Month: January 2015

Weekend reading

This is a weekly post we publish every Friday with links to articles we think anyone interested in equitable growth should read. We won’t be the first to share these articles, but we hope by taking a look back at the whole week we can put them in context.

Monetary policy

Matthew C. Klein on the rise of borrowing in dollars outside of the United States and the implications for monetary policy. [ft alphaville]

Annie Lowrey on how central bankers should heed the lessons of the rap duo Outkast. [new york]

Capital and taxation

Peter Orzag argues that profit-sharing for employees can help alleviate the problems stemming from the decline of the labor share of income. [bloomberg view]

Justin Fox writes on the high price of avoiding taxes and corporate inversions. [bloomberg view]

The labor market

Allison Schrager looks at the data on labor force participation and finds that the dropouts are mostly students or retirees from high-income households. [businessweek]

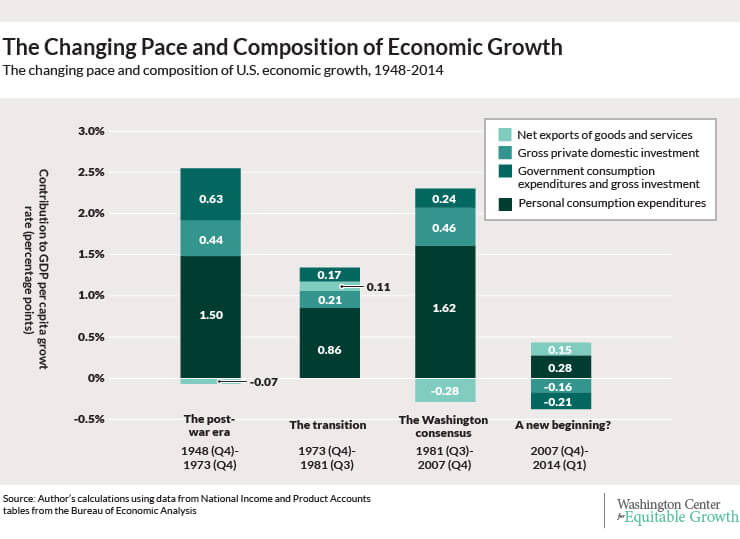

Friday Figure

Morning Must-Read: Chris Mooney: The Midwest’s Climate Future

for the business community–Michael Bloomberg… Hank Paulson, and… Tom Steyer–are back…. A higher prevalence of extremely hot temperatures could severely impact corn and wheat production, the report warns, unless we take serious evasive action…. By 2100… the more likely range for losses, says the document, is 11 to 69 percent…

A look at the near-term future of unionization rates

The U.S. Bureau of Labor Statistics later this morning will release new data on union membership and coverage for 2014 in the United States. Over the past several decades, these releases have shown a declining unionization rate as membership decreased as a share of the workforce. In 1983, the unionization rate was 20.1 percent but by 2013 it stood at 11.3 percent. What’s the implication of this trend and did it continue in 2014?

Before attempting to answer those questions let’s first look at the reasons for the decline of unionization. Globalization, changes in labor laws, and the shift of employment from highly unionized industries (manufacturing) to less-unionized industries (personal services) are the most likely factors. Regardless of the relative importance of each cause, the trend in unionization across the developed world has been about the same, down, which is indicative of this confluence of causes.

What’s more, there is no coincidence that the period of deunionization coincides with an era of rising income inequality. A wide range of research finds that declining union membership is associated with increases in income inequality. According to one study by University of California-Berkeley economist David Card, the decline in male unionization between 1973 and 1993 was responsible for between 12 to 20 percent of the increase in wage inequality. Looking at data from 1973 to 2007, sociologists Bruce Western at Harvard University and Jake Rosenfeld at the University of Washington find that deunionization explains between 20 to 33 percent of the increase in inequality.

So, what should we expect when BLS releases the numbers this morning?

Year-to-year movements are hard to guess, but it’s a good bet that the unionization rate won’t increase by any significant amount. There’s been a well-publicized return of manufacturing jobs over the past several years, but for the most part they’ve been returning to non-unionized firms. The National Labor Relations Board, the country’s semi-judicial agency overseeing labor law, has made several changes in recent years to help boost unionization. But these changes are at the edges, and while helpful, seem unlikely to reverse or even halt the trend.

So when looking at unionization rates in the private sector, trends in specific industries may be more interesting. Manufacturing jobs are returning, but whether this will boost the unionization rate in these industries has yet to be seen. In particular, look at the unionization rate for durable goods manufacturing, which includes the auto industry—the heart of many of the high-paid union jobs of the past.

