False promises about corporate taxes and American workers

Republicans in Congress and in the Trump administration have turned to tax reform, touting it as crucial for investment, job creation, and economic growth that will benefit American workers. While most policymakers agree that tax reform is overdue, true reform seems far less likely than poorly designed corporate tax cuts, and economic research shows that the results from such tax cuts are likely to be deeply disappointing to American workers. The benefits from these corporate tax cuts would accrue to corporate shareholders and senior managers—the same groups that have prospered the most in recent decades, while wages for middle-class Americans have stagnated.

If policymakers actually want to help American middle-class workers with tax cuts, they should simply direct those tax cuts to the taxes these workers pay. Income and payroll taxes are by far the dominant source of workers’ federal tax payments. There is no question that workers pay nearly all payroll and labor income taxes, including the portion of the payroll tax ostensibly paid by employers since workers pay for the employer portion of the payroll tax in the form of lower wages.

How would corporate tax cuts affect the middle class? For corporate tax cuts to benefit workers, the resulting increase in corporate after-tax profits would need to fuel new investments, those new investments would need to increase the productivity of labor, and the higher productivity would need to boost wages. But why rely on indirect mechanisms to help workers when we have far more direct tools? If the aim is to help workers, then policymakers should go straight to the taxes that fall on them. Workers would get nearly 100 percent of payroll and labor income tax cuts.

Research shows that corporate tax cuts are far more likely to end up in the hands of those at the top of the income distribution. All major models from the Joint Committee on Taxation, the Congressional Budget Office, the U.S. Department of Treasury, and the nonpartisan Tax Policy Center put the vast majority of the corporate tax burden on capital or shareholders. And there is little to no empirical evidence that corporate tax cuts increase investment and wages across countries; research suggesting as much has rarely found a place in peer-reviewed publications, and early implausible results have been subsequently questioned or overturned.

Further, much of the U.S. corporate tax base at present is excess profits, which are profits above the normal level accruing due to intangible sources of economic value and market power. U.S. Treasury economists now calculate that three-quarters of the corporate tax base is excess profits, often in the hands of very few superstar companies. Giving a tax cut to this part of the tax base just makes excess profits even larger, without stimulating capital investment or wages.

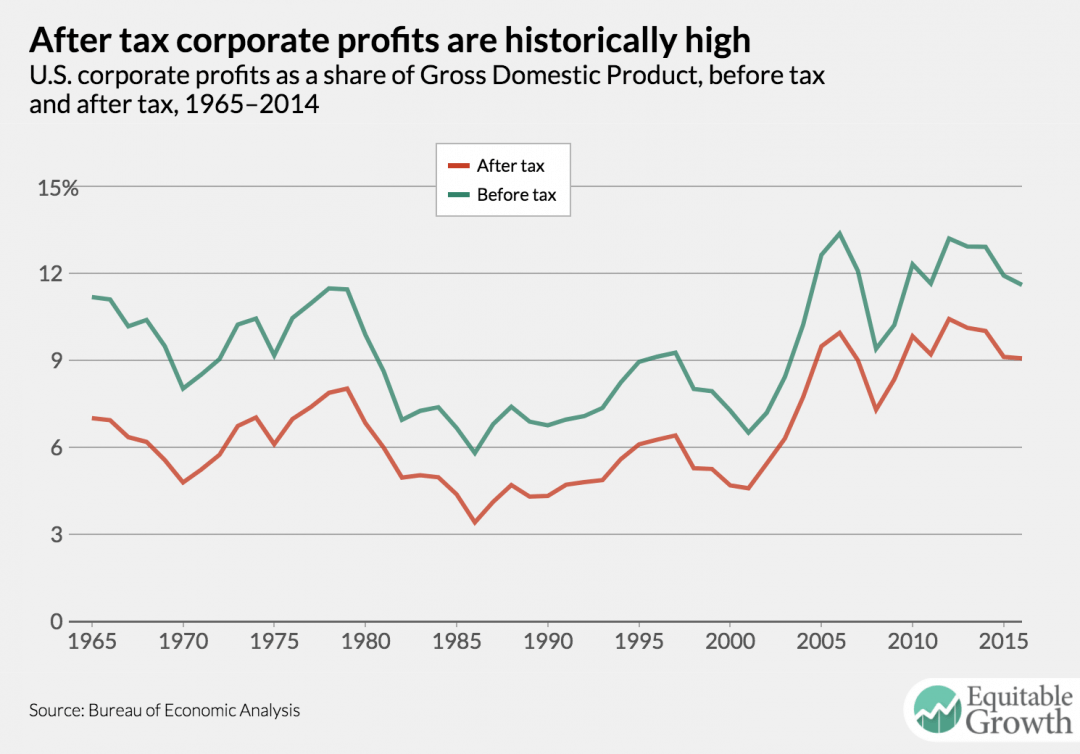

If burgeoning corporate after-tax profits were the key to investment and wage growth, then the previous 15 years should have been a paradise of wage growth, as after-tax profits in recent years have been about 50 percent higher than in decades prior (as a share of Gross Domestic Product), and higher than at any point in the past half-century. (See Figure 1.)

Figure 1

Are policymakers really to believe that low after-tax profits are the key economic problem that tax reform should address? Those arguing for corporate tax cuts typically cloak their arguments under the guise of competitiveness. But this is nonsense. Our multinational companies are the most competitive on the planet. The United States has a disproportionate share of the Forbes 2000 list of global companies, and after-tax profits are at record levels. Further, our multinational companies are so skillful at exploiting loopholes to lower their tax bills that they often achieve effective tax rates in the single digits. Business tax reform should not lower tax collections from the country’s corporations—collections that are already 1 percent of GDP lower than corporate tax collections in other countries.

To be clear, there is a pressing need for corporate tax reform. Such reform could lower headline rates somewhat if policymakers were serious about protecting the corporate tax. Evidence suggests that the U.S. government is probably losing more than $100 billion each year due to corporate profit shifting to tax havens, and a similar amount of revenue is being lost as business activity moves into pass-through form. This leaves a lot of room for true tax reform to simultaneously close loopholes and lower rates. But the rates that have been suggested—rates as low as 15 percent or 20 percent—would not deliver substantial economic benefits for the middle class and would instead result in huge revenue losses for the federal government and a much lighter tax burden for those at the top of the income distribution. Further, there is no indication that these proposals will be serious about corporate tax-base protection.

So far, tax cuts seem to be far more important to Republican policymakers and the Trump administration than tax reform, and the planned tax cuts are heavily skewed toward those at the top at the expense of future generations of taxpayers. To help middle-class workers, give them the tax cuts, and keep business tax reform—and tax reform as a whole—at least revenue neutral.

— Kimberly Clausing is the Thormund A. Miller and Walter Mintz Professor of Economics at Reed College.