How would homebuyers respond to a less generous U.S. mortgage interest deduction?

What would happen to U.S. homeownership rates, home sizes, and borrowing levels if tax reform reduces the generosity of the home mortgage interest deduction? A recent working paper examining the economic effects of the mortgage interest deductions in Denmark raises important questions about the appeal of such policies in the United States. The paper, by economists Jonathan Gruber of the Massachusetts Institute of Technology, Amalie Jensen of the University of Copenhagen, and Henrik Kleven of the London School of Economics, finds that the mortgage interest deduction in Denmark has no effect on homeownership but does have a meaningful effect on home size and a large effect on borrowing levels.

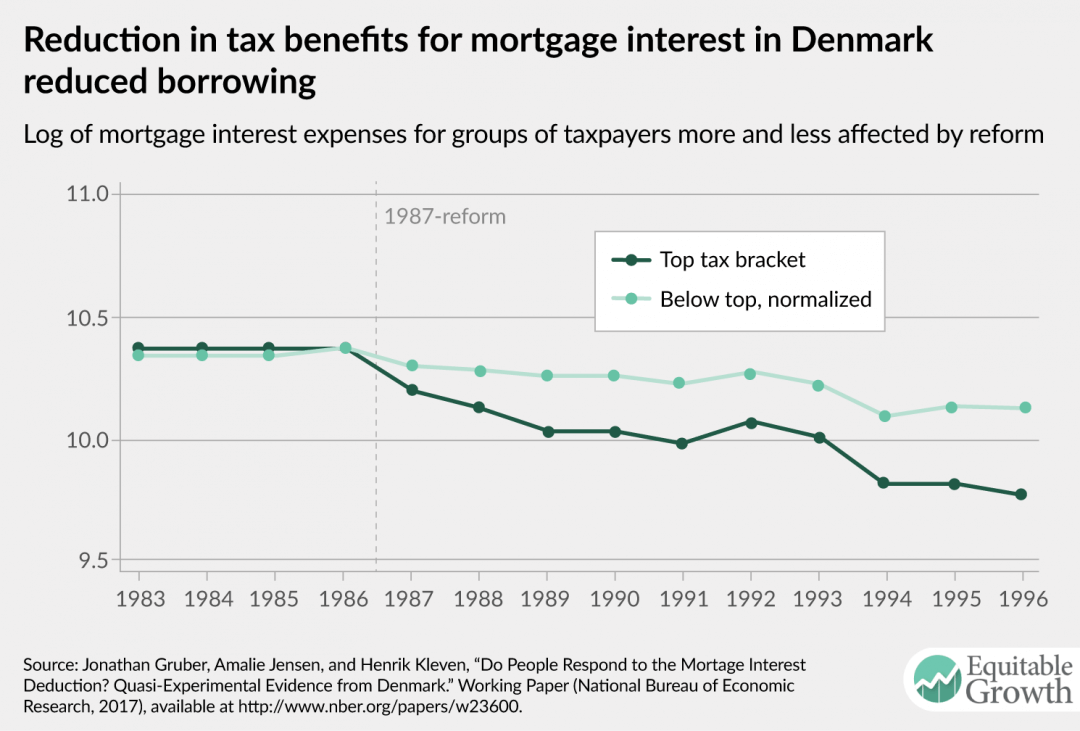

The authors use housing and tax records from Denmark to study the impacts of a 1987 reform. This tax policy change reduced the value of the mortgage interest deduction considerably for top-rate taxpayers, but not nearly as much or not at all for lower-rate taxpayers. They find that affected homebuyers responded most strongly to the subsidy in their financing decisions, reducing total borrowing by up to 20 percent. (See Figure 1.)

