Must-Read: Two takeaways this morning from Stan Fischer, and from Tim Duy reading Stan Fischer:

- 1.4%-2% inflation “positive and broadly consistent with price stability” “not in another universe [from 2%]… not a negative number” is the new 2% inflation target.

-

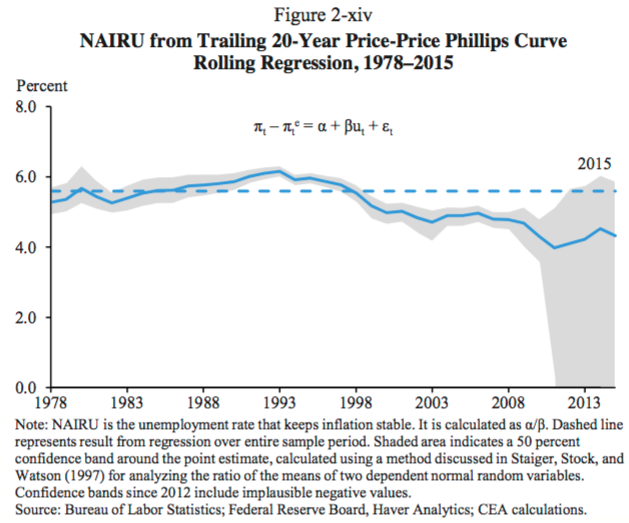

Because the Federal Reserve has no confidence in its ability to nudge the unemployment rate up to its long-run NAIRU level without overshooting and causing a recession, it must always attempt to glide down to the NAIRU from above–and must not follow policies that risk pushing unemployment below the NAIRU, whatever it really is:

Tim Duy and Friends: [Stan Fischer] Resisting Change?](https://twitter.com/TimDuy/status/694715619929780224): https://t.co/2g24mCkTzv

Lance Bachmeier: @kocherlakota009 @TimDuy: “Good post…

…SF/EG (inadvertently?) communicate that 1.5-2% inflation is ‘good enough’ for them.

NRKocherlakota: “@TimDuy Problem: if 2% is the true symmetric…

…target of policy, the FOMC needs a U-Turn, not just a pause: https://sites.google.com/site/kocherlakota009/home/policy/thoughts-on-policy/1-21-16

Tim Duy: “@kocherlakota009 So…

…I don’t really believe the target is symmetric. Need to prove it to me.

NRKocherlakota: “@TimDuy Yes, and I worry that public/markets…

…have your same (reasonable!) doubts. SF’s and EG’s remarks don’t help assuage those doubts.

Lance Bachmeier: “@kocherlakota009 @TimDuy The strange thing…

…is that they’re lowering the [inflation] target after we’ve learned 2% is too low already.

Lance Bachmeier: “@kocherlakota009 @TimDuy I’m not even sure 2% is a ceiling…

…they want to prevent inflation from [even] reaching 2%.

Tim Duy: Resisting Change?: “Stanley Fischer[‘s]… speech… was both illuminating and frustrating…. Although his confidence is fading… he is resisting change…. The first source of my frustration… [is that] his definition of ‘accommodative’ depends upon a specific idea of the neutral Fed Funds rates. From the subsequent discussion:

Well, I think we have to wait to see…. We expect…. somewhere around 3 ¼, 3, 3 ½ percent, which is on average a bit lower than in the past. But we’ll be data-dependent….

If you don’t know the longer-run rate, how can you know how accommodative policy is? If the longer-run rate is close to 2 percent, then policy is less accommodative than you think it is. The endgame of policy is the dual employment/price stability mandate, not a specific level of interest rates…. [That the] Fed’s forecasts… have been foiled by oil and the dollar… would suggest a slower or delayed pace of rate hikes, but more on that later. As for market volatility and external events:

In addition, increased concern about the global outlook, particularly the ongoing structural adjustments in China and the effects of the declines in the prices of oil and other commodities on commodity exporting nations, appeared early this year to have triggered volatility in global asset markets. At this point, it is difficult to judge the likely implications of this volatility. If these developments lead to a persistent tightening of financial conditions, they could signal a slowing in the global economy that could affect growth and inflation in the United States. But we have seen similar periods of volatility in recent years that have left little permanent imprint on the economy.

This is unimpressive…. The likely implications of the volatility are straightforward. The decline in longer term yields signals the Fed is likely to be lower for longer…. It seems that Fischer does not acknowledge the Fed’s role in minimizing the impact of similar bouts of volatility. They have responded by either easing via additional quantitative easing, or easing by delaying tightening…. When you fail to recognize your role, you set the stage for a policy error. They can’t use the logic that they should hike in March because past volatility had no impact on growth when that same volatility actually changed their behavior and thus the economic outcomes. I guess they can use that logic, but they shouldn’t. So is March on the table still?… I can tell a story where they push ahead on the labor data alone. Back to Fischer….

A persistent large overshoot of our employment mandate would risk an undesirable rise in inflation that might require a relatively abrupt policy tightening, which could inadvertently push the economy into recession. Monetary policy should aim to avoid such risks and keep the expansion on a sustainable track….

Policymakers fear that they cannot allow unemployment to drift far below the natural rate because they do not believe they could just nudge it back higher without causing a recession. They can only glide into a sustainable path from above… [thus] the Fed will resist holding rates steady…. Indeed, one voting member is already working hard to downplay recent events. Today’s speech by Kansas City Federal Reserve President Esther George:

While taking a signal from such volatility is warranted, monetary policy cannot respond to every blip in financial markets. Instead, a focus on economic fundamentals, such as labor markets and inflation, can help guard against monetary policy over- or under- reacting to swings in financial conditions. To a great extent, the recent bout of volatility is not all that unexpected, nor necessarily worrisome, given that the Fed’s low interest rate and bond- buying policies focused on boosting asset prices as a means of stimulating the real economy. As asset prices adjust to the shift in monetary policy, it is to be expected that the pricing of risk will realign to this different rate environment…. If we wait for the data to provide complete confirmation before making a policy decision, we may well have waited too long….

Watch for policymakers to downplay the inflation numbers as well. Back to George:

Finally, inflation has remained muted as a result of lower oil prices and the strong U.S. dollar…. Yet… core measures of inflation have recently risen on a year-over-year basis. And although inflation rates… have hovered below the Fed’s goal of 2 percent, they have been positive and broadly consistent with price stability.

Note the ‘positive and broadly consistent’ line. And Fischer:

And our view of progress is what the law calls maximum employment and what we call maximum sustainable employment, and a 2 percent inflation rate. And when we get there—we’re there—we’re very close to there on employment, and on inflation the core number that came out this morning was 1.4 percent. You know, that’s not 2 percent. It’s not in another universe. It’s not a negative number. But inflation’s been pretty stable, and we’d like it to go up.

Not in ‘another universe’ from 2 percent. Not negative. Sure we’d like it to go up, but are we really worried about it? Doesn’t sound like it to me.

Bottom Line…. I suspect market volatility and lack of inflation data keep them on hold in March and maybe April…. However (although not my baseline), I can tell a story where they feel like the employment data forces their hand. Especially so if they continue to downplay the inflation numbers. A substantial part of their policy still appears directed by a pre-conceived notion of ‘normal’ policy. This I think is the Fed’s largest error; the fact that the yield curve stubbornly resists being pushed higher suggests that the Fed’s estimates of the terminal fed funds rates is wildly optimistic. There appear to be limits to which the Fed can resist the global pull of zero (or lower) rates.

{kind=link}