In contrast, the unionization rate for public-sector employees has been relatively constant over the past several decades, hovering in the mid-to-upper 30 percent range. But over the past 5 years, politicians in several states successfully made a concerted effort to reduce union bargaining power and membership among state-and-local employees. The public unionization rate dropped 0.6 percentage points from 2012 to 2013. This downward trend may well have continued in 2014.

So given current trends, the future for the unionization rate looks negative. The rate in the United States is already quite low, below seven percent in the private sector. Can the trend be reversed? If not can the positive aspects of unions be brought back in a different form? And what would that mean for the future of income inequality? These are all difficult questions, with no easy answers.

Morning Must-Read: Mark Wilson: The Upshot

For an organization that is working as hard as it possibly can to become a trusted information intermediary–and, overwhelmingly, a *useful* trusted information intermediary–look at David Leonhardt’s The Upshot:

…an online news and data visualization portal on the New York Times’ website… entrust[ed]… to the paper’s former Washington bureau chief and economics columnist David Leonhardt…. To Leonhardt, The Upshot is more of a laboratory where he can lead a team of 17 cross-disciplinary journalists to rethink news as something approachable and even conversational. The goal: to enable readers to understand the news and by extension, the world, better. publisher. But we live in the puppy-GIF era…

Things to Read on the Evening of January 22, 2015

Must- and Shall-Reads:

- : “There must be a statute of limitations for those who say there will be inflation…”

- : The Davos oligarchs are right to fear the world they’ve made

- : “Roughly 6.3 million people… will drop their Obamacare coverage or face using as much as half of their income for health insurance if a Supreme Court ruling dismantles subsidies in states that haven’t established their own exchanges… nearly two-thirds of those who lose subsidies are white Southerners, and nearly half have full-time jobs…”

- : What have we learned about the ACA over the last year?

- : Higher Education, Wages, and Polarization

- : “Obama wasn’t exactly able to claim morning in America… but he was able to talk about success and moving forward…. Why the difference?… On the secular stagnation front… the euro area’s working-age population peaked in 2009…. Aggregate euro-area fiscal policy has been substantially tighter than in the US…. On the monetary side Europe zagged when America zigged… behaved throughout as if debt and inflation were the overwhelming risks…. Europe’s woes are no mystery, although it’s hard to allocate the blame; policy did everything wrong, so it’s hard to tell which wrongness mattered most…”

-

: Economist Appoints Its First Female Editor: “Zanny Minton Beddoes has been appointed editor of the Economist, the first female to land the role in the publication’s 170-year history…” -

: The Fall of the House of Samuelson: “[Paul] Samuelson was a convinced Keynesian… in a limited sense. He dismissed most of Keynes’s attack on the orthodox economics of his day as unnecessary, writing ‘had Keynes [started] with the simple statement that he found it realistic to assume that money wages…were sticky and resistant to downward movements… most of his insights would have remained just as valid.’ For Samuelson, Keynes’s real contribution was the tools he gave governments to prevent depressions. Reading The Samuelson Sampler, it is extraordinary to realize just how confident economists of his generation were that the New Economics… had solved the problem of depression and mass unemployment. As Samuelson put it in his 1973 introduction, ‘the specter of a repetition of the depression of the 1930s has been reduced to a negligible probability.’… Because governments knew how to stop depressions, voters would insist that they use this knowledge. ‘If printing bits of green can save banks and business from ruin,’ he argued in 1966, ‘today’s electorate will ensure that either party in power will [so] act.’ This was irrespective, Samuelson thought, of the ideological preferences of those in power…” -

: Why People Hate Economics, in One Lesson: “What is wrong with this?… Tabarrok and Cowen are trying to communicate… ‘incentives matter’… a methodological point… [that] should be presented in… as platitudinous [a way] as possible…. There are many ways of doing that, since the problem with the public… is not that they think incentives don’t matter… it’s just that they underestimate the[ir] power of incentives, or they don’t see some of the unexpected ways…. The right way… is to say ‘here’s something that we can all agree upon–but have you thought through the consequences of it? Perhaps not. That’s what economists do.’ But Tabarrok and Cowen are unable to restrain themselves…” -

: Betting Against Subprime Mortgages Was a Good Thing): “Billionaire Robert Burns… richly deserves to be ridiculed… [for] want[ing] people to get used to lower living standards…. People are wrongly attacking Burns when they complain about his betting against subprime mortgage backed securities…. The securities were in fact bad. Burns betting against them made that clear in the markets somewhat sooner than would have otherwise been the case, bringing down the bubble earlier and more rapidly. This is good… fewer people were caught up in it than if the bubble had continued…. It would have saved people an enormous amount of pain if there had been lots of Robert Burns betting against subprime mortgage backed securities in 2003-2004…. Burns was acting out of greed, not a desire to help the economy and society. But this is a case where greed was good…” -