Figure 1

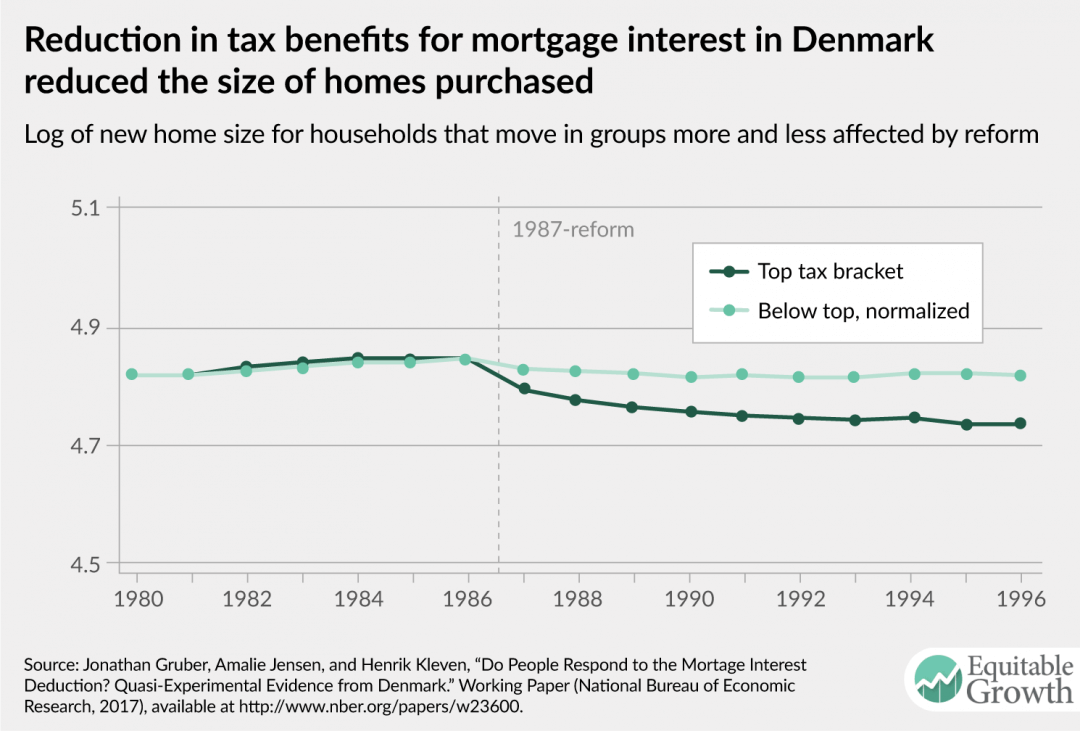

In response to the less generous tax subsidy, homeowners in Denmark reduced the size in square footage and the value of their homes when they moved. (See Figure 2.)

Figure 2

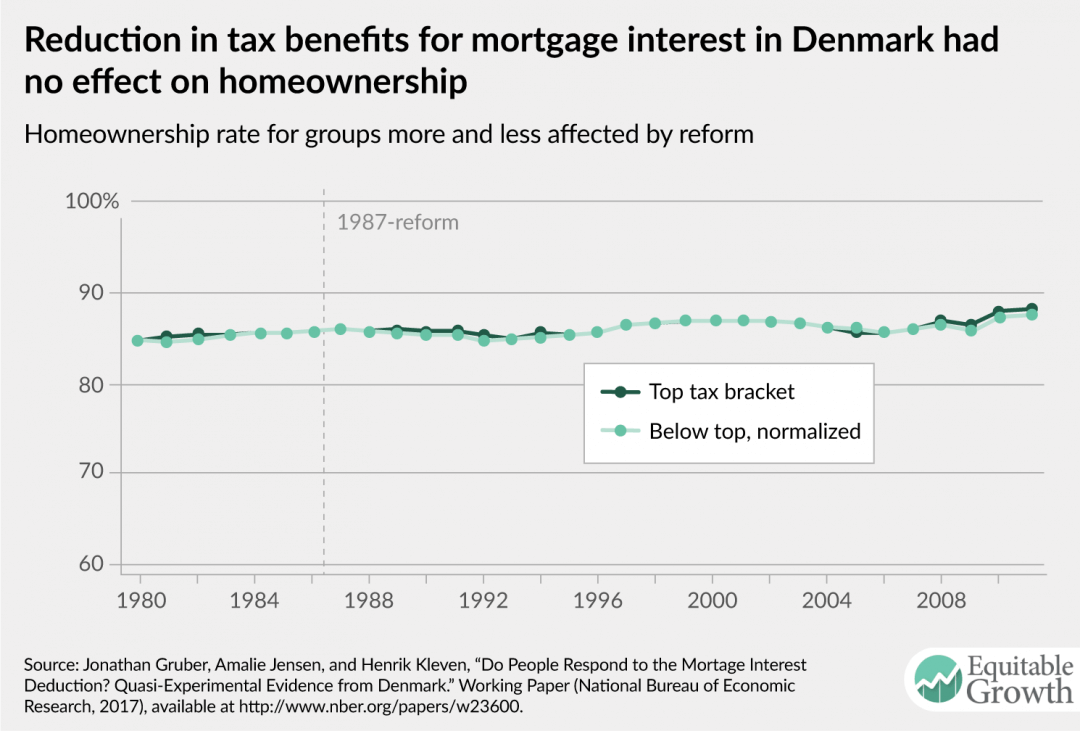

The reform, however, had no effect on the share of households owning a home in either the short or long run. (See Figure 3.)

Figure 3

These findings have important implications for the tax reform debate in the United States. The deductibility of mortgage interest is one of the largest tax expenditures in the U.S. tax code (an estimated $63.6 billion in 2017). Subsidies for homeowners have been primarily motivated by the possibility of positive externalities such as the social benefits of homeownership and greater spending by homeowners on their homes, yet there is no conclusive evidence on the existence of such externalities. As a result, many economists argue that the current policy leads to overinvestments in housing, as well as excessive borrowing by homeowners.

The finding that the tax subsidy has no effect on homeownership, even in the long run, refutes the argument that mortgage interest deductions promote possible positive externalities from homeownership regardless of whether such externalities exist, as the policy has no effect on whether families choose to buy or rent. Furthermore, the subsidy—at least as currently implemented in the United States—is inequitable because, among other reasons, high-income households tend to have greater mortgage debt and thus benefit more from the tax subsidy.

Policymakers may well have a chance to consider reforming the federal mortgage interest deduction in the coming months. Denmark’s experience with reform should be part of the debate.