What have we learned about geographic cross-sectional fiscal multipliers?

The limits of monetary policy during the Great Recession pushed fiscal policy back to the forefront of macroeconomic policy discussions in the United States. Yet empirical estimates of the effects of fiscal policy vary. Two main challenges dominate economic thinking. First, fiscal policy can respond to a changing economic trajectory, as when the American Recovery and Reinvestment Act of 2009 increased spending precisely because unemployment was already rising. Second, changes in spending often coincide with changes in taxes or other policies. Both challenges mean that the naïve relationship between government spending and subsequent outcomes may not measure the true causal impact.

The past several years delivered up a wave of new research using geographic variation in spending to better understand the employment and output effects of fiscal policy. By definition, a geographic cross-sectional fiscal multiplier uses variation in fiscal policy across distinct geographic areas within a single period of time to measure the effect of an increase in spending in one region in a monetary union. This cross-sectional approach has the advantage of identifying much greater variation in policy across space than over time, and variation more plausibly exogenous with respect to the no-intervention paths of outcome variables.

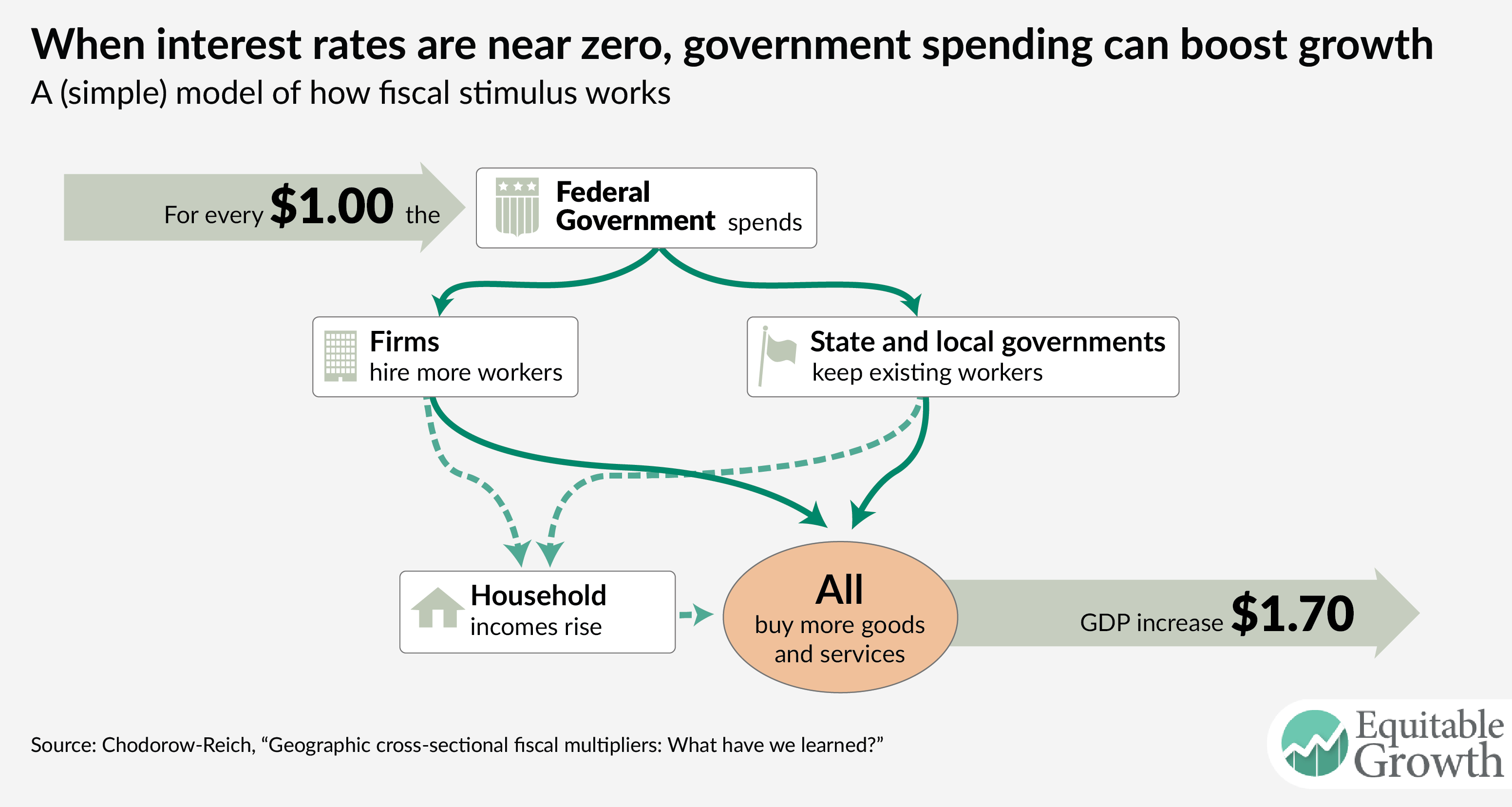

In a new review paper, I assess what we have learned from this research wave. I conclude the cross-sectional evidence implies a national multiplier of about 1.7 or above when monetary policy is constrained. This magnitude falls at the upper end of the range suggested by earlier studies using time series variation only, and suggests that fiscal policy can play an important role in the management of business cycles when monetary policy has reached its limits. (See Figure 1.)

Figure 1

An example based on three papers studying the effects of the Recovery and Reinvestment Act makes clear the meaning of a cross-sectional multiplier. These papers exploit variation in the non-discretionary, formulaic component of the distribution of ARRA funds, due to factors such as pre-recession Medicaid spending or the number of lane miles of federal highway. I combine the spending variation in the three studies and use updated employment data and new state output data to estimate cross-sectional instrumental variable regressions of the cumulative increase in employment and output during 2009 and 2010 as a function of ARRA spending in a state. I find a cross-sectional “cost per job” of roughly $50,000 and output multiplier of roughly 1.75.

A review of the recent empirical literature broadly confirms the lessons from this example. One strand of this literature examines various components of the Recovery Act. The cost-per-job across these studies ranges from roughly $25,000 to $125,000, with around $50,000 emerging as a preferred number. Using a production-function approach, this magnitude translates loosely into an output multiplier of about 2. Another set of recent papers uses variation from historical episodes or other countries, many quite creatively. The diversity of outcome variables and policy experiments makes reaching a synthesized conclusion across these studies harder. Nonetheless, those papers that estimate a cost-per-job find numbers of around $30,000, and (with one or two notable exceptions) those which estimate income or output multipliers find numbers in the range of 1.0 to 2.5.

