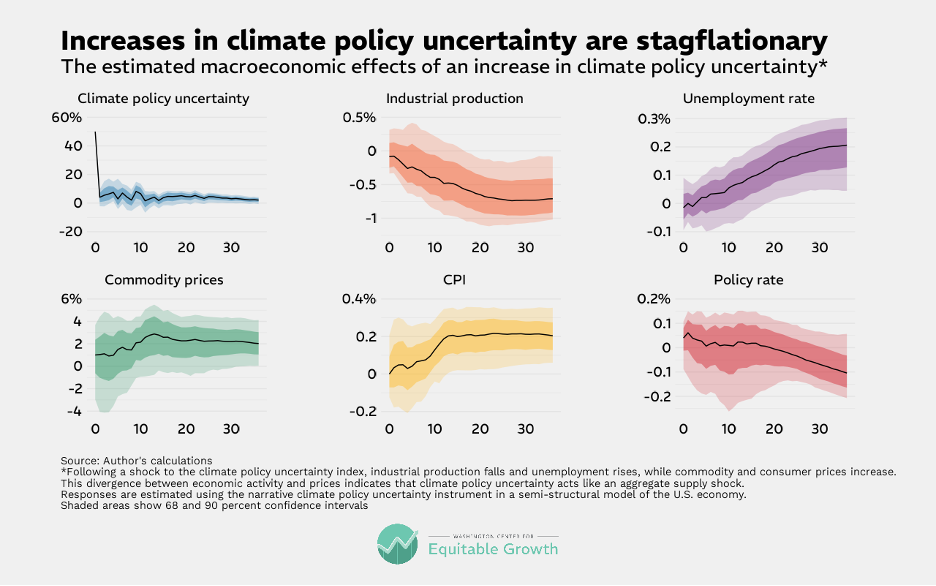

Using this instrument in a semi-structural model of the U.S. economy, we estimate the macroeconomic effects of a shock increasing climate policy uncertainty. We find that higher climate policy uncertainty leads to declines in output, investment, and employment. Greenhouse gas emissions also fall, largely reflecting the reduction in economic activity. At the same time, prices rise. (See Figure 2.)

Figure 2

These responses indicate that climate policy uncertainty propagates as an aggregate supply shock. When firms become uncertain about the future regulatory environment, they postpone investments, scale back production plans, or adopt more cautious production strategies to hedge against possible regulatory changes. At the same time, uncertainty raises expected future production costs due to the risk of stricter emissions standards or higher compliance costs. These responses reduce productive activity while putting upward pressure on prices, generating the combination of lower output and higher inflation—the classic definition of stagflation.

The results also reveal substantial effects at the firm level, with meaningful impacts on firms’ employment, investment, and R&D expenditures. This suggests that companies view climate policy uncertainty as a material financial risk. The effects are particularly pronounced when firms are more exposed to climate-related risks.

The findings from our paper have important implications for policymakers. Because climate policy uncertainty is stagflationary—reducing economic activity while raising prices—it creates a difficult trade-off for monetary policymakers. Central banks facing such shocks cannot simultaneously stabilize inflation and output as easily as they can in the case of demand-driven economic downturns.

More broadly, our results suggest that the macroeconomic consequences of climate policymaking extend beyond the direct effects of regulation. Uncertainty about the future path of climate policymaking can itself be a significant source of economic fluctuations. For policymakers, this highlights the importance of clear and credible policy frameworks that reduce uncertainty about the long-term trajectory of climate policies.

Did you find this content informative and engaging?

Get updates and stay in tune with U.S. economic inequality and growth!

Stay updated on our latest research