: ECB QE. Much too Late and Not to Be Counted on: “The slow, drawn out, reluctant, piecemeal way that the ECB has handled the crisis… and the disputes that have raged about whether and how to do QE… minimise the bang per buck…. Second, in so far as QE works by signalling intentions about future central bank rates, there is now little to be got…. Third, in so far as QE acts through lowering term, liquidity or other premia, it’s too late for that too. Something has squeezed those premia out in Northern countries. And the risk that the remaining premia in the South reflect is not going to be taken off the local sovereign balance sheet…”

Should Be Aware of:

- : Now we know how many drivers Uber has, and how much money they’re making

- : “Hubbard is defending… the 2003 cuts in tax rates on dividends and long-term capital gains… all it did was boost payouts to shareholders…. Two-thirds of the benefits from the dividend tax cut went to the top 1 percent…”

- : CEO inanity, at the Davos World Economic Forum and beyond

- : “Week one, we had a Speaker election that didn’t go as well as a lot of us would have liked. Week two, we spent a lot of time talking about deporting children, a conversation a lot of us didn’t want to have. Week three, we’re debating reportable rape and incest–again, not an issue a lot of us wanted to have a conversation about. I just can’t wait for week four…”)

-

: High Broderism, Once Influential Conservative Democrat Edition: “Bill Galston, the prescient analyst cryogenically frozen at a 1991 DLC meeting, has some Deep Thoughts about the SOTU: ‘Still, as Mr. Obama began speaking, a key uncertainty remained: What balance would he strike between the desire to shape the political terrain for 2016 and the imperatives of governing in 2015? The former required bold initiatives, of a kind likely to evoke sharply negative reactions from Republicans who command majorities in both the House and the Senate. But successful legislating this year will require compromise with those very majorities. Could he thread the needle, making the Democratic political case for next year without undermining the possibility of legislative progress this year?’ Yes, in 2015 it’s very, very hard to tell if congressional Republicans would be willing to pass sensible middle-of-the-road compromises. But either way, I think that we can agree that whether it will happen will depend on the precise wording of the State of the Union address…” -

: On ECB QE: “€60 billion a month including: Sovereign Debt; Super-national (read EIB/ESM) debt; Asset-Back Securities; Covered Bonds. It does NOT include Corporate Bonds. (or equities..) It will buy bonds with remaining maturity between 2 and 30 years. It will buy inflation linked bonds. Purchases will start in March (in six weeks, when that month’s reserve maintenance period starts) and will continue until at least September 2016. The breakdown of purchases will be by Central Bank capital key, with the ECB itself accounting for 8% of purchases. So, if you want to work out how much each national central bank will buy, get the banks capital share here (be sure to adjust to 100% total), multiply that by €60bn, then multiply that by 0.92. Interestingly, there is nothing in the guidelines stopping an NCB buying the sovereign debt of another euro-area country, although it would be doing so at its own risk. I’ve written here about why the non-risk sharing is probably a good thing. But, also, I think ECB QE buying at this level is most likely to work more to weaken the € currency than necessarily have a positive portfolio effect. Overall, this is good news. It would be churlish to ask for more, at the moment.” -

: The Peripheral: “A blogpost on the William Gibson book of the same name, with copious spoilers… his best for some time; maybe, depending on your druthers, the best novel that he’s ever written…. Gibson… wants, I think, to talk about the relationship between the 99% and the 1%, using science fiction to turn the social relationships that Piketty and Saez talk about into a kind of ontology. The farther future is one in which the 1% has won and become a global ruling class…. The nearer future timeline is set in a rural America where the real economy has collapsed, leaving illicit drugs and dead end jobs working for the homeland security…. In this timeline, we don’t see the 1%, although they’re there in the background. Instead we see the kind of people who are about to be left behind and perish in the Jackpot…”

An Inadequate Note on Nick Bunker on Bank Leverage…

I’ve been trying to think of an intelligent comment to make on the extremely-fast-at-the-keyboard Taxation in the name of equity on the desirability of taxing borrowing by big banks. I strongly approve: too-big-to-fail banks are extremely bad news, I have come to believe, for three reasons:

- They create systemic risk.

- They are extremely powerful lobbyists–much more powerful than ten banks each one-tenth their size would be.