Research into the mapping between cross-sectional multipliers and national multipliers also has advanced. Three main differences can arise, depending on who pays for the spending, what monetary policy does, and the different openness of regions and the country as a whole.

Starting with the first, in many cross-sectional multiplier studies the spending does not affect the present value of local tax burdens, for example, because the spending is paid for by the federal government. Standard economic theory, however, suggests that such outside financing can have a small effect on local output. Fully rational, forward-looking, liquidity unconstrained households (sometimes denoted as so called “Ricardian agents”) will increase their private spending by only the annuity value of the outside transfer, which for transitory spending implies a small increase relative to the direct change in government purchases, while spending by fully “rule-of-thumb” or “liquidity-constrained” agents does not depend at all on the present value of the tax burden. In either case, the fact that the financing of the spending comes from outside the region adds little to the local private-spending response.

Monetary tightening in response to higher spending may reduce the output impact. Therefore, cross-sectional multipliers best help to characterize national multipliers when monetary policy is constrained, for example, by a zero lower bound on interest rates. Finally, expenditure switching and import leakage exert a downward influence on regional multipliers relative to the aggregate multiplier.

Combining these three arguments, the cross-sectional multiplier offers a rough lower bound for a national multiplier as long as the spending is relatively transient and monetary policy is constrained. These conditions appear likely to hold in many empirical settings, including during the implementation of the Recovery Act.

Combining the empirical evidence and the recent theory, the cross-sectional studies suggest a closed economy, constrained monetary policy, deficit-financed multiplier of about 1.7 or above. This magnitude falls at the upper end of the range suggested by earlier studies using time series variation only.

The cross-sectional literature and my review essay have focused their attention most on understanding what cross-sectional multipliers imply about national multipliers. Other lessons also emerge. Foremost, many of the cross-sectional studies test for and find evidence of higher multipliers or less crowd-out in regions and periods with more unused resources. These results suggest multipliers may be larger during downturns and for reasons beyond constraints on monetary policy.

I conclude this summary with a comment on research practices. In the wake of the Great Recession of 2007-09, many have criticized the economics profession and macroeconomists in particular. The foray into cross-sectional multipliers offers a positive example of economists directing their research toward understanding newly relevant policy levers. Necessarily, the effort involved both empirical and theoretical advances. As a result, I believe we have a better grasp of the efficacy of fiscal policy than we did before the Great Recession started.

— Gabriel Chodorow-Reich is an assistant professor of economics at Harvard University. His research focuses on macroeconomics, finance, and labor markets. His working paper upon which this column is drawn can be found here.