Overview

What is household economic insecurity?

Households are economically insecure when they’re unable to plan for expenses, save or invest for their future economic security, and pay down debts. Household insecurity in the United States can be influenced by differences in income, wealth, credit access, or family structure.

Download File

Household insecurity matters for U.S. economic growth and stability

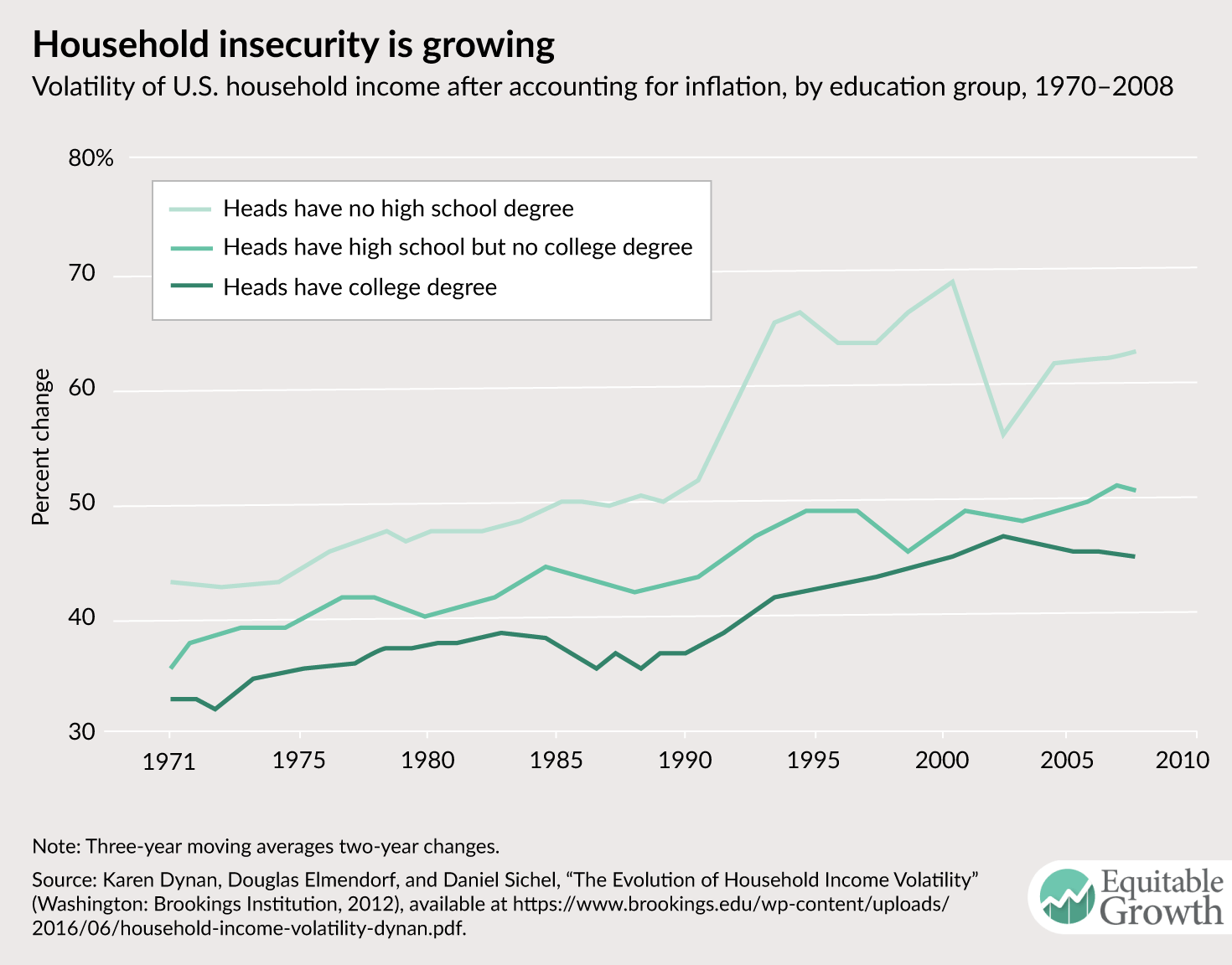

Economists use income volatility as the easiest proxy for household insecurity. Households that experience a gain or drop in income of 25 percent or more from one month to the next or one year to the next can be said to have a volatile income. Large swings in income can make it difficult to plan for expenses, and volatile drops in income increase a household’s likelihood of experiencing insecurity, especially if coupled with low savings (lack of wealth), lack of social insurance, and limited access to credit.

Household income volatility has been increasing for all families, even those with a college-educated head of household. A 2016 Federal Reserve report found that 32 percent of U.S. adults report that their incomes vary from month to month, and 42 percent of those with volatile incomes and/or volatile expenses say that they have “struggled to pay their bills at times because of this volatility.” This insecurity matters, not only for a family’s ability to cope with daily expenses but also has implications for wider economic stability.

Key Takeaways

What are some drivers of household income volatility and potential buffers?

For low- and middle-income households, income from work is the largest source of total household income. Therefore, changes in labor market conditions that impact families’ incomes have significant implications for their economic security such as:

- Alternative work arrangements—including temporary work, contracting, on-call work, and freelancing—mean more variable work hours and income, with less access to benefits that can help smooth volatility such as unemployment insurance.

- Unpredictable work schedules, enabled by “just-in-time” scheduling software, make worker hours and incomes unpredictable and variable, even from week to week.

Savings and access to credit are stopgaps that families can use to fill in the gaps when income is insufficient to meet basic needs such as due to job loss. Specifically:

- Recent research finds that increasing displaced workers’ credit limit allows individuals to take up to 3 weeks longer to find a job, and when they do find work, they receive higher earnings.

- Another recent paper shows the significant decline in the wealth share of the bottom 90 percent of American families over the past three decades, which in turn means they have less savings to fall back on in times of high negative volatility.

Social insurance is another buffer against income volatility, especially from job loss and in the absence of savings and credit. Examples include unemployment insurance and the Supplemental Nutrition Assistance Program.

Why does household insecurity matter for macroeconomic stability?

Household insecurity has implications for how much families decide to consume. Household consumption contributes nearly 70 percent of overall Gross Domestic Product, the largest component of U.S. economic growth. Therefore, maintaining strong consumer demand is important for stable economic growth.

Principles to support household security and macroeconomic stability

Factors that are drivers of household income volatility such as alternative work arrangements are on the rise. Factors that mitigate exposure to risk—such as social insurance programs and family savings—are declining. Therefore, in order to help increase household security and support stable economic growth, we must look for remedies to promote access to stable economic resources and to minimize risk. Some examples of ways to do this include:

- Policies that ensure workers are guaranteed more stable and predictable work schedules, which can help families to better manage expenses and responsibilities

- Policies that support strong labor force attachment such as paid family and medical leave

- Strengthening social insurance programs such as unemployment insurance and SNAP

Explore the Equitable Growth network of experts around the country and get answers to today's most pressing questions!