- Regulation of too-big-to-fail banks too-easily steps over the line into social-network revolving-door corruption.

For all these reasons, we want to make it hard to be a too-big-to-fail bank and profitable for managers and shareholders to split such things up–internalize these externalities!

But I find myself of divided mind on the more general Admati-Heilwig-Bunker point that banking should run with a lower debt-to-equity ratio. Equity capital is scarce in this world, and it is far from clear to me that it is best-deployed backstopping banks…

A Note on Carter Price’s: What Have We Learned About the ACA Over the Past Year?

The estimable in his What have we learned about the ACA over the last year? has a nice set of links (http://www.rand.org/blog/2014/04/survey-estimates-net-gain-of-9-3-million-american-adults.html https://www.cbo.gov/publication/45231 http://kff.org/health-reform/issue-brief/analysis-of-2015-premium-changes-in-the-affordable-care-acts-health-insurance-marketplaces/ http://kff.org/uninsured/fact-sheet/key-facts-about-the-uninsured-population/ http://www.advisory.com/daily-briefing/resources/primers/medicaidmap http://www.cepr.net/index.php/blogs/cepr-blog/today-aca-boosts-voluntary-part-time-employement http://www.nber.org/papers/w19220 http://content.healthaffairs.org/content/34/1/104.abstract http://www.arktimes.com/ArkansasBlog/archives/2013/10/24/more-than-60000-arkansans-have-enrolled-in-the-private-option-for-medicaid-expansion) with commentary to assess how ObamaCare has done over its first implementation year.

I find myself, over and over again, how well ACA implementation is doing in the Blue States that have implemented it enthusiastically–I would have expected at least one more-serious state exchange blowup and something going wrong with costs and competition somewhere. But, instead, the only downward surprise has been the extent to which Red States have been able to nullify implementation–at, I must say, a remarkably large cost to their state economies and to the ability of their governors and legislatures to promote the general welfare…

Morning Must-Read: Joseph Heath: Why People Hate Economics, in One Lesson

We see this strikingly in the many, many right-wing economists who assign moral fault to liberals who don’t free ride, don’t pollute, don’t work hard to externalize as many costs as they can and make others bear them. A doctrine that gleefully assigns positive moral value to being a schmuck is a very odd doctrine to advocate indeed…

…Tabarrok and Cowen are trying to communicate… ‘incentives matter’… a methodological point… [that] should be presented in… as platitudinous [a way] as possible…. There are many ways of doing that, since the problem with the public… is not that they think incentives don’t matter… it’s just that they underestimate the[ir] power of incentives, or they don’t see some of the unexpected ways…. The right way… is to say ‘here’s something that we can all agree upon–but have you thought through the consequences of it? Perhaps not. That’s what economists do.’ But Tabarrok and Cowen are unable to restrain themselves….

[They] present it in a way that makes it seem both morally suspect and politically conservative… set up a contrast between ‘economy’ and morality, with the latter being dismissed somewhat contemptuously as mere ‘sentiment’ (as though people were being tender-minded fools for thinking that there should be moral rules that prohibit killing people…. By buying into Chadwick’s contrast between ‘economy’ and ‘benevolence,’ Tabarrok and Cowen are accepting the narrowest reading of the ‘incentive’ concept, that which identifies it, not just with people’s self-interest, but with their pecuniary interests.

Second, there is the (again somewhat contemptuous) reference to the British parliament passing ineffective ‘regulations.’ The fact that Tabarrok and Cowen use this term, which is anachronistic in the context, shows that they can’t resist getting a little dig in against the left, with its tender-hearted conviction that government can be an effective force for good in the world. But this is not the right place to be doing it… present the foundational ideas of economics in a way that makes them neutral with respect to political ideology…”

Morning Must-Read: Dean Baker: Betting Against Subprime Mortgages Was a Good Thing

As Dean Baker points out, stabilizing financial speculators are an enormous asset to an economy:

Robert Burns Jeff Greene…

…richly deserves to be ridiculed… [for] want[ing] people to get used to lower living standards…. People are wrongly attacking Greene when they complain about his betting against subprime mortgage backed securities…. The securities were in fact bad. Greene betting against them made that clear in the markets somewhat sooner than would have otherwise been the case, bringing down the bubble earlier and more rapidly. This is good… fewer people were caught up in it than if the bubble had continued….

It would have saved people an enormous amount of pain if there had been lots of Jeff Greenes betting against subprime mortgage backed securities in 2003-2004…. Greene was acting out of greed, not a desire to help the economy and society. But this is a case where greed was good…”